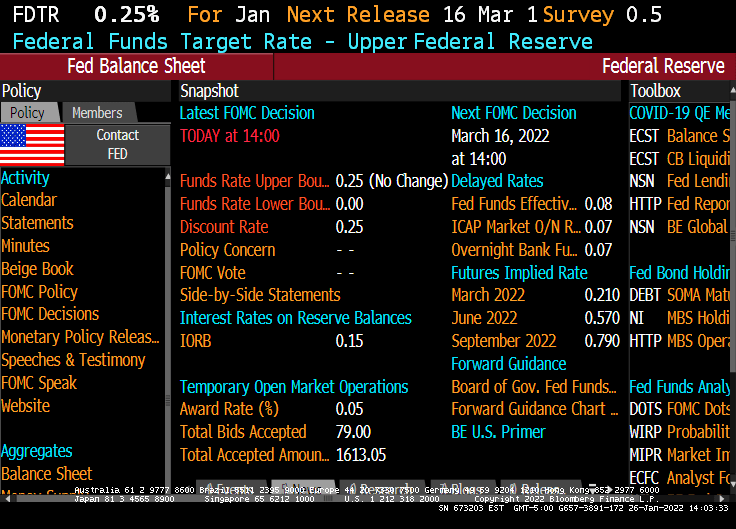

Yes, The Federal Reserve could have raised their target rate at their January meeting, but chose not to raise rates. Instead, Chairman Powell said that rate increases are a comin’!

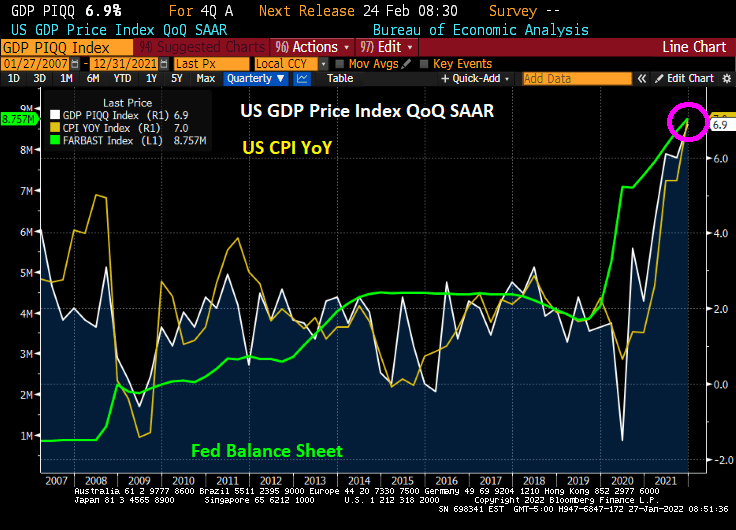

I hope Powell wasn’t hoping for a slowdown in inflation, because today’s Q4 GDP report showed a surge in GDP to 6.9% QoQ. But with that GDP surge we also got a surge in prices paid by consumers to 6.9% as well. Thanks to the continuing massive Federal stimulus being poured into markets.

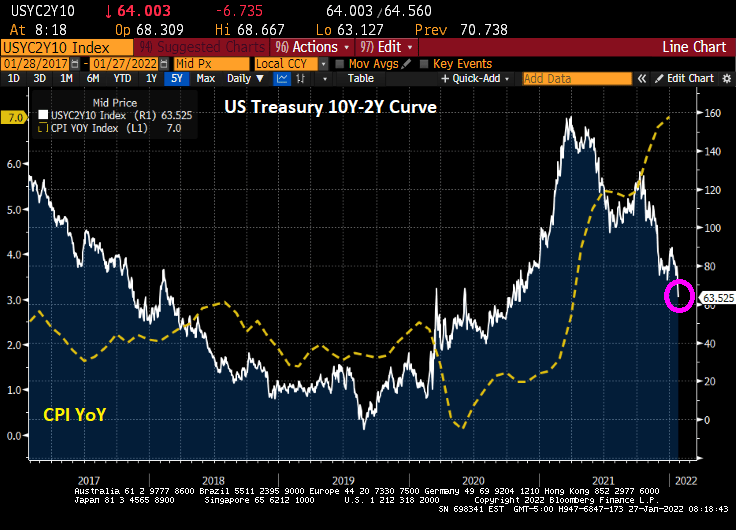

Despite the positive news on Q4 GDP, we are still seeing 7% inflation and a diving 10Y-2Y yield curve.

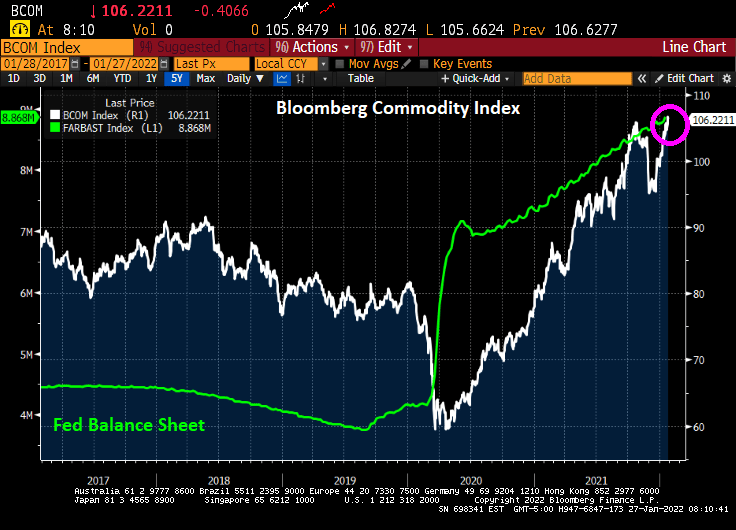

Along with that surprising GDP report, we are seeing the Bloomberg Commodity Index rising like a bat out of hell (RIP, Meatloaf).

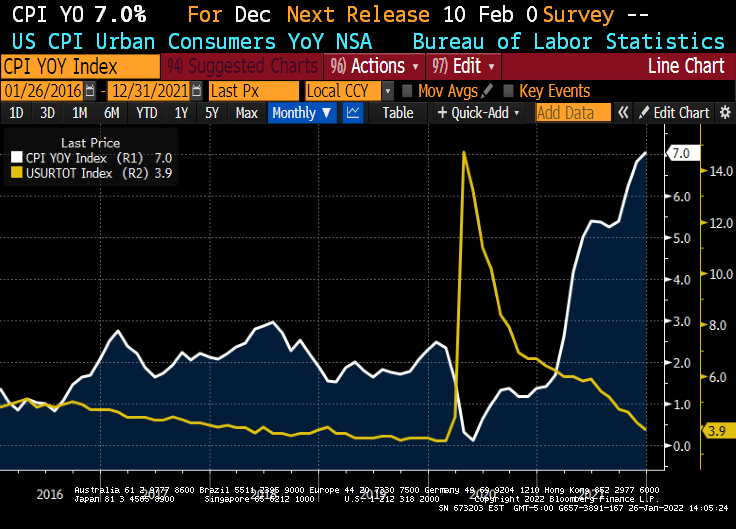

Despite inflation growing at 7% (versus The Fed’s target rate of 2%) and U-3 unemployment being only 3.9%, one would have thought that Jay and The Gang would have started increasing rates at the January meeting.

But nooooo. The Fed actually sat on their hands and did nothing.

What did The Fed say?

“The Committee seeks to achieve maximum employment and inflation at the rate of 2 percent over the longer run. In support of these goals, the Committee decided to keep the target range for the federal funds rate at 0 to 1/4 percent. With inflation well above 2 percent and a strong labor market, the Committee expects it will soon be appropriate to raise the target range for the federal funds rate. The Committee decided to continue to reduce the monthly pace of its net asset purchases, bringing them to an end in early March. Beginning in February, the Committee will increase its holdings of Treasury securities by at least $20 billion per month and of agency mortgage‑backed securities by at least $10 billion per month.“

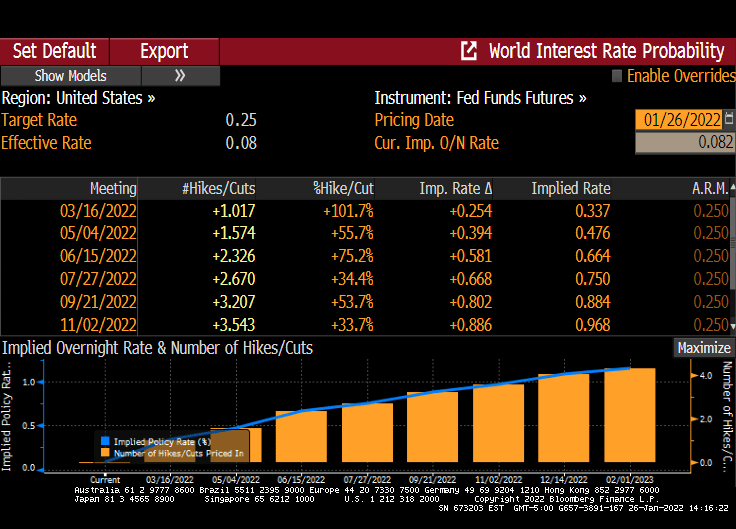

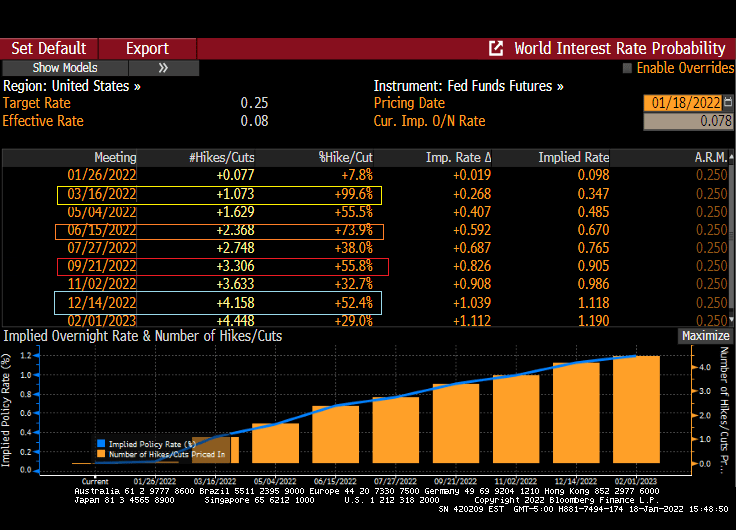

According to The Fed Funds Futures data, the market is anticipating 1 rate increase at the March FOMC meeting. And another at the June FOMC meeting.

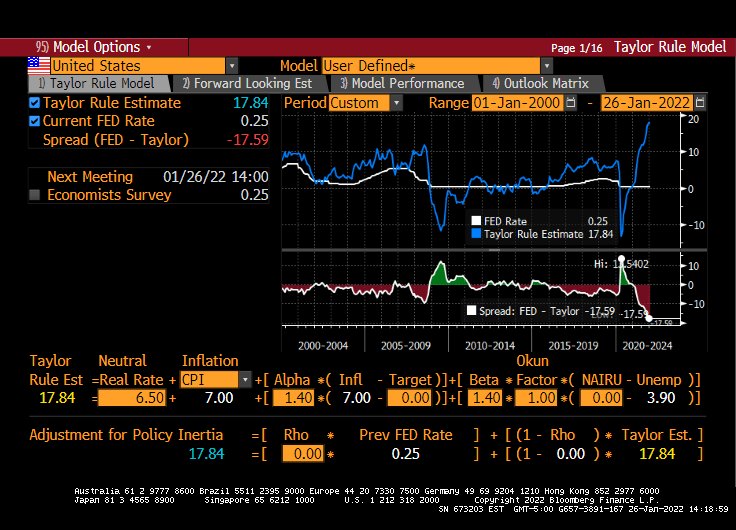

The Taylor Rule (not used by Jay and The Gang), suggests that The Fed should have their target rate at almost 18%! NOT 0.25%.

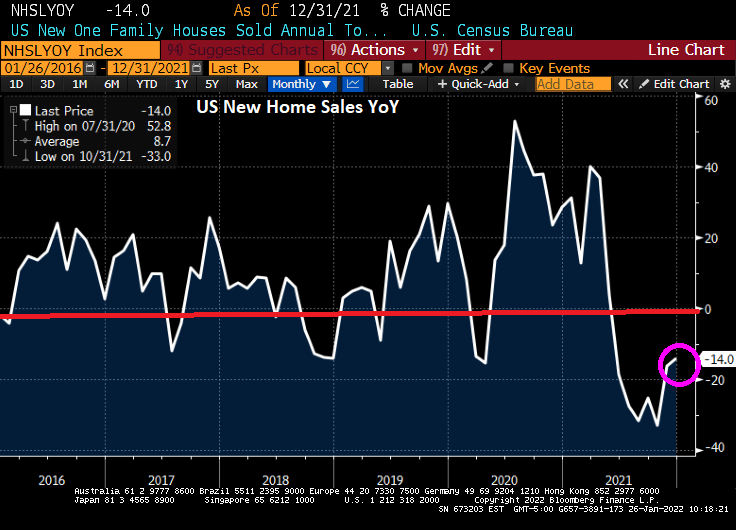

US new home sales spiked in December by 11.9% from November, but were down 14% year-over-year.

But the median price of new home sales (YoY) declined to 3.4%.

The Midwest saw a surge in new home sales (+56%).

The MBA’s mortgage applications index shows declining purchase applications (-1.83%) and declining refinancing applications (-12.60%) as mortgage rates increased from 3.64% to 3.72% for the week of 01/21.

Now, mortgage purchase applications rose for the week of 01/21 if we used non-seasonally adjusted data.

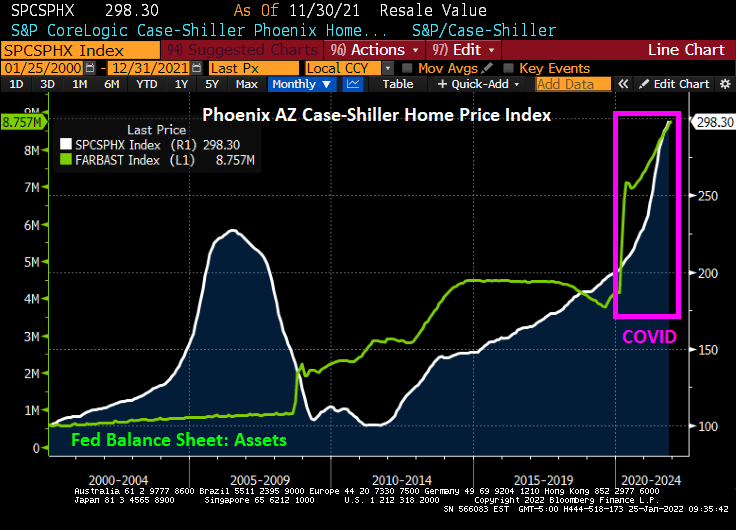

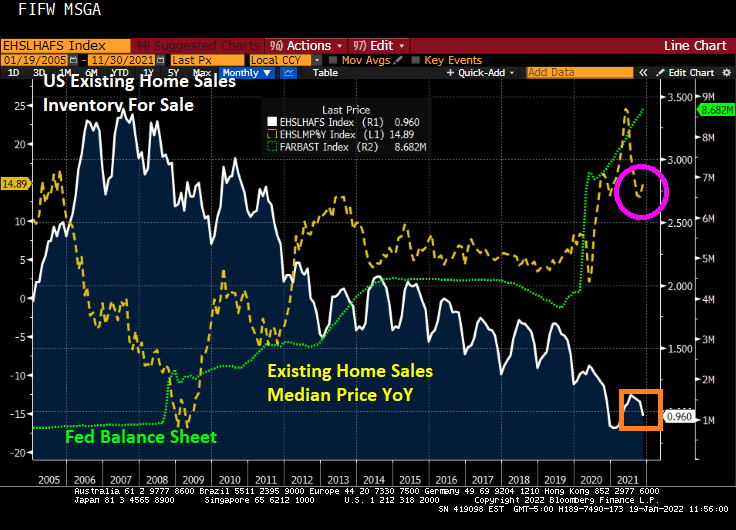

The Case-Shiller National home price index “slowed” to 18.81% YoY in November as The Fed continues its monetary stimulypto. Notice that The Fed is easing even when there is limited inventory available. Result? Hideous home price inflation.

Which metro area is growing the fastest, making housing even more unaffordable for renters? Phoenix AZ is growing at a 32.2% YoY clip while Washington DC is the slowest growing metro area at 11.1% YoY. The second faster growing metro area in Tampa FLA.

Phoenix AZ is growing at the fastest rate in the nation as The Fed still has its monetary stimulus at FULL SPEED AHEAD.

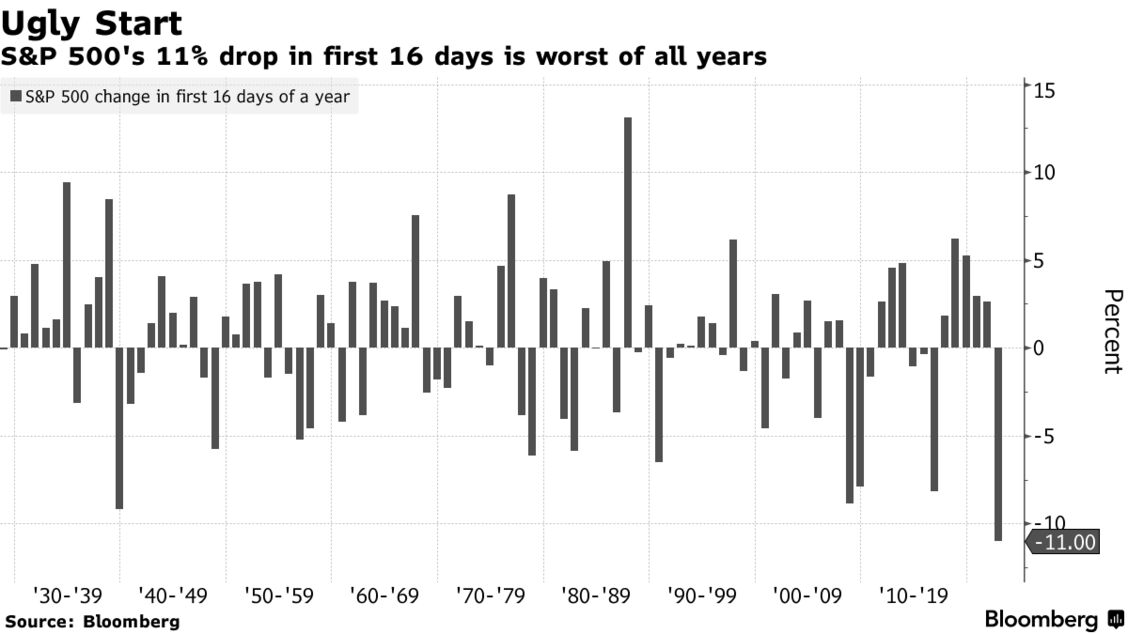

The stock market has never started a year falling as quickly as it is now.

The S&P 500 has dropped 11% — heading into correction territory — in the first 16 trading days of 2022 in its worst-ever start to a year, according to Bloomberg data that goes back over nine decades.

The downturn comes as traders brace for the Federal Reserve to tighten monetary policy and a surge in U.S. Treasury yields weighs on the outlook for stocks. A host of technical signals also suggest that more volatility may be coming up ahead.

“The Fed pulled the punchbowl, liquidity has evaporated, and the S&P and NDX broke below their 200dma for the first time since the Covid outbreak,” said Rich Ross, technical strategist at Evercore ISI.

A bear market down to the 3,800 level is likely for the S&P 500, Ross said, given “the dramatic erosion of the technical backdrop, in conjunction with the highest inflation, tightest policy, and most uncertain political and geopolitical condition in years” — not to mention its historic rally since 2020.

The Shiller CAPE ratio is extremely high …. not surprising how much air The Fed pumped into the market tires.

Is this the bubble burst many were expecting once The Federal Reserve starting raising rates?

Well, if today’s market opening is an indication, the answer is yes. The NASDAQ Composite Index is down 1.36% and West Texas Intermediate Crude Oil futures prices are down 2%.

The S&P 500 index is down over 10% since January 3rd.

Drawdown is taking place.

But if you think the US equities are deflating, look at European equities. The Euro Stoxx 50 index is down 4.04%.

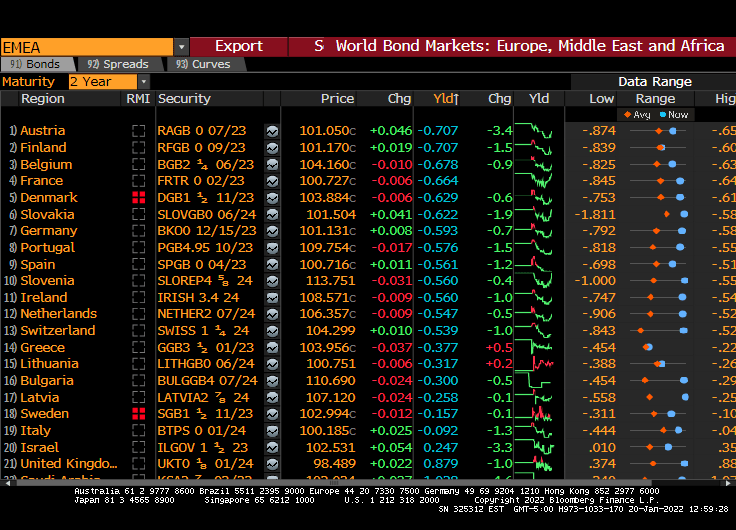

Let’s see how The Federal Reserve is going to compete with other central banks when 19 European nations have negative 2-year sovereign yields. Call them the “Nervous 19.” Note that France has the lowest 2Y yield of the big 3 (France -0.664%, Germany -0.593% and Italy -0.092%).

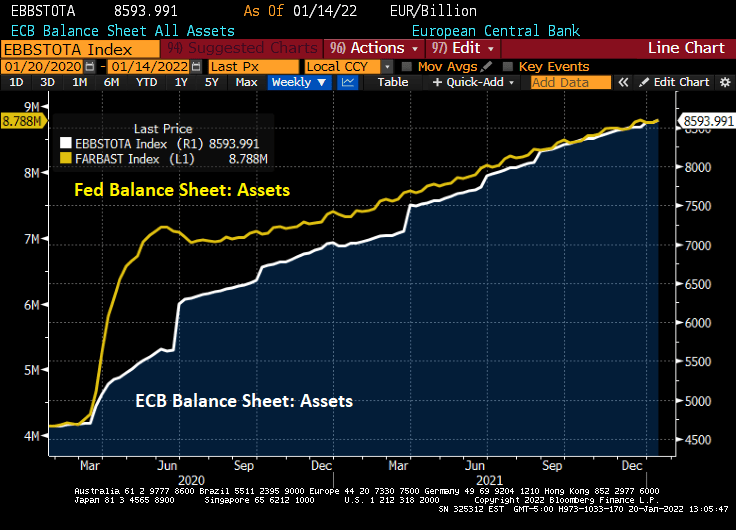

True, The Fed’s reaction to COVID shutdowns was more extreme than the ECB’s reaction.

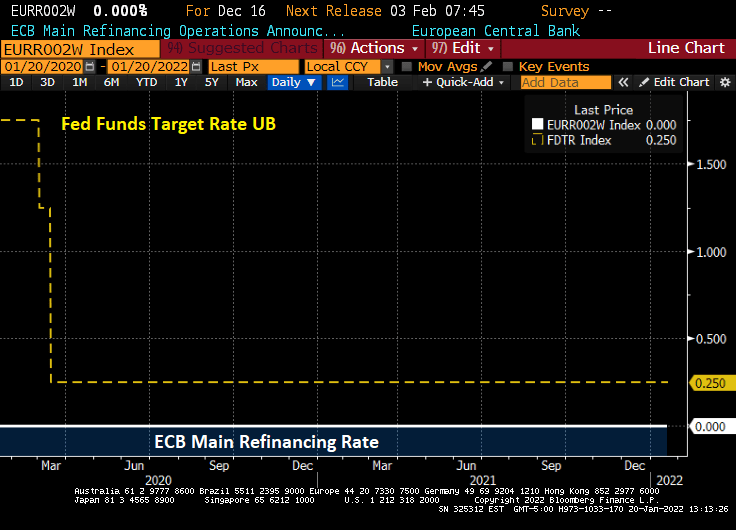

The ECB’s main refinancing rate is 0% and The Fed’s target rate is 0.25%.

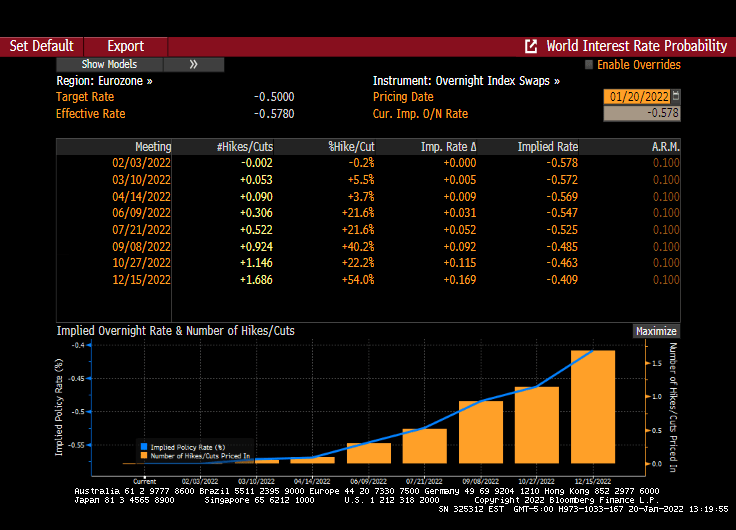

Unlike the US with its 4 expected rate increases, the Eurozone is pricing in only 1 rate increase for 2022 … in October.

The ECB’s monetary policy is as stiff as French President Emmanuel Macron.

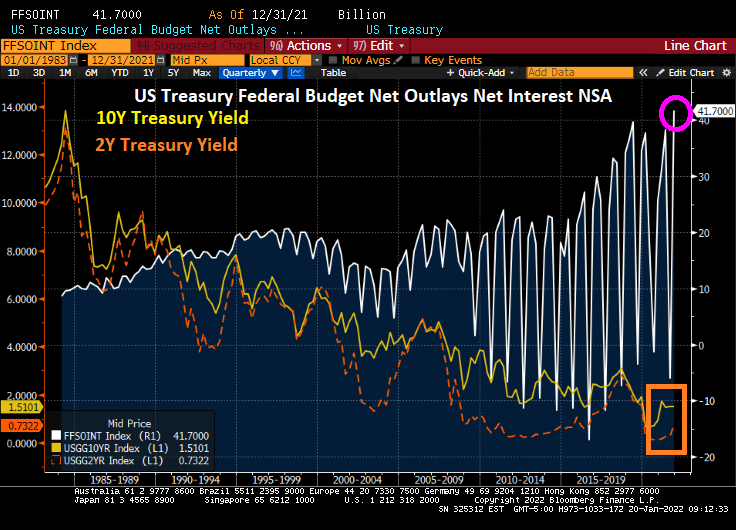

Treasury Secretary Janet Yellen is having trouble with the curve (yield curve, that is). It keeps inching up, meaning that Treasury’s cost of debt financing is inching up too.

As Treasury yields keep rising, so does the problem of financing the massive Federal debt load. Here is a chart showing the interest outlays in the Federal budget against the cost of Federal funding at the 10-year and 2-year tenors.

Now, The Fed is predicted to raise their target rate 4 times in 2022 (according to Fed Funds Futures data) and it looks like a whopping 100 basis points (or 1%). Holding the rest of the yield curve constant, this will considerably flatten the 10Y-3M Treasury curve. Resulting in a more expensive refinancing of the Federal Debt load.

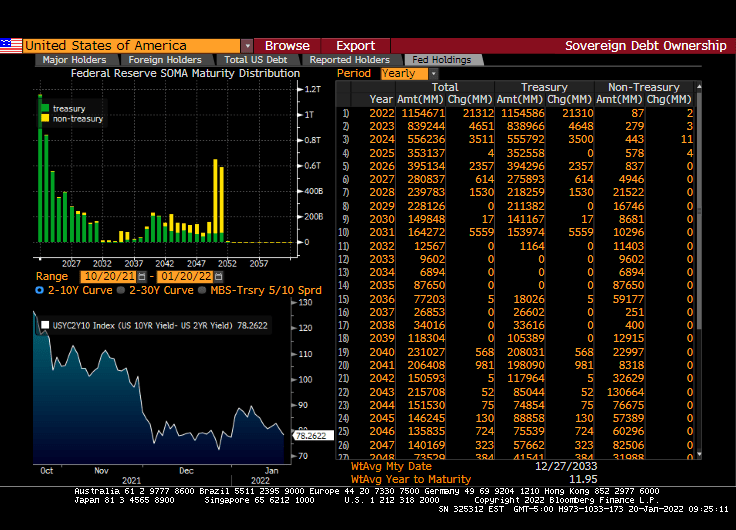

If we look at The Fed’s System Open Market Holdings (SOMH), we can see that The Fed’s holdings are primarily Treasuries with non-Treasuries (primarily agency mortgage-backed securities) not maturing (or running off) until 2050.

The majority of The Fed’s COVID expansion was picked-up by The Fed (light blue line).

How about the Treasury Inflation-protected Securities curve? Negative yields across the tenor range.

With Congress trying to spend trillions more (since Build Back Broke failed, Democrats are producing MORE spending legislation with the voting act included, of course), Treasury is going to have progressively more trouble with the (Treasury) curve.

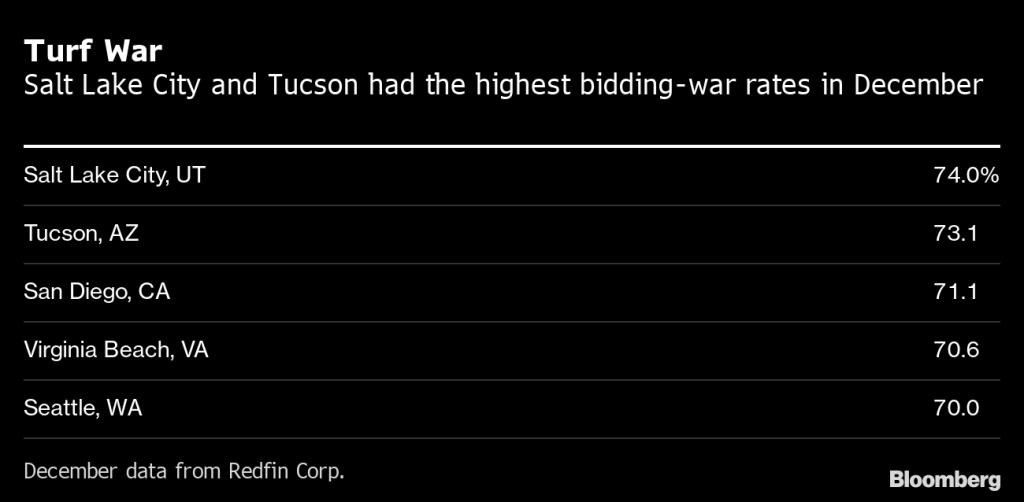

Massive Federal stimulus (both fiscal and monetary) have led to bidding wars among the wealthiest Americans. Despite clamoring for The Fed to increase rates and speed-up the shrinking of The Fed’s balance sheet, nothing has happened … yet.

(Bloomberg) — Home buyers willing to spend almost a $1 million are competing the most for a piece of the red-hot U.S. housing market.

Homes priced between $800,000 and $1 million saw the highest rate of bidding wars at 64.6%, followed by 62% for homes between $1 million to $1.5 million and 61.7% for homes above $1.5 million, according to December data from Redfin Corp.

“Buyers should anticipate that they may not win a house until their sixth or seventh bid,” Candace Evans, a Redfin team manager in New York, said in a statement. “If you’re the type of person who falls in love with a house, this is not your market.”

Salt Lake City had the highest bidding-war rate of 37 U.S. metropolitan areas analyzed, with 74% of offers facing competition in December, the firm said. Tucson had a 73.1% bidding-war rate and followed by 71.1% for San Diego.

Prospective buyers are competing for homes as relatively cheap mortgage rates and a proliferation of remote-working opportunities in the wake of the Covid-19 pandemic boost demand for homes in smaller cities. The number of available homes in several of the hottest markets continue to shrink.

Nearly 60% of home offers written by Redfin agents across the U.S. faced competing bids in December, the firm said. It was the lowest rate in 12 months but an increase from 54% in December 2020 as pandemic-driven demand for housing remains strong.

Vacation homes, which are often pricey and have increased in popularity due to Covid-19, may have contributed to bidding wars in the high-end market, Redfin said. Townhouses had a bidding-war rate of 62% followed by 61.3% for single-family homes, the firm said.

Now its a race against the clock as potential home buyers try to beat Powell and the Gang as they raise mortgages rates.

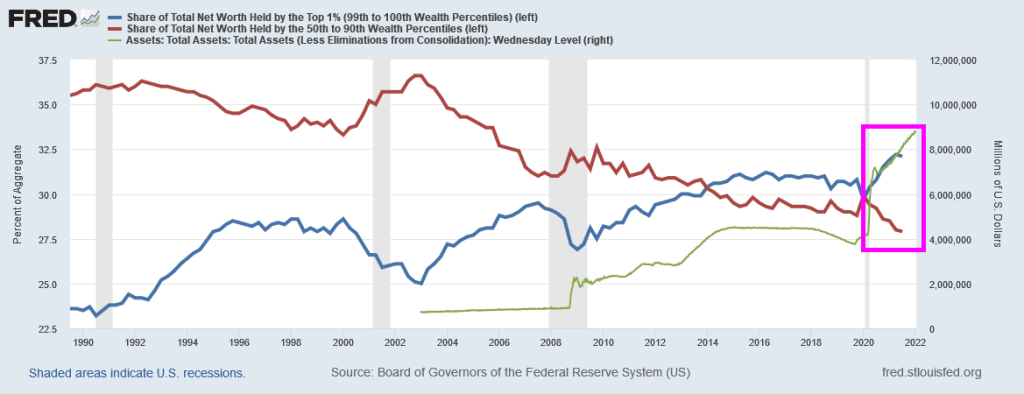

Yes, Federal stimulus has made the top 1% increase their share of total net worth that includes $800,000+ homes.

The 10-year Treasury Note yield rose to 1.869% this afternoon as Freddie Mac’s 30-year mortgage commitment rate rose to 3.45%.

And if you like The Fed Funds Futures data, it is pricing in 4 rate hikes by The Fed (March, June, September and December). For a grand total of … 100 basis points or 1%.

By keeping rates soooo low for soooo long, The Fed has committed a serious policy error. Or as Kevin Malone calls it, “The Fed’s Famous Chili!”

You must be logged in to post a comment.