In August 2020, the Federal Reserve unveiled its new strategic framework. One major objective of the Fed was to address its concerns over the potential consequences for the conduct of monetary policy when the policy rate was constrained by its effective lower bound. This article concludes that there are significant flaws in the new strategy and that it encourages a more discretionary approach to monetary policy and increases the risks of policy errors. The new framework is an overly complex and asymmetric flexible average inflation targeting scheme that introduces a significant inflationary bias into policy and expands the scope for discretion by broadening the Fed’s employment mandate to “maximum inclusive employment.” In a postscript, the article describes how quickly the flaws have been revealed and urges a reset toward a more systematic and coherent strategy that is transparent and broadly understood by the public.

I attended a speech by macoeconomist Gershon Mandelker at the National Association of Realtors where he called on the Federal Reserve to follow some observable rule rather than the complex (or seat of the pants) approach to monetary policy.

With today’s inflation report (core inflation YoY of 6%) results in a Taylor Rule estimate of The Fed Funds Target Rate of 12.07%. We are struggling to reach 5% as a “terminal” Fed target rate (currently at 4% and likely to rise 50 basis points at tomorrow’s Fed meeting).

The matrix of CPI and unemployment under the Taylor Rule shows that The Fed’s target rate isn’t at even 5% for any relevant combination of core CPI (inflation) and unemployment rate.

Note that since the financial crisis the Fed’s target rate (white line) has been consistely below the Taylor Rule implied rate (blue dashed line).

This will be the last time (Fed rate hikes) as the US economy is forecast to either go into a recession in 2023 or slow down to an anemic 1.20% Real GDP YoY. Even the Fed is forecasting 3.10% core inflation in 2023, still higher than their target rate of 2%.

One of the sectors that is suffering is commercial real estate.

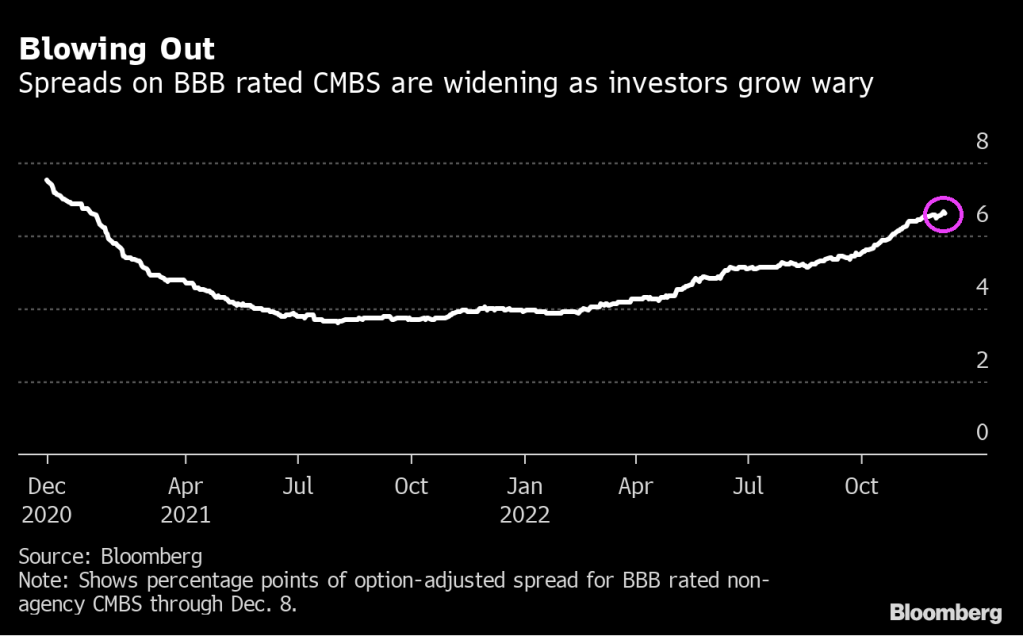

Commercial mortgage bonds could get clobbered in the coming months, and investors are backing away from the securities.

Some $34 billion of the bonds come due in 2023, and refinancing property loans is difficult now. Property prices could fall 10% to 15% next year, according to JPMorgan Chase & Co. strategists. And some types of properties seem particularly vulnerable as, for example, city workers are slow to come back to their offices full time.

That may be why spreads on BBB commercial mortgage bonds have widened by about 2.7 percentage points this year through Thursday to around 6.6%, for the securities without government backing. They are now at their widest since January 2021. They’ve been getting hit particularly hard in the last few months, even as risk premiums on investment-grade and high-yield corporates have been shrinking on hopes the Federal Reserve will scale back its tightening campaign.

“For CMBS investors, there’s lots of uncertainty, especially around whether maturing loans are going to get refinanced or not, and if not, what the resolution will be,” said David Goodson, head of securitized credit at Voya Investment Management, in an interview. “Layering in risk from lower office utilization makes the assessment even tougher.”

The trouble that the bonds face won’t necessarily translate to a surge in defaults in the near term, which is part of why betting against them is so difficult. When property owners can’t refinance mortgages that have been bundled into bonds, noteholders have a difficult choice to make. They can seize the buildings and liquidate them, or they can extend the debt and accept repayment later. They usually go for the second option.

Extending maturities allows bondholders to kick the can down the road and potentially recover more later, said Stav Gaon, head of securitized products research at Academy Securities. The question is whether properties have permanently lost value as, for example, people reorder their lives after the pandemic, or whether declines may be more temporary because of higher rates.

“Foreclosing on a loan, rather than granting an extension, can be really messy — that’s a lesson that was learned during the great financial crisis,” said Gaon. “The lenders also recognize that today’s higher interest rates are a very sudden development that many high-quality borrowers need time to adjust to.”

Some investors that are still buying are focusing on higher-quality borrowers and properties, that are likelier to withstand any downturn in real estate prices without having to seek extensions on loans.

“We think trophy properties will fare better due to better access to the debt markets, lower potential property declines, and a continued tenant flight to quality,” said Zach Winters, senior credit analyst at USAA Investments.

He acknowledges that this strategy isn’t always popular now, even if it turns out to make sense.

“When we go out and bid on a bond tied to a trophy office building now, usually the number of buyers is significantly less than before,” Winters said.

After the Pandemic

The market for commercial mortgage bonds without government backing was about $670 billion as of the end of 2021, and although the securities soared in the second half of 2020 as the Fed opened the money spigots, they’re facing more difficulty now. With office occupancy still below 50% in many cities as more people work from home, corporate buildings may see their values drop. Retail space is similarly under pressure as consumers have grown used to buying more online. And while travel volume is rising, many hotels are struggling to reach 2019 levels for room charges.

A survey of institutional real estate market professionals in November found that firms expect office values to fall about 10% next year, and overall commercial property declines of 5%, according to the Pension Real Estate Association.

The $34 billion of bonds due next year includes mostly fixed-rate CMBS bonds sold without government backing. It’s a steep increase from the $24.4 billion of such bonds maturing this year, according to Academy Securities.

There’s another $103 billion of a type of CMBS known as single-asset single-borrower bonds maturing next year, according to Academy — although most of that debt pile has a built-in contractual ability to extend loans, meaning they’ll be able to seek extensions more easily.

Next year won’t be the first time that CMBS bondholders and servicers have faced tough choices about whether to allow en masse extensions to the underlying borrowers. After the 2008 financial crisis, commercial property values plummeted and many lenders chose to give owners of those properties more time to pay back their loans. As a result they ended up getting more money back than if they’d immediately foreclosed on the loans and liquidated the properties, said Jeff Berenbaum, head of CMBS and agency CMBS strategy at Citigroup.

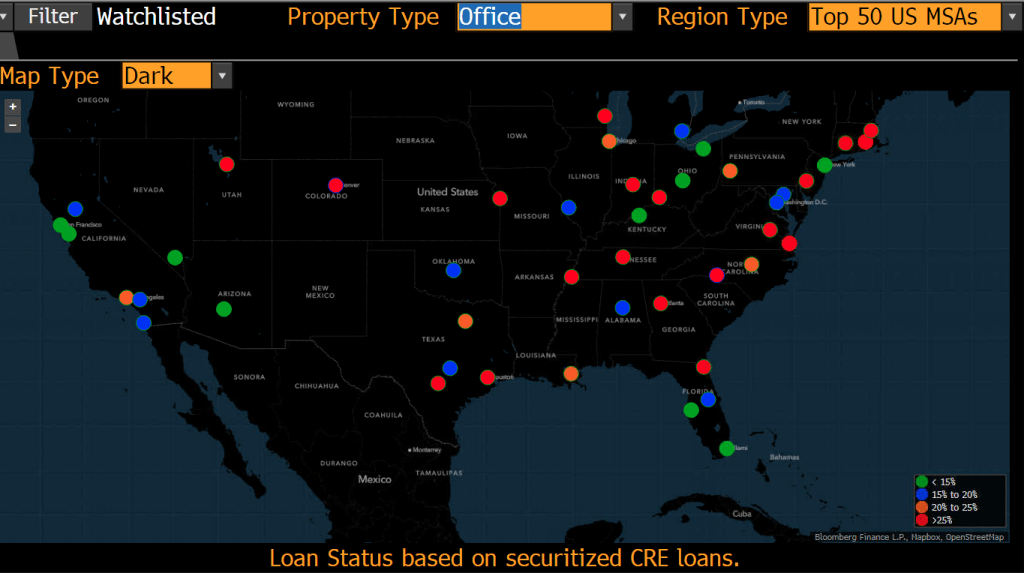

In terms of watchlisted CMBS loans, currently most of the USA is in the green (good) except for San Francisco, New Orleans, Memphis and Chicago all have elevated commercial loans on the watchlist (loans being watched for going late and into default). Puerto Rico is also in the red (>25%) watchlisted commercial loans, so I expect AOC to be asking for a bailout.

On the office property front, we can see red (>25% of commercial loans watchlisted) pretty much across the board.

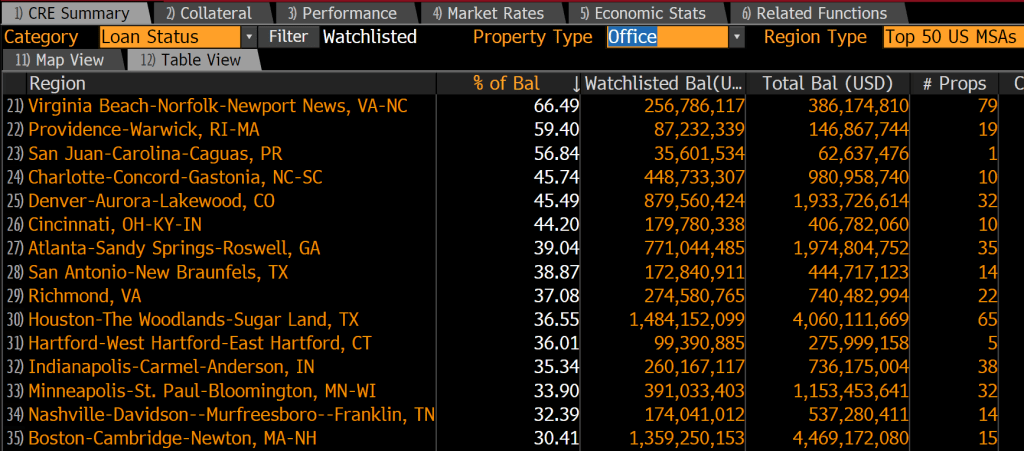

The leading metro area in terms of watchlisted office property loans is … Virginia Beach-Norfolk-Newport News VA-NC at 66.49% (that is pretty bad). Providence RI is second and San Juan Puerto Rico is third followed by Charlotte NC in fourth place. The only Ohio city in top 15 is Cincinnati, home of Skyline Chili and Montgomery Inn.

While most are calling for more rate hikes in 2023, I predicted that December’s likely 50 basis point hike with be the last one for a while as the US economy grinds to a halt. Or it’s all over now for Fed rate hikes.

While The Fed predicts slow growth, markets are pointing to recession. The Fed is out of touch with reality. As is the US Secretarty of Treasury, “Too low for too long” Janet Yellen.

The start of a new week and the US Treasury 10-year yield is up 10 basis points, always a noteworthy change. And with it, the 30-year mortgage rate should climb.

Since Biden/Pelosi/Schumer are in a lame duck session with Republicans taking the House in January, let’s see if Republicans can halt the insanity in Washington DC.

Be that as it may, Fed Funds Futures are pointing at a 50 basis point rate hike at the December 14th FOMC meeting.

Seriously, how is The Federal Reserve going to cope with $204 TRILLION … and growing Federal debt AND unfunded liabilities?

As The Federal Reserve continues its assault on inflation by raising their target rate, Blackstone Inc.’s $69 billion real estate fund for wealthy individuals said it will limit redemption requests, one of the most dramatic signs of a pullback at a top profit driver for the firm and a chilling indicator for the property industry.

Blackstone Real Estate Income Trust Inc. has been facing withdrawal requests exceeding its quarterly limit, a major test for the one of the private equity firm’s most ambitious efforts to reach individual investors. The news, in a letter Thursday, sent Blackstone stock falling as much as 10%, the biggest drop since March.

You can see the problem facing commercial real estate. Since December 31, 2021, NAREIT’s all-equity REIT index has fallen -23.6% while NAREIT’s mortgage REIT index has fallen -28.6%. It looks like Blackstone’s Real Estate Income Trust has a decline coming.

If I look at NCREIF’s commercial property index, we can see that The Fed helped boost CRE values. But what will happen if and when The Fed actually shrinks its balance sheet.

I call The Fed’s attempts at cooling inflation “Fed Dead Redemption” since it resulted in redemptions from real estate funds.

Deutsche Bank, my former employer, said that The Fed will slash rates by 200 basis points by mid-2024 after staying hawkish in the short term.

Deutsche Bank increased its view on the terminal rate and now sees it hitting 5.1% in May.

The Federal Reserve will remain hawkish in the short term but will cut benchmark rates sharply after that, according to a Monday note from Deutsche Bank.

The central bank has hiked rates by 375 basis points so far this year, with another half-point increase widely expected next month. Even more tightening will come, with analysts at Deutsche Bank increasing their view on the terminal rate, which they now see hitting 5.1% in May.

“Risks remain skewed to the upside, and we caution that the transition to pausing and eventual cuts may not be entirely linear,” the note said. “If elevated inflation and labor market imbalances persist, or financial conditions fail to tighten, a higher terminal rate could be needed.”

Meanwhile, the economy will slow down amid the aggressive tightening, and Deutsche Bank sees an 80% probability of a recession in the next year.

Analysts anticipate a moderate recession beginning mid-2023, with real GDP falling about 1.25 percentage points over three quarters and the unemployment rate reaching a peak of 5.5%.

“With a sharp rise in the unemployment rate and inflation showing clearer signs of progress, the Fed should cut rates by 200bps by mid-2024 when it approaches a neutral level around 3%,” analysts said. “QT should cease when the Fed cuts rates, to ensure both tools are not working in competing directions. Balance sheet drawdown could be modified or halted earlier if reserves continue to fall faster than expected.”

The first rate cut will be 50 basis points in December 2023, followed by 150 basis points of cuts into 2024, the note said.

The last Fed Dots Plot shows the next leg of The Fed Rollercoaster.

In the short term, Fed Funds Futures are pointing at another 106 basis point increase by June 2023.

The cryptocurrency market is getting hammered thanks mostly to two things: 1) Sam Bankman-Fried’s horrid failure with FTX (fraud, Enron, front-running, stupid investors, Democrat-Ukraine connection) and 2) Fed tightening to combat high inflation.

Bitcoin, the Mac Daddy of cryptos, is down another 2% today.

The rest of the story.

The NEW face of the US Federal government and why they will sweep the Bankman-Fried fiasco under the rug, just like Hunter Biden’s laptop fiasco.

US mortgage rates fell last week by the most since the end of July, slipping below 7% and helping generate a bounce in purchase applications that otherwise remain depressed, but only in the Seasonally Adjusted data. The NON-Seasonally Adjusted data show a hefty decline.

The contract rate on a 30-year fixed mortgage decreased 24 basis points to 6.9% in the week ended Nov. 11, according to Mortgage Bankers Association data released Wednesday. The group’s index of applications to buy a home rose 4.4% — the most since June — but is still near the weakest level since 2015.

But the bounce was in Seasonally Adjusted data only. The NON-seasonally adjusted data remained depressed.

Mortgage applications decreased -10.0 percent SA from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending November 11, 2022. This week’s results include an adjustment for the observance of Veterans Day.

The Refinance Index decreased -11.44% percent from the previous week and was 88 percent lower than the same week one year ago.The unadjusted Purchase Index decreased -10 percent compared with the previous week and was 46 percent lower than the same week one year ago.

Mortgage purchase applications will continue to fall in NSA terms since it is the Winter and home buying season won’t really start until January. Refinancing applications actually dropped -11.44% even with the drop in mortgage rates.

The data. As my former students know, I like the “raw” data, better known as NON-seasonally adjusted (NSA) data and avoid seasonally-adjusted data (SA) since it hides what is going on.

And on The Fed Futures Front, The Federal Reserve is still looking a hiking their target rate from 4% to just under 5%.

The evidence from the last thirty years is clear. Keynesian policies leave a massive trail of debt, weaker growth and falling real wages. Furthermore, once we look at each so-called stimulus plan, reality shows that the so-called multiplier effect of government spending is virtually inexistent and has long-term negative implications for the health of the economy. Stimulus plans have bloated government size, which in turn requires more dollars from the real economy to finance its activity.

As Daniel J. Mitchell points out, there is evidence of a displacement cost, as rising government spending displaces private-sector activity and means higher taxes or rising inflation in the future, or both. Higher government spending simply cannot be financed with much larger economic growth because the nature of current spending is precisely to deliver no real economic return. Government is not investing; it is financing mandatory spending with resources of the productive sector. Every dollar that the government spends means one less dollar in the productive sector of the economy and creates a negative multiplier cost.

When society decides to use a certain part of the resources generated by the productive sector for non-economic return activities, be it social spending or mitigation of threats, it can only do it by understanding how much of the productive capacity of the economy is able to sustain a larger cost. When costs are not considered as a burden, but considered as entitlements that can only grow, the productive capacity is not strengthened, but weakened.

The main problem of the past decades, but particularly since 2008, is that government spending and monetary policy have become solutions of first resort to any slump in economic activity, even if that decline was created by government decisions, such as shutting down the economy due to a health crisis. Furthermore, government spending increases and loose monetary policy continued even in growth periods. This, in turn, creates an unsustainable public deficit that needs to be monetized or refinanced. Both mean a larger harm for the productive sector as the debt increase leads to higher taxes for everyone but also a soaring cost of living coming from the destruction of purchasing power of the currency.

Government spending does not boost private sector activity, even less so when the entire budget is spent on non-investment outlays. It is even worse when citizens believe that infrastructure or real economic return investments should be conducted with taxpayers’ money. If an investment is productive and economically viable there is no need to involve the government. At best, the government should only participate as a co-investor, as the example of technology and defence shows, but never as a resource allocator for a simple reason. Public intervention is always aimed at perpetuating the existing inefficiencies and maximizing the budget. Efficient resource allocation cannot come from entities that have a core interest in expanding the budget and always perceive any inefficiency or poor result as the consequence of not having spent enough.

Yes, US public debt has exploded, particularly since the 2008 financial crisis and then again the Covid outbreak of 2020.

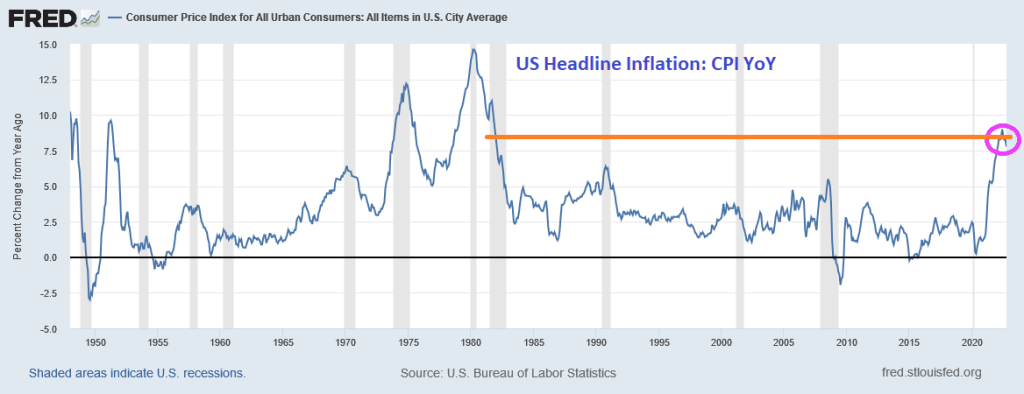

And inflation is near a 40-year high.

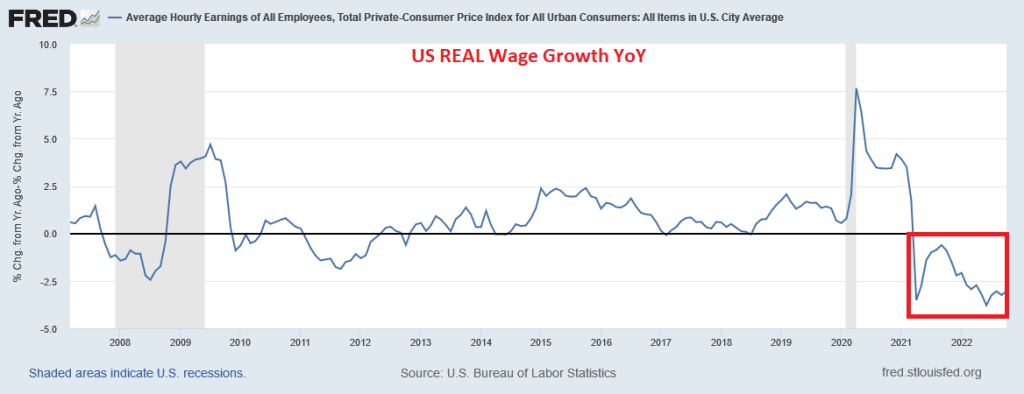

Then we have 19 consecutive months of negative wage growth in the US.

Biden is apparently doubling down on “Green Schemes” now that the US House of Lords (aka, Senate) remain under Keynesian control (aka, Democrat). So watch for inflation to start increasing again.

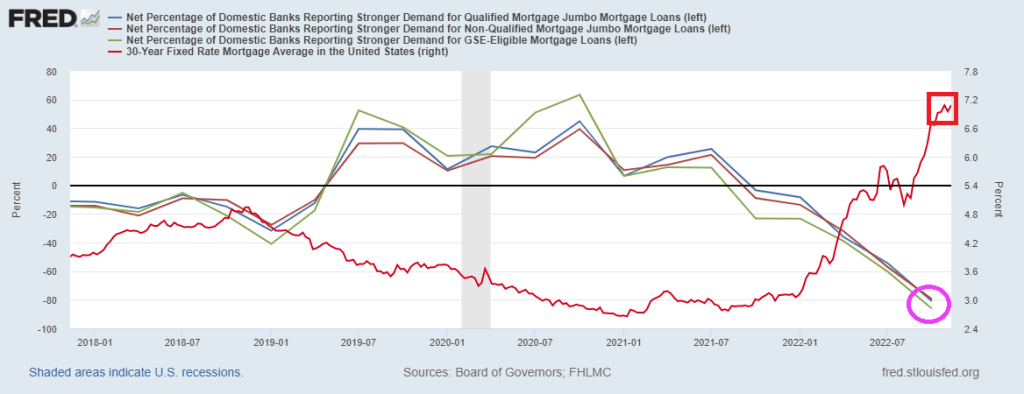

The Net Percentage of Domestic Banks Reporting Stronger Demand for Mortgage Loans is sinking faster than Joe Biden’s oratory skills as The Fed tightens their monetary belts.

And today, the University of Michigan (BOOO!!) consumer survey for housing buying conditions fell to the lowest level in recorded history.

Given the latest inflation numbers (improving from disastrous, 8.2% YoY to really horrible, 7.70% YoY), and unemployment rate rising from 3.5% to 3.7%, we now see that Taylor Rule estimate for Fed Funds is now … 13.85%. The US is currently at 4.00%. THAT is a big gap!

Yes, The Fed will not be able to fill the gap between the Taylor Rule and the current Fed Funds Target Rate, without incredible damage being done.

Unfortunately, this is an ACTIVE FAILURE for The Fed which has left monetary stimulus too high for too long since late 2008.

On a personal note, I am glad the midterm elections are over. We saw John Fetterman arguing until he was blue in the face that he loved fracking and will continue to let Pennsylvania frack. Then PA governor-elect Josh Shapiro came out yesterday and said that PA will end all fracking. And we are to believe that Lt Gov Fetterman did not talk with PA Attorney General Shapiro about fracking? To quote Joe Biden, “C’mon man!”

You must be logged in to post a comment.