One reason is diesel fuel prices are up 102% under Biden’s Reign of Error. While inventory of diesel fuel down -37%. Meanwhile core inflation is up from a measly 1.3% to a whopping 6.6% at the latest inflation report.

Introducing Biden’s Thanksgiving dinner … in a can to cope with rising prices.

Just kidding. This is too clever for the clueless Biden Administration. But Karine Jean-Pierre might get as confused as Joe Biden and repeat it as one of the ways that The Biden Administration is helping consumers.

As I told my Chicago, Ohio State and George Mason University finance and real estate students, repeatedly, “Watch out when The Fed begins to tighten monetary policy. It will be a bloodbath for taxpayers.”

Well, here we are. I argue that Biden’ green energy knucklehead policies are driving inflation, or it could be the insane level of Federal spending that Obama economist Larry Summers warned us about, or rising wages (in part due to Federal spending) is to thank for inflation. Or all of the above.

Regardless of the cause, the bond market is enduring its worst selloff in a generation, triggered by high inflation and the aggressive interest-rate hikes that central banks are implementing. Falling bond prices, in turn, mean paper losses on the massive holdings that the Fed and others accumulated during their rescue efforts in recent years.

Rate hikes also involve central banks paying out more interest on the reserves that commercial banks park with them. That’s tipped the Fed into operating losses, creating a hole that may ultimately require the Treasury Department to fill via debt sales. The UK Treasury is already preparing to make up a loss at the Bank of England.

The Reserve balance has crashed into negative territory.

And Fed losses are skyrocketing.

Agency MBS prices are up today, but are down since August 2022. But risk measures duration and convexity are zooming upwards.

The Federal Reserve’s DOTS PLOT shows where each Fed official’s projection for the central bank’s key short-term interest rate is headed. As of the September 21, 2022 Fed Open Market Committee (FOMC) meeting, the prediction of future Fed target rates is decidedly DOWNWARD SLOPING.

The Fed hawks, those that want to tighten monetary policy, are Bowman, Waller, Kashkari, Mester and George. The Fed doves (or those who are neutral) are Biden recent appointees Barr, Cook, Jefferson, Logan, Collins. Note that Brainard and Bostic are the only technical doves.

I call the hawks at The Fed “The Blackhawks” since their mission of fighting inflation may lead to a recession. And Bowman, Mester and George are Lady Blackhawks.

Bloomberg’s recession probability over next 12 months is … 100%.

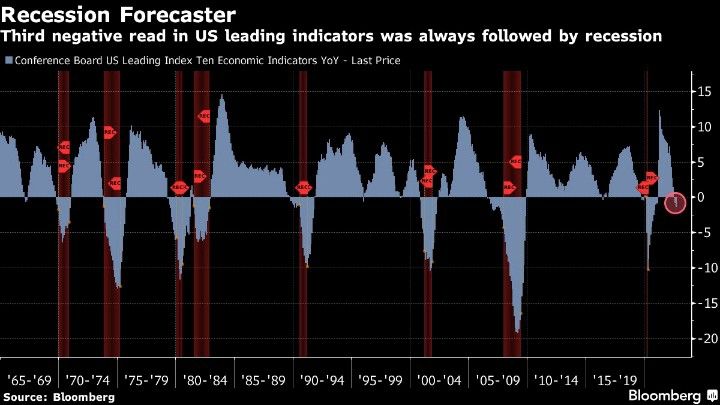

And how about the Conference Board’s Leading index of 10 economic indicators YoY? Third negative read ALWAYS followed by recession.

The Federal Reserve may be forced to pivot. This may be one reason why the Dow is up 565 points today (+1.86%) as recession and pain become ever more likely.

Look at commercial banks deposits. Wonder why liquidity is drying up?

Pension funds have long been investing in “safe” agency mortgage-backed securities.

But as The Fed does its “tighten up”, we are seeing agency MBS prices falling and duration risk rising.

I remember showing my Fixed-income class at Chicago and George Mason the “MBS doom chart” showing the perils of The Fed pushing rates so low that the risk of rising rates becomes a serious problem when rates start to rise. Well, here we are … after I have retired from teaching.

Note the double whammy of Fed rate increases and the gradual shrinking of The Fed’s balance sheet as The Fed withdraws it ample stimulus. But while The Fed was overstimulating markets, it was quite a rush.

But the rush is gone … for the moment. But “Feddie Krueger” is waiting in the wings to do it all over again!

One of my friends on Wall Street wrote my yesterday claiming “The 10-year Treasury yield is set to crash. Brace for impact!” Then I logged into Bloomberg this AM and saw the 10-year Treasury yield up almost 10 basis points (although it is down -2 BPS at 10:20am). Did markets not read his comments?? Maybe they did!

Well, The Fed is doing the Tighten Up. That is, The Fed is FINALLY removing their excessive monetary stimulus left over from the Bernanke Blowout (2008 adopting Japan’s print ’till you drop model).

But as The Fed removes their monetary stimulus (rate increases), we are seeing negative effects in the housing market. I call this chart “The X Factor.”

The US Treasury 10-year yield is up to 4.3% this morning, a far cry from 1.804% when Biden was crowned as President on January 20, 2021. The 30-year mortgage rate is up from 3.67% on Coronation Day to 7.32% yesterday, an increase of … 100% (that is, the 30-year mortgage rate has doubled under Biden). At the same time, Existing Home Sales YoY have gone from -2.41% in January 2021 to -23.79% in September 2022. THAT is a HUGE decline!

University of Michigan’s consumer sentiment for housing for 77 in January 2021 to 39 in November 2022. That is a -49% decline in consumer confidence. Also a big decline.

But going back to my pal’s email, he also said that The Fed is unwinding its balance sheet at a dangerously rapid rate (orange line). Relative to just increasing it, I would agree with him. But The Fed’s balance sheet is barely declining to my eyes. The troubling thing for housing is that inflation is so hot that REAL average hourly earnings YoY (yellow line) has fallen from +0.24% growth YoY on January 25, 2021 to a horrific -2.80% YoY rate in September 2022.

Bill’s point to me is that lending is still hot (at least commercial and industrial lending or C&I) while The Fed’s balance sheet remains in force (green line).

The Fed has a lot more work to do if they want to cool the commercial lending market. They have successfully slowed down the residential mortgage market.

Today’s existing home sales were … gruesome. While EHS month-over-month were down only -1.5%, on a year-over-year basis EHS was down a staggering -23.79%.

If you look at the declining growth rate of M2 Money (green line) and rising mortgage rates (yellow line), we can see why the housing market is struggling.

How about median price? That dropped to 8.07% YoY as inventory for sale remains lower than before Covid and Covid stimulypto.

US 30-year mortgage rates rose to 7.20% yesterday, the highest rate since 2000. Why?

Core inflation is rising and its the highest since 1992. Diesel prices, the all-important fuel for the transportation industry, is rising again after a brief respite and is near the all-time high.

But will mortgage rates continue to rise? That depends on The Federal Reserve. Will they continue to try to combat inflation (largely caused by … The Federal Reserve and voracious Federal spending under Biden/Pelosi/Schumer (The Three Amigos).

As of today, investors in Fed Funds Futures are pointing to a peak of Fed tightening in May 2023, then a slow decline in rates.

While this is The Fed Funds rate, it is likely that mortgage rates will continue to rise to May 2023 then level out at 9%-9.25%.

I really miss teaching college students. An example of a test question I gave was the first chart: who was The President when all hell broke loose (pink box)? 1) Joe Biden, 2) Donald Trump or 3) Millard Fillmore?

The answer, of course, is Joe Biden.

Doesn’t Millard Fillmore, the 13th President of the United States, look like actor Alec Baldwin after too many cheeseburgers and chocolate milkshakes at In-N-Out Burger?

Bear in mind that the are numerous wildcards in play, like the Russia/Ukraine war and the probability the China will invade Taiwan in the near future.

You must be logged in to post a comment.