US Real GDP Annualized QoQ printed at -1.5%. And GDP prices QoQ printed at 8.1%, also higher than expected.

At least Personal Consumption printed higher than expected at 3.1%.

Import prices (goods) led the way at 20.9%. Part of Biden’s brilliant strategy of reducing domestic oil production and import expensive energy from overseas?

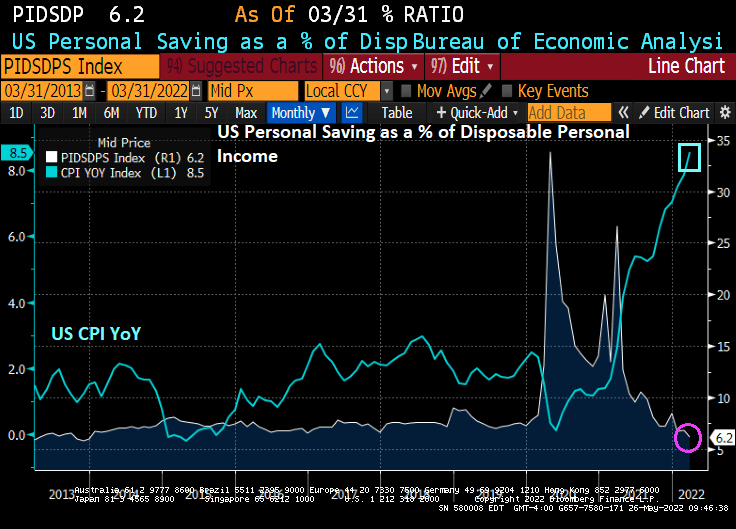

Consumers are spending more, but the personal savings rate is down to the lowest level since 2013 at 6.2% as consumers try to cope with inflation.

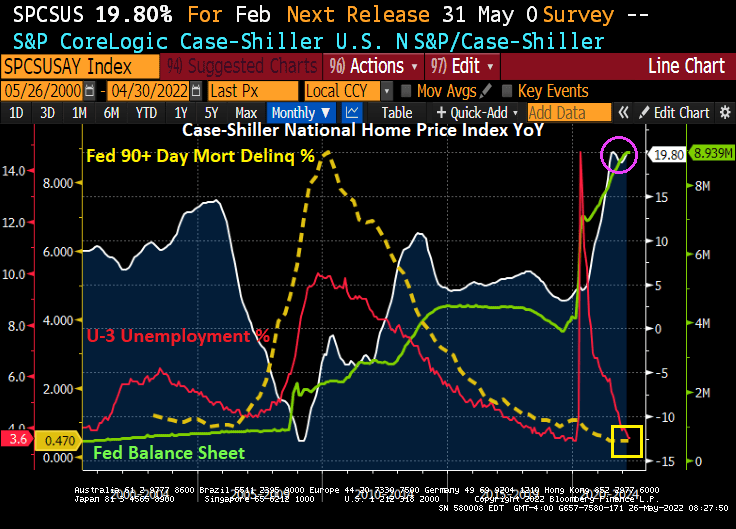

If we look at 90+ days late for mortgages (yellow line), we see that the surge in unemployment with the Covid outbreak and subsequent government shutdowns (red line) did not lead to a surge in mortgage foreclosures.

This situation is quite unlike 2008 when collapsing home prices and the subsequent surge in the unemployment rate led to a 90+ days late surge on mortgages (yellow line).

Difference between today and 2008? The Federal Reserve’s asset purchase (green line) surge happened twice AFTER the 2008 housing crash. Once in late 2008 through 2014, then a second, bigger surge in March 2020 after the Covid outbreak. One big difference is the surge in home prices, home price growth was 3.69% YoY in December 2019 and skyrocketed to 19.80% as of February 2022. This translates to a massive increase in homeowner equity, leading to a lower probability of default.

So, there you go. Powell and The Federal Reserve made housing unaffordable for millions of Americans, but The Fed did help thwart another mortgage default crisis. BUT we will see what happens with future rate hikes from The Fed.

Here is Attom’s US Foreclosure Starts chart. Yes, that is hardly a surge, although foreclosure starts did rise in Q1 2022.

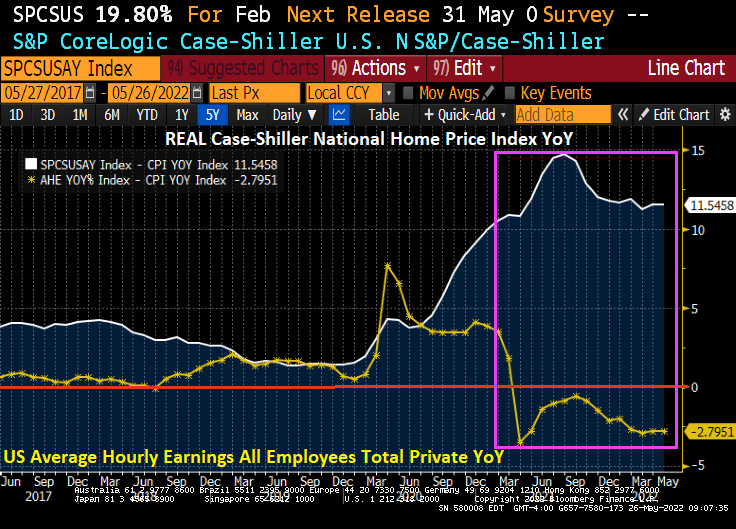

So, The Fed has helped make housing simply unaffordable. Look at the growth of REAL home prices relative to REAL average hourly earnings.

The US Q1 GDP report is due out tomorrow morning. The forecast is for -1.3% decline in GDP.

The Atlanta Fed GDPNow real-time GDP tracker is for 1.806% for Q2. If this holds, then recession fears will diminish.

Even though the US may avoid consecutive negative GDP quarters, M2 Money Velocity (GDP/M2 Money) got crushed by The Fed’s reaction to Covid back in 2020.

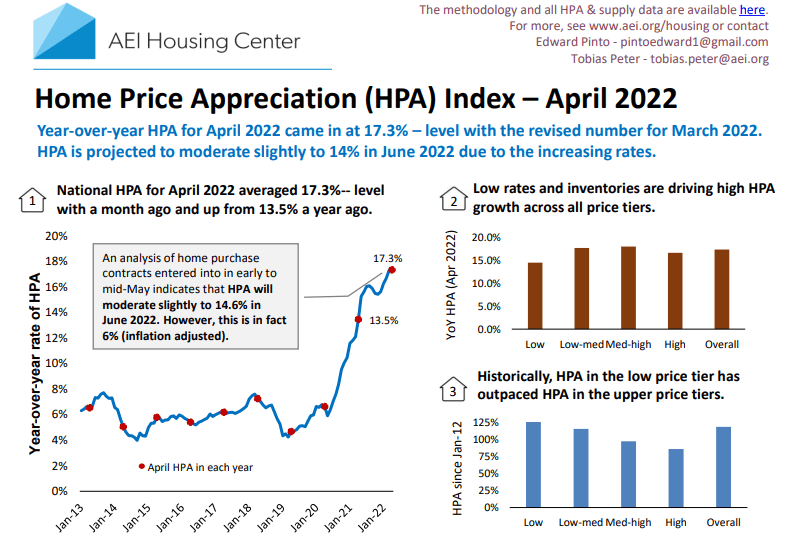

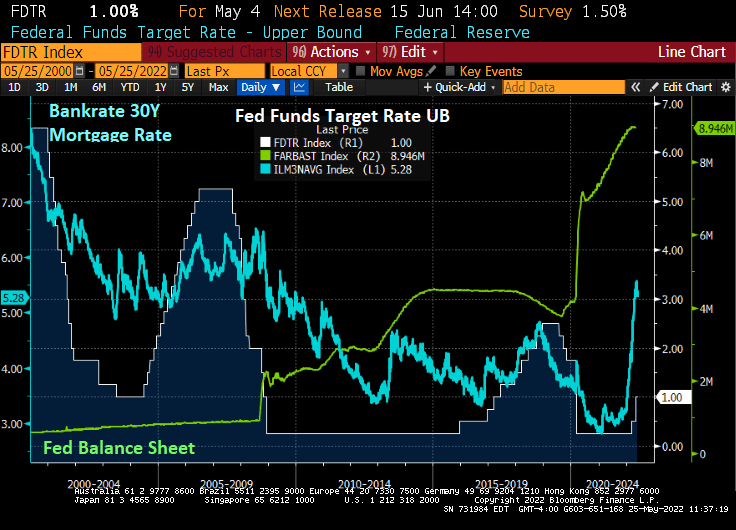

The reason why home prices are still raging at 17.3% YoY? The Fed’s monetary stimulypto is STILL in place! The Fed’s balance sheet (green line) is still staggering, and The Fed Funds target rate (white line) is a measly 1%.

Atlanta Fed President Raphael Bostic is talking about a pause in Fed tightening. Which they haven’t paused yet.

Fed Chair Jerome Powell is really “slowhand,” not Eric Clapton. Bostic is now a member of The Fed’s “Slowhand” strategy.

I have never seen two Federal entities make such a mess in my life. The Federal Reserve and The Federal government.

The good news? The 10-year Treasury yield is down -12.9 BPS this morning generally resulting in lower 30-year mortgage rates. Of course, the reason why the 10-yield is falling is generally bad news.

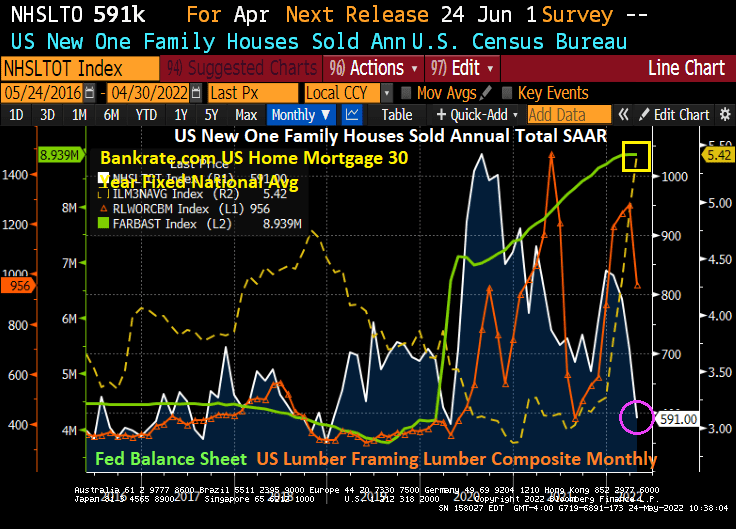

The bad news? US New Home Sales fell -16.6% MoM in April as mortgage rates skyrocketed.

Since the installation of Joe Biden as President, new home sales have plunged -31.2%, mortgage rates are up 88.9%, and framing lumber prices are up 29.2%.

Biden is out there bragging about rising energy prices which he views as a necessity to force the conversion of America to electric cars and trucks. Biden is the first President in history to gloat over the suffering of American households.

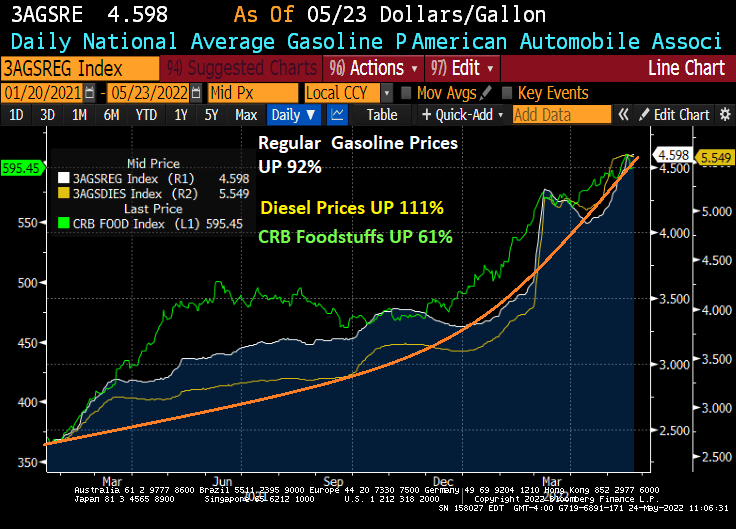

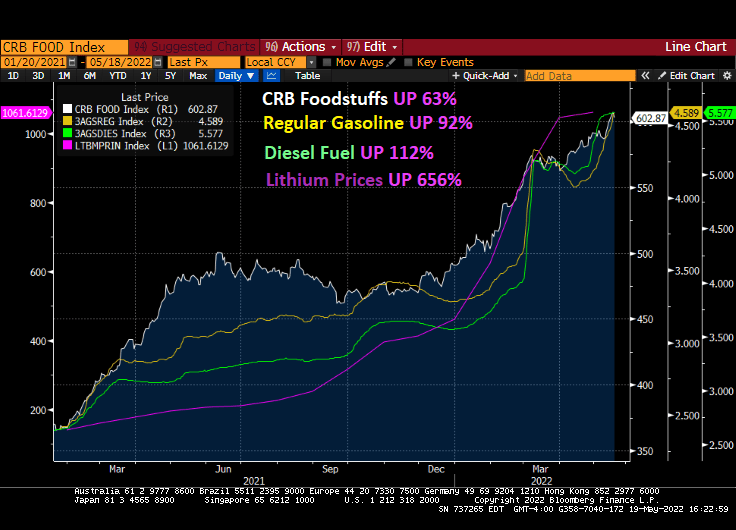

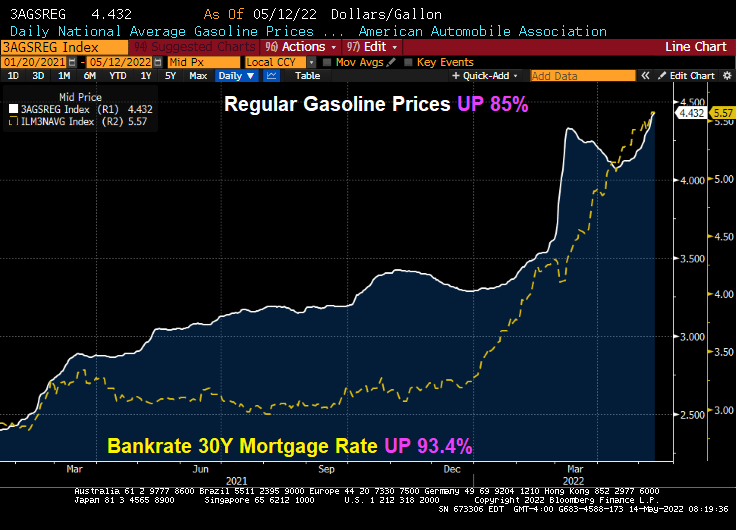

Under Biden, regular gasoline prices are up 92%, diesel prices are up 111%, and CRB Foodstuffs are up 61%.

Say, framing lumber for housing is cheaper than food. Maybe Biden will suggest Americans transform to being beavers and gnaw on wood.

As The Federal Reserve tries to fight inflation (it can’t thanks to Federal energy policies and bottlenecks), it is causing a disconnect between mortgage current coupon rate and the MBS index coupon. The disconnect is so bad that it is back to 1985 levels.

The Fed can certainly try to cool inflation, but Biden is intent on raising energy prices (leading to food price increases, and everything else) to shift us to electric cars. So, Biden is unlikely to back off.

So, The Fed is left trying to fight a war against inflation that only Biden can fight.

Meanwhile, the US mortgage market is getting pulverized

Mortgage rates have increased dramatically under “Middle Class Joe” as The Federal Reserve attempts to choke-off inflation caused by … The Fed coupled with Biden’s energy policies (hope you are enjoying those high gasoline and diesel prices!) and the Federal government’s staggering spending spree under Pelosi, Schumer and McConnell.

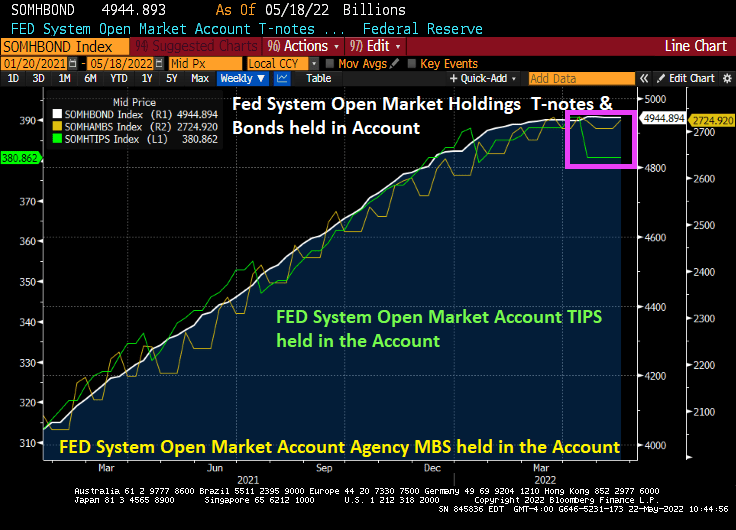

Thus far, The Federal Reserve has leveled-out out their Treasury Note and Bond purchases, increased their Agency Mortgage-backed Securities (AgMBS) holdings, but strangely have reduced their holding of Treasury Inflation-Protected Securities (TIPS) in the face of rising inflation.

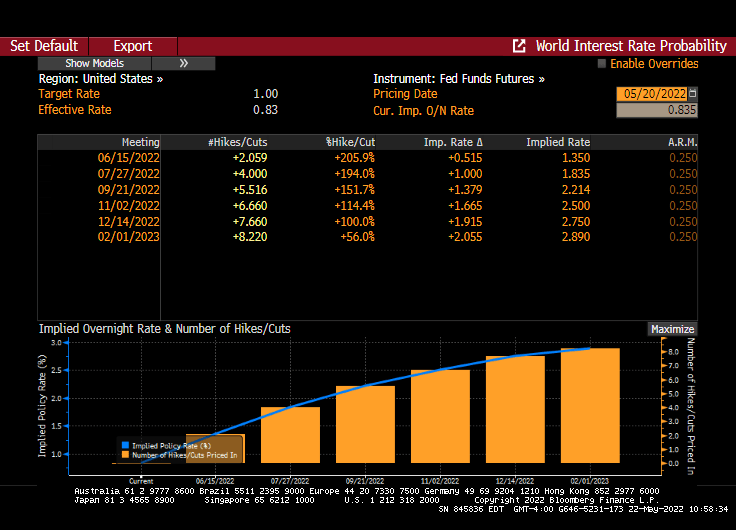

And while The Fed Funds Target rate is a lowly 1%, it is projected to rise to 2.890% by the February 1, 2023 FOMC meeting. That should send mortgage rates up.

As if mortgage rates haven’t skyrocketed already, thanks to The Fed’s jawboning about having to raise rates and extinguish inflation.

With sizzling mortgage rates (cooling a bit as the global economy slows), home mortgage payments have risen +43.4% YoY.

Now we have President Biden trying to scare us about the Monkey Pox, yet leaves the southern border wide open. One would think that Biden would shut the borders (as if the surge in Fentanyl, sex trafficking and other diseases aren’t reason enough. But I do predict another massive spending bill from Biden/Congress to combat Monkey Pox and the resurgence of Covid variants.

Meanwhile The Fed jawbones fighting inflation with monetary tightening in the future, even if they jawboning causes mortgage rates to soar and mortgage payments to spiral.

The inflation that is crushing Americans is due to energy and food price increases. That is, the non-core inflation. Under Biden, food is up 63%, gasoline is up 92% and diesel prices are up 112%. But The Fed doesn’t consider food and energy prices, per se.

If we look at the Taylor Rule considering fighting inflation including food and energy, The Fed would have to raise their target rate to … 21.38%.

Now, The Fed can clearly cool-off the housing market by raising rates. In fact, my fear is that they go too far and crash the housing market. The Fed will NEVER get to 20% again like we last saw under Volcker in 1981. 20% rates certainly cooled home prices back then and Fed rate hikes helped crash the housing market in 2008.

So, when The Fed says they want to be the inflation-fightin’ Fed, we must be aware what The Fed can and cannot do. They can’t tame the inflation beast in the form of food and energy prices (unless they crash the economy), but they can crush home prices.

In the two-pronged attack out of Washington DC, The Federal Reserve is tightening their monetary policy in an effort to combat 40-year highs in inflation (caused by excessive Federal spending and Biden’s ill-advised energy policies), causing residential mortgage rates to soar 93.4% under Biden’s Reign of Error.

It is almost like the Biden Administration and The Federal Reserve are engaged in an economic demolition derby to see who can cause the most destruction to America’s middle class and lower-wage workers.

We should call the current administration and The Federal Reserve “Demolition Men.”

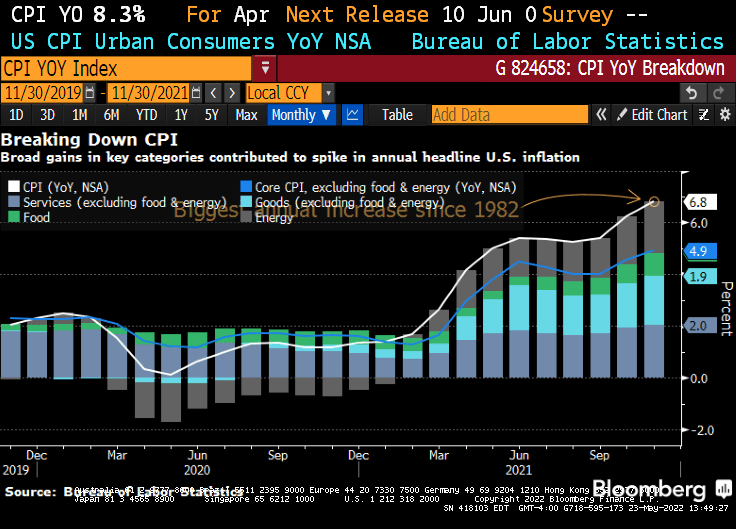

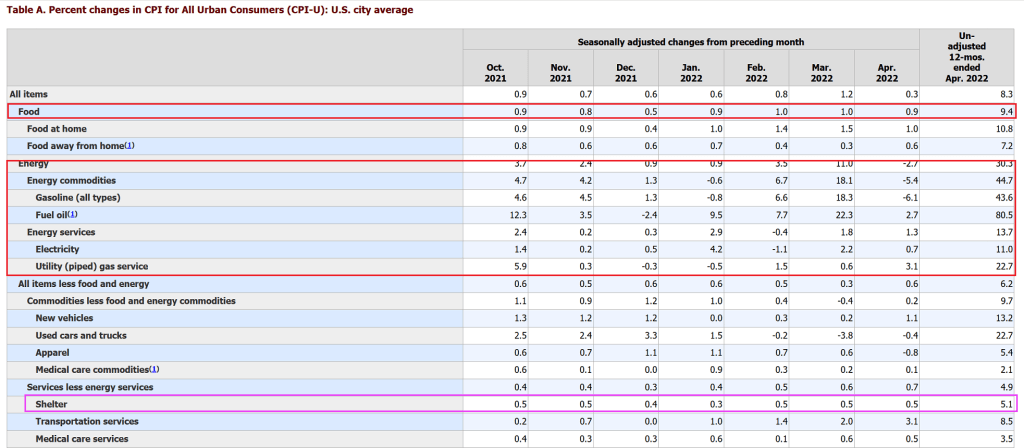

April’s inflation numbers are out and, at first glance, inflation seems to be cooling from 8.5% YoY in March to 8.3% YoY.

But the headline inflation numbers do not accurately reflect the pain and suffering of American households. Food is up 9.4% YoY and gasoline is up 43.6% YoY.

The strange way the BLS measure “shelter” shows that housing only grew at 5.1% YoY. That’s odd since home price growth is almost 20% YoY and rent growth is near 20%.

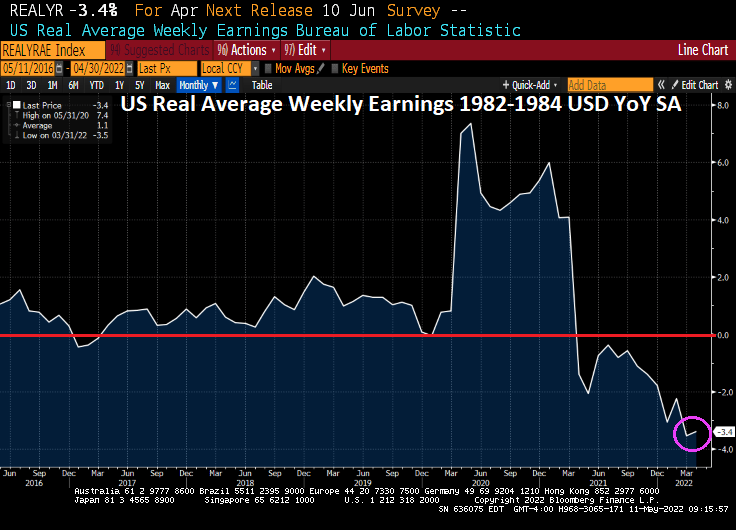

Runaway home prices and rents are especially painful given that inflation is destroying the purchasing power of the dollar for consumers. Real average weekly earnings YoY are at -3.4% YoY.

Hence, the purchasing power of the US Dollar keeps eroding.

Good luck out there with inflation still roaring, and food/housing/energy prices soaring.

Here is a photo of American children trying to create energy from flying a kite made from progressively devalued US currency.

You must be logged in to post a comment.