The Covid outbreak of early 2020 begat a massive surge in monetary stimulus which has dissipated. Notice that home price growth is dissipating as well.

Also causing problems for housing is NEGATIVE REAL WAGE GROWTH. While the US is suffering from inflation and decling real wage growth, trading partner Germany has even a worse REAL WAGE GROWTH problem.

Deutsche Bank, my former employer, said that The Fed will slash rates by 200 basis points by mid-2024 after staying hawkish in the short term.

Deutsche Bank increased its view on the terminal rate and now sees it hitting 5.1% in May.

The Federal Reserve will remain hawkish in the short term but will cut benchmark rates sharply after that, according to a Monday note from Deutsche Bank.

The central bank has hiked rates by 375 basis points so far this year, with another half-point increase widely expected next month. Even more tightening will come, with analysts at Deutsche Bank increasing their view on the terminal rate, which they now see hitting 5.1% in May.

“Risks remain skewed to the upside, and we caution that the transition to pausing and eventual cuts may not be entirely linear,” the note said. “If elevated inflation and labor market imbalances persist, or financial conditions fail to tighten, a higher terminal rate could be needed.”

Meanwhile, the economy will slow down amid the aggressive tightening, and Deutsche Bank sees an 80% probability of a recession in the next year.

Analysts anticipate a moderate recession beginning mid-2023, with real GDP falling about 1.25 percentage points over three quarters and the unemployment rate reaching a peak of 5.5%.

“With a sharp rise in the unemployment rate and inflation showing clearer signs of progress, the Fed should cut rates by 200bps by mid-2024 when it approaches a neutral level around 3%,” analysts said. “QT should cease when the Fed cuts rates, to ensure both tools are not working in competing directions. Balance sheet drawdown could be modified or halted earlier if reserves continue to fall faster than expected.”

The first rate cut will be 50 basis points in December 2023, followed by 150 basis points of cuts into 2024, the note said.

The last Fed Dots Plot shows the next leg of The Fed Rollercoaster.

In the short term, Fed Funds Futures are pointing at another 106 basis point increase by June 2023.

The US has an inflation problem. Both headline and core inflation YoY remain high compared to the previous 40 years. And The Federal Reserve is resolute in trying to curb inflation to 2%.

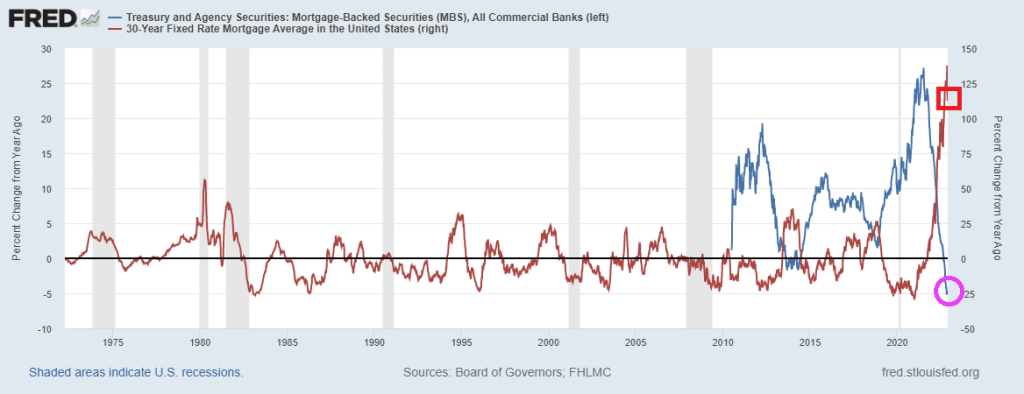

But as The Fed counterattacks inflation by raising their target rate, we are seeing a problem forming at the nation’s commercial banks. The growth in deposits YoY is now -0.6%. Commercial bank holdings of Treasuries and Agency MBS are declining as well. Agency MBS holdings are down -4.6% YoY and Treasuries and Agency holdings are down 0.0%.

How about M2 Money growth and M2 velocity? M2 Money growth has fallen to 1.3% YoY while M2 velocity has not been the same since the Covid sugar splash by The Fed and Federal government.

While inflation is creating havor for commercial bank deposit growth, it is interesting to follow the adventures of a spoiled child from MIT and his multi-billion dollar lemonade stand with all the controls of a child.

Once again, how did regulators get this SOOOOO wrong? And why didn’t investment advisors look at the balance sheet of FTX and Alameda Research. Yes, the media loves to report on FTX orgies, but the FTX fiasco points to something far more sinister. Were Sam Bankman-Fried and his paramore Caroline Ellison fronting this operation on behalf of some other parties?

I recall one of Woody Allen’s best lines. When asked what an investment manager does, the response was “they manage your money until nothing is left.” Sounds like SBF has a great future on Wall Street! And Caroline Ellison should have known better than to post things like “Here are what I think about some things: controlling most major world governments.”

Due to high inflation, reduced consumer spending, higher rents and other economic pressures, U.S.-based small business owners’ rent problems just escalated to new heights nationally this month, based on Alignable’s November Rent Poll of 6,326 small business owners taken from 11/19/22 to 11/22/22.

Unfortunately, 41% of U.S.-based small business owners report that they could not pay their rent in full and on time in November, a new record for 2022. Making matters worse, this occurred during a quarter when more money should be coming in and rent delinquency rates should be decreasing. But so far this quarter, the opposite has been true.

Last month, rent delinquency rates increased seven percentage points from 30% in September to 37% in October. And now, in November, that rate is another four percentage points higher, reaching a new high across a variety of industries.

All told in Q4 so far, the rent delinquency rate continues to increase at a significant pace, up 11 percentage points from where it was just two months ago.

Well, this is not good.

And on the mortgage front, not all is quiet.

Commercial bank holding of Agency mortgage-backed securities (MBS) has collapsed with Fed tightening and mortgage rate increases.

With an impending railroad strike that can torpedo the US economy (but if that is possible, why is the Biden Clan vacationing in Nantucket for Thanksgiving weekend when Joe should be talking with railroads and the unions to not let this happen?), let’s see what interest rates are telling us.

First, the US Treasury 10Y-2Y yield curve continues to descrend into the abyss (now at -80 basis points).

Second, the latest Fed Dot Plot (from September, new one will be issued during December) show that The Fed thinks that their target rate, while rising in 2023, will likely start falling again in 2024.

Third, since it is Thanksgiving Day, US bond markets are closed. But in Europe, the 10-year sovereign yields are falling, a sign that the ECB is reversing course by increasing monetary stimulus and/or a European are slow down.

Fourth, US mortgage rates have cooled since peaking (locally) at 7.35% on November 3, 2022 and now sit at 6.81%, a decline of 54 basis points. A clear sign of cooling.

Fifth, how about Fed Funds Futures data? It is pointing to a peak Fed Funds Target rate of 4.593% at the June FOMC meeting. Then a decline in rates to 2.301% by January 2024.

Now, go and enjoy your Thanksgiving dinner with friends and family (up 20% since last year), courtesy of Jerome Powell, Joe Biden, Nancy Pelosi and Chuck Schumer.

Not surprisingly, the median price of new home sales are up 8.2% MoM (since September).

The Fed’s minutes for their last FOMC meeting will be out at 2pm EST. Let’s see if they discuss WHY they haven’t reduced their balance sheet by much which is contributing to asset bubbles.

Here is The Fed’s Dots plot from the September meeting. I get the impression that The Fed thinks that their target rate will be coming down in 2024 and after.

The global economic slowdown has one nice unintended consequence: as the 10-year Treasury yield softens, mortgage rates decline.

US mortgage rates retreated sharply for a second week, hitting a two-month low and providing a bit of traction for the beleaguered housing market.

The contract rate on a 30-year fixed mortgage decreased 23 basis points to 6.67% in the week ended Nov. 18, according to Mortgage Bankers Association data released Wednesday.

Rates have plunged nearly a half percentage point in the past two weeks, the most since 2008, as recession concerns mount, inflation shows signs of cooling and a number of Federal Reserve officials say it may soon be appropriate to slow the pace of monetary tightening.

The slide in borrowing costs helped stir demand as the group’s index of applications to buy a home climbed 2.8%. That marked the third-straight increase since the gauge stumbled to the weakest level since 2015.

The pickup in demand allowed the overall measure of mortgage applications, which includes refinancing, to rise for a second week, but it still remains depressed. The index of refinancing activity edged up from a 22-year low.

The Refinance Index increased 2 percent from the previous week and was 86 percent lower than the same week one year ago.The unadjusted Purchase Index increased 9 percent compared with the previous week and was 41 percent lower than the same week one year ago.

But you need an electron microscope to see the increase in both purchase and refi apps.

One indicator of a slowing global economy is the decline of FANG (Facebook, Amazon, Netflix, Google) with declining liquidity.

The US economy is in “The Deep.” Deep into yield curve inversion, that is.

The US Treasury 10Y-2Y yield curve swam deeper into inversion at -75 basis points. The deepest inversion since just before The Great Recession and housing market crash.

During the Covid crisis of 2020 (red box). consumer credit declined and households were saving. But following the end of US Covid economic shutdowns, we saw inflation soaring to 40-year highs as Biden declared war on fossil fuels and a Pelsoi-led Congress went on an epic spending spree. But with soaring inflation, came a decline in personal savings and soaring consumer credit outstanding in an attempt to cope with Bidenflation.

Meanwhile, in the crypto universe, CNBC’s Jim Cramer and ARK’s Cathie Wood are going big for cryptos. With Wood buying Bitcoin and Cramer touting Coinbase.

Hmmm.

But at least Litecoin and the others are up today. Likely because Cramer and Wood are touting cryptos with “buy the dip!” strategy.

And on the Sam Bankman-Fried fiasco front, I am watching the deflection of wrongdoing from SBF to his girlfriend and now the co-CEO of Alameda Research, Sam Trabucco.

Bloomberg: He has a degree from MIT and cut his teeth as a trader at Susquehanna International Group. Yet the former co-head of Alameda Research made it clear that poker and black-jack tables were where he honed the gambler’s instincts he applied to cryptocurrency trading.

“I may or may not be banned from 3 casinos for this,” Sam Trabucco once tweeted about counting cards at black jack tables.

As I mentioned on Varney and Company on Fox Business, housing is going to suffer when The Fed starts to tighten their monetary policy. And here we are, folks!

US existing home sales fell a staggering -28.43% YoY in October as M2 Money growth grinds to almost a halt.

October’s existing home sales YoY of -28.43% is the WORST since The Great Recession and collapse of Lehman Brothers.

The median price of existing home sales slowed to 6.6% YoY. Inventory of EHS remains below pre-Covid levels.

Unrelated to housing, Prince Imhotep (Federal Reserve Bank of Minneapolis President Neel Kashkari) said Friday that the whole idea of cryptocurrency is “nonsense” after the implosion of FTX revealed the industry’s shortcomings.

“This isn’t case of 1 fraudulent company in a serious industry,” Kashkari said on Twitter, commenting on an article about how investors fell for FTX. “Entire notion of crypto is nonsense. Not useful 4 payments. No inflation hedge. No scarcity. No taxing authority. Just a tool of speculation & greater fools.”

Or it could be that investors don’t trust The Fed or Federal government to act in their best interest.

Here is a crypto investor (in red fez) being lectured by Minneapolis Fed President Neel Kashkari.

You must be logged in to post a comment.