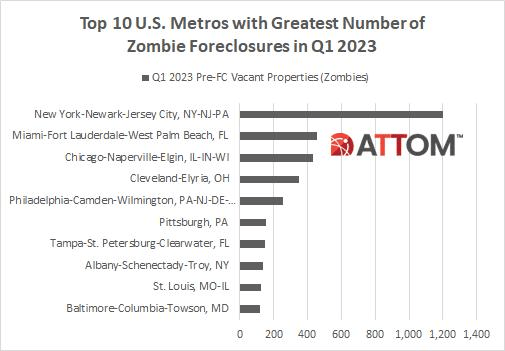

According to Attom Data, New York City leads the nation in zombie forceclosures.

A zombie foreclosure refers to a situation where a homeowner vacates their property after receiving a notice of default, expecting they will lose the home in the pending foreclosure. The foreclosure may get canceled for any number of reasons and never completed.

New York City and its surrounding areas lead the nation in zombie foreclosures. Followed by Miami. Chicago and Cleveland. Then Philadelphia.

You must be logged in to post a comment.