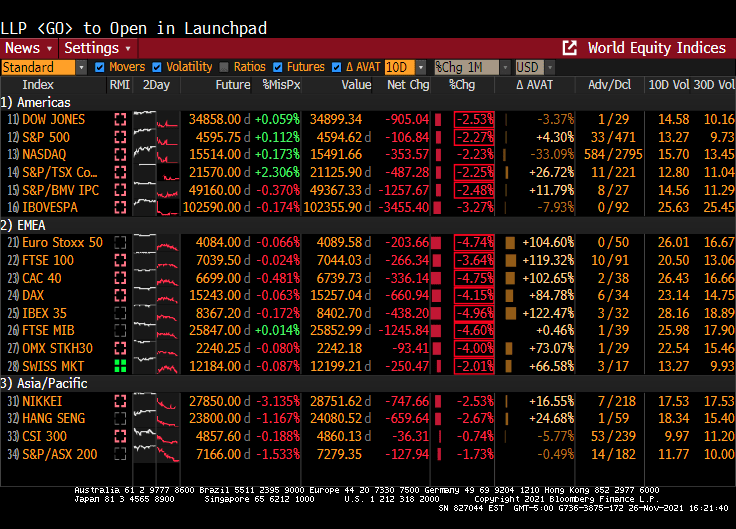

It has been a grim Friday. The Dow fell 900 points, 10Y Treasury yields fell 16.1 basis points and West Texas Crude fell to $68.17.

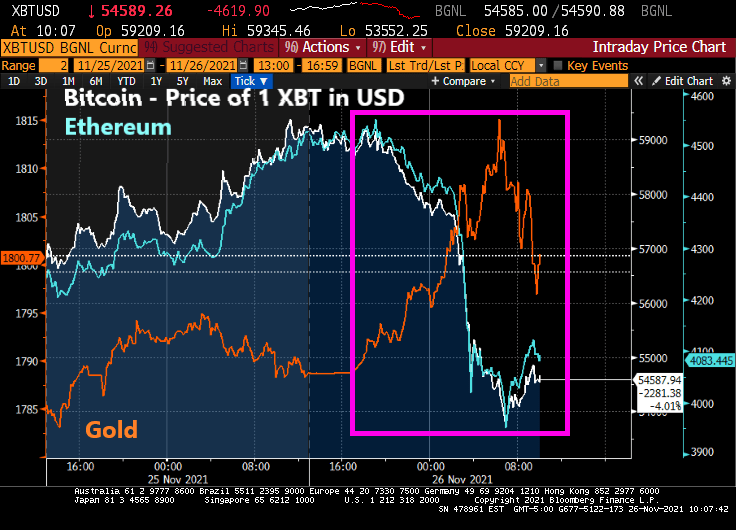

Bitcoin tumbled 20% from record highs notched earlier this month as a new variant of the coronavirus spurred traders to dump risk assets across the globe.

The world’s largest cryptocurrency fell as much as 8.9% to $53,624 on Friday during London trading hours. Ethereum, the second-largest digital currency, dropped more than 12%, while the wider Bloomberg Galaxy Crypto Index declined as much as 7.5%. On the other hand, gold rose as cryptos fell, then retreated as cryptos rebounded.

A new variant identified in southern Africa spurred liquidations across markets, with European stocks falling the most since July and emerging markets also slumping.

The Dow is down around 900 points … and look at Europe!

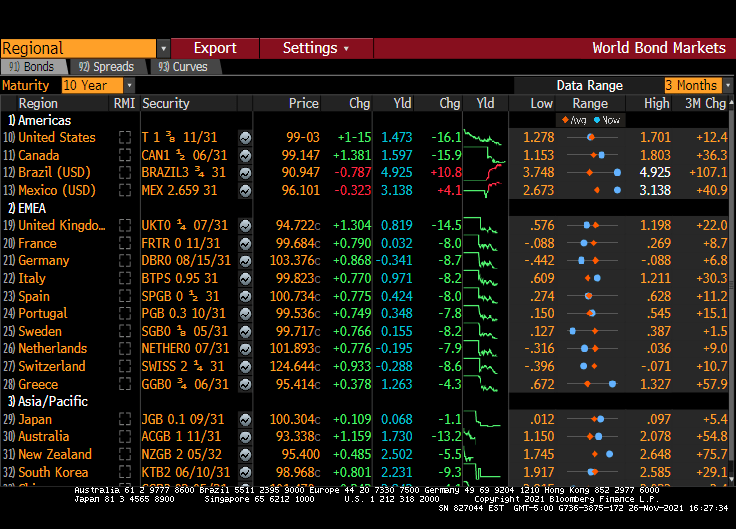

The 10-year Treasury yield is down 16.1 basis points. Most of Europe is down around 8-9 basis points while the UK is down 14.5 BPS.

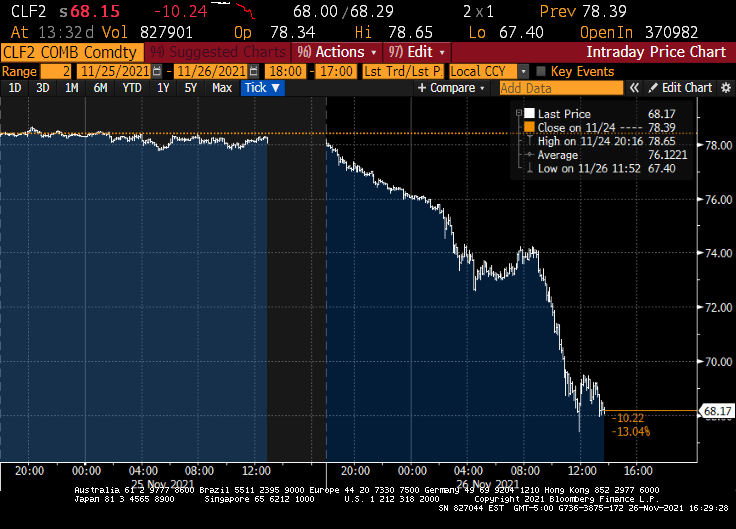

And West Texas Intermediate crude futures are down to 68.17 from 78.39. No Jen Paski, this isn’t due to Cousin Eddie (Biden) releasing the Strategic Petroleum Reserve (SPR).

Maybe it was all the tryptophan released by eating turkey.

Its Thanksgiving in the USA! Confession: I don’t like turkey. Prime rib with horseradish sauce? You bet!!

Anyway, Treasuries ended mixed Wednesday with the yield curve sharply flatter after a raft of U.S. economic data and minutes of the November FOMC meeting bolstered expectations for an earlier start to Fed rate increases. Two- and 5-year yields reached YTD highs, and 5s30s spread reached narrowest since March 2020.

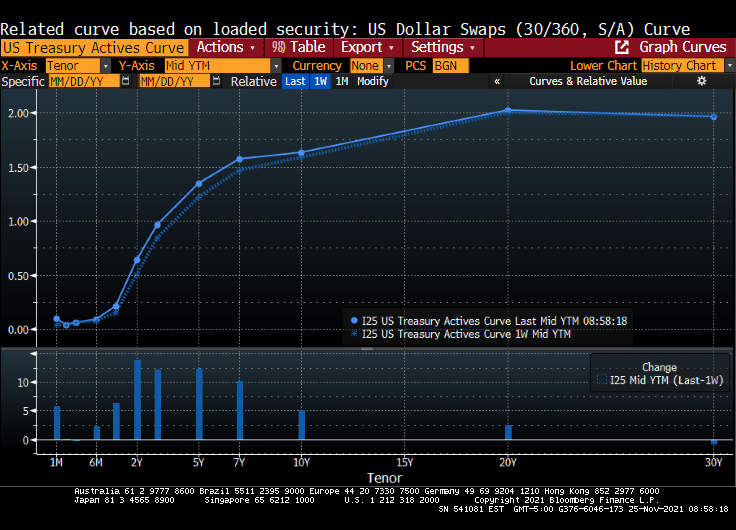

Over the past week, the Treasury actives curve rose 13.85 basis points at the 2 year tenor.

Yields ended richer by ~6bp across long-end of the curve, while front-end cheapened almost 3bp; 2s10s flattened more than 5bp, 5s30s more than 6bp; 10-year yields shed ~3bp to ~1.635% Release of Nov. 2-3 FOMC meeting minutes drew minimal market reaction, as flatter curve held its shape.

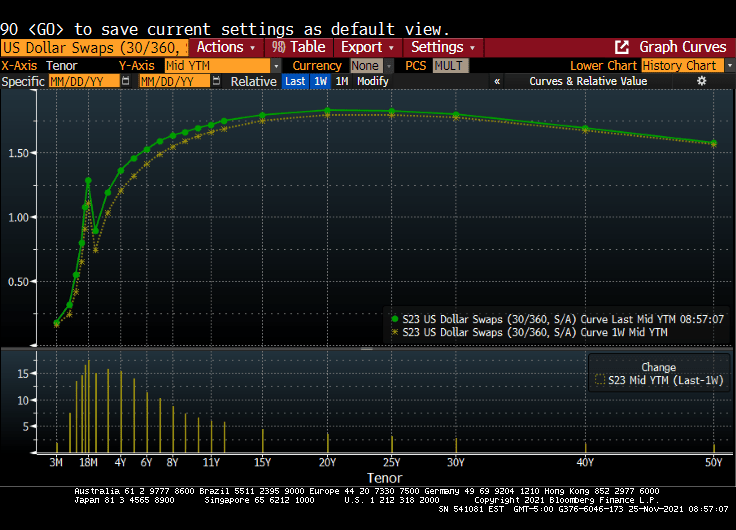

The US Dollar Swaps curve rose from the previous week as well.

Minutes said participants considered elevated inflation as likely transitory, “but judged that inflation pressures could take longer to subside than they had previously assessed”

Earlier, front-end and belly sold off after a heavy slate of U.S. economic data including the lowest initial jobless claims tally since 1969

Also during U.S. morning, Fed’s Daly said she would support accelerated tapering of asset purchases, which added to pressure across front-end Treasuries

Subsequently, eurodollars traded heavy over the session as rate-hike premium continued to ramp up in 2022 and 2023; overnight index swaps showed 30% chance of a March hike, while around three hikes — or 75bp — were priced in by the end of next year

Renters in the US are getting clobbered by inflation.

The US Zillow Rent Index All Homes YoY + CPI YoY is one measure of renter misery.

The classic misery index (CPI YoY + U-3 unemployment rate) is 10.80%.

Then there is inflation in food prices, gasoline, heating oil, natural gas, etc.

While Biden is releasing the Strategic Petroleum Reserves (SPR) in order to mitigate the problem that he created by terminating the energy pipelines and oil/natural gas drilling permits in the name of “Going Green!” But on the announcement of tapping the SPR, crude oil futures actually rose.

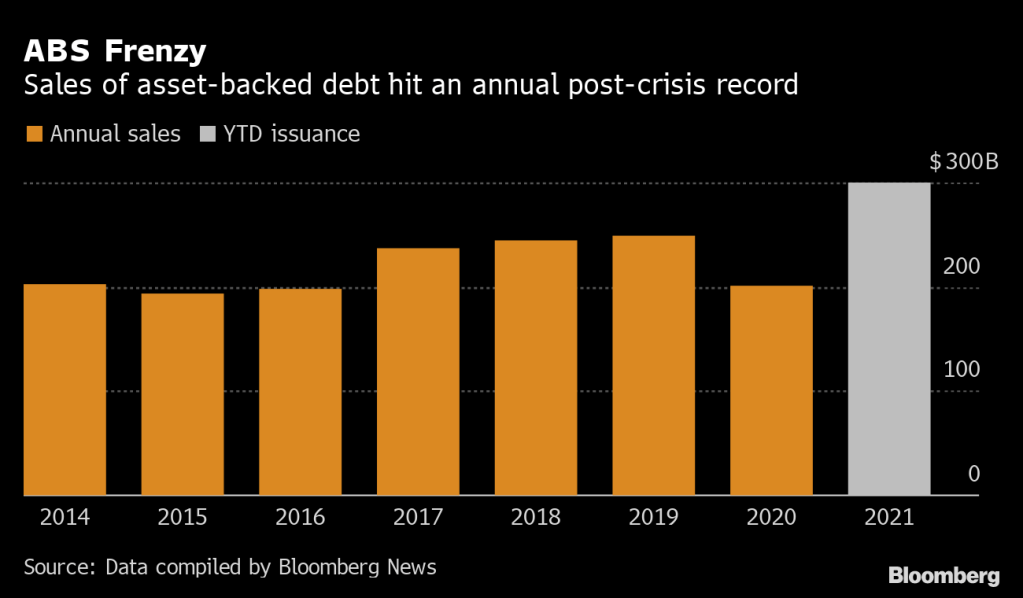

I remember the surge in securitization of loans, receivables, etc during the housing bubble of the mid-to-late 2000s. Today seems like 2007 all over again.

(Bloomberg) — Bankers are repackaging everything from fast food franchises to fitness-center fees into bonds at the fastest clip since the global financial crisis as investors chase yield and inflation protection.

This year’s sales of U.S. asset-backed securities have already surpassed $300 billion, according to data compiled by Bloomberg — and more is expected by year-end. Post-crisis issuance records have also been set in private-label commercial mortgage bonds and collateralized loan obligations, which are also seen accelerating.

“Solar, consumer loans, container lease and whole business transactions to some degree all offer attractive yields and spreads,” said Dave Goodson, head of securitized credit at Voya Investment Management. “These so-called esoteric sectors remain well supported with plenty of money to invest.”

On Monday, Self Esteem Brands, a franchiser of businesses including its flagship gyms Anytime Fitness, priced a $505 million ABS that was backed by franchise agreements, royalties and fees. In whole business securitizations like these, companies mortgage virtually all their assets.

Last month, fried chicken restaurant chain Church’s Chicken sold a $250 million securitization backed by franchise and royalty collateral. Golden Pear Funding recently securitized litigation fees related to financial settlements on everything from personal injury cases to wrongful convictions. And Oasis Financial priced a similar deal linked to payments on medical liens.

Then we have this headline that will send chills through the CMBS market for retail space, particularly at a time when commercial real estate (particularly RETAIL) are trying to recover from COVID lockdowns and the growth of online shopping.

“Retailers Sound Alarm on Organized Theft as States Warn of Rise”

Retailers say shoplifting is getting more brazen in the U.S.: A California Nordstrom store was recently hit by a flash mob of more than 80 people who made off with designer goods, while more than a dozen people pilfered from a Louis Vuitton location in a suburb of Chicago.

On Tuesday, the impact of shoplifting reached Wall Street, with Best Buy Co. shares plunging after the electronics retailer said widespread theft contributed to a decrease in one gauge of profitability. Last month, Walgreens said it would close five San Francisco stores after theft rates there spiked.

Seemingly, no one learns from history. Or as the zen master Yogi Berra once said “It’s like déjà vu all over again.”

Or “You better cut the pizza in four pieces because I’m not hungry enough to eat six.”

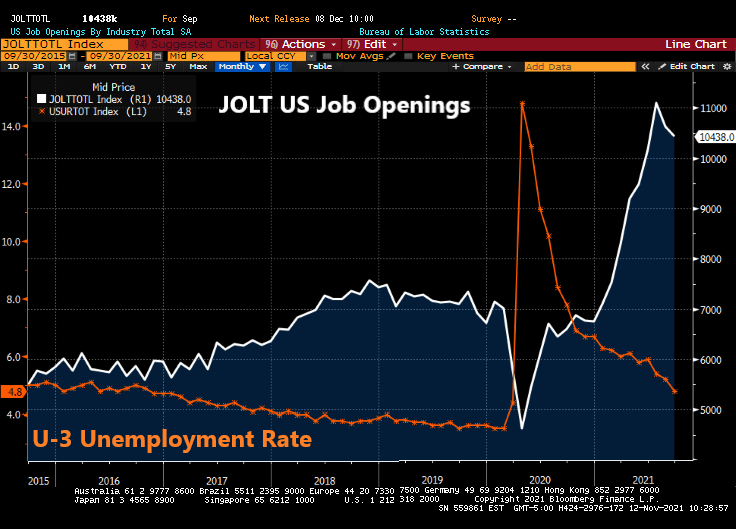

Is the US at full employment? That is, is the US at REALISTIC full employment? And if the US is at realistic full employment, why is The Federal Reserve keeping rates at 25 basis points??

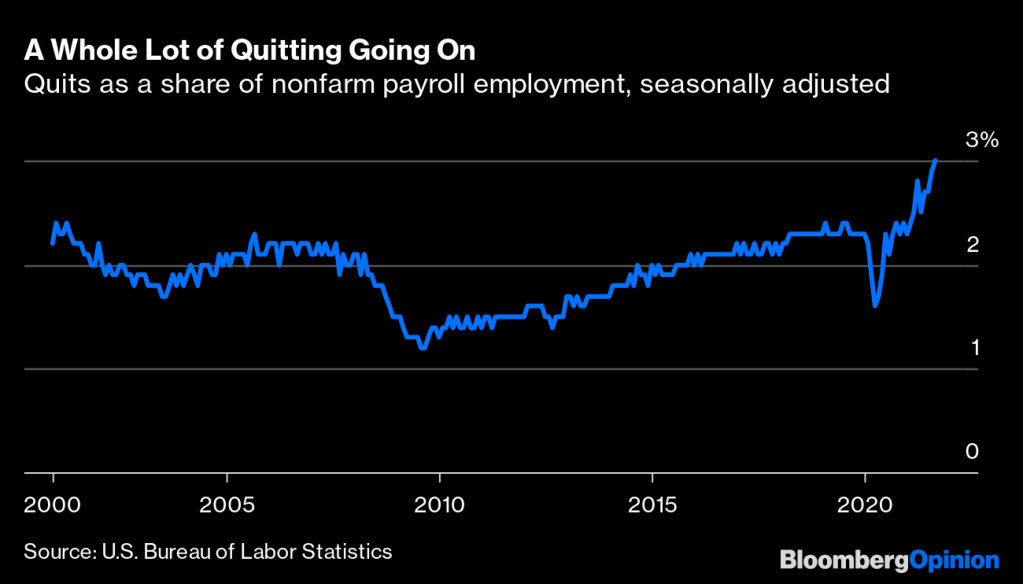

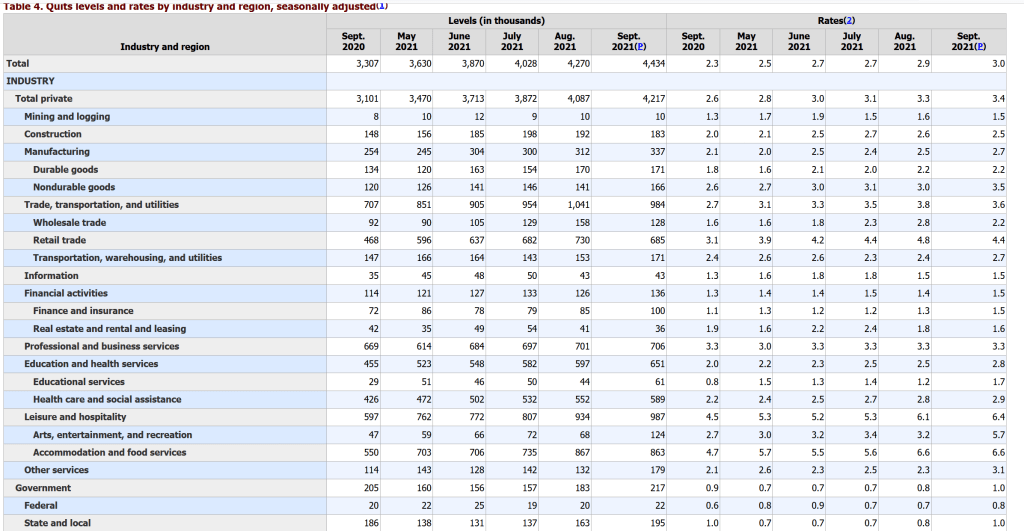

Let’s start with the “quits” data. An estimated 3% of American workers quit their jobs in September, the Bureau of Labor Statistics reported last week.1That’s the highest percentage since the BLS started keeping track two decades ago.

Front-line and low-wage workers are leaving at rates higher than historical norms while higher-paid office workers aren’t. College-educated workers haven’t been quitting or dropping out of the workforce at higher rates than before the pandemic, but less-educated workers have.

The quits rate in professional and business services was just 0.4 percentage points higher in September than before the pandemic in February 2020. In financial activities it was unchanged. In the information sector, made up of telecommunications, publishing, broadcasting, motion pictures, software and most internet companies, the quits rate was down 0.3 percentage points.

The biggest increases in quit rates were in sectors such as leisure and hospitality where office workers are few, working remotely seldom an option and wages low. Within manufacturing, the quits-rate increase has been much bigger in lower-paying nondurable goods (of which food manufacturing is the biggest part) than in higher-paying durable goods.

In particular, fast food restaurants are offering above minimum wage salaries to attract workers. Burger King was even offering college tuition (not to University of Chicago, but to the local community college).

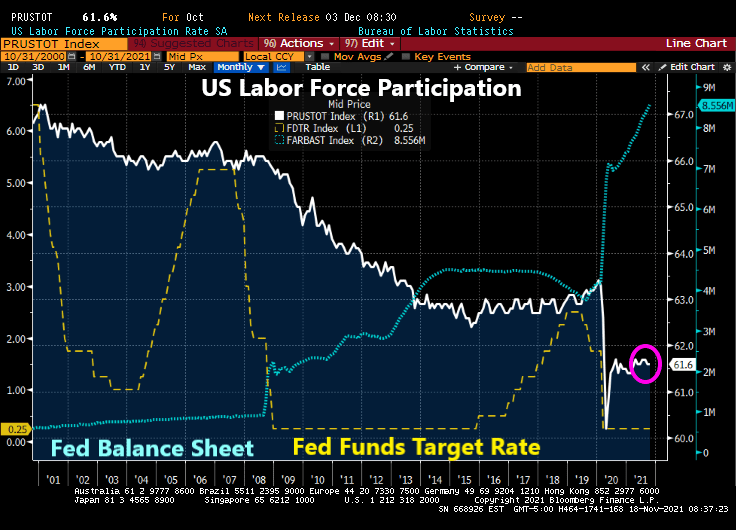

Labor force participation crashed with COVID and has struggled to recover, despite the staggering monetary stimulus. If this a sign that the US is at full employment (or very difficult to entice workers to enter and stay in the labor force)?

Nothing has been the same since the housing bubble of the 2000s, the resulting banking meltdown and the takeover of the economy by The Federal Reserve.

And since the 2000s housing bubble and financial crisis, The Federal Reserve has taken control of the economy resulting in M2 Money Velocity crashing to historic lows.

Policy blunders perpetrated by the Biden White House have made a bad problem worse.

For instance, oil prices are higher for two reasons. First, U.S. production has declined by about two million barrels per day since 2019, even as demand has recovered from the COVID-19-induced downturn. Oil markets are global, so the fall-off in output would not necessarily jack prices up, but our declining output needs to be offset by an increase elsewhere.

Enter OPEC, which has not restored output to the level necessary to bring down prices, despite repeated pleas from Biden.

Meanwhile, Biden has done a lot to discourage a resurgence in U.S. drilling and production. He has cancelled pipelines, threatened oil and gas producers with higher taxes, taken promising acreage out of play, such as the Arctic Natural Wildlife Refuge, slow-walked leasing and new drilling permits and, most recently, imposed new methane-curbing rules that make drilling more expensive.

What sensible person would invest in the oilfield in the face of such unrelenting hostility? Drilling activity is up, but nowhere near where it should be at $82 per barrel oil.

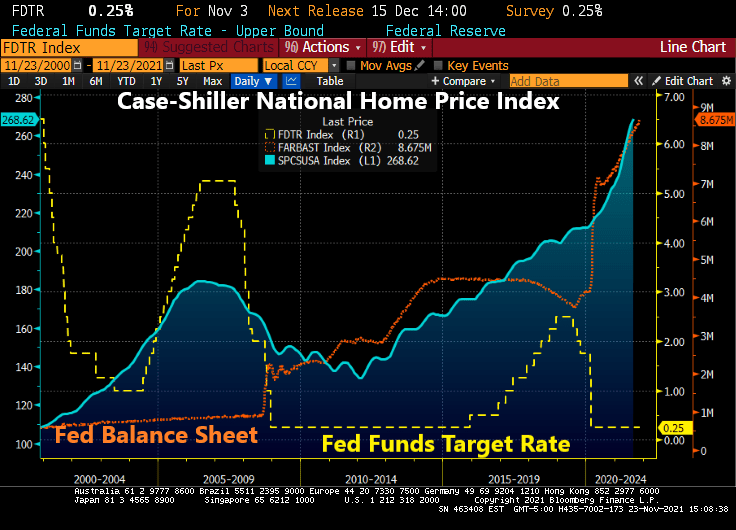

Another boost to inflation came from housing. With “shelter” accounting for some 40 percent of the CPI, economists have warned that fast-rising home prices would eventually seep into higher inflation readings. In October, we saw this occur, with the increase in the cost of shelter accelerating to 0.5 percent from September, an annualized rise of 3.48 percent. The CPI owners equivalent rent of residence rose to 3.13% YoY. Too bad home prices are increasing at almost 20% YoY.

One reason home prices have been increasing at nearly 20 percent per year is that the Federal Reserve has continued to buy up $15 billion worth of mortgage-backed bonds each month, keeping mortgage rates artificially low. The result has been a booming market, driving home prices, and now rents, higher.

At long last, the Federal Reserve has announced it will begin to throttle back its bond-buying program, including the purchases of mortgage-backed bonds. Critics think the Fed is behind the curve, having seriously underestimated price pressures.

Biden does not control the Fed, but he has made no secret of his preference for the easy money policies that have helped prop up the economy, and the stock market. Fed Chair Jerome Powell’s term ends in February; Biden has recently interviewed not only Powell but also Fed Governor Lael Brainard, a known dove and Obama appointee, for the position.

That these are the only two candidates he seems to be considering sends a clear signal. He will choose growth over stability, even if it means that inflation continues to accelerate. Unhappily, Powell is listening.

Finally, Biden has not only encouraged monetary excess, but has also endorsed big-spending packages that have put money in consumers’ pockets but also kept workers on the sidelines. The biggest shortage we have in this country today is labor. The labor participation rate is mired at 61.6 percent, 1.7 percentage points below the level in February 2020.

Studies have shown that the slew of benefits contained in the Cares Act and subsequent relief bills, including incremental unemployment benefits, expanded child tax credits and rent moratoriums, have offered Americans up to $100,000 per year while not working. These payments may have been necessary early in our recovery from the pandemic, but no longer are needed.

And then people are surprised that grocery prices are getting so f&^*ing high???

Wu-Xia employs an approximation that makes a nonlinear term structure model extremely tractable for analysis of an economy operating near the zero lower bound for interest rates. It can be used to summarize the macroeconomic effects of unconventional monetary policy (ZIRP + QE). The Shadow Rate is now -1.7021%.

And you wonder why we have inflation and house prices going into orbit?

With inflation also going into orbit, we see that breakeven 10 year inflation rate rising above the 5Y5Y (nominal forward 5 years minus US inflation-linked bonds forward 5 years). In other words, the US has abnormally high inflation and is expected to grow and NOT be transitory.

The Shadow knows … that the US is hyperstimulated. And inflation isn’t going away anytime soon.

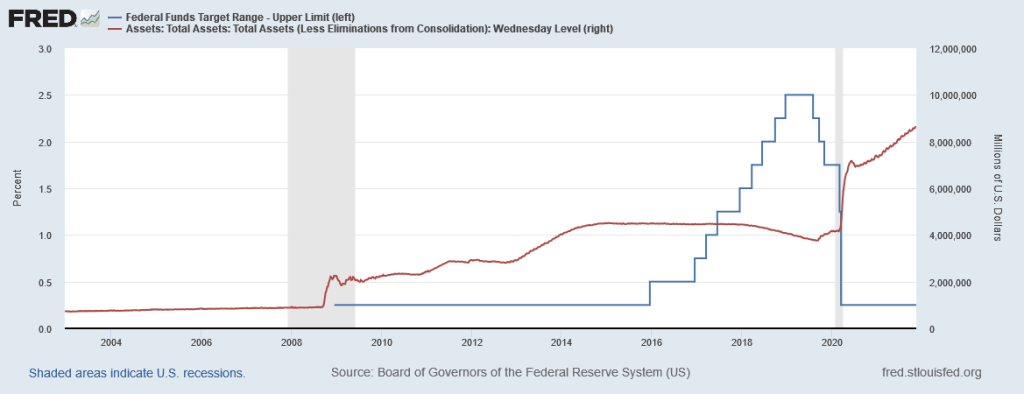

With The Federal Reserve leaving its target rate at 0.25%, but hinting at a tapering (slowdown) of asset purchases, I thought it would be good to present where The Fed sits at the moment.

You can see the rise in the effective Fed Funds rate from 2016 to early 2020, then KABOOM! COVID struck, the effective Fed Funds rate crashed while The Fed dramatically increased their purchases of Treasuries and Agency MBS. Both Treasury and Agency MBS purchases are projected to decline by mid-2022. The Fed’s target rate (purple line) is project to rise to 1% after 2023.

Where SHOULD The Fed Funds Target rate be? How about 8.80% instead of 0.25%.

So we still have over-stimulypto with The Fed projected to raise rates at a snail’s pace.

Face it, Wall Street wants interest rates low, even if inflation burns out of control.

You must be logged in to post a comment.