Heartaches By The Number … for American households and mortgage lenders as The Federal Reserve begins FINALLY removing monetary stimulus.

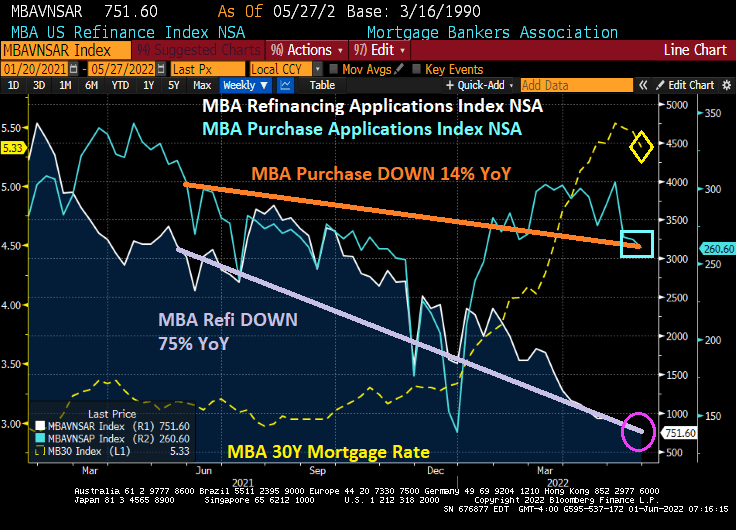

Mortgage applications decreased 2.3 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending May 27, 2022.

The Refinance Index decreased 5 percent from the previous week and was 75 percent lower than the same week one year ago.

The seasonally adjusted Purchase Index decreased 1 percent from one week earlier. The unadjusted Purchase Index decreased 2 percent compared with the previous week and was 14 percent lower than the same week one year ago.

Under Biden, mortgage refi applications are down -82.4%, purchase applications are down -7.5% and mortgage rates are up +80.7%.

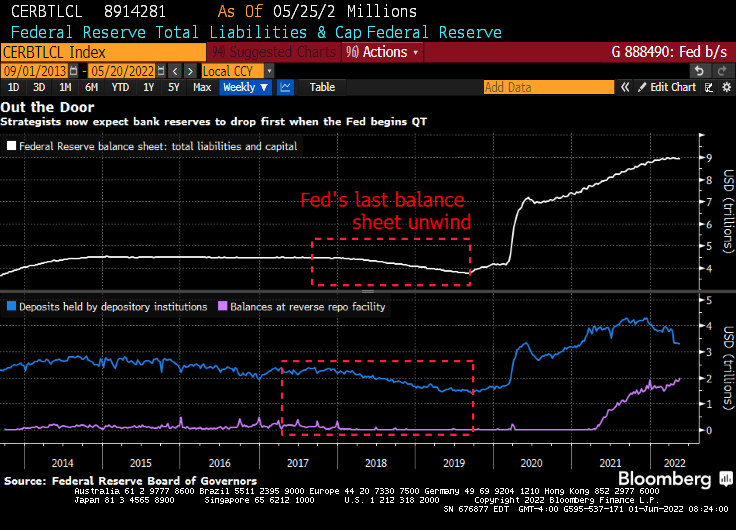

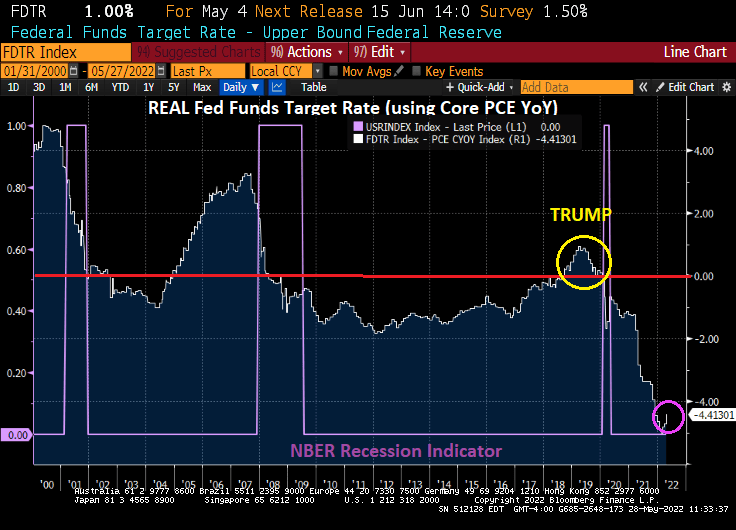

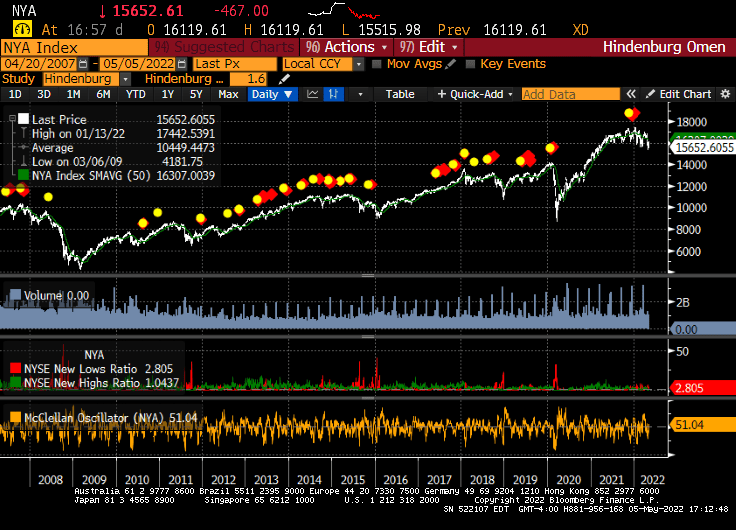

Then we have this headline: “Fed Starts Experiment of Letting $8.9 Trillion Portfolio Shrink”

The Fed is capping monthly runoff at $47.5 billion — $30 billion for Treasuries and $17.5 billion for mortgage-backed securities — until September. Those thresholds will then double to a combined $95 billion. That compares to a peak of $50 billion a month when the Fed performed the exercise starting in 2017.

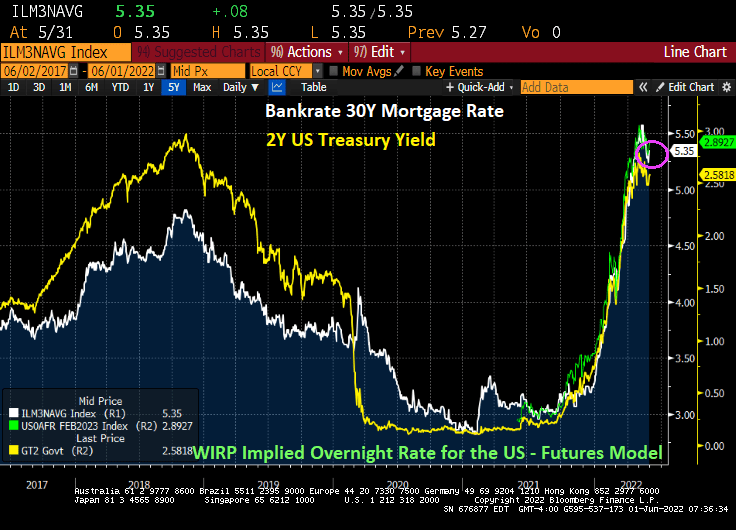

As expectation of Fed rate hikes increase, mortgage rates have soared like Tom Cruise’s Super Hornet aircraft from Top Gun: Maverick climbing over the steep mountain.

And mortgage rates are up a bit today.

Meanwhile, The Federal Reserve begins shrinking their balance sheet for the first time since Yellen and company started shrinking it under Trump.

You must be logged in to post a comment.