The Biden Administration and The Federal Reserve together should be called “The Cooler Kings” in that their policies are putting a Big Chill on the mortgage market and equities.

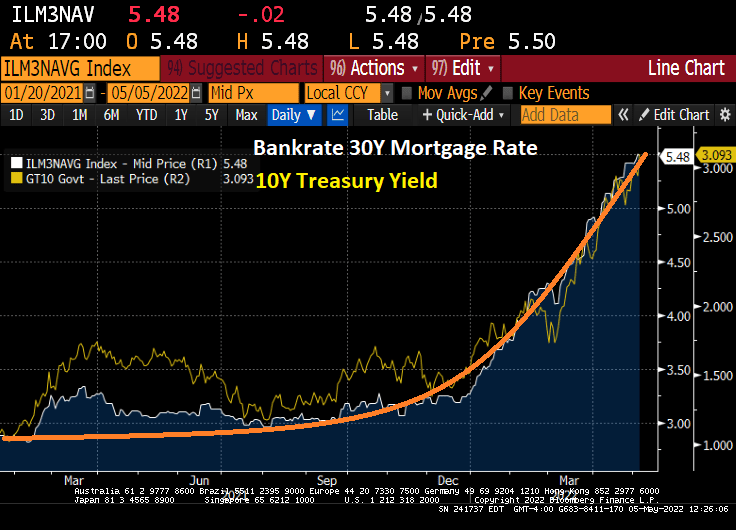

Mortgage rates are skyrocketing thanks to the Federal Reserve.

The 30-year fixed-rate mortgage averaged 5.27% for the week ending May 5, according to data released by Freddie Mac FMCC, -1.62% on Thursday. That’s up 17 basis points from the previous week — one basis point is equal to one hundredth of a percentage point, or 1% of 1%.

House price growth to wage growth is below the all-time high, but remains above housing bubble levels of 2005-2007.

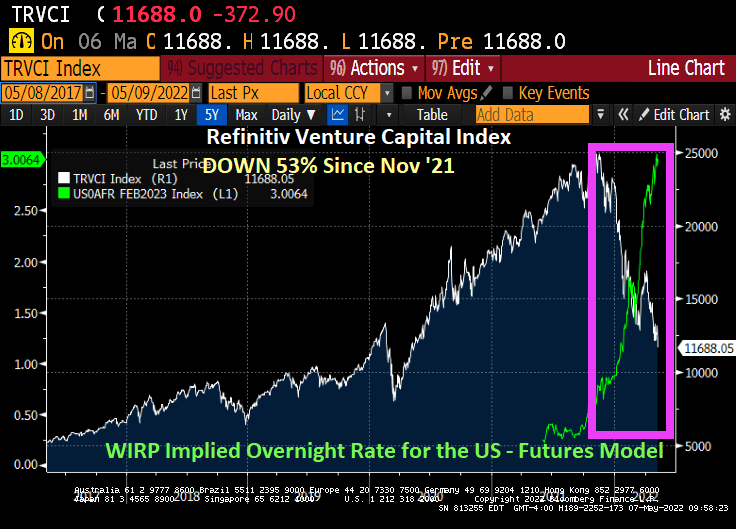

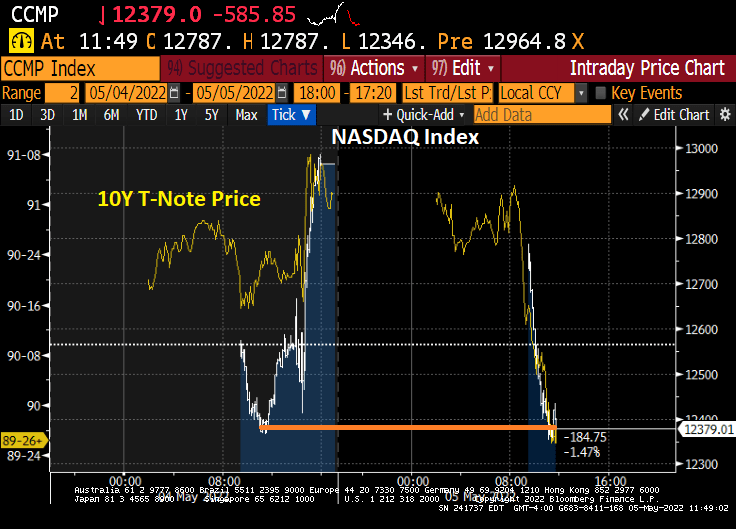

The Refinitiv Venture Capital Index is down 53% since November ’21 as The Fed cranks up interest rates.

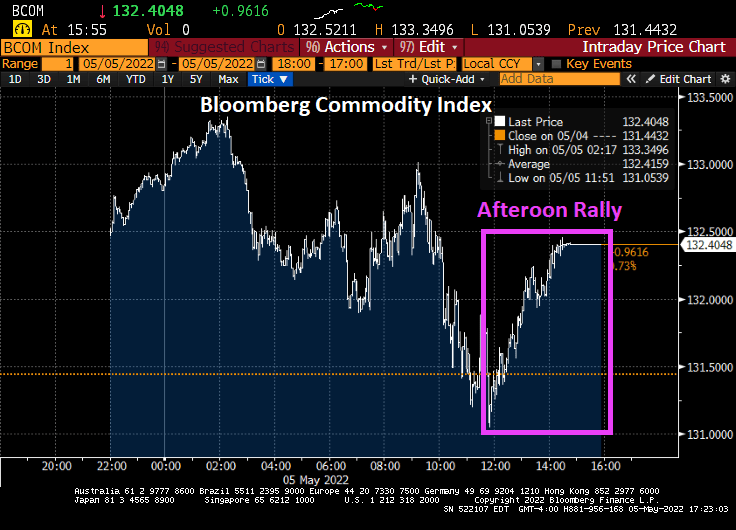

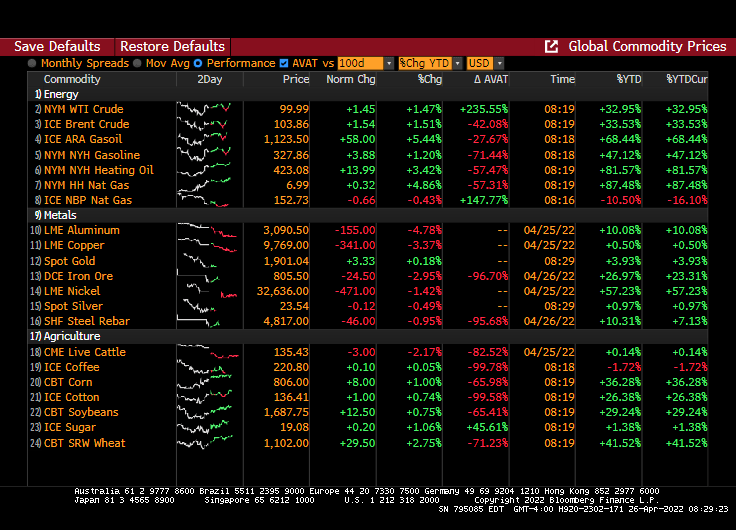

Well, at least commodities are soaring under “The Cooler Kings.” Pretty much everything else is sucking wind.

The question, of course, is whether The Federal Reserve will back off its plans to aggressively raise interest rates in lieu of crashing stock market, venture capital, and possibly home prices.

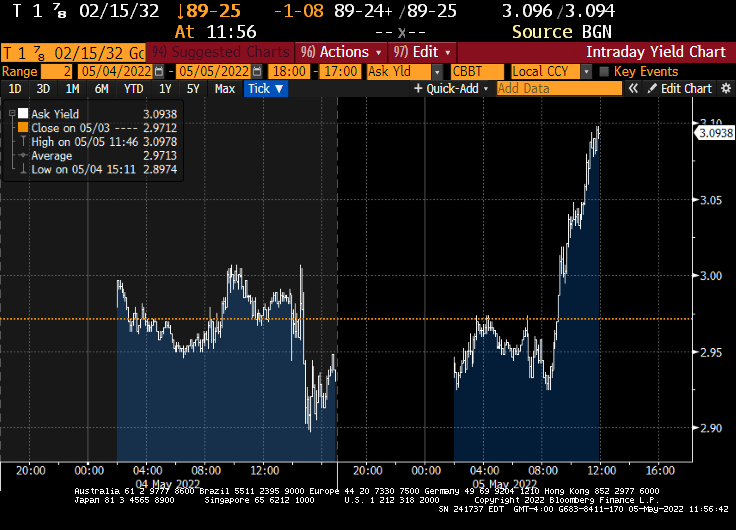

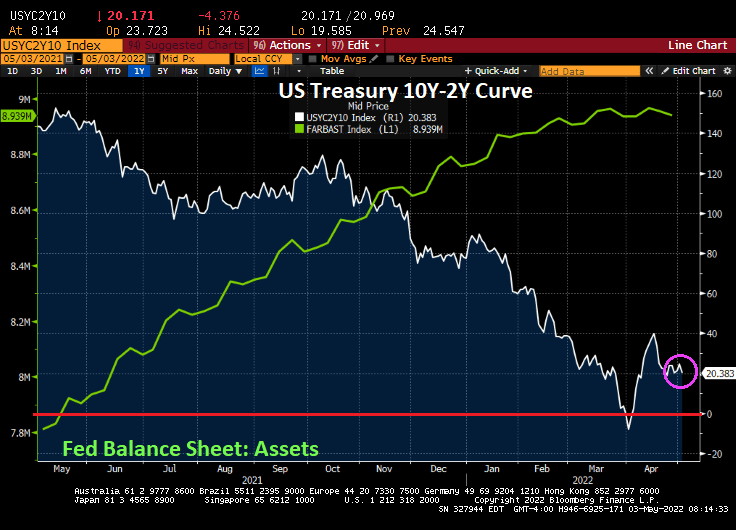

The U.S. Treasury market is showing signs of stress that may have implications for whether the curve keeps steepening.

Over the past month the curve has retraced from an inversion to a steepening driven by a surge in yields on benchmark 10-year bonds. That has led to interesting outlier indications, as traders weigh the outlook for Federal Reserve interest rate increases and inflation.

The US Treasury yield curve has settled-in at 20.383 bps (effectively zero) as The Fed continues its war on inflation.

On the SOFR front, we see SOFR Coupons being slow to benefits from Fed rate hikes. So, SOFR Coupons are behaving like Stouffer’s lasagna, frozen and tasteless.

On the other hand, mortgage rates continue to soar on EXPECTATIONS of Fed rate hikes.

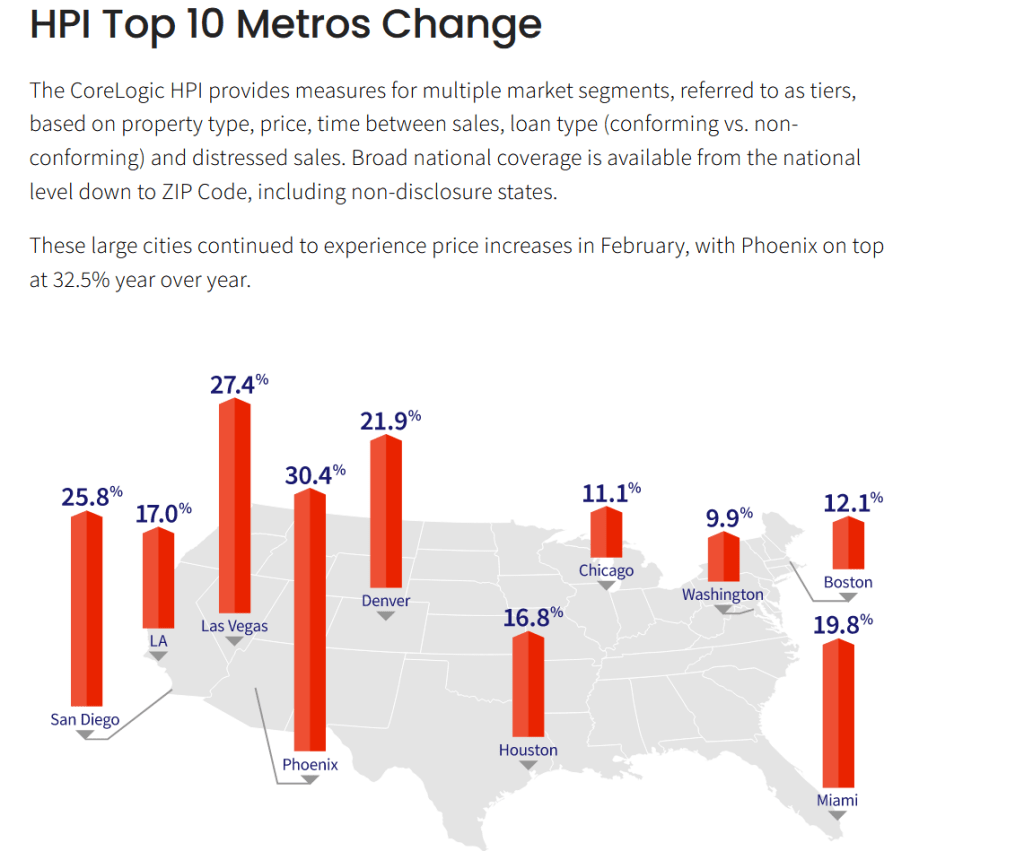

Phoenix AZ leads the top ten at 30.4% with Washington DC lagging at 9.9%.

So, its official. The Federal Reserve is best exemplified by former Yankee/Mets first baseman “Marvelous” Marv Throneberry. When players presented Mets’ manager Casey Stengel with a birthday cake but neglected to give piece of cake to Throneberry, Stengel replied to Throneberry when asked why no cake, “Because I was afraid your were going to drop it.”

Just like The Federal Reserve, the honorary Marv Throneberry of the the global economy.

M2 Money Velocity (GDP/M2 Money) peaked in Q3 1997, but after several bouts of Fed money printing, M2 Money Velocity is near the all-time low at 1.1216 In Q1 2022. And M2 Money stock is still growing at a torrid pace of 9.9% YoY. But the massive overreaction of The Federal Reserve in response to the Covid outbreak has led to near zero money velocity.

Now with The Federal Reserve considering removing the monetary stimulus, what will happen to US GDP left to survive on its own?

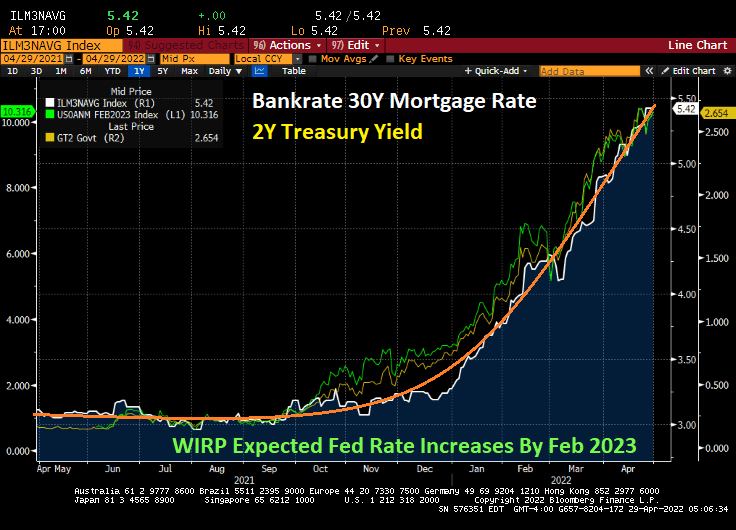

An example of how The Fed’s expected tightening of monetary policy can be seen in the meteoric rise in mortgage rates.

So, the US has hit terminal money velocity. I wish The Fed lots of luck going forward.

Is Charlie Sheen the Chairman of The Federal Reserve Board of Governors?? That must be Lael Brainard falling out of the sky with Charlie Sheen (aka, Jerome Powell).

I hope America’s foreign policy wizards (Biden, Harris and Blinken) weren’t relying on the Russian Ruble staying pulverized, because the Ruble (relative to King Dollar) has regained all its losses.

On the other hand, the Japanese Yen and Chinese Yuan have crashed harder than Biden’s popularity.

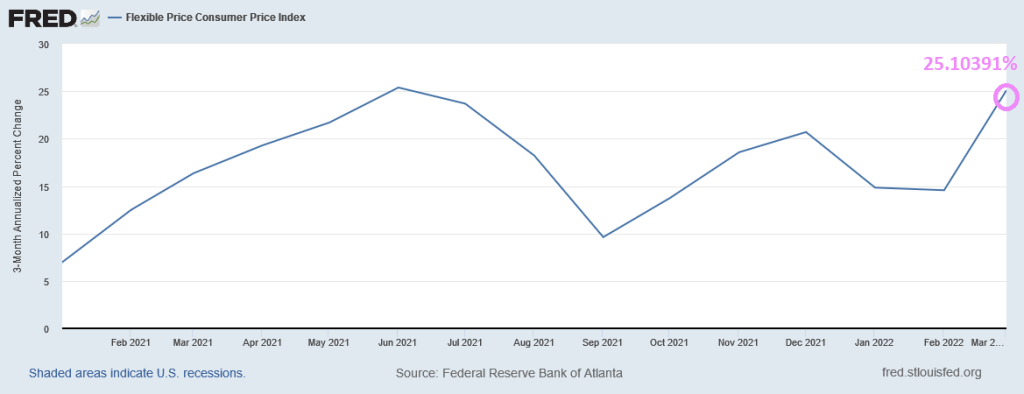

Actually, The Atlanta Fed’s flexible price inflation rate is 25%, up from 3.90% Pre-Joe.

Perhaps Biden, Harris and Blinken think Putin is a pasta sauce.

Here is Dvorak’s New World Symphony, an appropriate piece the global turmoil that has taken place after Russia’s invasion of Ukraine.

Here is the ratio of the S&P 500 index against the Bloomberg Commodity Price Index. This ratio is plotted against The Federal Reserve’s balance sheet of assets. Notice the decline in the Commodity Ratio in 2022, even ahead of the Russian invasion of Ukraine.

Global currencies, on the other hand, have been really crushed since the Russian invasion of Ukraine. The Japanese Yen, China’s Renminbi and Europe’s Euro relative to the US Dollar are falling due to a variety of reasons. Covid lockdown in China, Japan’s insistence on monetary easing while other Central Banks are tightening and the Euro with Russia threatening nuclear war.

WTI Crude is back to $100 a barrel. Critical metals are down today related to a slowing global economy and wheat is up 2.75%.

Could it be that US Dollar hegemony is nearly over and commodity-backed currencies are the way of the future?

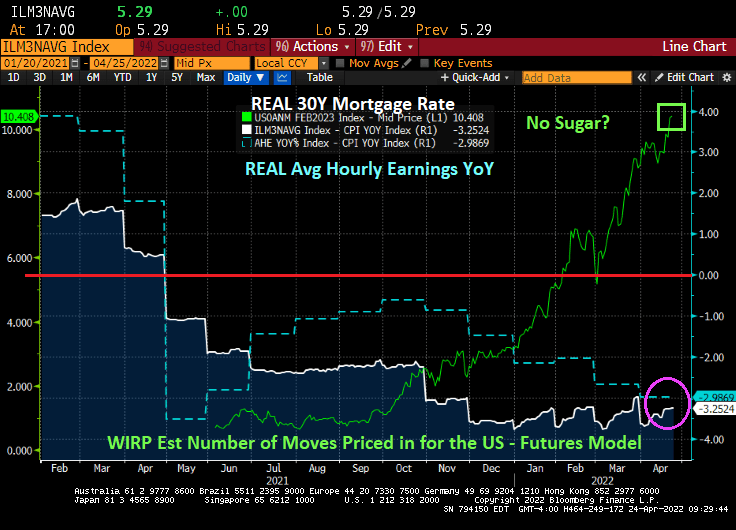

As The Fed sings “No sugar tonight” exemplified by the number of expected Fed rate hikes by February 2023 has grown to 10.4. Mortgage rates are now the highest since 2009, but inflation is the highest in 40 years. The result? The REAL 30-year mortgage rate is -3.25%.

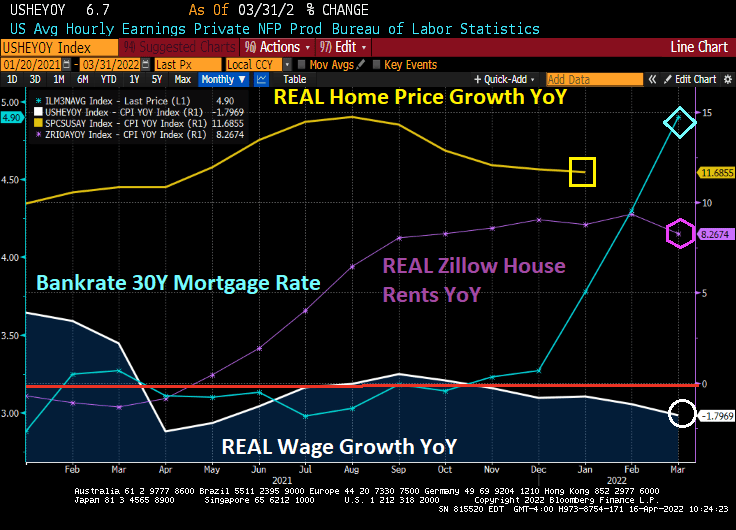

REAL average hourly earnings are now a terrible -2.99% YoY thanks to the worst inflation in 40 years. REAL home prices are growing at 11.8% YoY.

Traders are betting that even with the Fed boosting its target for the federal funds rate by 2.5 percentage points this year to 3% won’t be enough to get the inflation rate back down to 2% over the next decade from around 8.5% currently.

In nominal terms, mortgage rates are seemingly trying to rise to 2007 levels (6.5%). But the gap between the 30-year mortgage rate and Fed Funds target rates is back to 2009 levels.

Talk about Fed and Fed government OVER stimulypto! Even REAL US home prices grew at 12% YoY pace while the REAL Fed Funds Target rate is -8.04%.

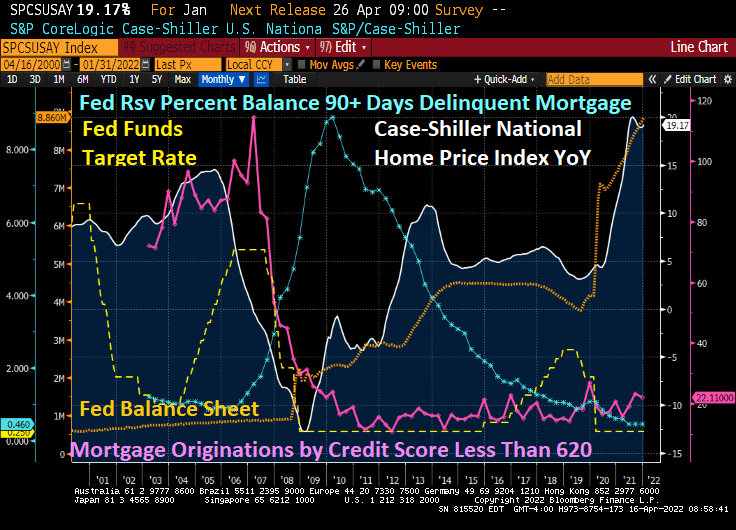

The book and movie “The Big Short” revolved around the 2005-2007 housing bubble driven by lending to borrowers with subprime credit (and little or no underwriting). As we know, Bear Stearns, Lehman Brothers and other investment banks too large positions in subprime asset-backed securities (SABS) that became highly toxic once the demand for high-yield subprime ABS dried up. The decline in US home prices coupled with soaring 90-day mortgage delinquencies led to the failure of Bear Stearns and Lehman Brothers along with Fannie Mae and Freddie Mac being put into conservatorship by their regulator.

Fast forward to today. Mortgage originations by credit scores of 620 or less have shriveled while home price growth YoY is even higher than the subprime mortgage crisis of 2005-2007. So, is the US facing another “Big Short” scenario? Yes and no.

The answer is no in that lenders have tightened their credit box sufficiently so that investment banks are no longer buying large quantities of subprime credit paper. The answer is yes if we consider that the current housing bubble is fueled by extraordinary monetary stimulus due to Covid (as well as rampant Federal government stimulus spending).

Following the Federal Reserve of Dallas’ lead, here is a chart of REAL home price growth YoY against REAL average hourly earnings YoY. I added REAL Zillow house rents YoY as well.

Look at the affordability gap during the Subprime Bubble of 2004-2006 and then the Fed Bubble of 2020 to today. Both bubbles show a disconnect between REAL home prices and REAL wages. REAL Zillow home rents are not as high as REAL home price growth, but still how a huge gap in rent affordability.

So, what can upset the apple cart? How about Jay and The Gang jacking up mortgage rates making home affordability even worse (unless it slows home price growth).

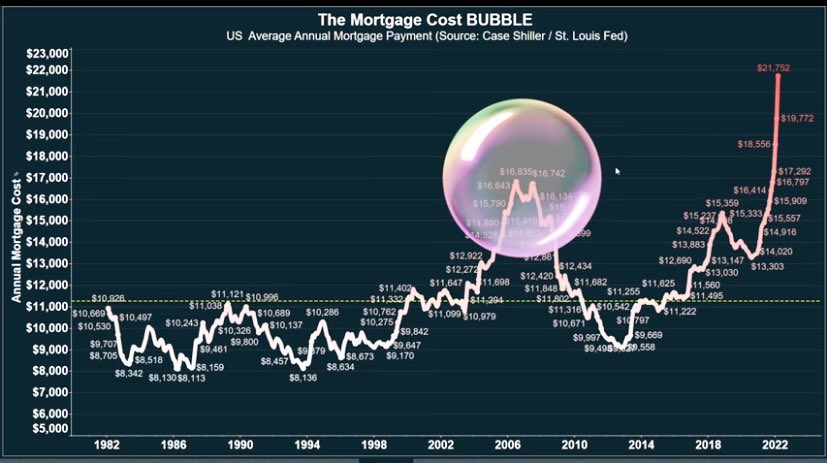

Thanks to The Fed’s propose quantitative tightening, mortgage rates are soaring and mortgage costs along with them. Mortgage costs, thanks to The Fed driving up housing prices AND mortgage rates, are substantially higher than during the subprime mortgage housing bubble.

The Fed’s whipsaw approach helped crash home prices during the subprime mortgage crisis by dropping rates too fast at first (helping to ignite a housing bubble) then raising rates too fast (helping to crash housing prices).

WASHINGTON (AP) — Long-term U.S. mortgage rates continued to climb this week as the key 30-year loan rate reached 5% for the first time in more than a decade amid persistent high inflation.

The average 5% rate on the 30-year mortgage was up from 4.72% last week, mortgage buyer Freddie Mac reported Thursday. The average rates in recent months have been showing the fastest pace of increases since 1994. By contrast, a year ago the 30-year rate stood at 3.04%.

The average rate on 15-year, fixed-rate mortgages, popular among those refinancing their homes, jumped to 4.17% from 3.91% last week.

Yet The Federal Reserve’s balance sheet keeps on growing.

You must be logged in to post a comment.