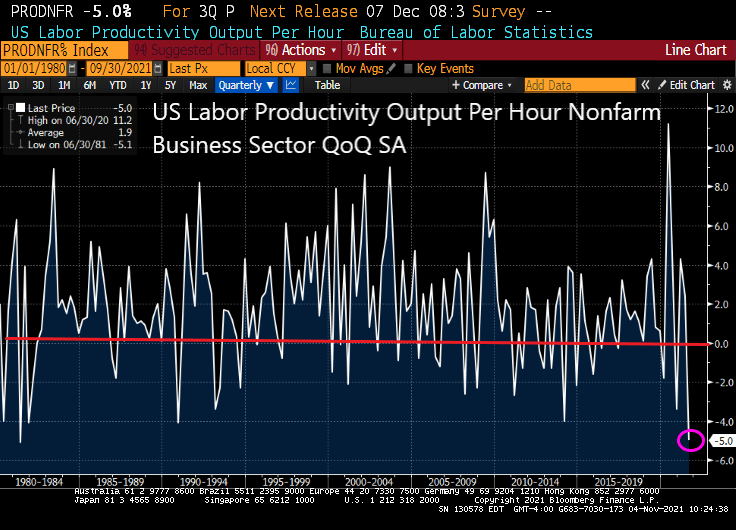

The last time we saw US labor productivity out per hour this low was in 1981 when President Reagan inherited stagflation from President Jimmy Carter.

As unit labor costs soar +8.3%.

Any wonder that the 1% have been doing so well relative to the bottom 50% in terms of wealth since entrance of The Fed in 2008 with zero-interest rate policies (ZIRP) and assets purchases (QE). And also after Covid struck.

“That will be $10,000 for your Big Mac, fries and a soda, please!”

From The Land of 1,000 Excuses, The Federal Reserve Open Market Committee (FOMC) will announce … no rate increases and a slight reduction in their assets purchases (Treasuries and Agency MBS). The announcement will be at 2pm EST (not at The Midnight Hour).

The Federal Open Market Committee is all but certain to hold rates near zero after a two-day policy meeting and announce a $15 billion monthly reduction in bond buying from the current $120 billion pace, judging that the test for tapering has been met as the economy heals from Covid-19.

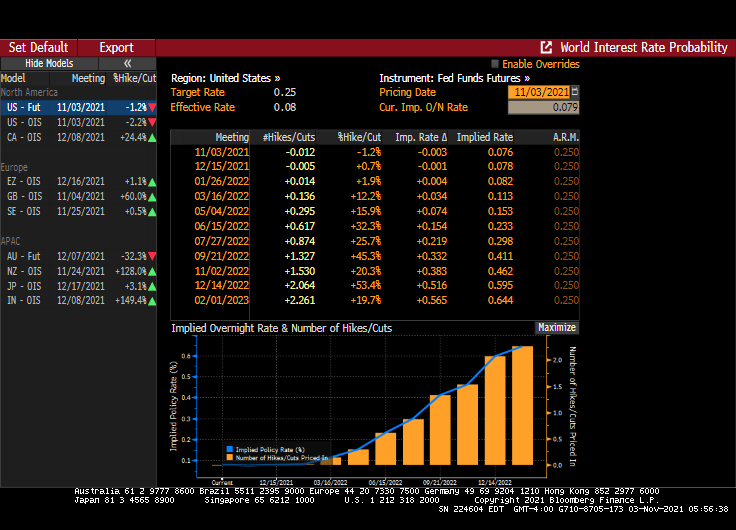

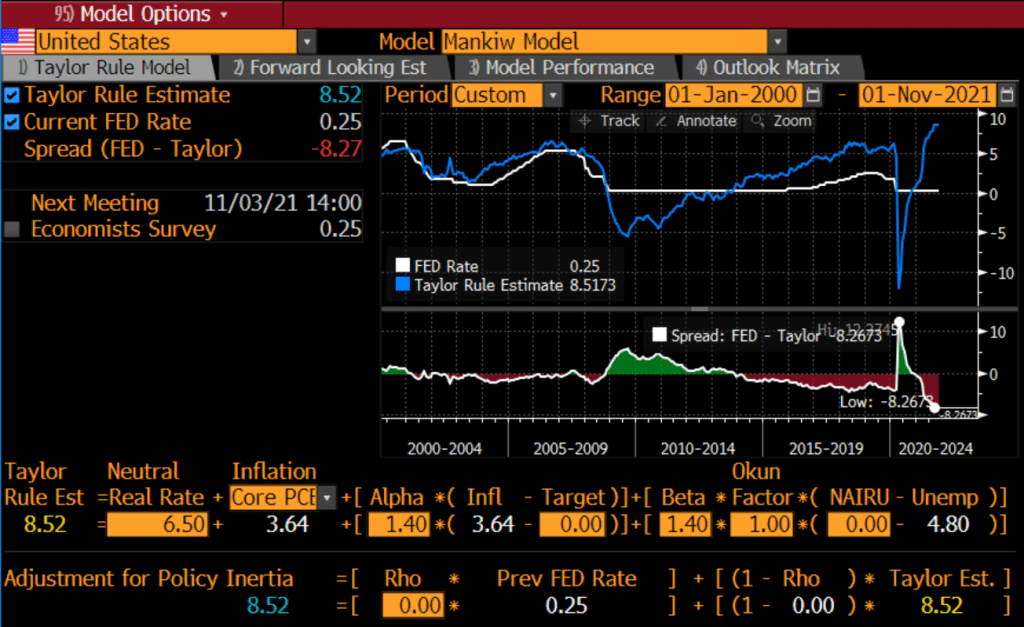

There are two rate increases baked into the Fed Funds futures data as of today.

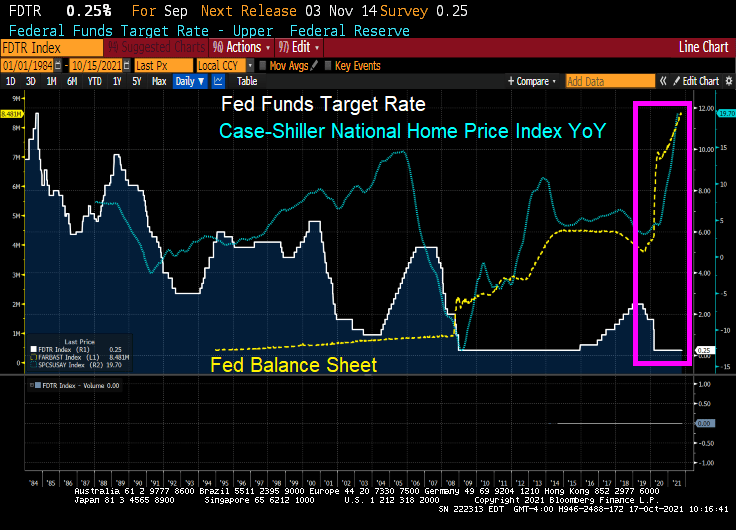

But a troubling aspect of The Fed’s monetary policy is that M2 Money Velocity is near the lowest in history and The Fed has been binge printing. What this means is that money printing has had little impact on GDP growth.

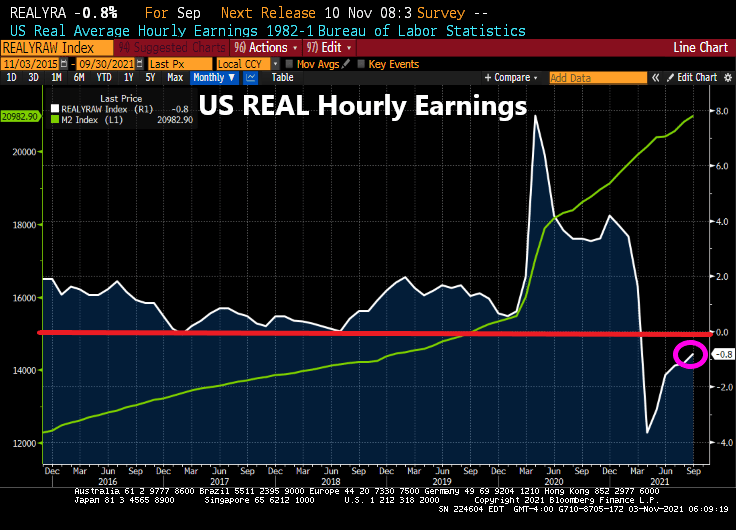

When The Fed mentions the post-COVID recovery, I hope they mention that REAL hourly wage growth is NEGATIVE.

And REAL S&P 500 earnings yield is also negative.

The Fed will likely to blame TRANSITORY effects such as the backed-up port traffic in Long Beach for rising prices rather than their flooding the markets with too much money.

But The Fed will continue to print, even though they will blame bottlenecks for inflation rather than their haphazard drowning of the economy in money.

Given that The Fed is monetizing the reckless spending by The Federal government, particularly Pelosi’s latest budget, we will see coordination between Chairman Powell and Treasury Secretary Janet Yellen (aka, Mustang Sally).

Call Jerome at 634-5789 to tell him to raise rate to normal levels.

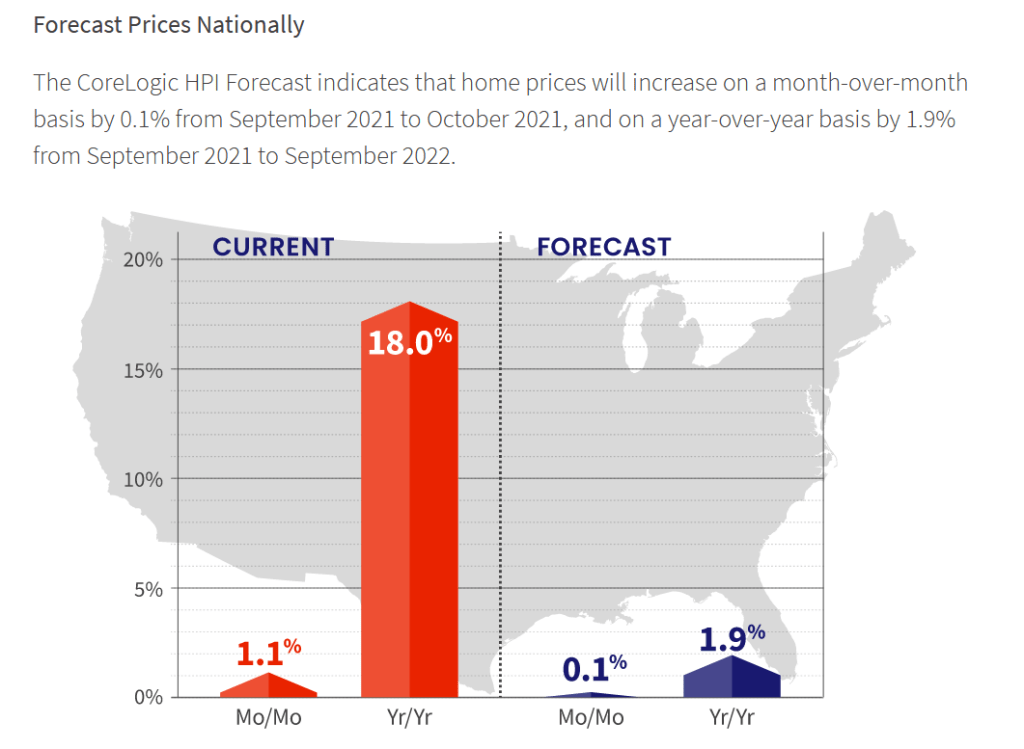

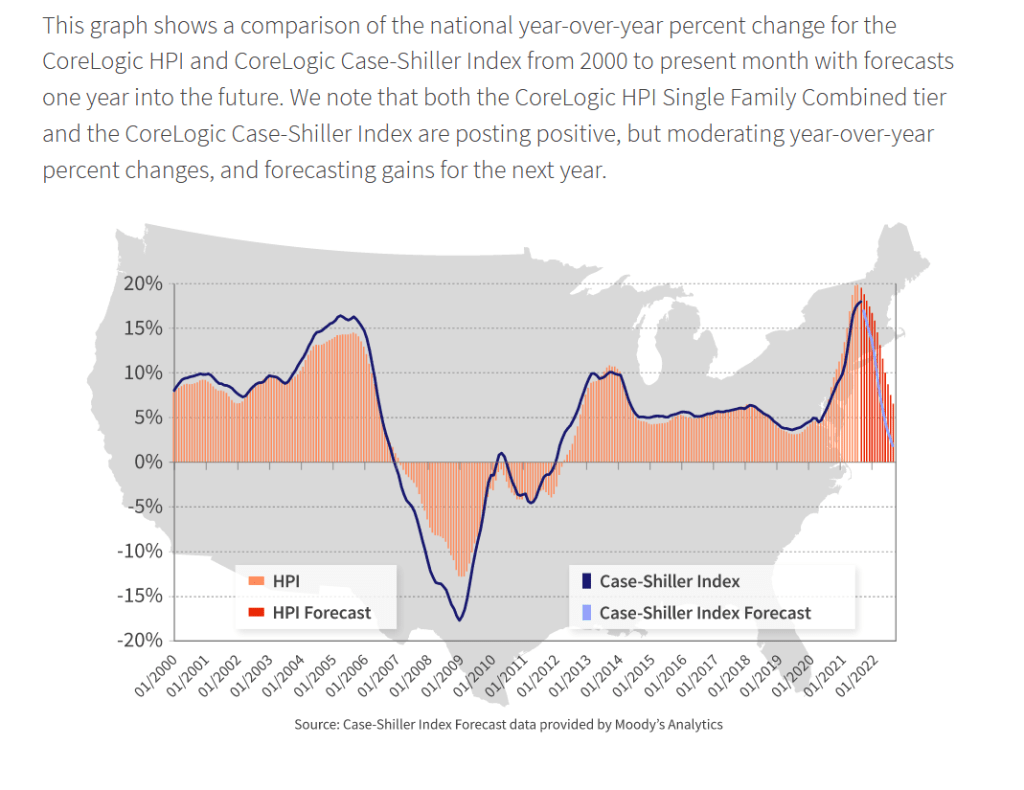

But the forecast for home price growth is for 1.9% YoY in 2022.

As home price growth crashes back to earth as wages don’t keep pace with home prices.

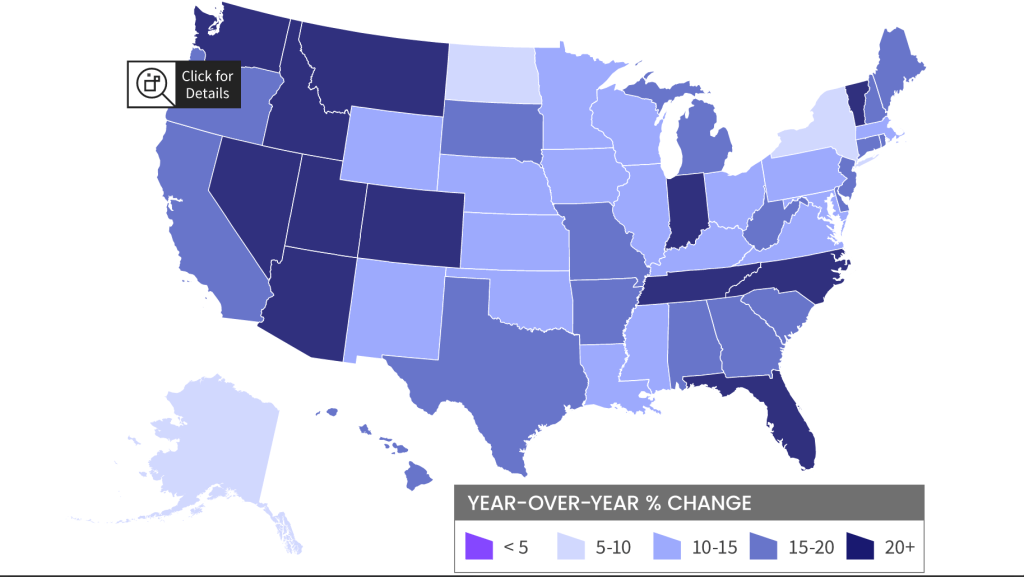

Home prices have been growing in most states out west where The Fed’s money pump has resulted in a boom in second homes and people escaping high tax California and Oregon for Nevada, Idaho, Arizona (again), Utah and Montana. The east coast is seeing the Carolinas booming along with Florida and Indiana. Escape from New York?

Escape from LA … to Arizona, Nevada, Idaho and Utah?

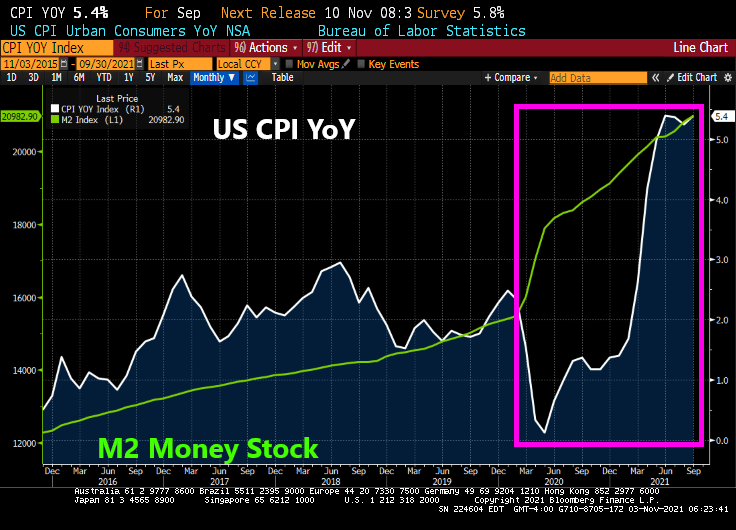

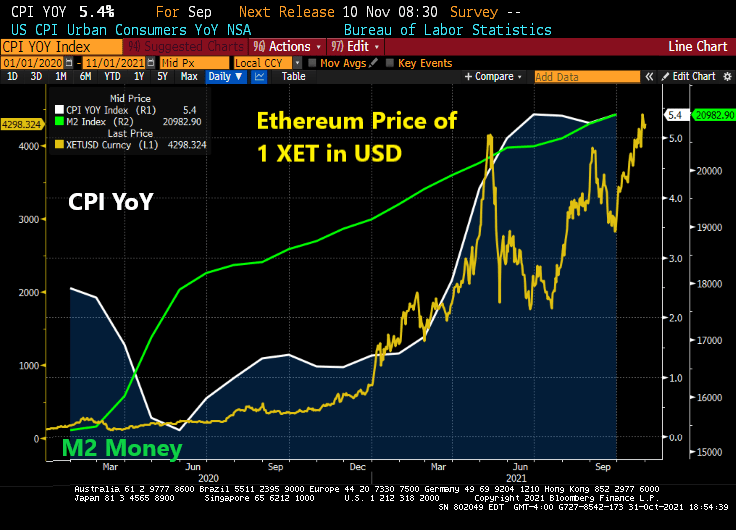

Ethererum, the cryptocurrency, is now at $4,298. It under $200 as the Covid crisis took shape in March 2020. Since Covid, The Federal Reserve went loco and massively increased their money supply and asset purchases. With that response (and economic bottlenecks), inflation has increased to 5.4% YoY.

The Fed’s new moto should be “Policy errors ARE our business!”

No, we don’t look to President Beavis to do much of anything positive about inflation.

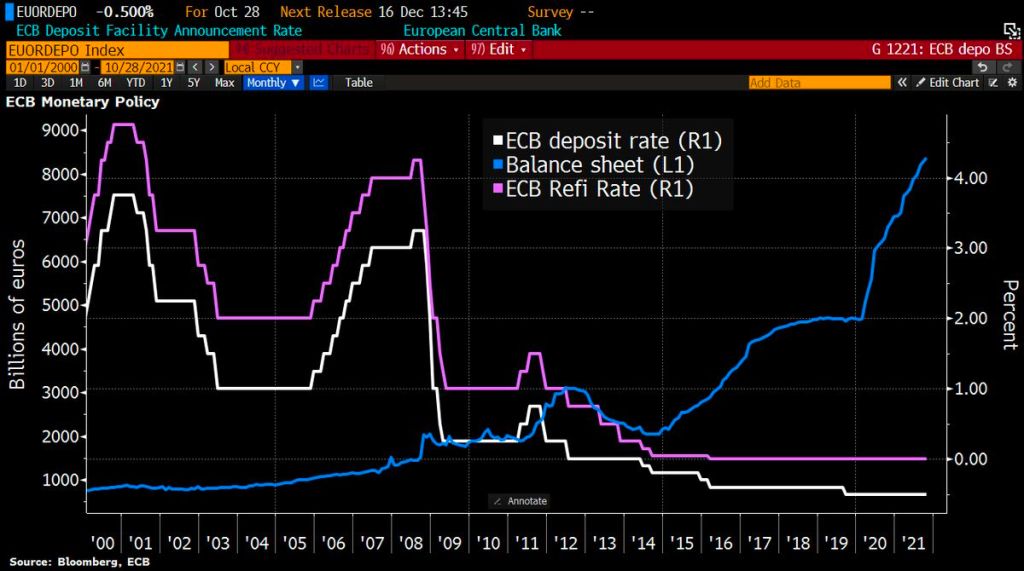

With central banks around the world signalling tighter policy amid rising prices, Lagarde said the ECB had done much “soul-searching” over its stance but concluded that inflation was still temporary, so a policy response would be premature.

Soul-searching? The ECB is just doing what Powell and the Fed (aka, Jerome Jett and the Blackhearts) are doing. Keeping the foot on the monetary gas pedal in the face of inflation.

Let’s start Eurozone inflation. It is now sitting a 4.10% YoY. And core inflation is sitting at 2.10% YoY. Inflation is now the highest since 2009 while core inflation is at the highest since 2001.

Like the Federal Reserve, the ECB still has its foot on the monetary accelerator pedal despite booming inflation.

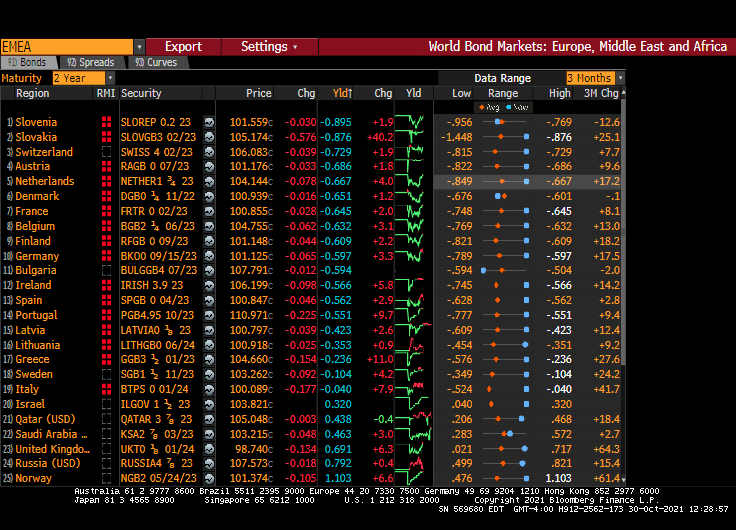

So, Christine, 19 nations in “Europe” having negative 2-year sovereign yields isn’t low enough for you?

The ECB’s platform in Frankfurt reminds me of a bad TV quiz show where participants try to guess prices next year. Call it “The Price Is Wrong.”

Unless, of course, the ECB sees a massive depression ahead.

Despite monetary Stimulypto from The Federal Reserve (still growing!), US real GDP has fallen to almost zero.

The GDPNow model estimate for real GDP growth (seasonally adjusted annual rate) in the third quarter of 2021 is 0.2 percent on October 27, down from 0.5 percent on October 19. After the October 19 GDPNow update and subsequent releases from the US Census Bureau, the National Association of Realtors, and the US Department of the Treasury’s Bureau of the Fiscal Service, a decrease in the nowcast of third-quarter real government spending growth from 2.1 percent to 0.8 percent was slightly offset by an increase in the nowcast of third-quarter real gross private domestic investment growth from 9.0 percent to 9.3 percent. Also, the nowcast of the contribution of the change in real net exports to third-quarter real GDP growth decreased from -1.56 percentage points to -1.81 percentage points.

And with a wave of her magic wand, Treasury Secretary Janet Yellen (aka, the Incredible Janet Yellenstone) will make inflation magically return to less than 2% after mid-2020.

Treasury Secretary Janet Yellen said she expects price increases to remain high through the first half of 2022, but rejected criticism that the U.S. risks losing control of inflation.

Inflation is expected to ease in the second half as issues ranging from supply bottlenecks, a tight U.S. labor market and other factors arising from the pandemic improve, Yellen said on CNN’s “State of the Union” on Sunday. The current situation reflects “temporary” pain, shesaid.

“I don’t think we’re about to lose control of inflation,” Yellen said, pushing back on criticism by former Treasury Secretary Lawrence Summers this month. “Americans haven’t seen inflation like we have experienced recently in a long time. But as we get back to normal, expect that to end.”

On Friday, Federal Reserve Chair Jerome Powell sounded a note of heightened concern over persistently high inflation as he made clear that the central bank will begin tapering its bond purchases shortly but remain patient on raising interest rates.

The S&P 500 Index posted its first decline in eight days, while benchmark Treasuries rallied to send 10-year yields down by the most in more than two months. Inflation expectations remain elevated — the 10-year breakeven rate of 2.64% is within 15 basis points of the record high reached in 2005 — and rates traders maintained bets the Fed will hike at least once within a year.

Powell said policies are “well-positioned” to manage a range of outcomes.

So Janet, are you saying that home price growth is going to slow to 2% YoY after mid-2022? Or that the Biden Administration is going to build the Canadian pipeline to help ease energy costs? Or that west coast ports get magically unclogged? Or that chips for cars will magically begin appearing?

I forget. The Fed doesn’t consider housing or energy prices in their inflation measurements. So, Yellen and The Fed ignore that most important expenditures for households.

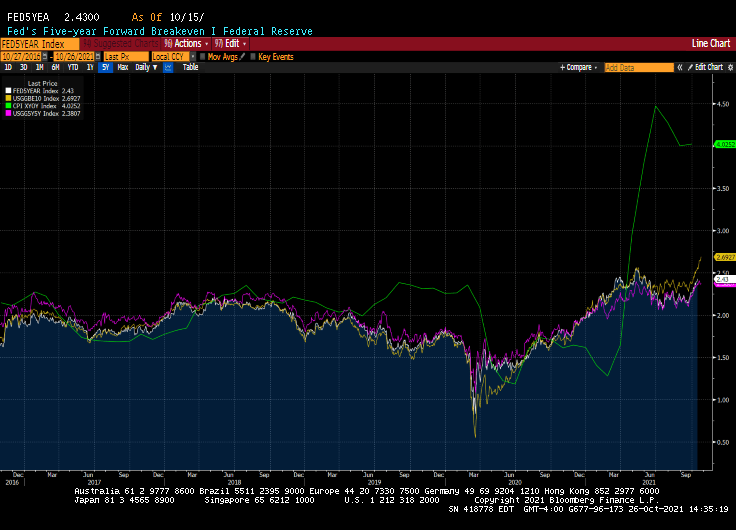

The Fed’s breakeven inflation rates are considerably lower than current core inflation (green line).

No wonder Yellen and Powell can make inflation magically disappear. Don’t count it!

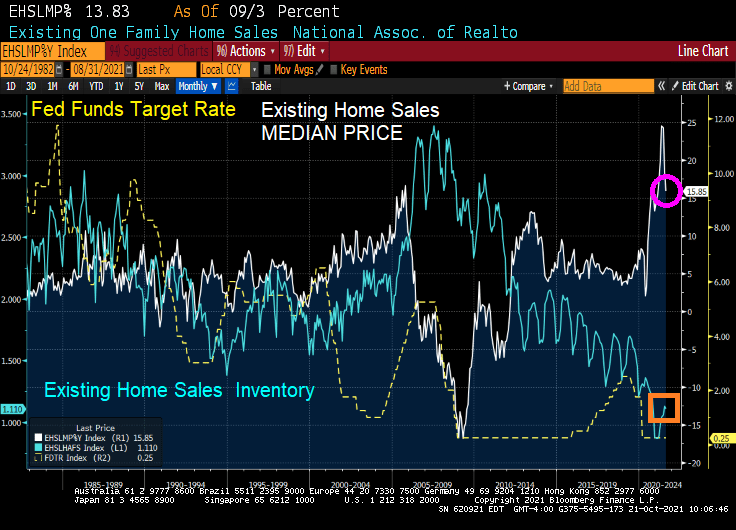

US new home sales rose a whopping 14% in September as the median price of new home sales rose 20.1%.

Existing home sales still remain low allowing median prices to soar with Fed money printing.

New home sales surged as The Fed turns a blind eye to out-of-control inflation in prices.

Thanks to The Fed, new homes under $150,000 have disappeared and new homes over $500,000 have grown to 31% of all new homes. Where have all the starter homes gone?

Between Fed stimulypto and massive over-spending by Congress and the Biden Administration, the economic system is clogged like an interstate toilet, driving construction prices soaring.

Apparently Fed Chair Jerome Powell and Treasury Secretary Janet Yellen have never experienced clogged plumbing in their homes. And President Joe Biden has probably forgotten.

I can’t wait to hear if Biden’s press secretary Jen Psnarki attempts to put a positive spin on this debacle.

https://www.redfin.com/news/housing-market-update-pending-sales-up-47pct-from-2019/According to Redfin, forty-four percent more homes are pending sale than at this time in 2019, but only 3% more homes recently hit the market—down from 12% growth over 2019 just 7 weeks prior. As a result of the severe imbalance between the number of homes for sale and the number of buyers, the pace of the market is picking up at a time when it typically slows. A third of homes are finding buyers within a week of hitting the market, up from 30.8% at the end of the summer. This week, we’re comparing today’s market with the pre-pandemic fall market of 2019 to highlight how hot the market remains, even as most measures are settling into typical seasonal patterns.

“Comparing today’s sales and new listings numbers to the 2019 levels helps to reveal the stark shortage of supply we are facing,” said Redfin Deputy Chief Economist Taylor Marr. “The boost of housing supply that came on the market during the summer has already faded away, even as demand tapers off as we expected it to in the fall. Relative to the last ‘typical’ fall of 2019, demand remains steady and strong thanks to the increased urgency many buyers have as mortgage rates inch up. Rising rates also make buyers more price sensitive, so homes that are priced right are increasingly likely to receive offers right away.”

Shortage of supply, indeed. It is a mystery to me why the supply of homes for sale is not matching the demand.

But what happened after 2019? COVID and the entrance of massive Federal Reserve and Federal government stimulus. With limited supply hitting the market, home prices soared with the government stimulus.

We are likely to see rising prices until Federal Stimulypto stops or at least slows.

Federal Reserve Chair Jerome Powell sounded a note of heightened concern over persistently high inflation as he made clear that the central bank will begin tapering its bond purchases shortly but remain patient on raising interest rates.

“The risks are clearly now to longer and more persistent bottlenecks, and thus to higher inflation,” Powell said Friday during a virtual panel discussion hosted by the South African Reserve Bank and moderated by Bloomberg’s Francine Lacqua.

“I would say our policy is well-positioned to manage a range of plausible outcomes,” he said. “I do think it’s time to taper and I don’t think it’s time to raise rates.”

Good luck with that, Jay! You are going to raise the short-end of the yield that will lead to a flattening of the Treasury yield curve. But you are going to continue to buy Treasuries and Agency MBS in order to monetize the rampant spending by Congress and the Biden Administration? C’mon man!

You can see where Powell spoke today. It is when gold tanked along with the 10-year Treasury yield. Both rebounded a bit, but the 10-year Treasury yield continue its fall to 1.6324%.

The US dollar (green) fell when Powell opened his pie-hole. But Bitcoin (blue) fell in advance as if they knew what Powell was going to say.

You must be logged in to post a comment.