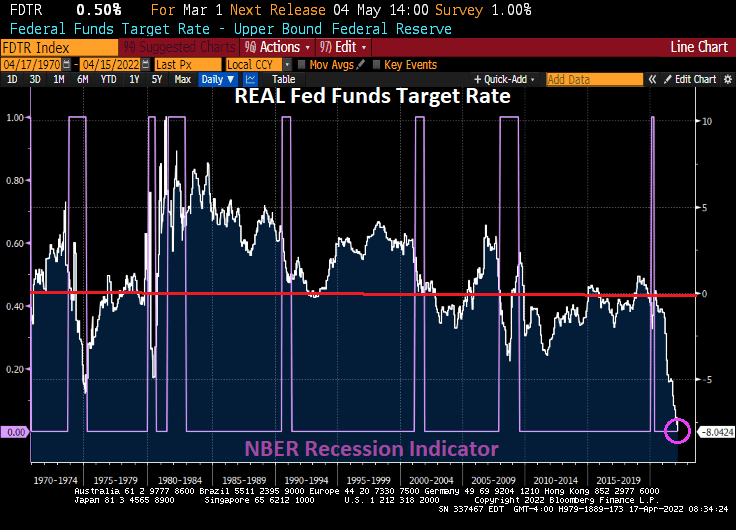

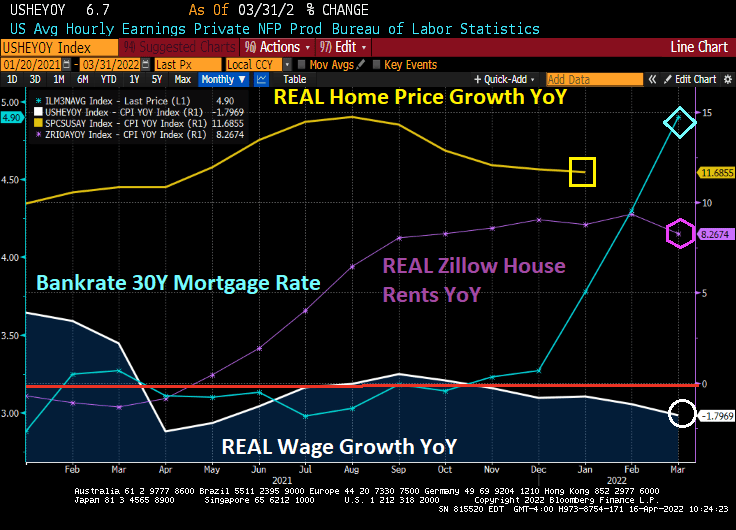

We have Federal Reserve of St Louis President James “Bully” Bullard saying that The Fed could raise rates by 75 basis points in May, the Japanese Yen to Dollar is crashing as mortgage rates continue to soar.

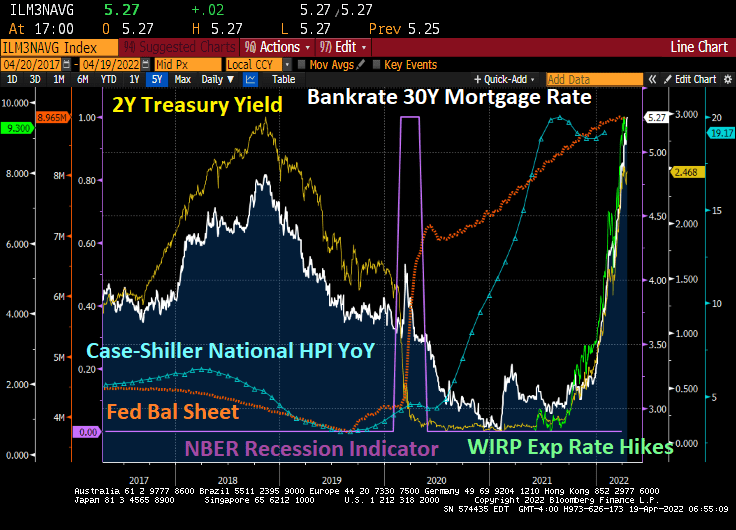

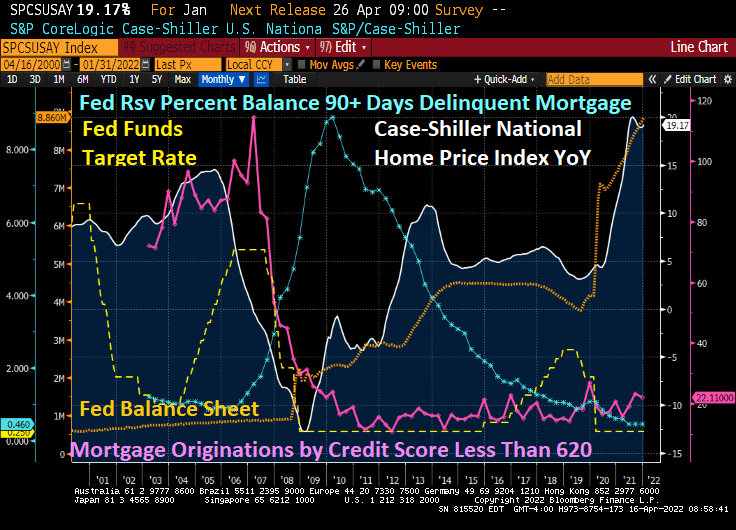

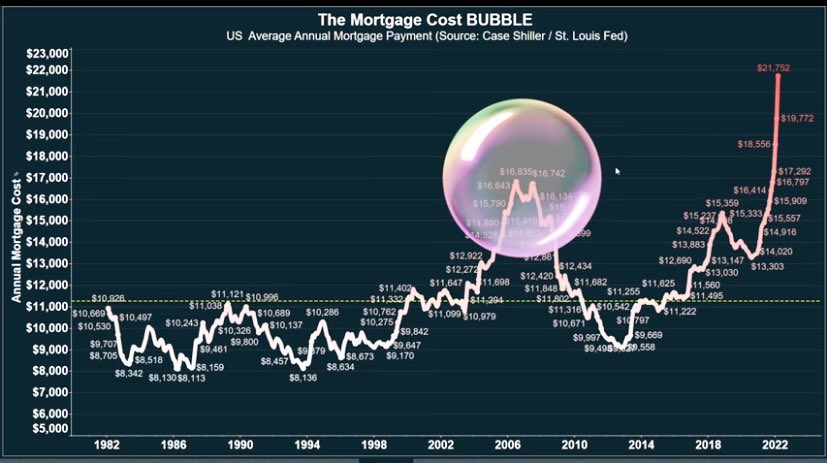

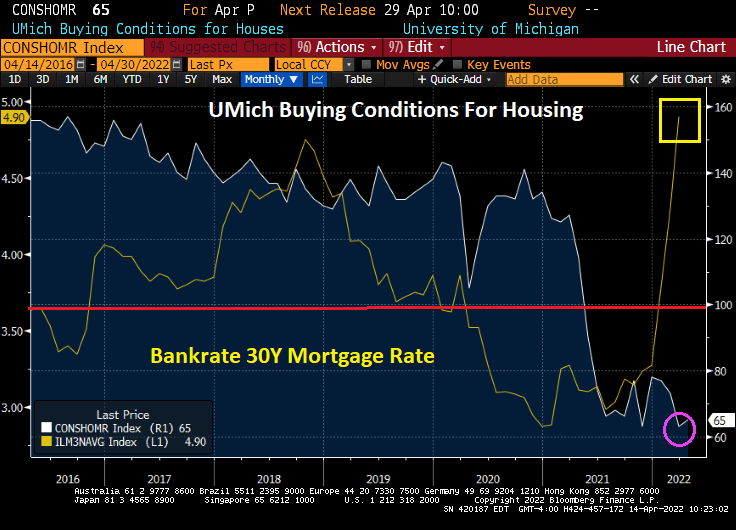

Here is a nice summary of The Fed’s massive balance sheet expansion in reaction to Covid (orange line) and the resulting soaring of home prices. Then The Fed signals that they will remove the “punchbowl” and mortgage rates have boomed. And not in a good day.

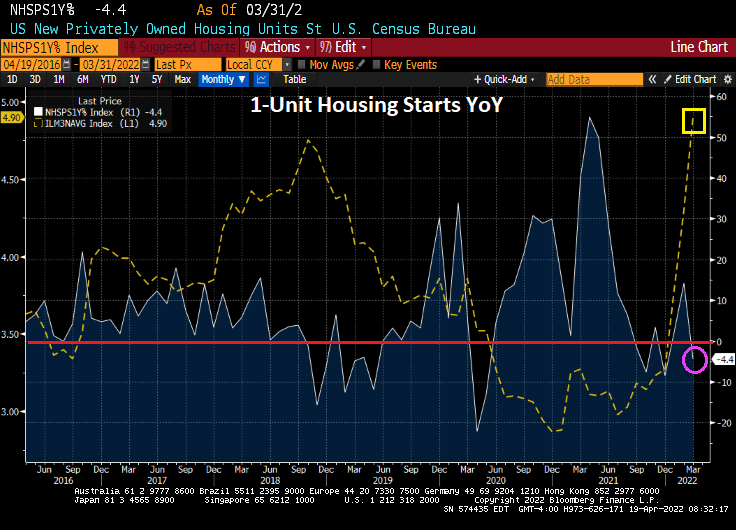

Today we have the US housing starts report. In a nutshell, 1-unit housing starts (single-family detached) declined -4.4% YoY as mortgage rates skyrocket.

5+ unit (aka, apartment stats rose 7.49% MoM in March while 1-unit starts declined by -1.72% MoM. 1-unit permits fell by -4.81% MoM while 5+ units starts rose by 10.89% MoM.

Soaring home prices coupled with soaring mortgage rates equals … apartment living.

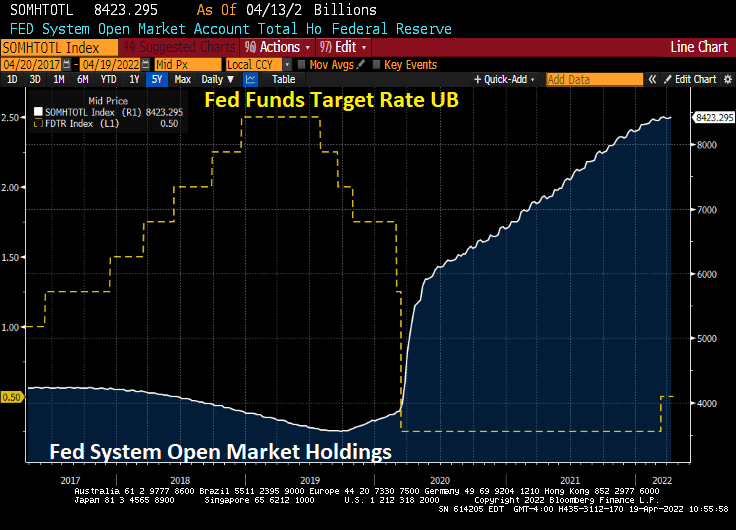

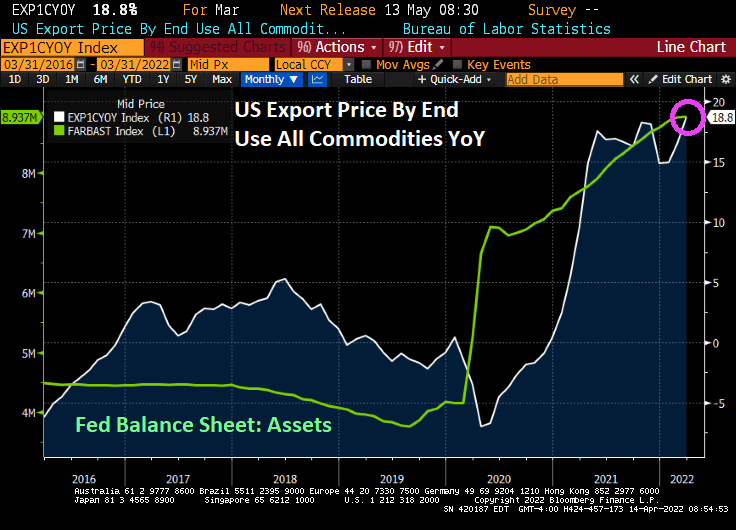

Bear in mind that The Fed STILL have massive monetary stimulypto outstanding!!

Now you to can lease an apartment next to Patrick Bateman from “American Psycho.” And listen to Huey Lewis and The News through the paper-thin walls.

You must be logged in to post a comment.