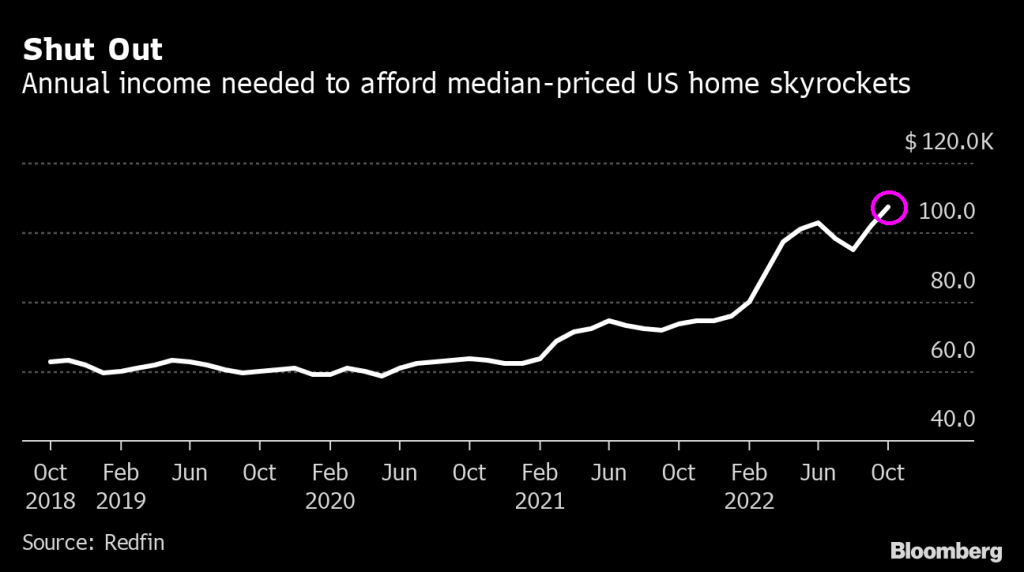

The US housing market is slowing, to be sure. Yesterday’s existing home sales (EHS) report revealed that US EHS were down -28.43% YoY and the median price of EHS slowed to 6.6% YoY.

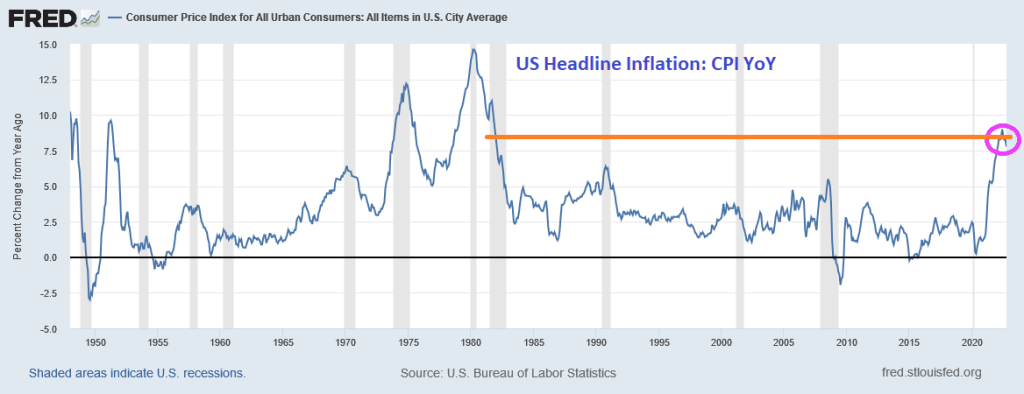

But that is just the surface of the EHS report for October. Once I removed inflation (CPI YoY) from the numbers, we are left with REAL median price of EHS growth of -1.17% and REAL average hourly earnings YoY of -3.0% YoY. The REAL 30-year mortgage rate is -5.25%. That reveals how horrible inflation is in the US.

It is important to note that EHS numbers are lower in October than they were before Covid stimulypto (my name for the massive spending spree by Congress and massive injection of monetary stimulus by The Fed. Even the REAL 30-year mortgage rate is negative at -0.5254%.

As I mentioned on Varney and Company on Fox Business, housing is going to suffer when The Fed starts to tighten their monetary policy. And here we are, folks!

US existing home sales fell a staggering -28.43% YoY in October as M2 Money growth grinds to almost a halt.

October’s existing home sales YoY of -28.43% is the WORST since The Great Recession and collapse of Lehman Brothers.

The median price of existing home sales slowed to 6.6% YoY. Inventory of EHS remains below pre-Covid levels.

Unrelated to housing, Prince Imhotep (Federal Reserve Bank of Minneapolis President Neel Kashkari) said Friday that the whole idea of cryptocurrency is “nonsense” after the implosion of FTX revealed the industry’s shortcomings.

“This isn’t case of 1 fraudulent company in a serious industry,” Kashkari said on Twitter, commenting on an article about how investors fell for FTX. “Entire notion of crypto is nonsense. Not useful 4 payments. No inflation hedge. No scarcity. No taxing authority. Just a tool of speculation & greater fools.”

Or it could be that investors don’t trust The Fed or Federal government to act in their best interest.

Here is a crypto investor (in red fez) being lectured by Minneapolis Fed President Neel Kashkari.

The Philadelphia Fed’s Business Outlook plunged to 1-9.40% YoY, the worst since 2012. Notice how the Philly Phed Plunge is related to M2 Money growth YoY.

Of course, it is easy to blame the figure on rapidly rising mortgage rates and Federal Reserve tightening.

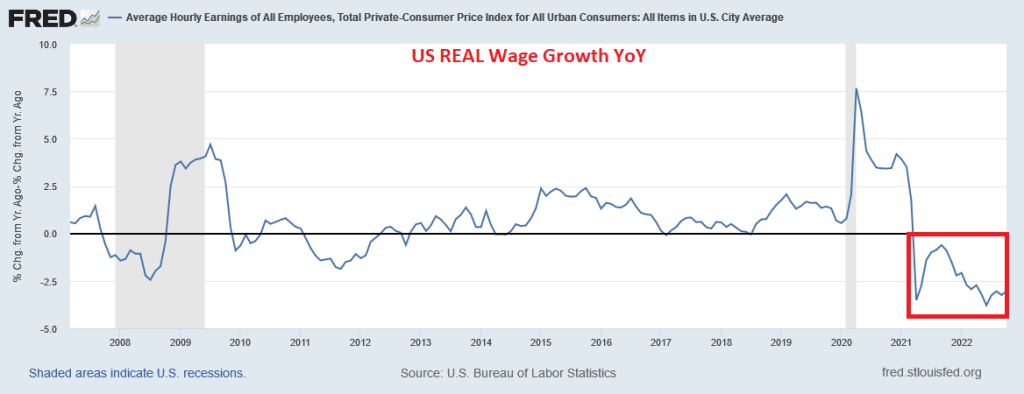

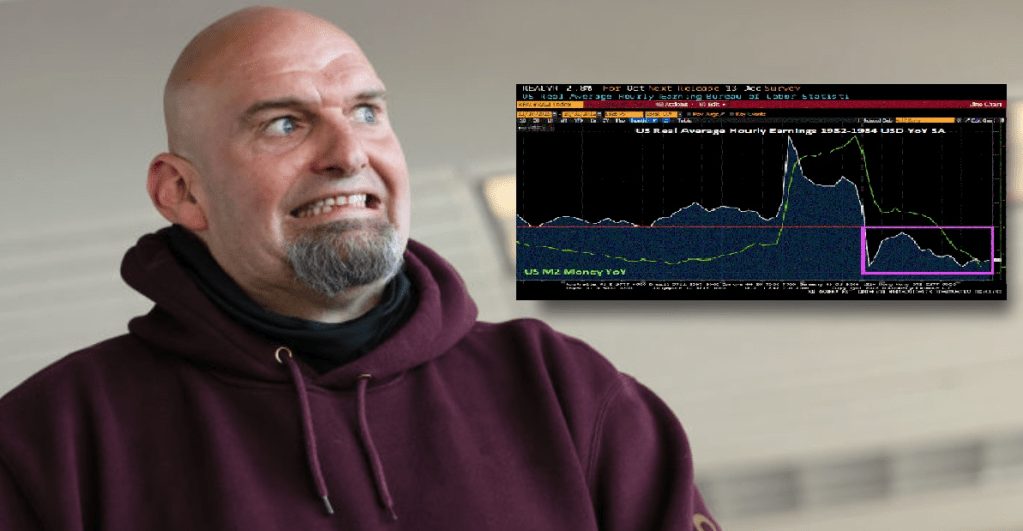

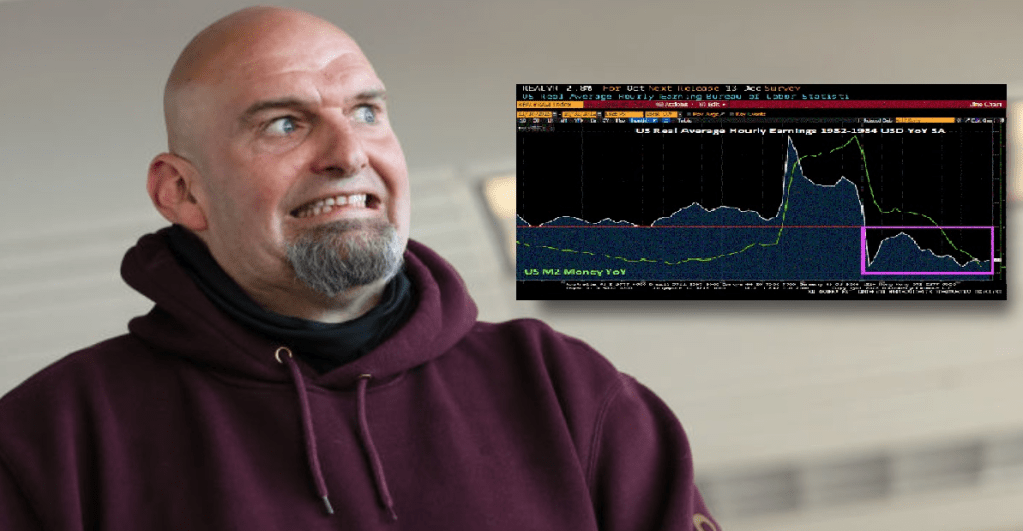

But the rest of the story (as Paul Harvey used to say) is that US REAL wage growth has been NEGATIVE for 19 straight months. This alone makes housing unaffordable for the middle class and low wage workers.

Again, why are Biden and Trudeau wearing Mao jackets in Bali? And why is Biden looking like a robot?? Biden does look like he is saying “Take me to my leader, Pei.”

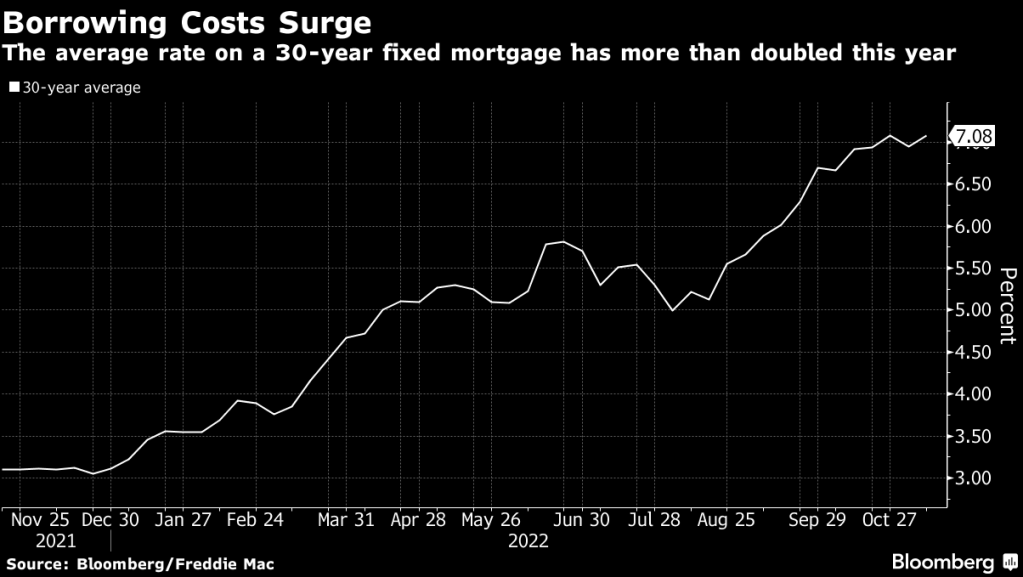

US mortgage rates fell last week by the most since the end of July, slipping below 7% and helping generate a bounce in purchase applications that otherwise remain depressed, but only in the Seasonally Adjusted data. The NON-Seasonally Adjusted data show a hefty decline.

The contract rate on a 30-year fixed mortgage decreased 24 basis points to 6.9% in the week ended Nov. 11, according to Mortgage Bankers Association data released Wednesday. The group’s index of applications to buy a home rose 4.4% — the most since June — but is still near the weakest level since 2015.

But the bounce was in Seasonally Adjusted data only. The NON-seasonally adjusted data remained depressed.

Mortgage applications decreased -10.0 percent SA from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending November 11, 2022. This week’s results include an adjustment for the observance of Veterans Day.

The Refinance Index decreased -11.44% percent from the previous week and was 88 percent lower than the same week one year ago.The unadjusted Purchase Index decreased -10 percent compared with the previous week and was 46 percent lower than the same week one year ago.

Mortgage purchase applications will continue to fall in NSA terms since it is the Winter and home buying season won’t really start until January. Refinancing applications actually dropped -11.44% even with the drop in mortgage rates.

The data. As my former students know, I like the “raw” data, better known as NON-seasonally adjusted (NSA) data and avoid seasonally-adjusted data (SA) since it hides what is going on.

And on The Fed Futures Front, The Federal Reserve is still looking a hiking their target rate from 4% to just under 5%.

Between Biden’s green energy mandates and the spendathon by the Pelosi/Schumer led Keynesians in Congress (or Kongress), we saw a 40-year high in inflation.

But with roaring Bidenflation, we have the S&P 500 index experiencing, in real terms, the worst performance since 1872.

That is, the worst since President Ulysses Grant.

President Biden is dressed in his Mao outfit with Canada’s Justin Trudeau.

And the WEF’s Klaus Schwab.

At least Biden, Trudeau and Schwab are wearing different colored Mao jackets.

The evidence from the last thirty years is clear. Keynesian policies leave a massive trail of debt, weaker growth and falling real wages. Furthermore, once we look at each so-called stimulus plan, reality shows that the so-called multiplier effect of government spending is virtually inexistent and has long-term negative implications for the health of the economy. Stimulus plans have bloated government size, which in turn requires more dollars from the real economy to finance its activity.

As Daniel J. Mitchell points out, there is evidence of a displacement cost, as rising government spending displaces private-sector activity and means higher taxes or rising inflation in the future, or both. Higher government spending simply cannot be financed with much larger economic growth because the nature of current spending is precisely to deliver no real economic return. Government is not investing; it is financing mandatory spending with resources of the productive sector. Every dollar that the government spends means one less dollar in the productive sector of the economy and creates a negative multiplier cost.

When society decides to use a certain part of the resources generated by the productive sector for non-economic return activities, be it social spending or mitigation of threats, it can only do it by understanding how much of the productive capacity of the economy is able to sustain a larger cost. When costs are not considered as a burden, but considered as entitlements that can only grow, the productive capacity is not strengthened, but weakened.

The main problem of the past decades, but particularly since 2008, is that government spending and monetary policy have become solutions of first resort to any slump in economic activity, even if that decline was created by government decisions, such as shutting down the economy due to a health crisis. Furthermore, government spending increases and loose monetary policy continued even in growth periods. This, in turn, creates an unsustainable public deficit that needs to be monetized or refinanced. Both mean a larger harm for the productive sector as the debt increase leads to higher taxes for everyone but also a soaring cost of living coming from the destruction of purchasing power of the currency.

Government spending does not boost private sector activity, even less so when the entire budget is spent on non-investment outlays. It is even worse when citizens believe that infrastructure or real economic return investments should be conducted with taxpayers’ money. If an investment is productive and economically viable there is no need to involve the government. At best, the government should only participate as a co-investor, as the example of technology and defence shows, but never as a resource allocator for a simple reason. Public intervention is always aimed at perpetuating the existing inefficiencies and maximizing the budget. Efficient resource allocation cannot come from entities that have a core interest in expanding the budget and always perceive any inefficiency or poor result as the consequence of not having spent enough.

Yes, US public debt has exploded, particularly since the 2008 financial crisis and then again the Covid outbreak of 2020.

And inflation is near a 40-year high.

Then we have 19 consecutive months of negative wage growth in the US.

Biden is apparently doubling down on “Green Schemes” now that the US House of Lords (aka, Senate) remain under Keynesian control (aka, Democrat). So watch for inflation to start increasing again.

What do Bernie Madoff and Sam Bankman-Fried have in common? Greedy investors who apparently didn’t bother to monitor what was going on.

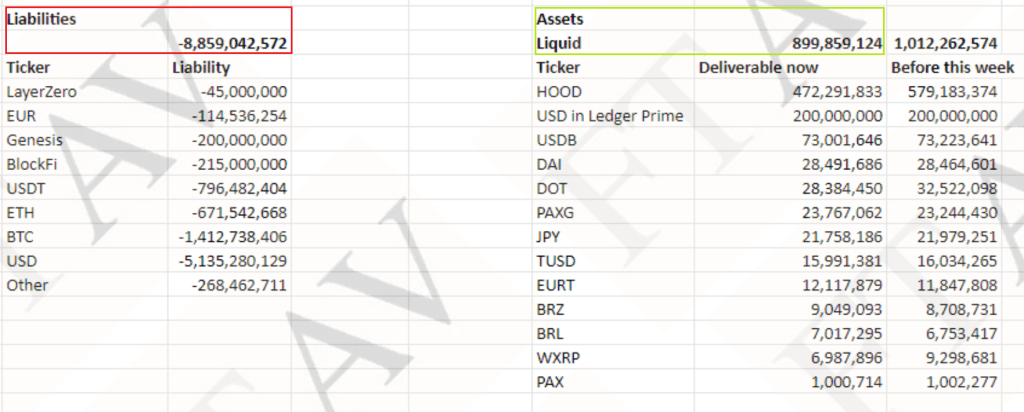

Yes, had they monitored FTX, Bankman-Fried’s company, they would have noticed that FTX held less than $1bn in liquid assets against $9bn in liabilities.

Generally, with buyer beware, the onus falls on investors to monitor what is going on. But The Fed’s completely dropped the ball on Bernie Madoff where investors didn’t seem at all curious about earning supercharged returns. The same is the case for FTX.

FTX had partnered with Ukraine to process donations to their war efforts within days of Joe Biden pledging billions of American taxpayer dollars to the country. Ukraine invested into FTX as the Biden administration funneled funds to the invaded nation, and FTX then made massive donations to Democrats in the US.

The SEC’s Gary Gensler blew it again. After his agency failed to warn investors about Terra and Celsius—whose collapses this spring sparked a trillion-dollar investor wipeout—the Securities and Exchange Commission chair allowed an even bigger debacle to unfold right under his nose. I’m talking, of course, about the revelation this week that the $30 billion FTX empire was a house of cards and that its golden boy founder, Sam Bankman-Fried, is the crypto equivalent of Theranos’s Elizabeth Holmes (Stanford University is where Holmes was an MBA student and Stanford Law School is where both SBF’s parents are professor).

To be fair, Gensler was not the only one suckered by SBF. Nearly everyone else fell for the narrative that SBF, with his cute afro and aw-shucks demeanor, was exactly the savior crypto needed to shake off its dodgy reputation and emerge as part of the mainstream financial system. The problem is that cop-on-the-beat Gensler not only failed to spot the crime—he appeared set to go along with a legislative strategy that would have given SBF a regulatory moat and made him king of the U.S. crypto market.

While it is easy to blame Gensler, the onus still falls on investors (and their managers) to MONITOR. Buyer beware.

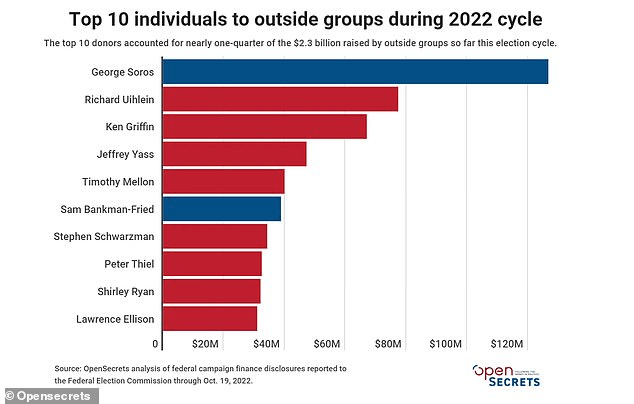

What will happen to Sam? Likely nothing. He is a golden child of Democrats and was the second biggest donor to Biden and the Democrats after America-hating George Soros. Just like Biden’s son Hunter will never pay for his many inappropriate antics, I doubt that Merrick “Double Standard” Garland will do much to Sam.

Steph Curry, Shaq and Tom Brady should fire their investment advisors and possibly sue then for failure to monitor. No one noticed $1bn in assets against $9bn in liabilities??

The Fed’s favorite yield curve measure, the implied yield on 3-month T-Bills in 18 months less the 3-month T-bill yield has inverted. Note that this curve inverts prior to a recession.

The new face of reckless Fed policy and Federal spending. 19 straight months of negative REAL earnings growth as America re-elects the same irresponsible fools that are turning the US into Venezuela.

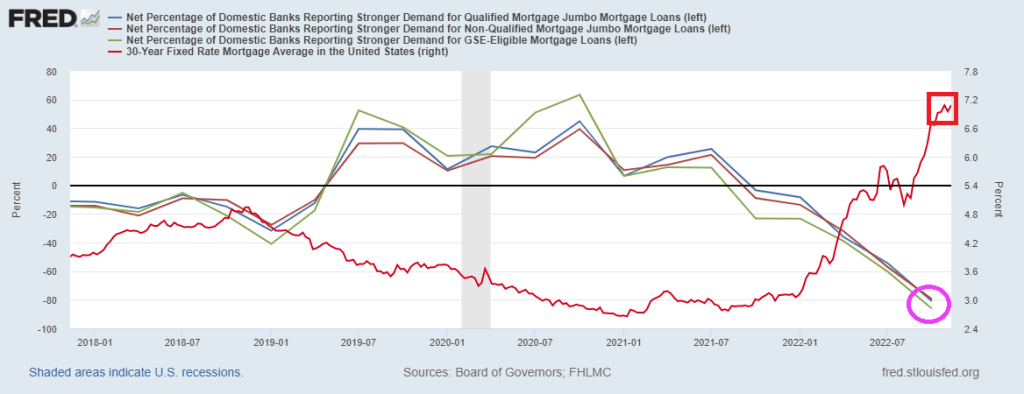

The Net Percentage of Domestic Banks Reporting Stronger Demand for Mortgage Loans is sinking faster than Joe Biden’s oratory skills as The Fed tightens their monetary belts.

And today, the University of Michigan (BOOO!!) consumer survey for housing buying conditions fell to the lowest level in recorded history.

Given the latest inflation numbers (improving from disastrous, 8.2% YoY to really horrible, 7.70% YoY), and unemployment rate rising from 3.5% to 3.7%, we now see that Taylor Rule estimate for Fed Funds is now … 13.85%. The US is currently at 4.00%. THAT is a big gap!

Yes, The Fed will not be able to fill the gap between the Taylor Rule and the current Fed Funds Target Rate, without incredible damage being done.

Unfortunately, this is an ACTIVE FAILURE for The Fed which has left monetary stimulus too high for too long since late 2008.

On a personal note, I am glad the midterm elections are over. We saw John Fetterman arguing until he was blue in the face that he loved fracking and will continue to let Pennsylvania frack. Then PA governor-elect Josh Shapiro came out yesterday and said that PA will end all fracking. And we are to believe that Lt Gov Fetterman did not talk with PA Attorney General Shapiro about fracking? To quote Joe Biden, “C’mon man!”

You must be logged in to post a comment.