The Federal Reserve and Federal government are helping make housing simply unaffordable!

In January 2020, just prior to the COVID outbreak in the US, the Case-Shiller national home price index was growing at 4% YoY, the Zilliow rent index (all homes) was growing at 2.92% YoY and REAL average hourly earnings were growing at 0.52% YoY.

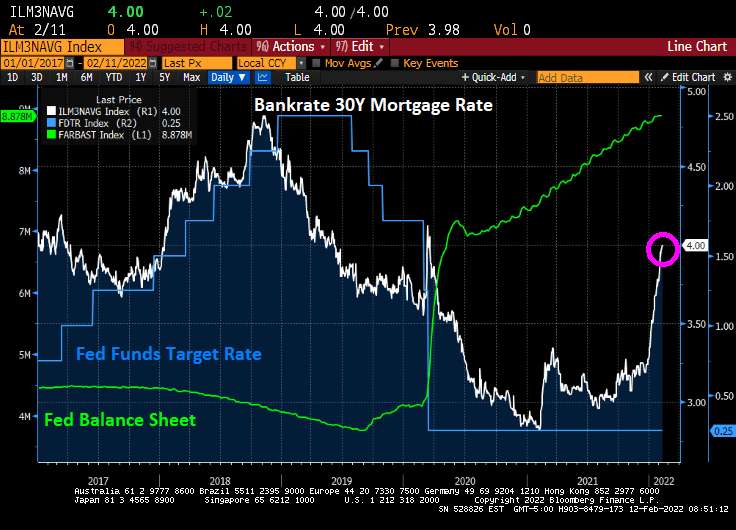

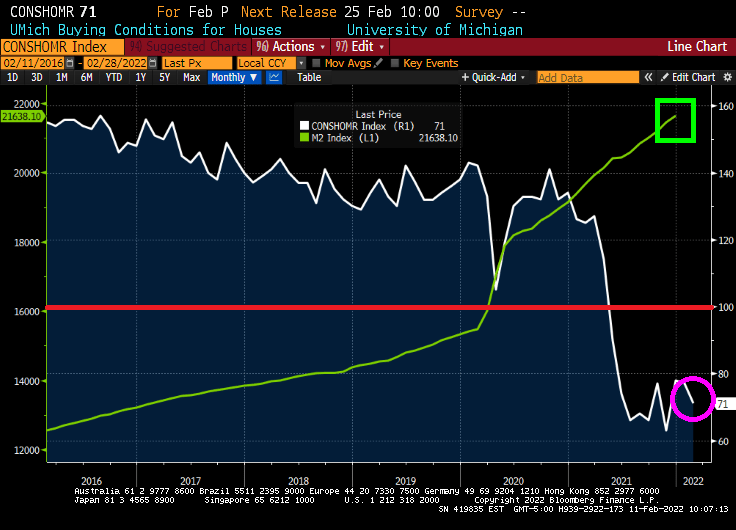

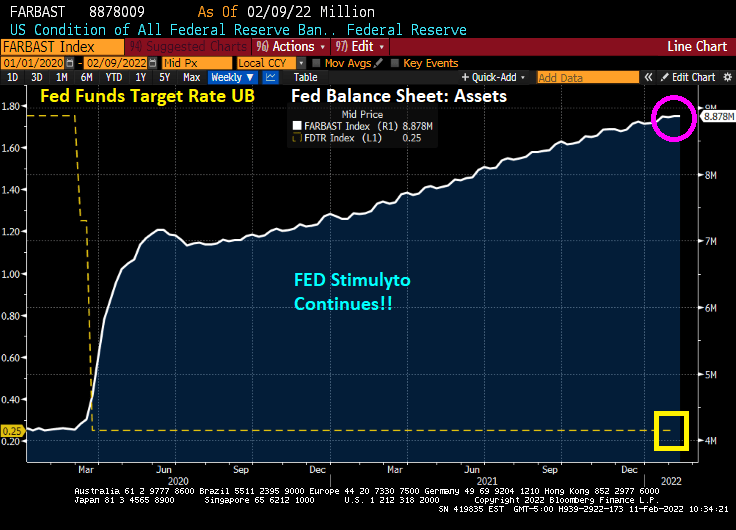

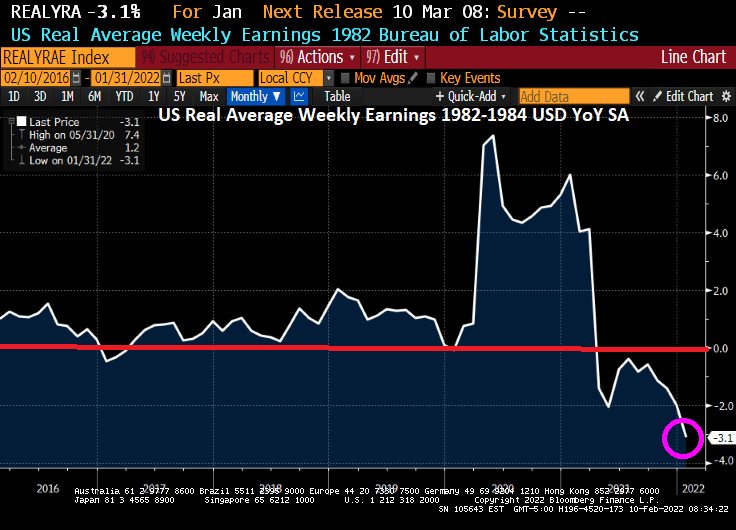

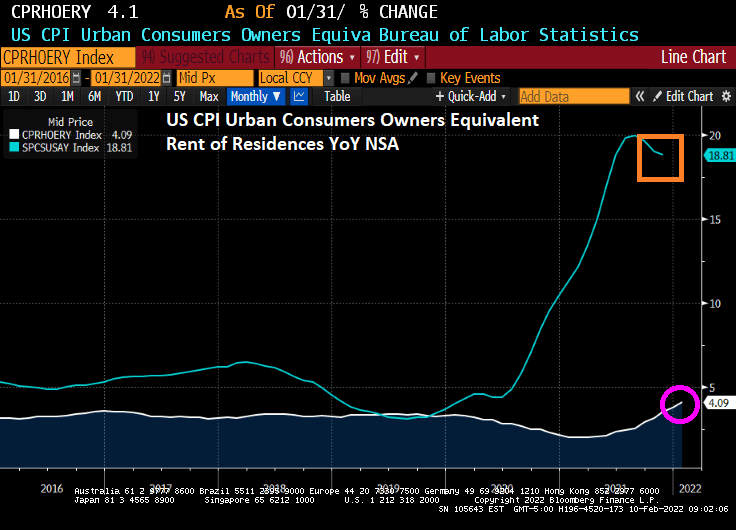

Then COVID struck and the Federal government dumped trillions of dollars of stimulus into the economy and The Federal Reserve massively expanded its balance sheet. Now the US has home prices growing at a 18.8% rate, rents (for those who can’t afford to purchase a home) growing at 14.91% and REAL hourly earnings growing at -1.80%.

The site Apartment List has an even bleaker view of rent growth, with rents in January 2022 having grown by 18% YoY.

Now that COVID is fading, we see New York City rents growing at 33.5% YoY followed by Florida and Arizona cities at 29.3% and higher rates. Irvine CA is seventh at 28%. The slowest growing city is Oakland, CA is growing at only 0.5%.

So, The Federal Reserve and Federal government have created their version of a horror film with even rents blowing out of control. And it’s getting weirder as inflation blows out of control.

You must be logged in to post a comment.