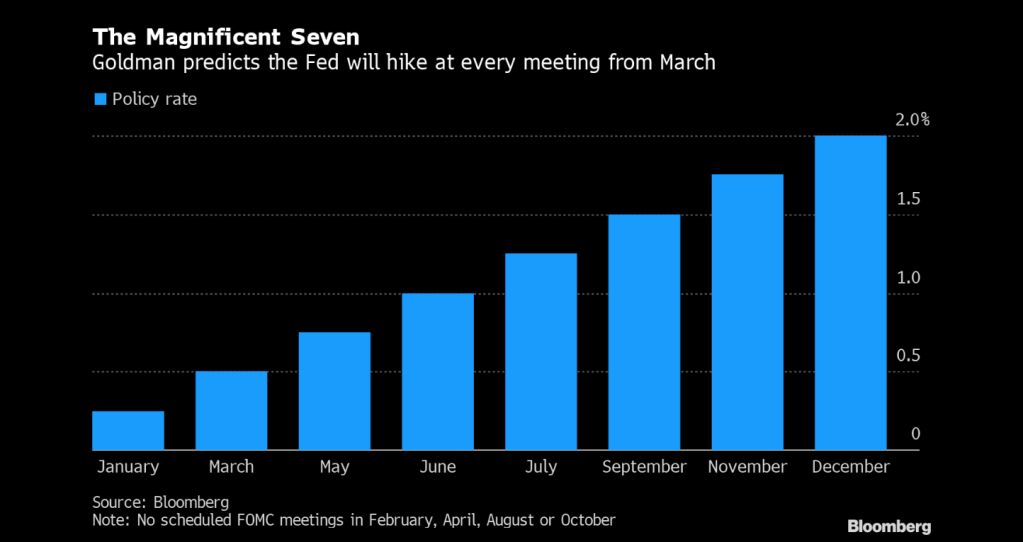

Credit Suisse’s Zoltan Pozsar thinks The Federal Reserve needs to spark a market crash. Really Zoltan??

If The Fed does its expected “shock and awe” (or shock and awful), it will be more than the stock markets will crash. The housing market could crash too.

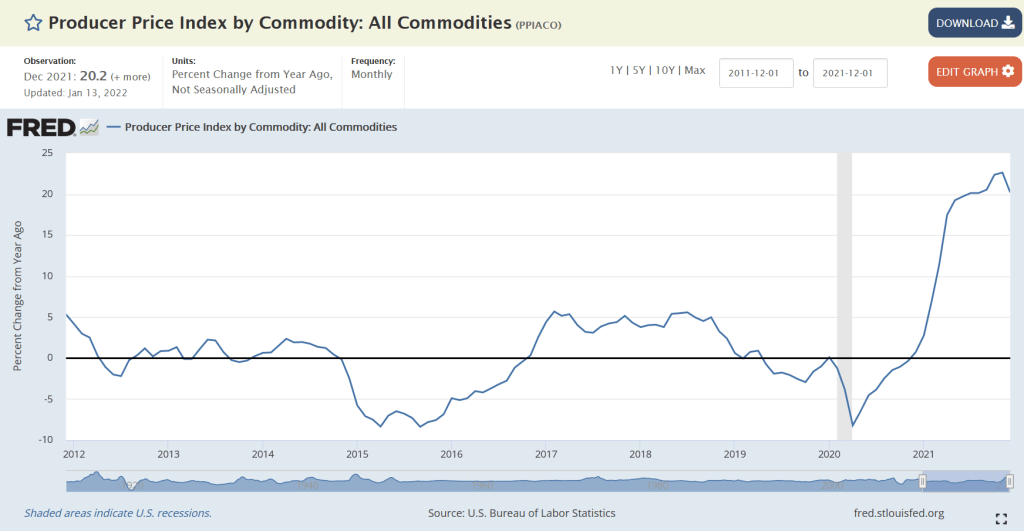

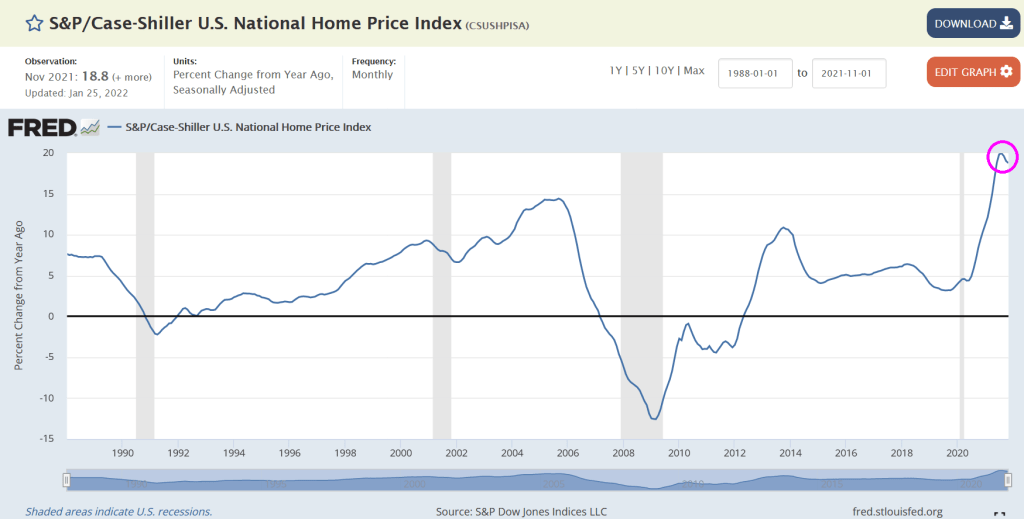

Take the current US housing situation with its limited inventory of listings combined with massive Fed stimulypto.

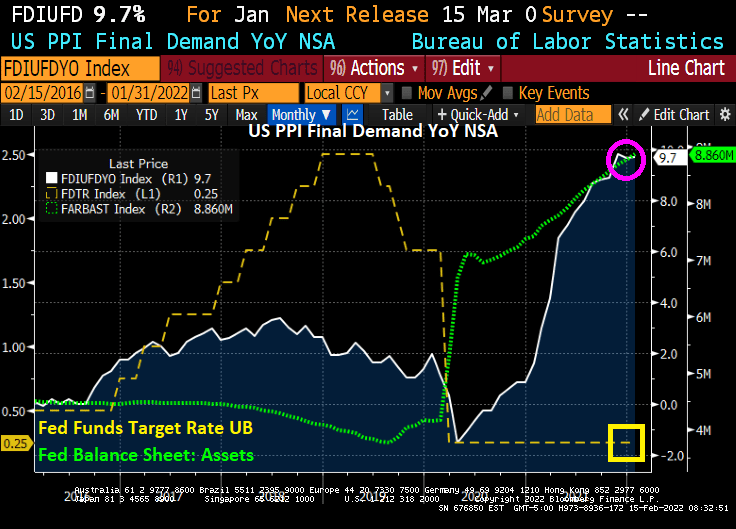

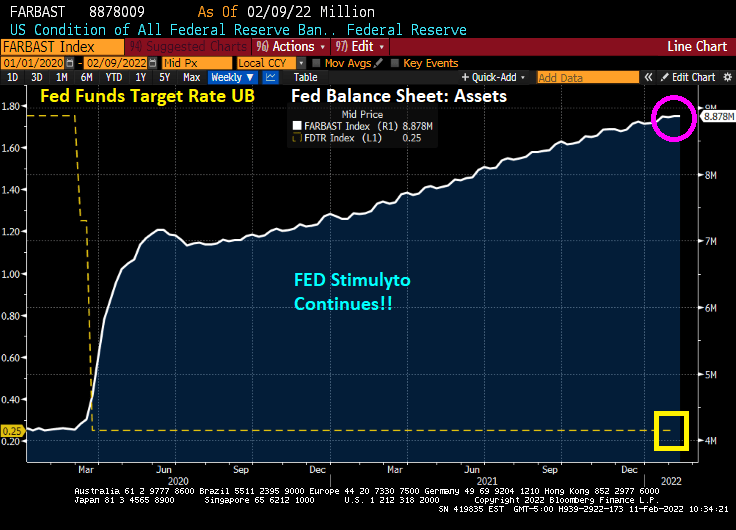

US 1-unit housing starts are down -4.1% in January. But heck, it is January! But on a year-over-year basis, 1-unit housing starts are down -2.4%. But what will happen if The Fed ACTUALLY withdraws its gargantuan monetary stimulus (green line)?

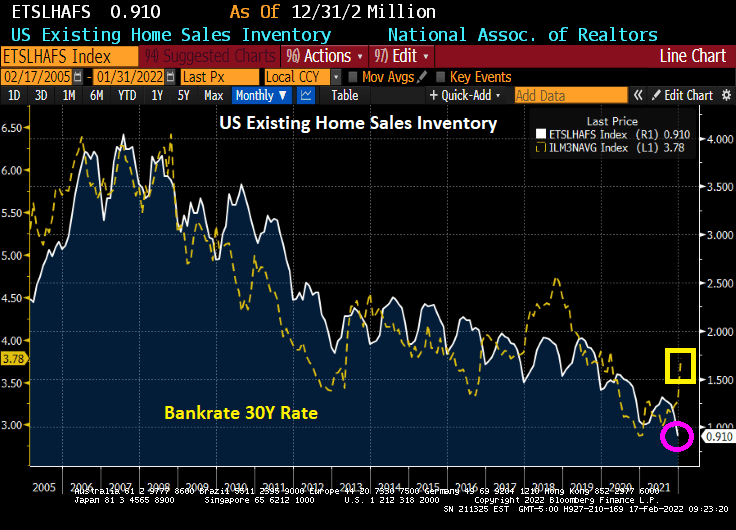

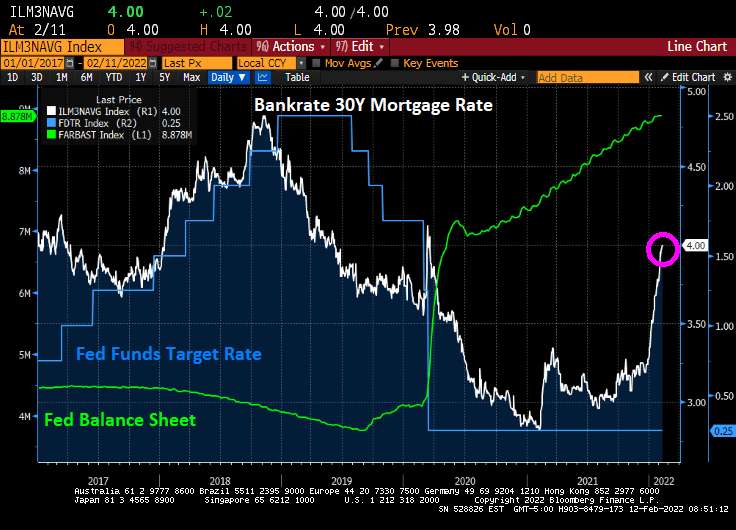

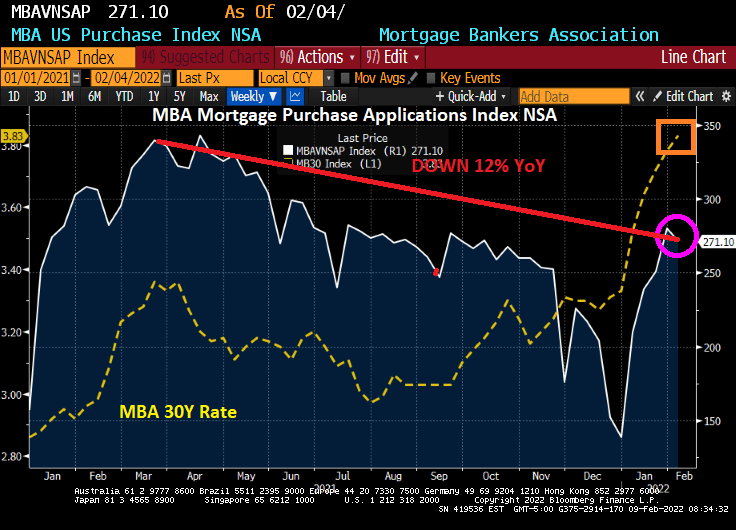

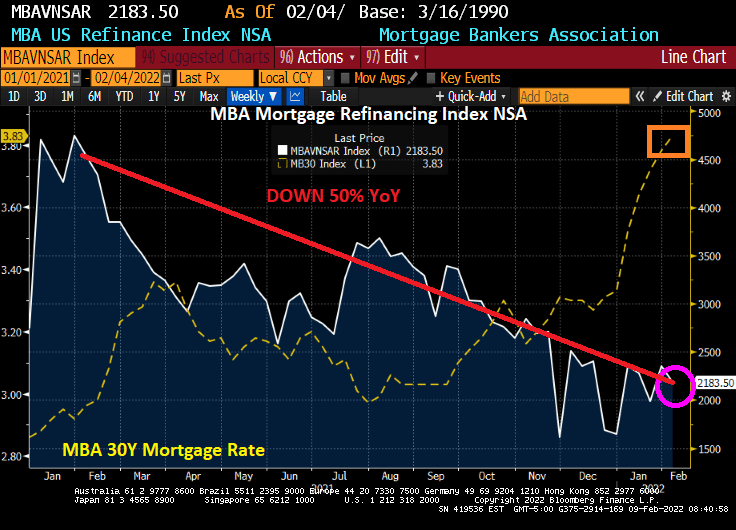

Existing home sales inventory continues to decline as Bankrate’s 30-year mortgage rate starts to climb with expectations of Fed “Shock and Awful.”

Say hello to The Federal Reserve Board of Governors!

You must be logged in to post a comment.