US labor productivity output per hour declined -4.1% QoQ in Q2 while unit labor costs rose 10.2% QoQ.

Confounded Interest – Anthony B. Sanders

Financial Markets And Real Estate

US labor productivity output per hour declined -4.1% QoQ in Q2 while unit labor costs rose 10.2% QoQ.

When we look at tomorrow’s US jobs report, it is important to acknowledge that 1) The Federal Reserve has not yet removed the Covid stimulus (green line) and 2) the ADP payroll jobs added was only 132k in August while non-farm payrolls jobs added in July was 528k. That is quite a spread!

(Bloomberg) The hotly anticipated US jobs report has the potential to tip the scales toward a third jumbo-sized hike in interest rates later this month after a wave of data that point to a resilient consumer and high labor demand.

Friday’s report is one of the last marquee releases Fed officials will have in hand before the mid-September policy meeting to help them decipher a complex economic and inflationary puzzle.

Forecasts call for a healthy, yet more moderate 298,000 gain in August payrolls and for the unemployment rate to hold steady at 3.5%, matching the lowest in five decades. Solid wage growth is also expected amid a persistent mismatch between labor demand and supply.

Such figures, in conjunction with a blowout July employment print, improving consumer sentiment figures and a surprise pickup in job openings, could be enough to push the Fed to raise borrowing costs by 75 basis points, extending the steepest interest-rate hikes in a generation to curb an inflation surge.

As of this morning, Fed Funds futures data is still pointing to The Fed Funds Target rate rising from 2.50% to around 4% by the March FOMC meeting. That is still a large jump of another 150 basis points anticipated.

When inflation is so bad that REAL wage growth is negative (-3.31% YoY), I would hardly call that a strong economy for the middle class and low-wage workers.

We also see that REAL home price growth (existing home sales median price YoY – CPI YoY) has slowed to only 2.23% YoY in July.

As The Fed tightens, it is only growing to get worse.

Perhaps Biden can enthrall us with yet another “Corn Pop was a bad dude” story.

The ADP National Employment Report SA Private Nonfarm Level Change printed this morning confirming what most of us already knew … the US economy is slowing if not already in recession.

The ADP jobs added grew by only 132k in August as The Fed’s M2 Money growth slowed.

Since The Federal Reserve and Federal government overstimulated the economy when Covid surfaced in early 2020, The Fed’s balance sheet expanded to near $9 TRILLION which helped existing home sales median price YoY hit 25.2% in May 2021 but falling to 10.8% YoY in July 2022 as The Fed tightened rates.

It will be a monetary inferno if The Fed decides to actually unwind its $9 trillion balance sheet.

Mortgage application volume dropped and remained at a multi-decade low last week (back to 1997), led by an 8 percent decline in refinance applications, which now make up only 30 percent of all applications. Purchase applications have declined in eight of the last nine weeks, as demand continues to shrink due to higher rates and a weaker economic outlook.

Mortgage applications decreased 3.7 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending August 26, 2022.

The unadjusted Purchase Index decreased 4 percent compared with the previous week and was 23 percent lower than the same week one year ago.

The Refinance Index decreased 8 percent from the previous week and was 83 percent lower than the same week one year ago.

Just wait for The Federal Reserve to start unwinding its enormous balance sheet!

Unfortunately, Powell and Company don’t have a …

US home price growth is decelerating as The Federal Reserve let’s some of the air out of the monetary tires.

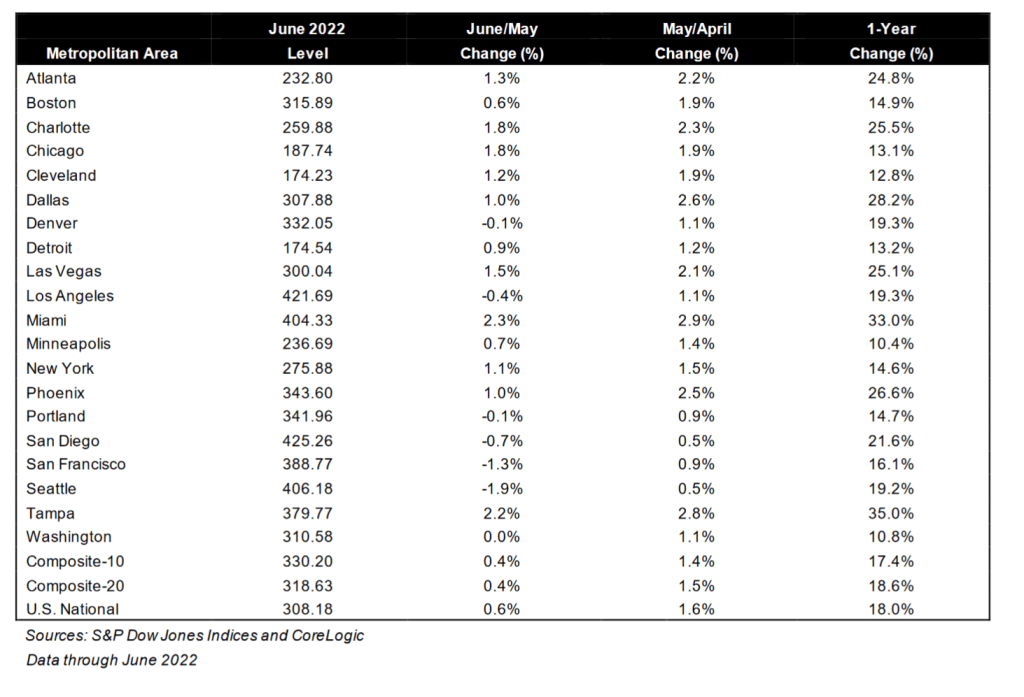

The S&P CoreLogic Case-Shiller U.S. National Home Price NSA Index, covering all nine U.S. census divisions, reported an 18.0% annual gain in June, down from 19.9% in the previous month. The 10-City Composite annual increase came in at 17.4%, down from 19.1% in the previous month. The 20-City Composite posted an 18.6% year-over-year gain, down from 20.5% in the previous month.

Tampa, Miami, and Dallas reported the highest year-over-year gains among the 20 cities in June. Tampa led the way with a 35.0% year-over-year price increase, followed by Miami in second with a 33.0% increase, and Dallas in third with a 28.2% increase. Only one of the 20 cities reported higher price increases in the year ending June 2022 versus the year ending May 2022.

While the Case-Shiller National home price index slowed to 18% YoY in June, the median price for existing home sales slowed to 10.55% YoY in July as The Fed’s M2 Money growth YoY slowed to 5.28% and Freddie Mac’s 30yr mortgage rate rose to 5.3%.

Bear in mind that Case-Shiller is lagged compared to the existing home sales numbers. Much like the New York Yankees manager picking the hottest batter in June to start in September. The Yankees traded poor-hitting Joey Gallo to the LA Dodgers to supplement poor-hitting Cody Bellinger.

In any case, as of June 2022, the 20 metro areas covered by Case-Shiller all grew in price in double digits with alligator-infested Tampa and Miami FL in the 30% rate, rattlesnake-infested Dallas is in 3rd place at 28.2%. Phoenix AZ, where I used to live, slowed to 26.6%. Yes, I had rattlesnakes on my property (a nest of Mohave Rattlers) and a large Diamond-backed Rattler behind my house).

Let’s see how housing holds up with more Fed monetary tightening. Fed Chair Powell is predicting “pain.”

As inflation burns the US middle class and low wage workers, The Federal Reserve reaffirmed at Jackson Hole that they are the NEW Smoky The Bear (only The Fed can fight inflation fire!) But of course, Federal spending and energy policies can drive up prices too.

Having said that, the 2-year Treasury yield and 30yr mortgage rate are rising rapidly.

The Fed is trying to cool demand by raising rates after lax monetary policy since late 2008.

While the US 2-year Treasury yield is up only slightly today, the Eurozone is seeing their 2-year sovereign yields spiking by 11-15+%.

The Federal Reserve’s overnight repo facility where banks park their money is seemingly becoming permanent.

As inflation has soared near the highest in 40 years, banks are increasingly parking their money at The Federal Reserve.

To quote Joe Biden, “All is well in the garden.” But apparently, not is all well in the banking industry or with the mortgage industry.

It is amazing that Biden is rising in the polls, simply because he got several inflation-generating, crony pay-off bills passed through a Democrat-controlled Congress. Even more amazing is that Americans aren’t more furious with Biden given that inflation is still raging at 8.5% YoY and the US Personal Savings Rate to cope with raging prices is at -51.5% YoY.

It looks like one quick fix to the inflation problem is for The Federal Reserve to shrink its balance sheet. But they are taking their own sweet time doing it.

And then we have the S&P 500 index which has done poorly since Powell and The Fed have undertaken their “fight inflation” mantra caused by their own folly and Biden’s green, anti-fossil fuel policies. Not to mention Congress spending like drunken sailors in port.

But the same is going on in Europe where inflation is even higher than in the USA and the EUR/USD is plunging like a paralyzed falcon.

And then we have Biden shrinking the Strategic Petroleum Reserve (orange line).

And in Europe, we have Germany suffering through a horrible energy price spike.

Finally, here is a baseball card of former Dodger pitcher Billy Loes. He almost reminds me of Biden trying to think through a complex problem like student loan debt forgiveness that may cost taxpayers an average of $2,000 yet buy votes for Democrats at the midyear elections.

The elite class “economists” (aka, cheerleaders) are meeting at Jackson Hole, Wyoming this week. But while they are planning our future, the revision to the miserable Q2 Real GDP report came out this morning.

Real gross domestic product (GDP) decreased at an annual rate of 0.6 percent in the second quarter of 2022, according to the “second” estimate released by the Bureau of Economic Analysis. In the first quarter, real GDP decreased 1.6 percent.

So, the second pass at measuring Real GDP produced a slightly better number (-0.6% vs -0.9%).

But the GDP PRICE index revision worsened from 8.7% to 8.9%. Look at REAL personal consumption (yellow line) as M2 Money growth slows.

Let’s see how things go at The Fed party at Jackson Hole, Wyoming. It is appropriate for The Fed to hold their party/meeting at Jackson Hole (Teton County) since it has the highest concentration of wealth per household than any other county in the nation.

Yee-haw!

You must be logged in to post a comment.