Mike Lea and I wrote a paper entitled “Do We Need The 30yr FRM (Fixed-rate Mortgage)”. We argue that millions of Americans would benefit from an adjustable-rate mortgage like the 5/1 ARM for a host of reasons.

One good reason for a 5/1 ARM is the fact that it 134 basis points less expensive than the 30yr fixed-rate mortgage.

Mortgage rates have risen dramatically with the expectation of Fed rate tightening (green line).

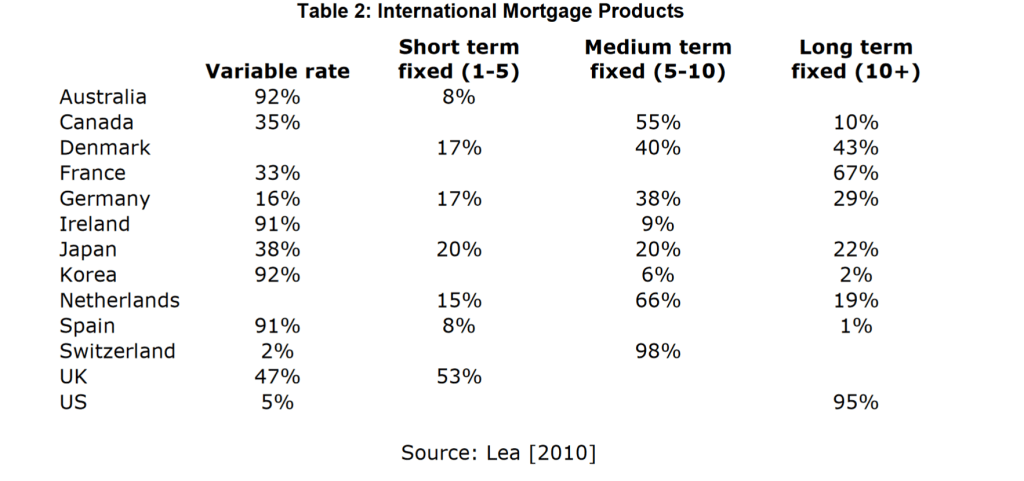

Yes, there is a “fear factor” built in the 30r FRM (“OMG! The mortgage market will collapse without the 30yr FRM!!!!) Hogwash. Or malarkey, as Joe Biden likes to say. The mortgage market actually see the US join the rest of the world in having adjustable-rate mortgage being the predominant mortgage product.

US ARM share peaked at 10.8% in June 2022 before retreating to 7.4% as the 30yr mortgage rate retreated.

The 5/1 ARM product can help the affordable housing crisis in the US if we just let markets work. But in Washington DC, the term “free markets” is like the old Dobie Gillis character Maynard G. Krebs and the word “Work.”

You must be logged in to post a comment.