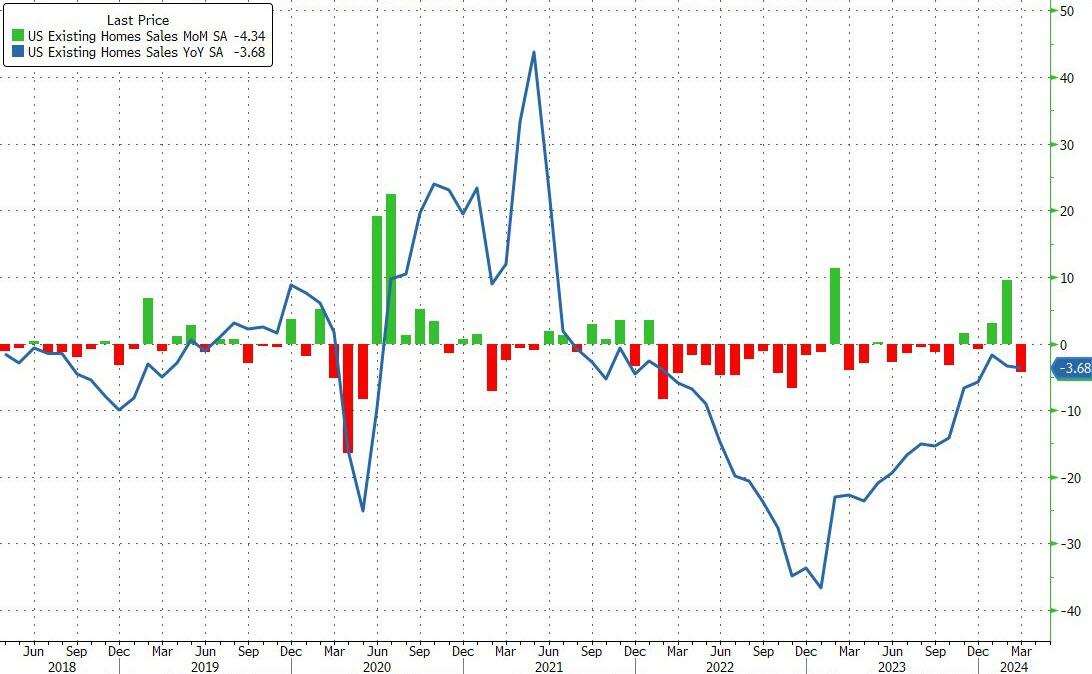

Sales were down almost 10% from a year earlier on an unadjusted basis, as sales of both single-family homes and condominiums and co-ops dropped.

Source: Bloomberg

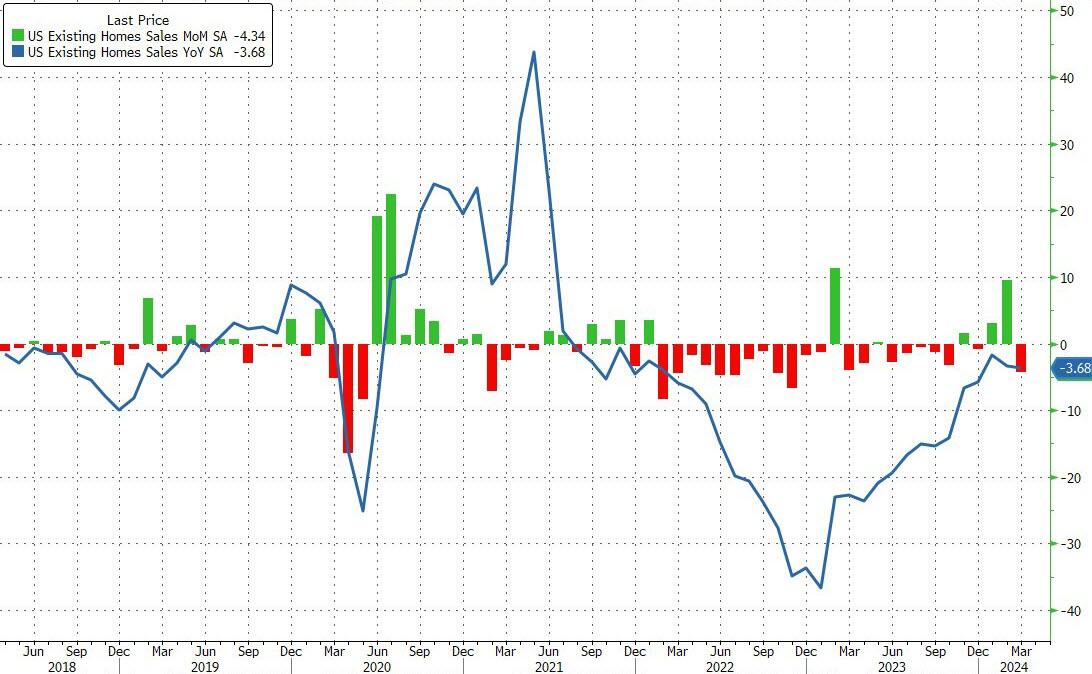

This dragged total existing home sales SAAR back down to 4.19mm…

Source: Bloomberg

“Though rebounding from cyclical lows, home sales are stuck because interest rates have not made any major moves,” said NAR Chief Economist Lawrence Yun.

“There are nearly six million more jobs now compared to pre-COVID highs, which suggests more aspiring home buyers exist in the market.”

…and it’s about to get worse…

Source: Bloomberg

Total housing inventory registered at the end of March was 1.11 million units, up 4.7% from February and 14.4% from one year ago (970,000). Unsold inventory sits at a 3.2-month supply at the current sales pace, up from 2.9 months in February and 2.7 months in March 2023.

“More inventory is always welcomed in the current environment,” Yun said.

“It’s a great time to list with ongoing multiple offers on mid-priced properties and, overall, home prices continuing to rise.”

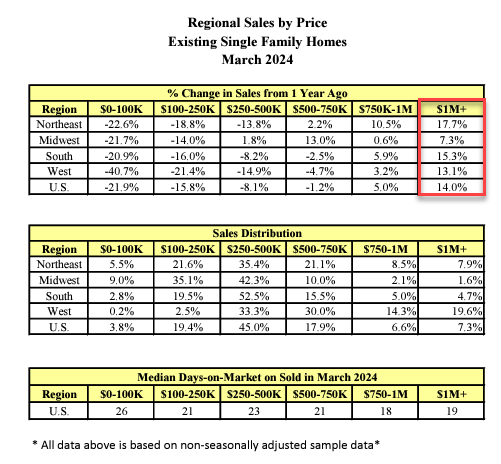

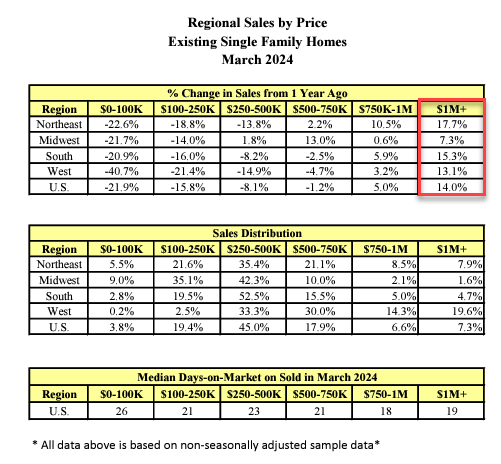

All price levels saw sales decline except $1mm+…

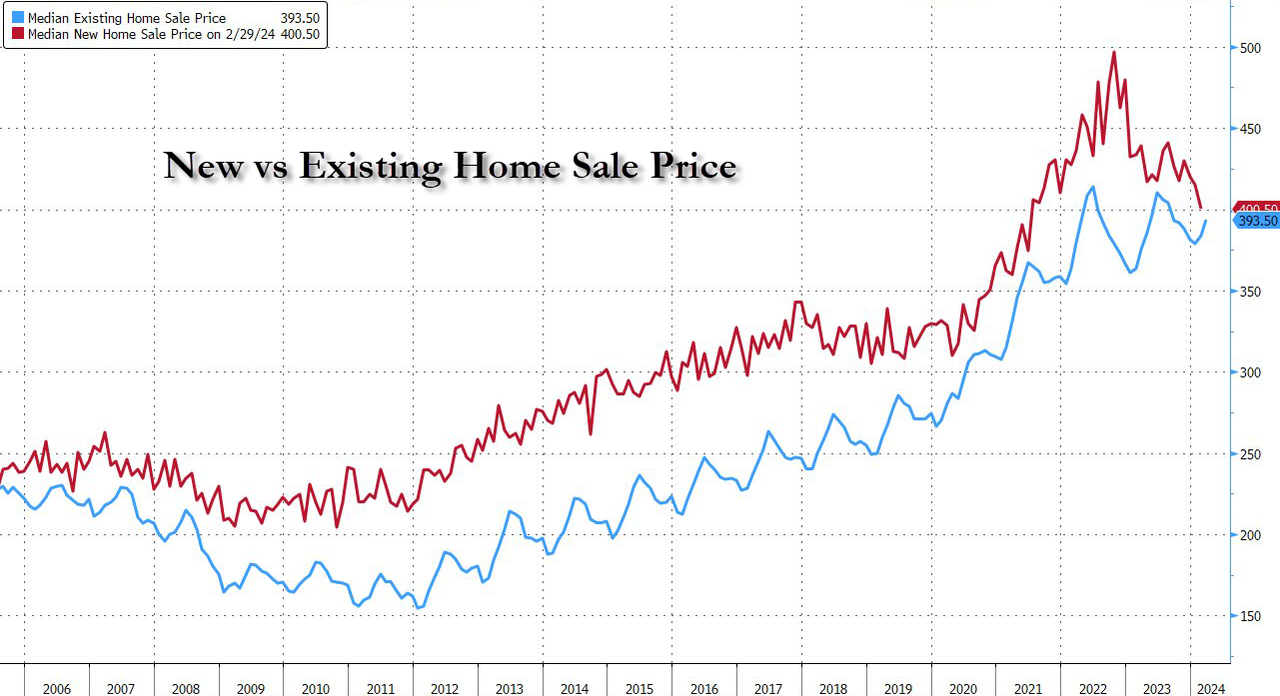

The median selling price increased 4.8% from a year ago to $393,500, the highest for any March on record.

Source: Bloomberg

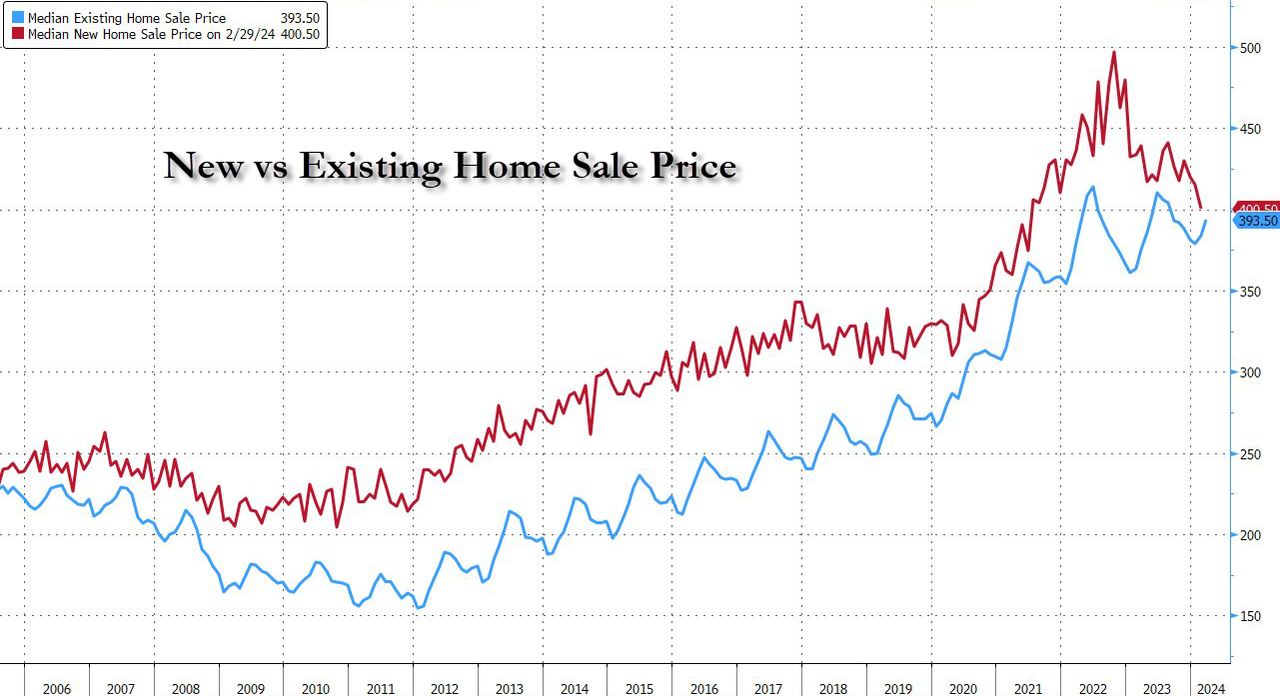

…and existing home prices are about to top new home prices…

Source: Bloomberg

First-time buyers made up 32% of purchases in March, up from 26% a month earlier.

Somehow, I don’t think Biden will brag about this report.

President Obama selected Slow Joe Biden as his Vice President because 1) he was white and 2) an alleged foreign policy wizard in The Senate. Between Afghanistan, Ukraine, Israel, Taiwan and every other foreign policy disaster under his leadership, I am beginning to doubt Biden’s foreign policy acumen. For example …

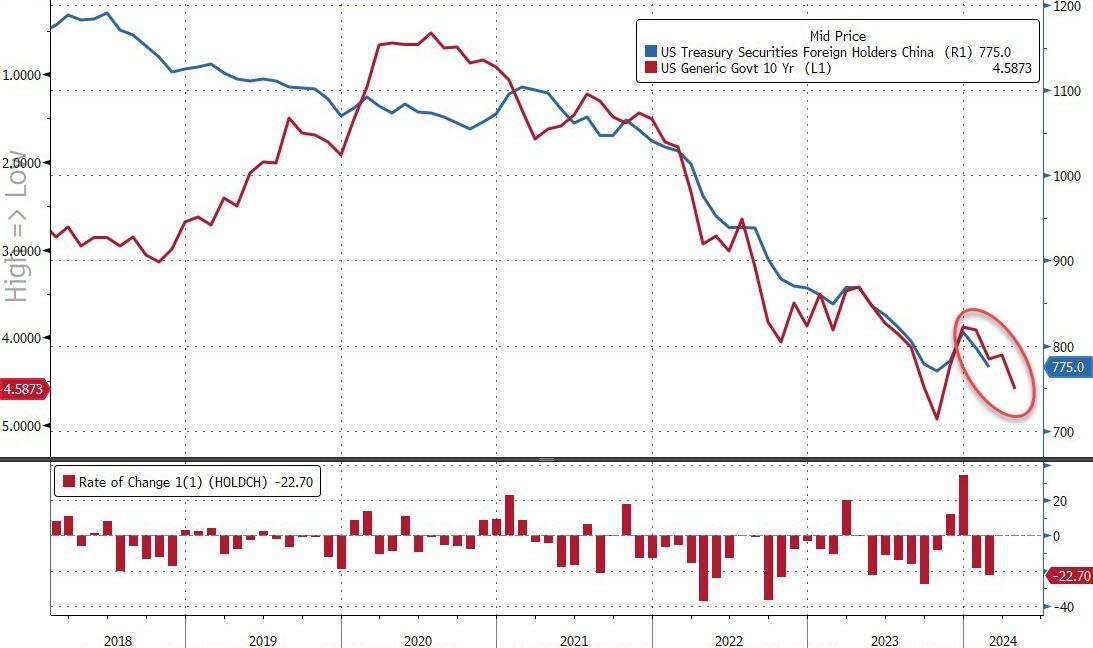

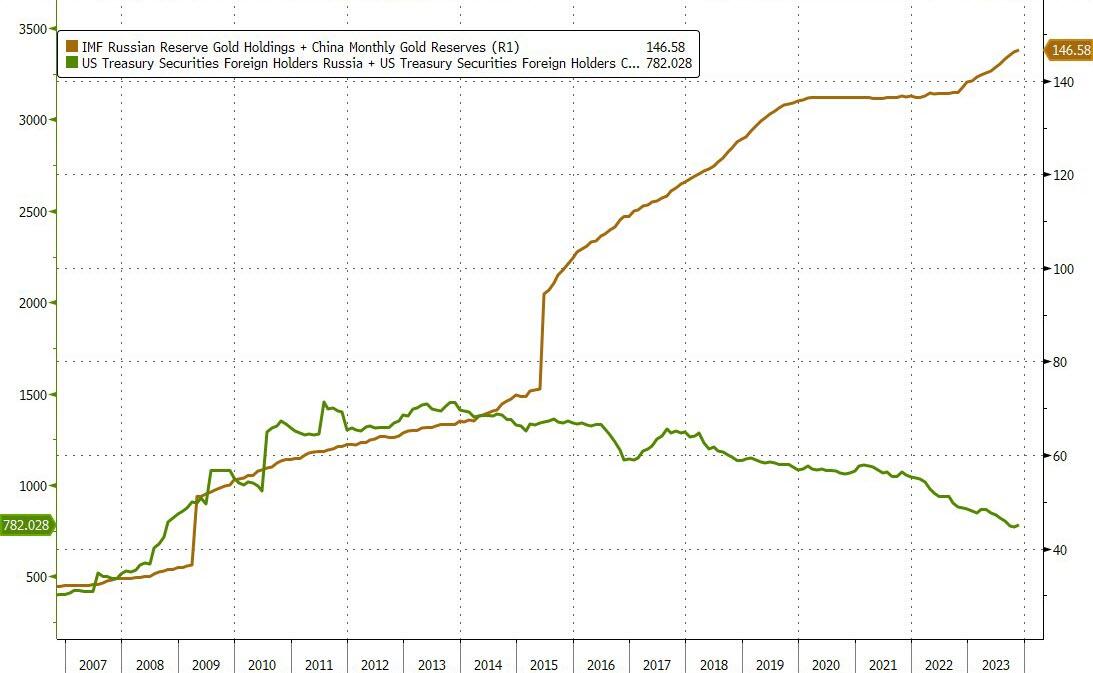

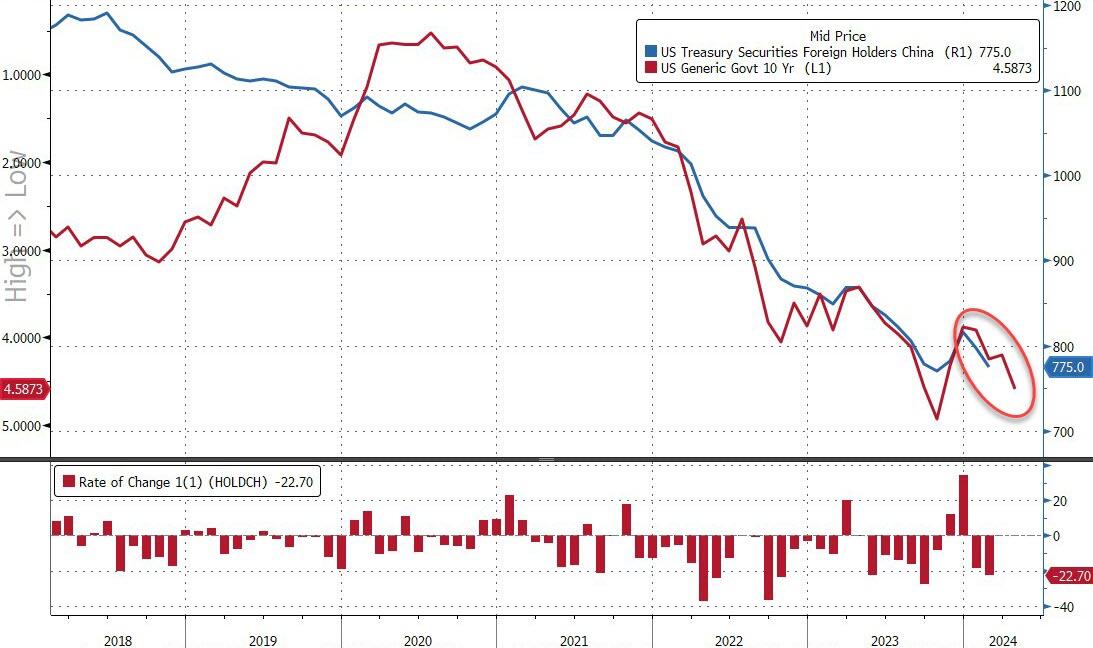

While we are acutely aware of the fact that ‘correlation is not causation’, one would find it hard to argue that the practically perfect concomitance of China’s Treasury holdings and the yield of the US 10Y Treasury note over the past three years makes us wonder (in our out-loud voices), if – away from The QT, The FedSpeak, the macro-economy, the geopolitical crises, the AI-hype, the growth scares – if it’s not just all a well-managed (slow and steady) liquidation of China’s (still massive) US Treasury holdings…

Source: Bloomberg

It’s hard to argue they don’t have an incentive to a) de-dollarize, and b) not liquidate it all at once, shooting themselves in the face.

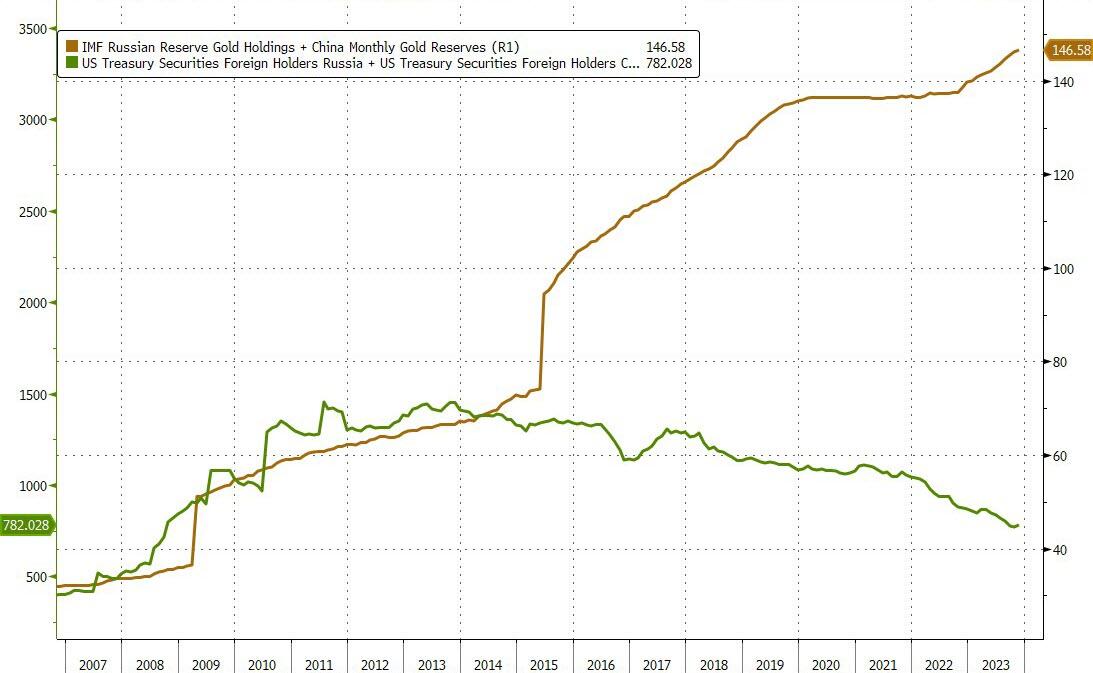

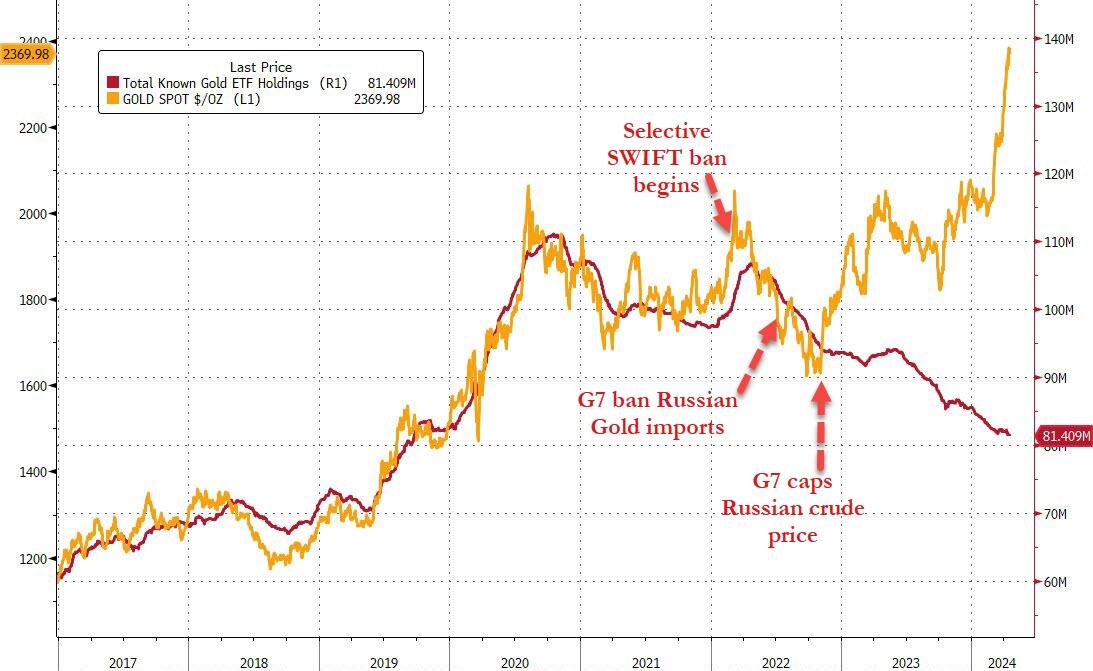

While the de-dollarizing has been steady in Treasury-land (enabled by a vast sea of liquid other players), things have been a little more ‘obvious’ in the alternative currency space – i.e gold.

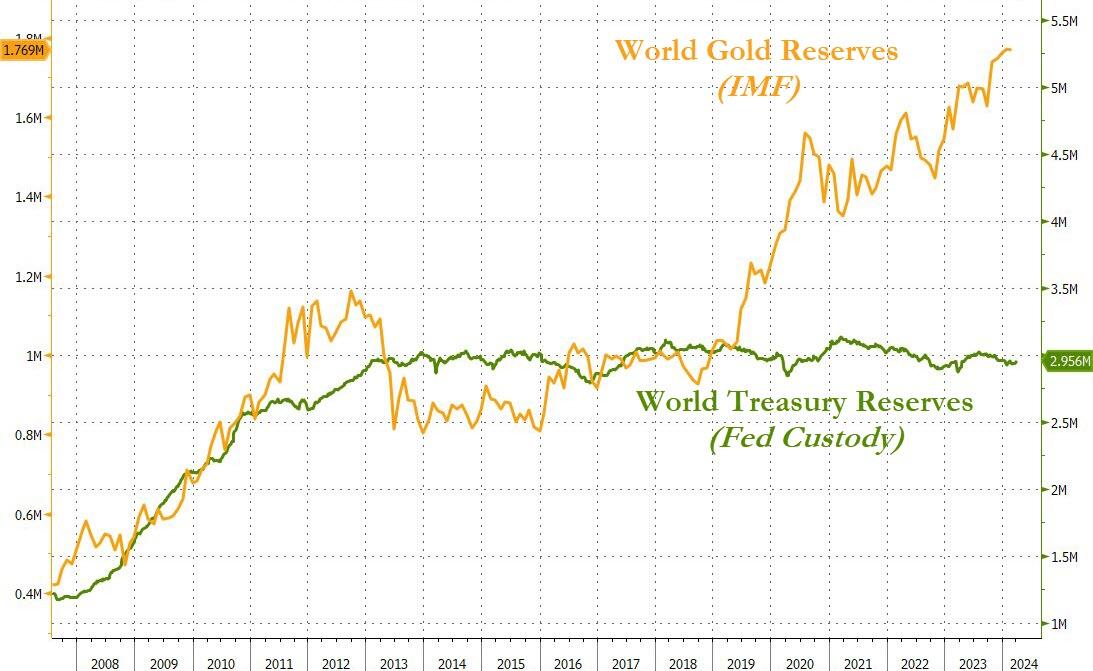

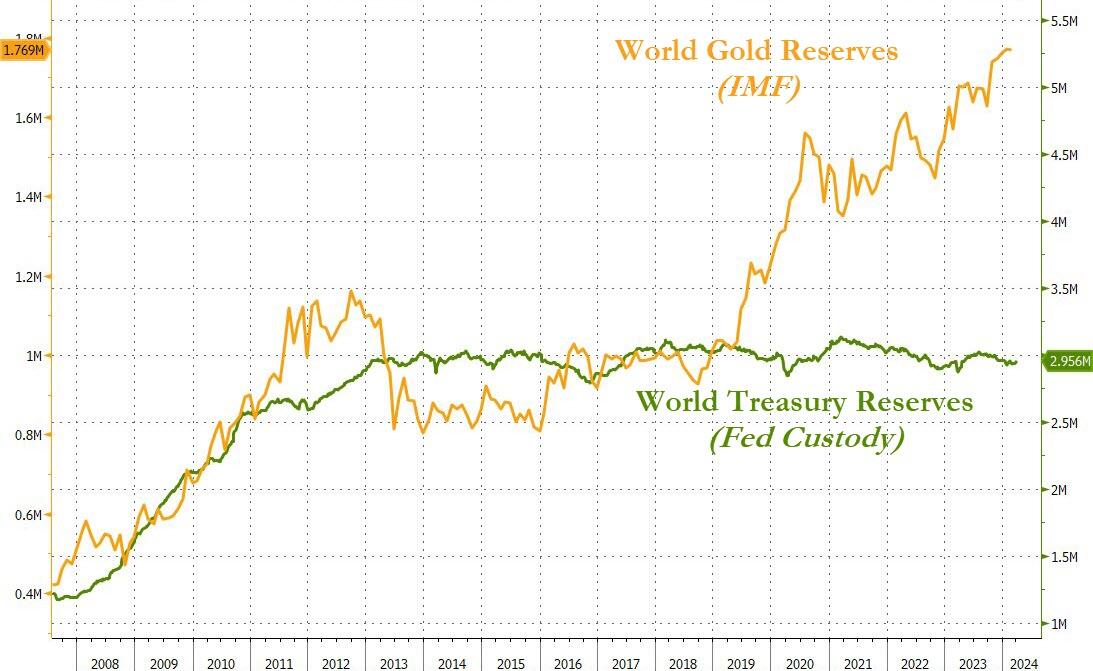

And in case you wondered, it’s not just China and Russia, world reserve Treasury holdings are ‘relatively’ flat (based on Fed’s custody data) while according to The IMF, the world’s sovereign nations have been buying gold with both hands and feet…

Source: Bloomberg

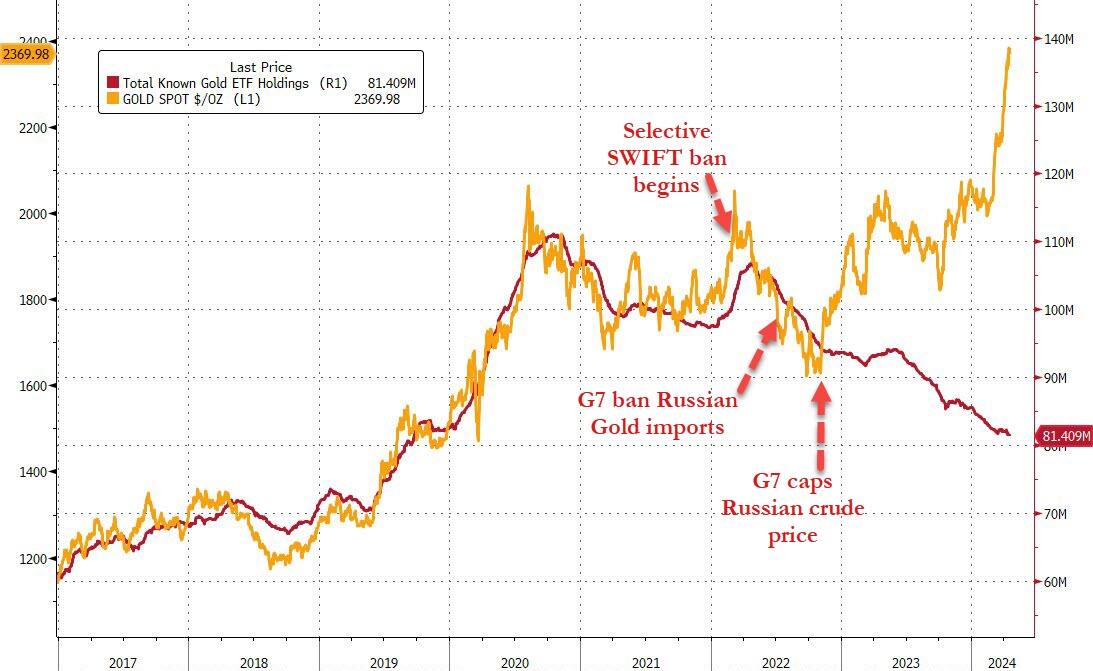

…happy to take whatever retail-ETF-sellers are offering into their physical vaults…

Source: Bloomberg

Finally, as we note in the chart, this all started to ‘escalate quickly’ when Washington really started to weaponize the dollar.

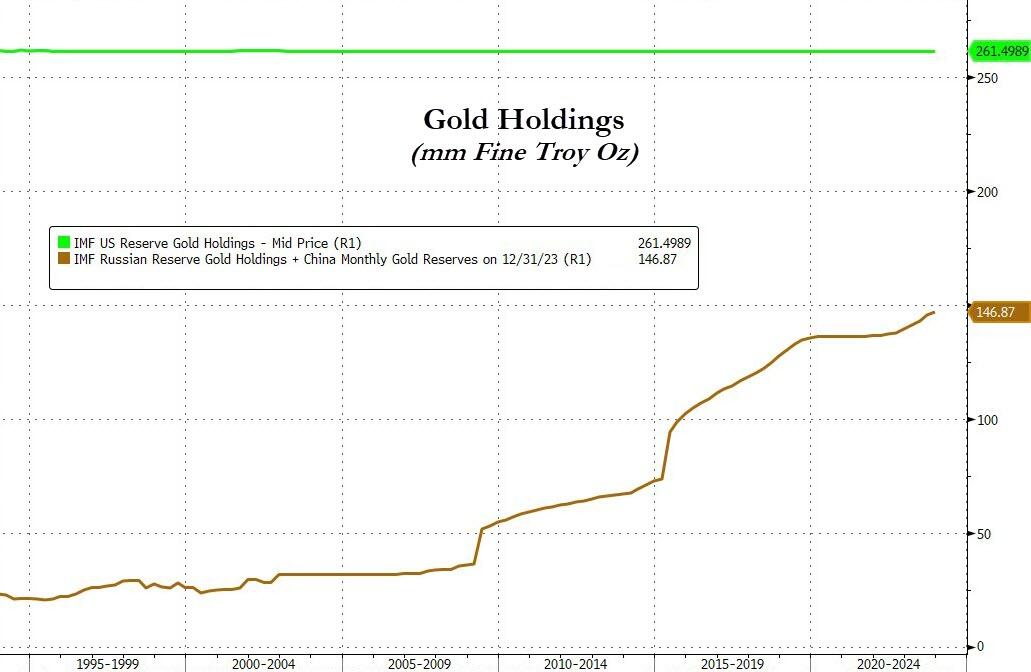

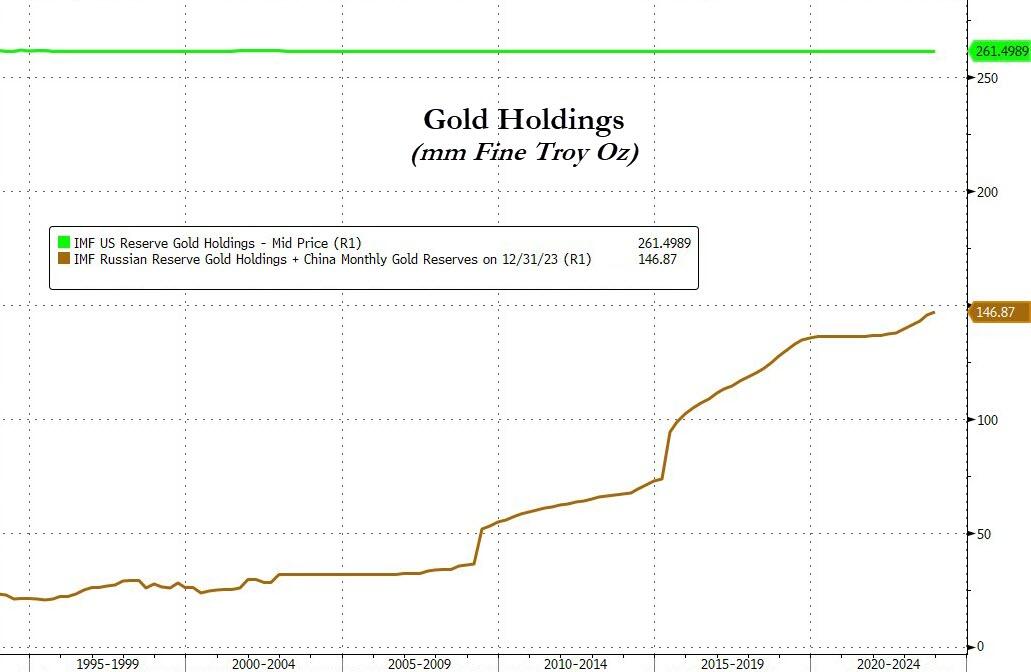

Assuming that all the US gold is still in Fort Knox (and assuming that China and Russia are honest about their holdings), the world’s ‘other superpowers’ are rapidly catching up to the US’ holdings…

Source: Bloomberg

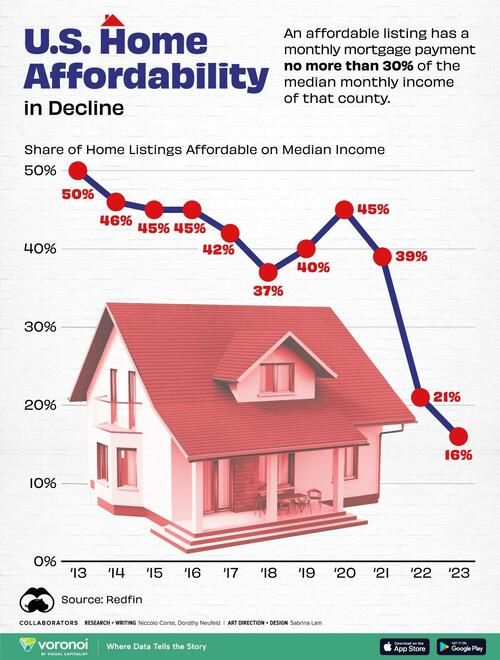

Who could have seen that coming? With mortgage rates hitting 7.5%, the home price to median household income ratio just hit an all-time high.

The 10Y Treasury yield just hit 4.519%.

And we have The Federal Reserve posting record losses.

Did we REALLY elect this fool Biden as President??

Biden lies constantly. This time about how HE reduced the Federal deficit. Odd since his student debt relief (buying votes) is going to raise the deficit by up to $750 BILLION.

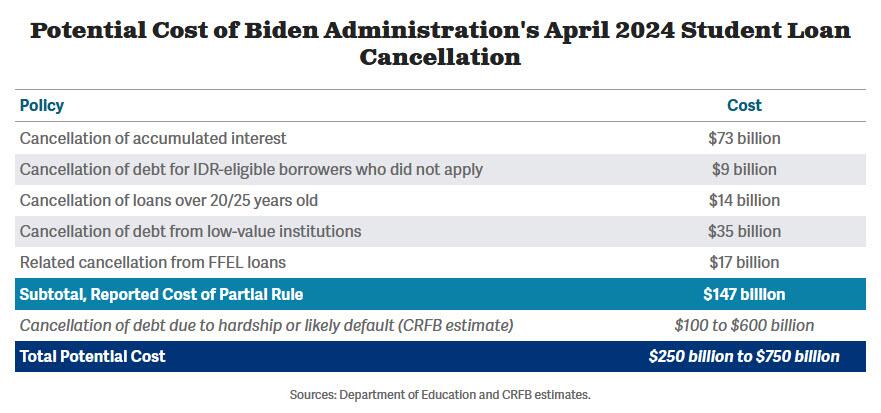

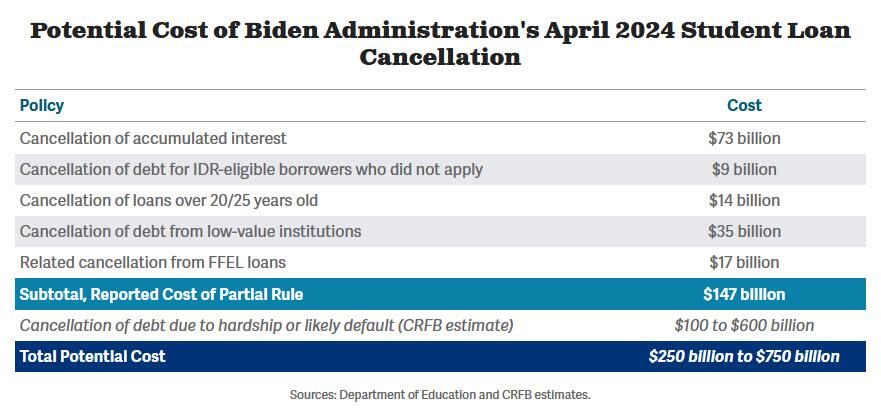

The Biden Administration recently announced a new plan to cancel student debt for up to 30 million borrowers and released a preliminary rule this morning detailing parts of this plan. The proposal, which is being introduced through the rule making process, would replace the Administration’s initial proposal to cancel between $10,000 and $20,000 per person of debt, which was struck down by the Supreme Court.

Elements of the plan in today’s proposed rule would cost nearly $150 billion, according to the Department of Education. However, this excludes a proposal to allow the Secretary of Education to cancel debt for those facing hardship or likely to default. Including this provision, we estimate the plan could cost $250 billion to $750 billion, depending on how the additional cancellation is designed.

The plan itself has five major components. It would:

Cancel accumulated interest for borrowers with balances higher than what they initially borrowed, capped at $20,000 for those in standard repayment and uncapped but restricted to individuals making less than $120,000 annually or couples making under $240,000 enrolled in an income-driven repayment (IDR) plan.

Automatically cancel loans for borrowers in standard repayment who would be eligible for cancellation had they applied for programs such as Public Service Loan Forgiveness (PSLF) or the new IDR program, Saving on a Valuable Education (SAVE).

Automatically cancel loans for borrowers who have been repaying undergraduate loans for over 20 years or graduate loans for over 25 years.

Cancel debt of those who attended low-financial-value programs, including those that failed accountability measures or were deemed ineligible for federal student aid programs.

Forgive debt of borrowers who are “facing hardships” or are likely to default on their loan payments.

The Department of Education has estimated the first four components of the plan would cost $147 billion over a decade, with half the cost stemming from the cancellation of accumulated interest. This is in line with estimates we are currently producing, though well above estimates of $77 billion from the Penn Wharton Budget Model (PWBM). A huge source of uncertainty is how these provisions would interact with existing IDR programs and how much of the debt would otherwise be cancelled under current policy.

Importantly, today’s rule does not include the Administration’s hardship cancellation plan, which would “authorize the automatic forgiveness of loans for borrowers at a high risk of future default as well as those who show hardship due to other indicators.”

This is by far the most unclear and potentially the most costly part of their proposal, since cancellation could be both wide-ranging and ongoing. We estimate this proposal could cost between $100 billion and $600 billion over a decade. However, there’s a tremendous amount of uncertainty, with design choices possibly resulting in much lower costs than our range – for example, PWBM estimates this provision would only cost $7 billion.

It is unclear how the Administration will define hardship, but they discuss 16 possible criteria such as other consumer debt, age, and health care or housing expenses and also declare hardship could be defined based on “any other indicators of hardship identified by the Secretary.” In assessing default risk, the rule allows cancellation for cancellation for those with an 80 percent likelihood of default, as determined by the Secretary. Importantly, over $150 billion of debt is currently in default (and loans in default generally have around a 70 percent recovery rate). We also estimate that a further 6 million borrowers are over 90 days delinquent on their loans, which is another predictor of a high likelihood of default and would further push up the number. The historically high rates of delinquency appear to be related to challenges around restarting student loan repayments last year.

While the default provision would be limited to the next two years under the most recent draft of the proposal, the hardship component has no time limit and thus opens a new venue for a future administration to cancel large amounts of student loan debt. An analysis by FREOPP argues that it could cover over 70 percent of college students.

In total, our $250 billion to $750 billion estimate for the total cost of the plan would be in line with the cost of the Administration’s $400 billion blanket debt cancellation, which was ruled illegal by the Supreme Court. It would be on top of more than $600 billion of debt cancellation already enacted through unilateral executive action. As we have shown before, these policies would put upward pressure on inflation and interest rates by supporting stronger demand, and much of the benefits would accrue to high-incomeandhighly-educated Americans. In the coming weeks, we will produce further analysis of the Administration’s latest proposal and continue to refine our cost estimates as more data is made available.

Mortgage applications increased 3.3 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending April 12, 2024.

The Market Composite Index, a measure of mortgage loan application volume, increased 3.3 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index increased 4 percent compared with the previous week. The seasonally adjusted Purchase Index increased 5 percent from one week earlier. The unadjusted Purchase Index increased 6 percent compared with the previous week and was 10 percent lower than the same week one year ago.

The Refinance Index increased 0.5 percent from the previous week and was 11 percent higher than the same week one year ago.

Bidenomics, a massive subsidy to the political donor class, but heartless towards the middle class.

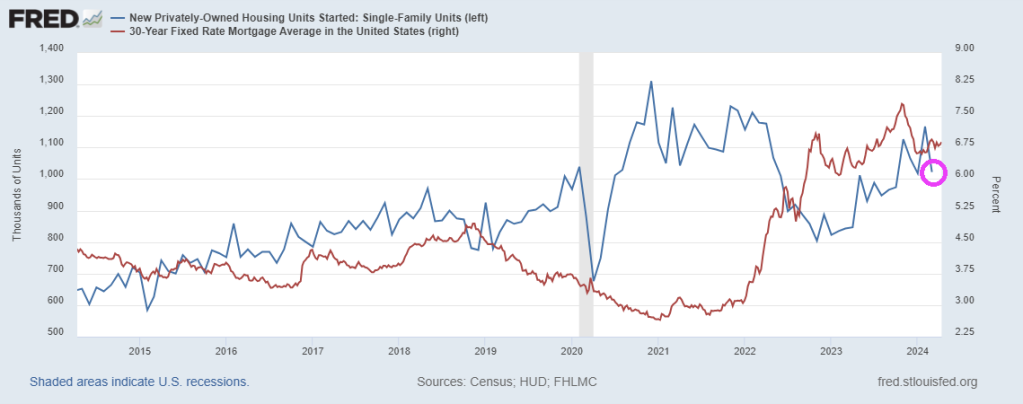

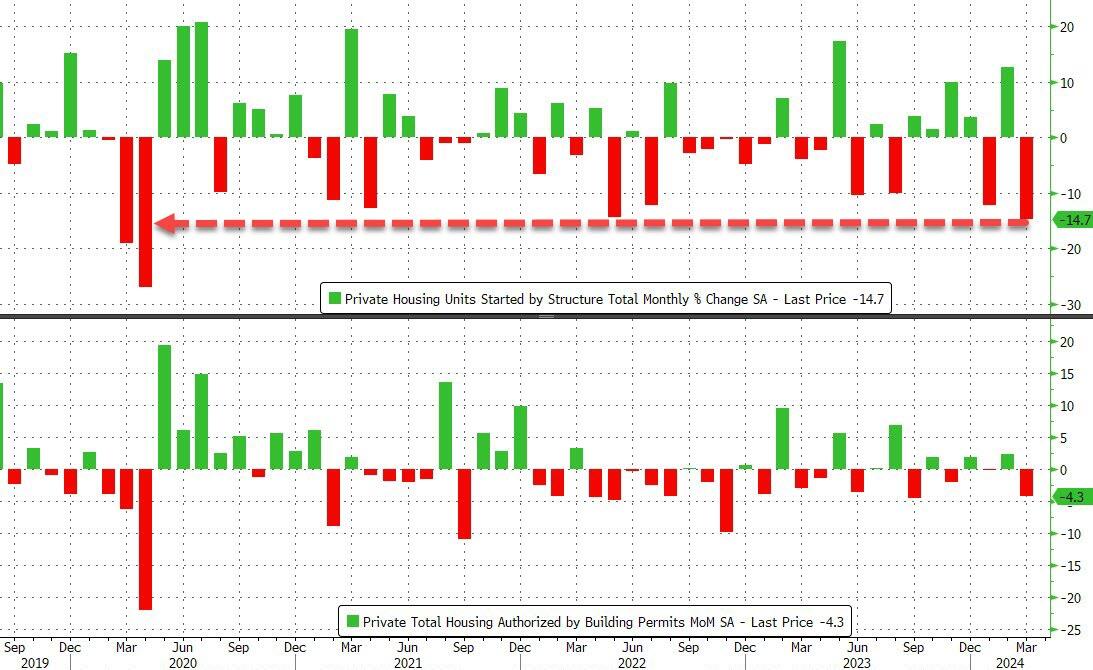

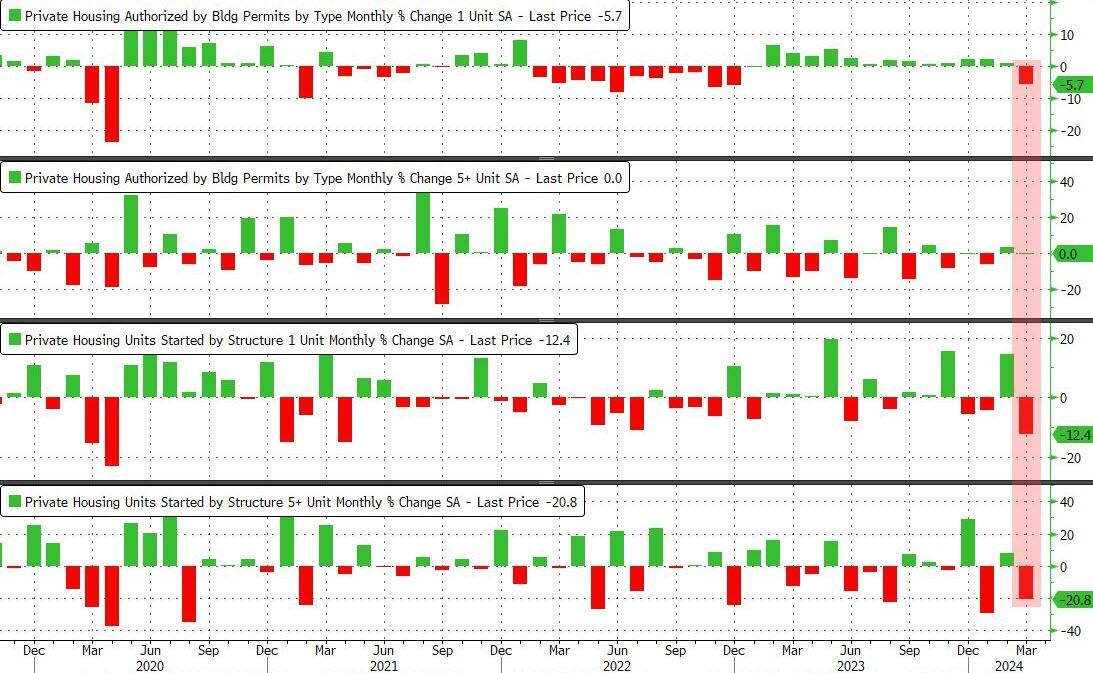

Come feel the noise! After steady growth in 1-unit housing starts under Trump, housing starts have been eratic under Biden despite the foreign invasion force of millions … of low wage workers.

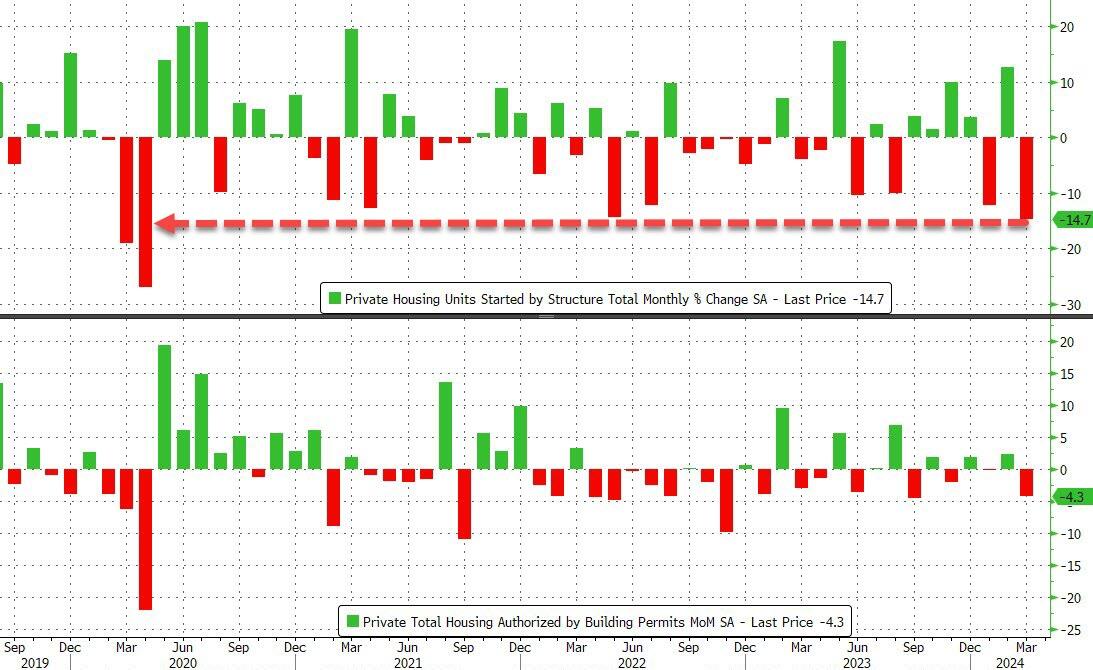

For context, this is the largest MoM drop in housing starts since the COVID lockdowns…

Source: Bloomberg

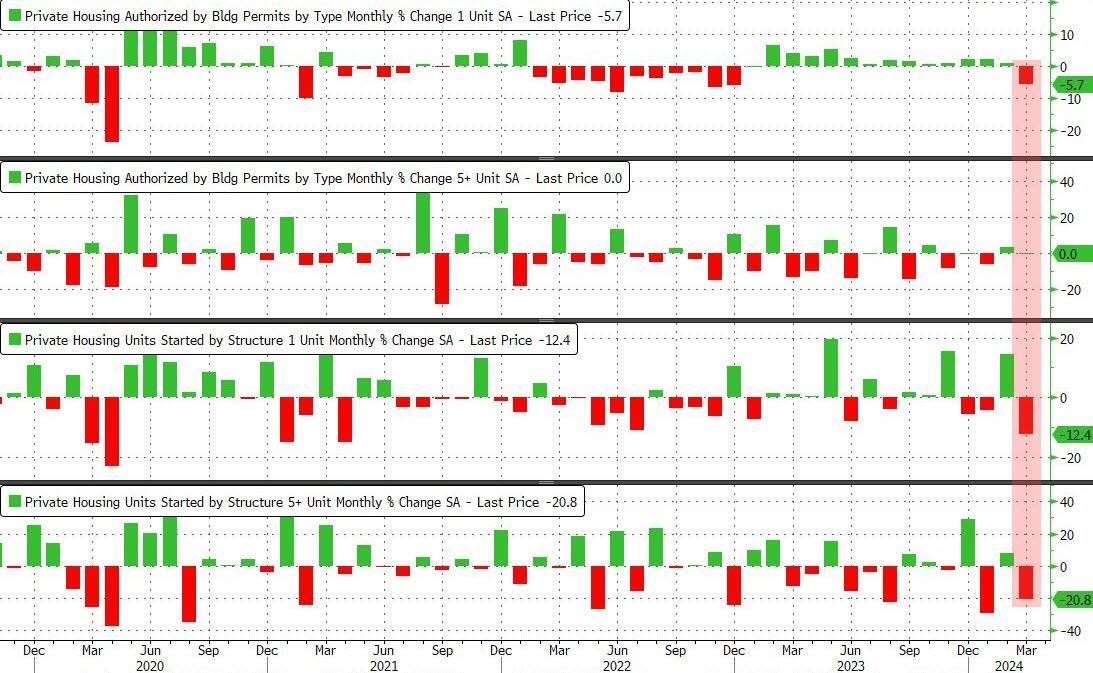

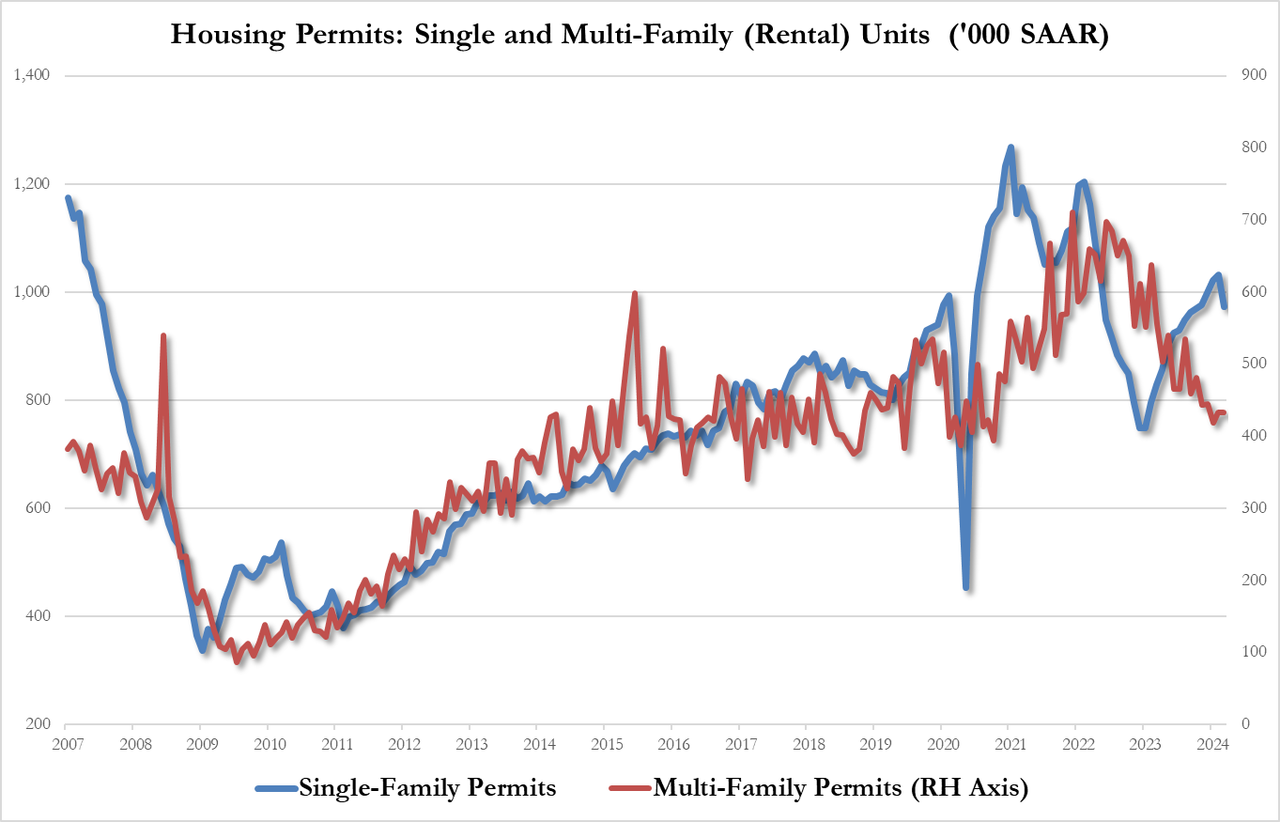

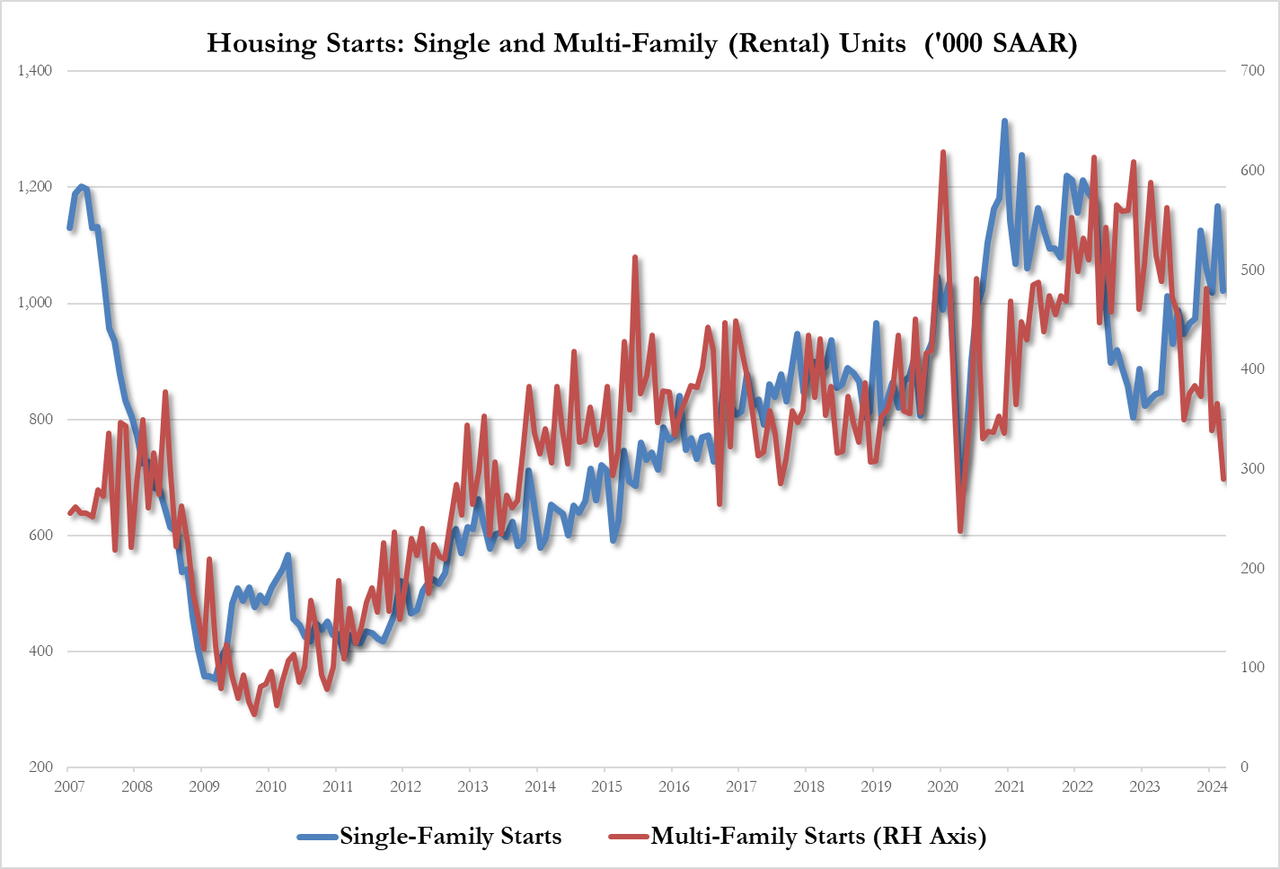

It was a bloodbath across the board with Rental Unit Starts plummeting 20.8% MoM…

Source: Bloomberg

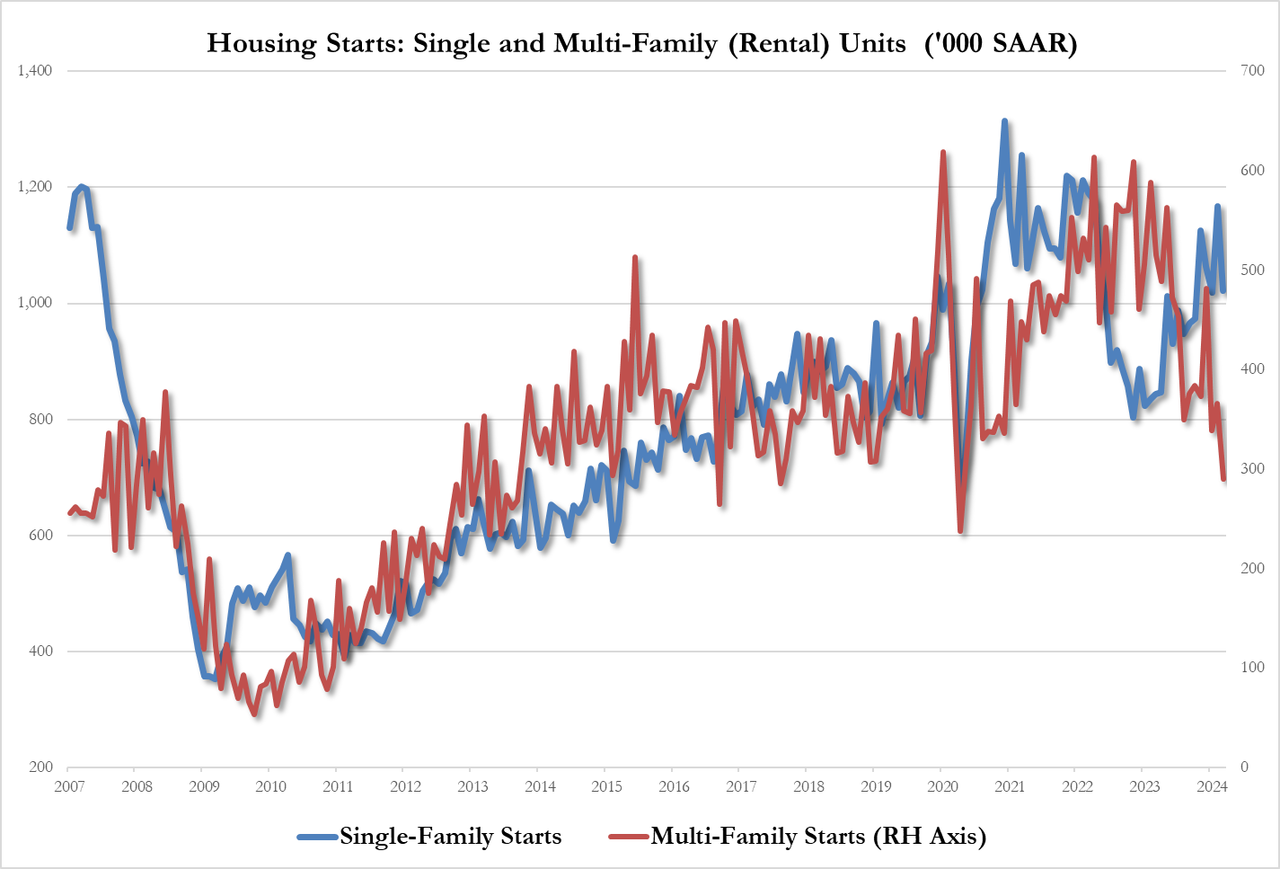

That pushed total multi-family starts SAAR down to its lowest since COVID lockdowns…

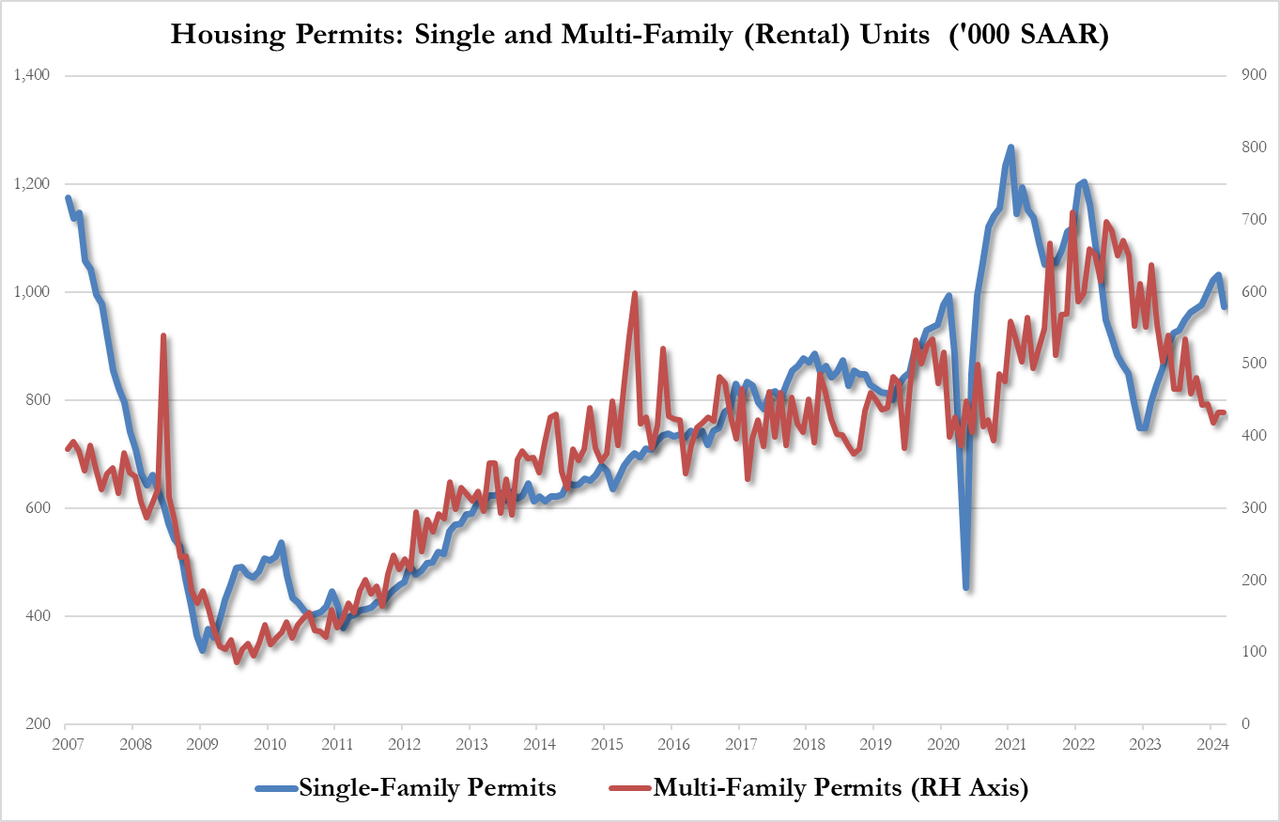

The plunge in permits was less dramatic and driven completely by single-family permits down 5.7% to 973K SAAR, from 1.032MM, this is the lowest since October. Multi-family permits flat at 433K

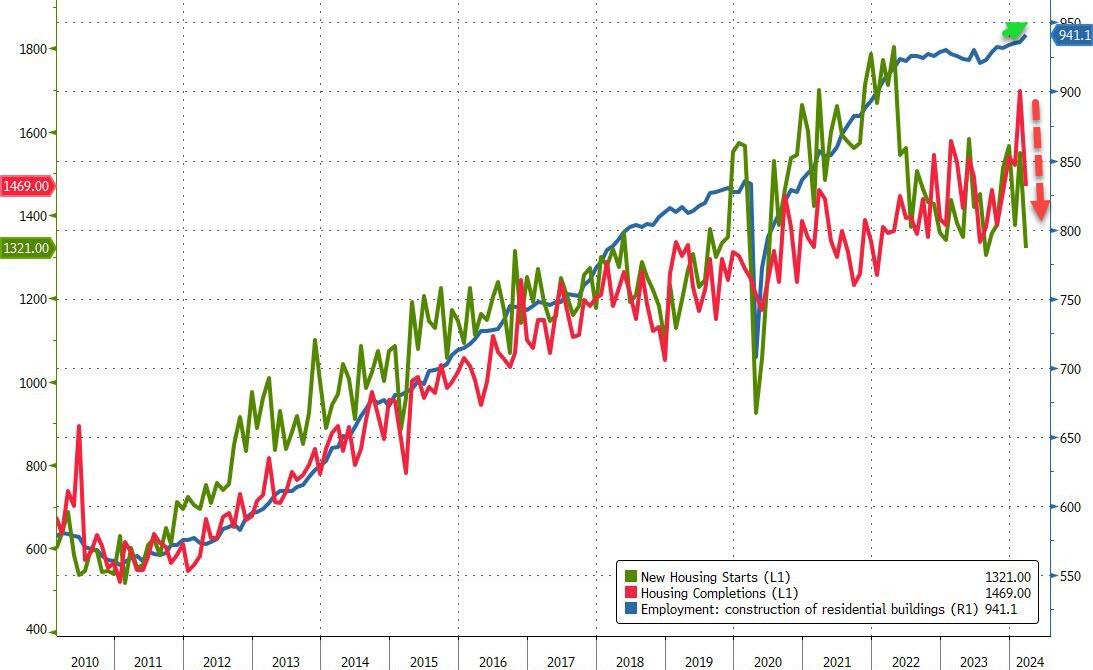

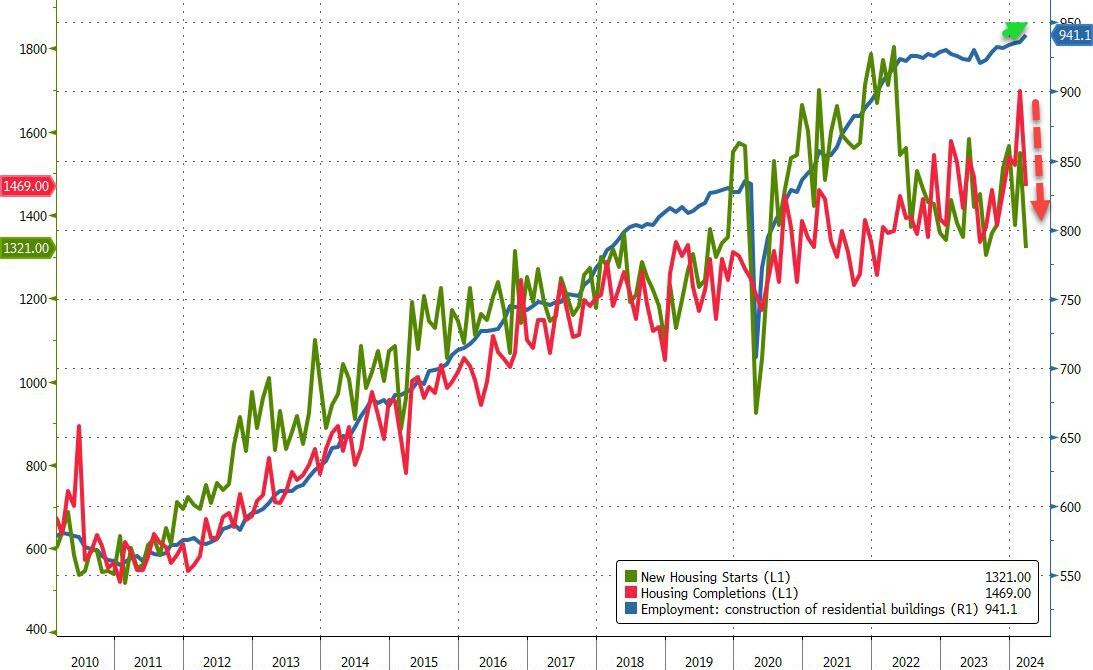

Intriguingly, while starts and completions plunged in March, the BLS believes that construction jobs surged to a new record high…

Source: Bloomberg

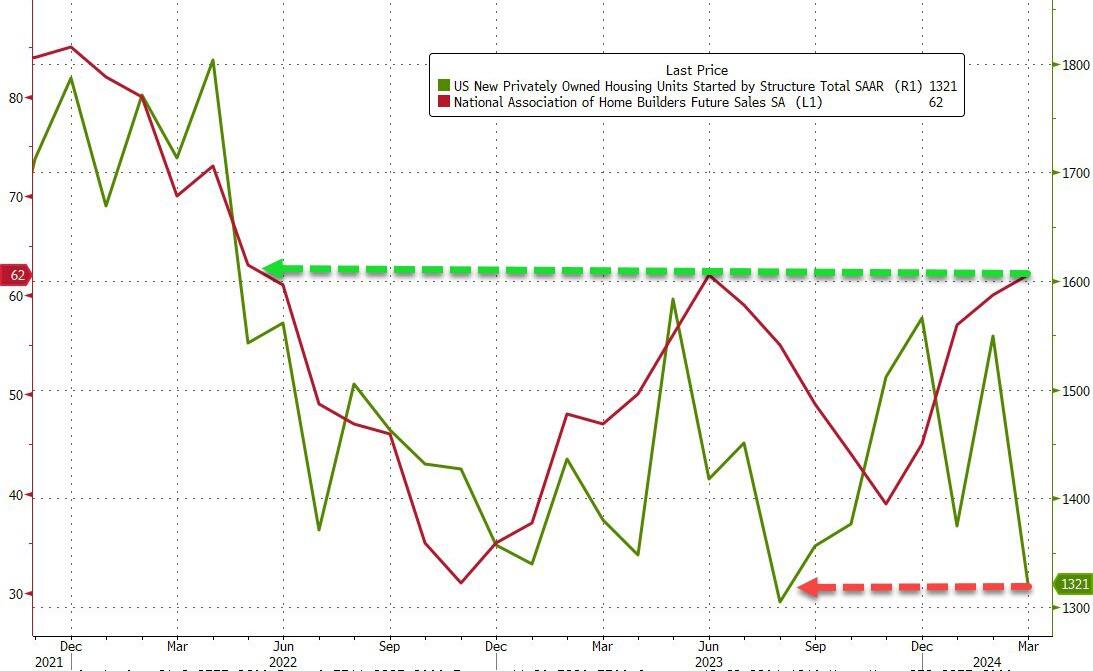

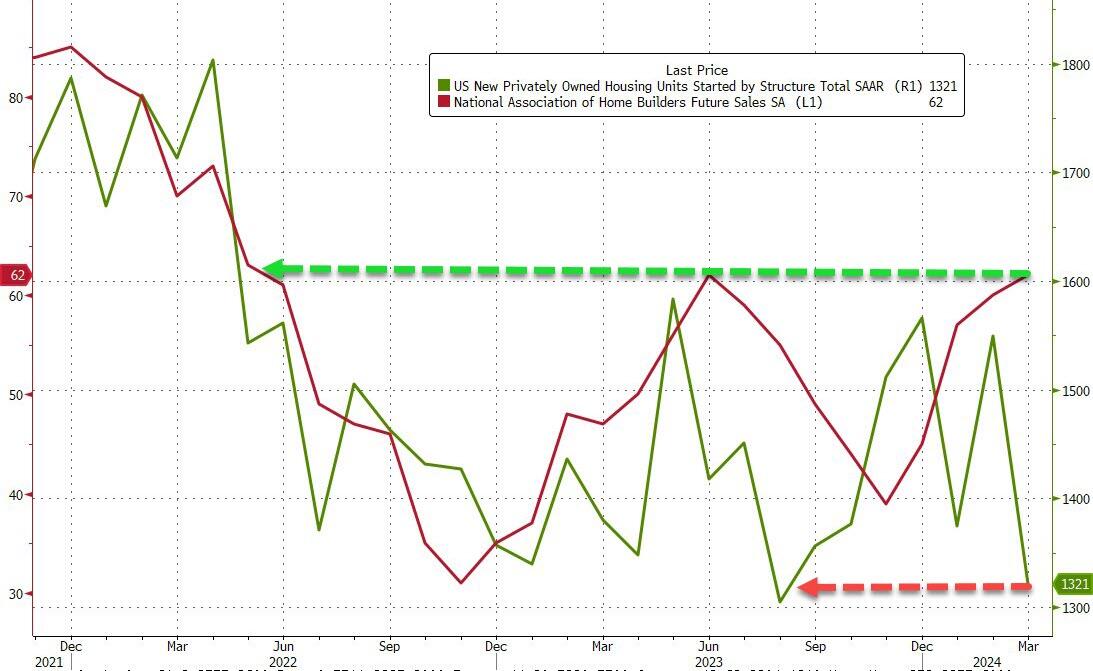

Finally, just what will homebuilders do now that expectations for 2024 rate-cuts have collapsed?

Source: Bloomberg

One thing is for sure – do not trust what homebuilders ‘say’ (as NAHB confidence jumped to its highest since May 2022 at the same time as housing starts crashed)…

Joe Biden likes to sell himself as “working class Joe” or “union Joe.” The truth is anything but. He is “Washington DC insider Joe” or “big corporate Joe.”

The US mortgage 30 year rate is down slightly today to 7.30%. That is a whopping 160% increase since Biden’s Presidency began.

Mortgage rates will continue to climb as the US Treasury 10-year yield climbs.

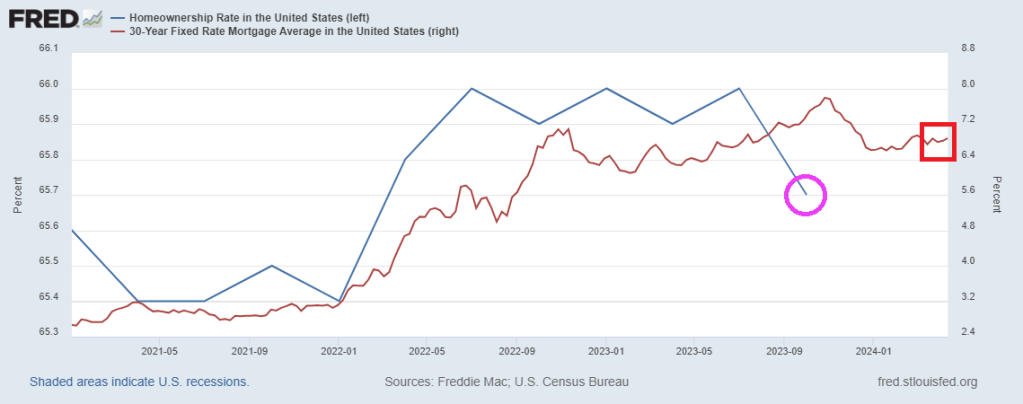

The US homeownership rate is falling as mortgage rates climb.

US CPI on trend for 4-5% at US election in November.

Source: BofA

Above 5%…?

Strong CPI raises market probability of YE25 rates above 5%.

Source: Goldman

Cyclical inflation remains too elevated

“Our measure of cyclical inflation–which should capture the impact of excess demand on prices–appears to be stuck at around 5%, which is too elevated”

Source: Safra

US alone

The US is the only economy in the G10 where the latest inflation print surprised to the upside.

Source: Goldman

200% of GDP

Under current policies, government debt outstanding will grow from 100% to 200% of GDP.

Source: Apollo

Close to $9 trillion in maturities

That’s a significant amount of government debt maturing within the next year.

Source: Apollo

Every year a deficit

OMB forecasts 5% budget deficit every year for the next 10 years.

Source: Apollo

A billion per day….is long gone

US government interest payments per day have doubled from $1bn per day before the pandemic to almost $2bn per day in 2023.

Source: Apollo

Biggest Story of 2020s…Ugly End of 40-year Bond Bull

Chart shows long-term US government bond (15+ year) rolling 10-year annualized returns, %.

Source: Flow Show

Highest yields in 15 years

The intermediate part of the yield curve still offers the highest yields in over fifteen years.

Source: Piper Sandler

Finally, electricity costs keeps rising, ESPECIALLY with the misnamed Inflation Reduction Act (IRA). The real name of the IRA should have been the Large Green Donor Increase Act (LGDIA).

Joe Biden, his Administration, and The Federal Reserve are really “The Alligator People.” Despite what they tell you, they have small brains (particularly Biden) and are hyperfocused on spending.

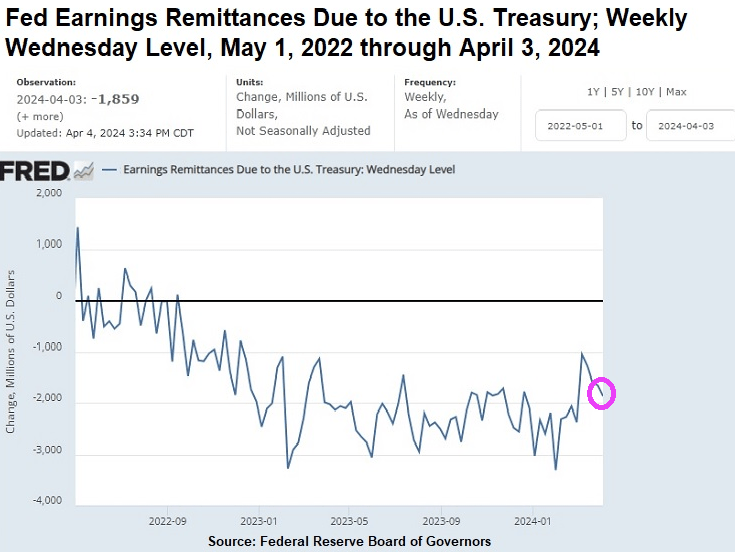

A good example comes from “Wall Street On Parade” where they show that The Federal Reserve is still paying BILLIONS to US Treasury in the form of remittances (losses). While at the same time, paying the mega banks on Wall Street high interest loans.

As of April 3 of this year, the Federal Reserve (Fed) has racked up $161 billion in accumulated losses. We’re not talking about unrealized losses on the underwater debt securities the Fed holds on its balance sheet, which it does not mark to market. We’re talking about real cash losses it is experiencing from earning approximately 2 percent interest on the $6.97 trillion of debt securities it holds on its balance sheet from its Quantitative Easing (QE) operations while it continues to pay out 5.4 percent interest to the mega banks on Wall Street (and other Fed member banks) for the reserves they hold with the Fed; 5.3 percent interest it pays on reverse repo operations with the Fed; and a whopping 6 percent dividend to member shareholder banks with assets of $10 billion or less and the lesser of 6 percent or the yield on the 10-year Treasury note at the most recent auction prior to the dividend payment to banks with assets larger than $10 billion. (This morning the 10-year Treasury is yielding 4.41 percent.)

Operating losses of this magnitude are unprecedented at the of Fed, which was created in 1913. In a press release dated March 26, the Fed stated this: “The Reserve Banks’ 2023 sum total of expenses exceeded earnings by $114.3 billion.”

As the chart above indicates, the Fed’s ongoing weekly losses have ranged from a high of $3.3 billion for the week ending Wednesday, January 31, 2024, to $1.86 billion for the most recent week ending Wednesday, April 3, 2024.

American taxpayers have good reason to sit up and pay attention to the Fed’s giant and ongoing losses. That’s because when the Fed is operating in the green, as it was on an annual basis for 106 years from 1916 through 2022, the Fed, by law, turns over excess earnings to the U.S. Treasury – thus reducing the amount the U.S. government has to borrow by issuing Treasury debt securities. According to Fed data, between 2011 and 2021, the Fed’s excess earnings paid to the U.S. Treasury totaled more than $920 billion.

WHO pays for the student loan forgiveness? It just doesn’t vanish, it is transferred to taxpayers. Alligators like Alexandria Ocasio Cortez going on talk shows to argue the benefits of being free from financial obligations that student voluntarily agreed to. Say, can AOC get my mortgage forgiven?? Just kidding. Now those same students can borrow additional money to get MBA degrees with the expectation that the student loan is “free money.”

Yes, Biden is acting recklessly (no surprise). Here is a picture of King Gator, Joe Biden.

The Biden Administration and The Federal Reserve ARE the alligator people. Except these gators are hungry for your money and votes constantly.

Despite Biden’s rambling that inflation is improving, bear in mind that the inflation rate is at it highest in 50 years. Yes, it has improved from 18% in 2022 to above 10% today.

A recent research paper by four noted economists, including Larry Summers, the former Treasury Secretary under Barack Obama and former Harvard President, discovered that the real inflation rate during the Biden years, using pre-1983 calculations reached 18% in 2022.

The number is the highest inflation rate the country has seen in over 50 years.

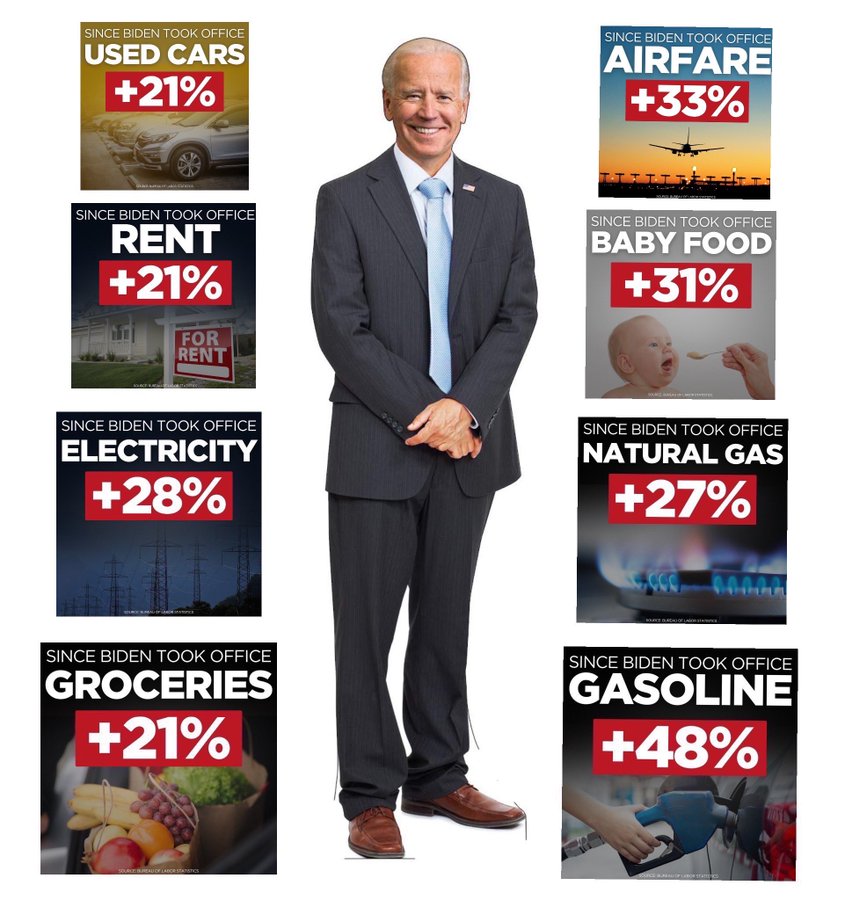

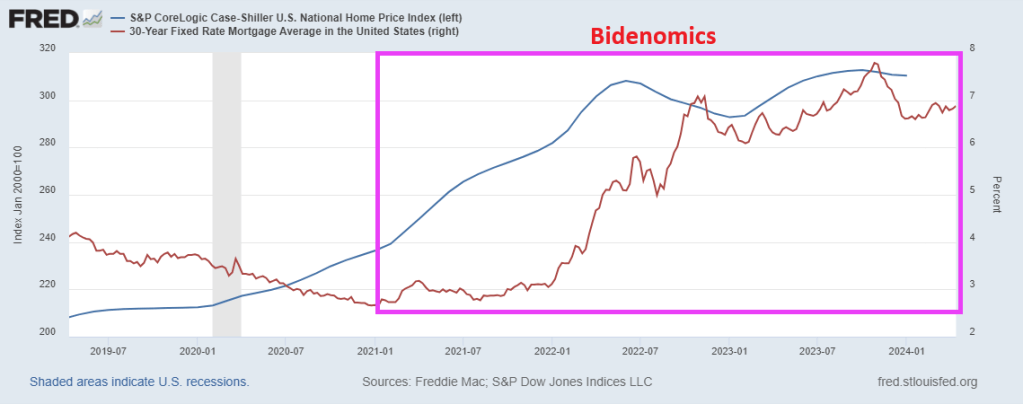

One reason that America’s youth is disgusted with Bidenomics is skyrocketing prices, particulalry housing. (simply unaffordable). Thanks to awful economic policies, home prices are up 32.5% under Biden and 30-year mortgage rates are up a whopping 160%! Good luck buying a home with a part-time job.

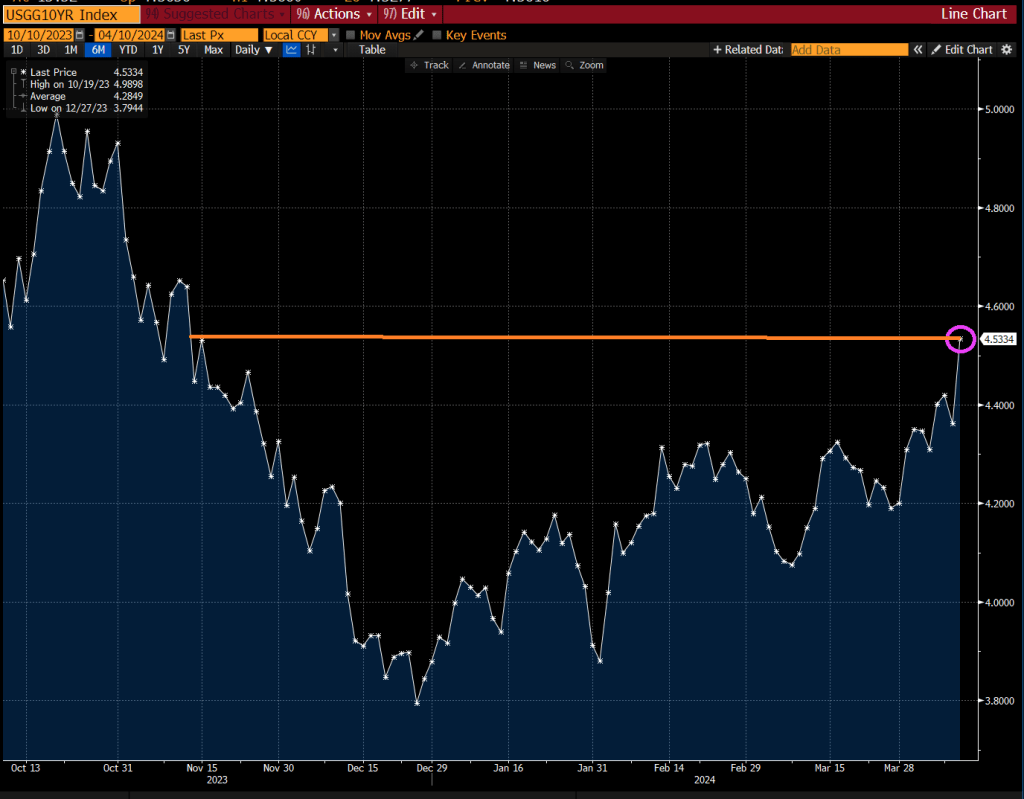

The bad news is that the 10-year Treasury yield rose to 4.53%, the highest since November 2023. This means that mortgage rates will rise even further.

Yes, rising rates AND home prices are daunting to part-time job holders.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

You must be logged in to post a comment.