- Rating company downgrades 10 lenders, citing dimmer outlook

- U.S. Bancorp, BNY Mellon among six firms facing potential cuts

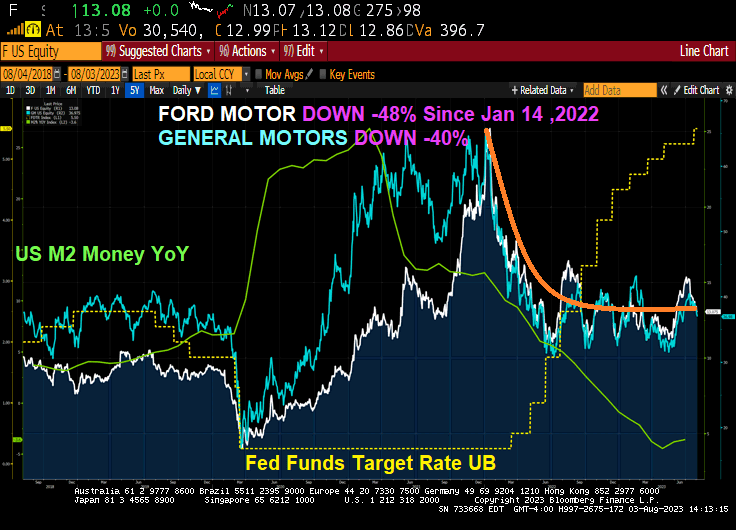

Not surprising given that Bidenomics is nothing more than giving big bucks to big corporations, including banks. Regional/small banks? Not so much.

Higher funding costs, potential regulatory capital weaknesses and rising risks tied to commercial real estate are among strains prompting the review, Moody’s said late Monday.

“Collectively, these three developments have lowered the credit profile of a number of US banks, though not all banks equally,” the rating company said.

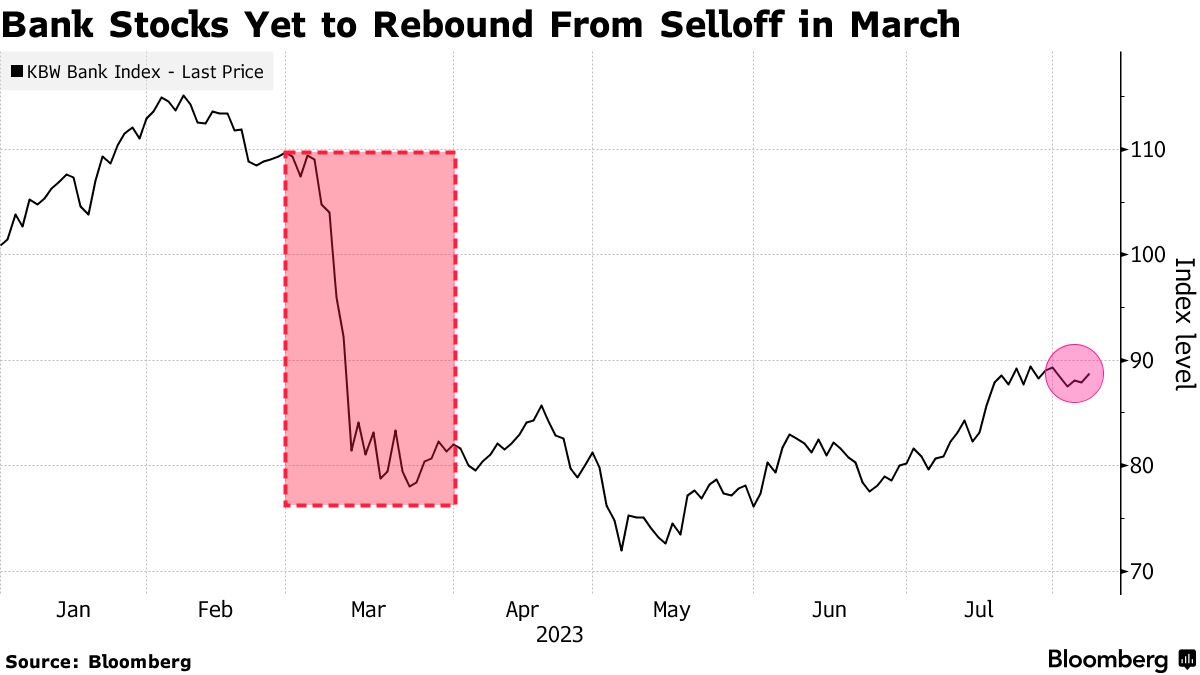

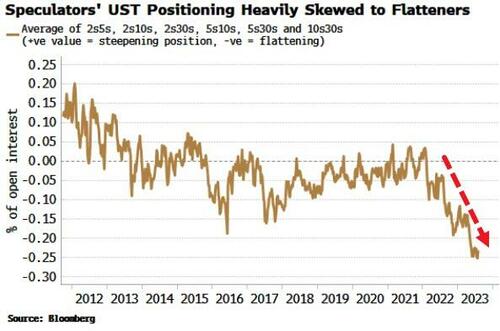

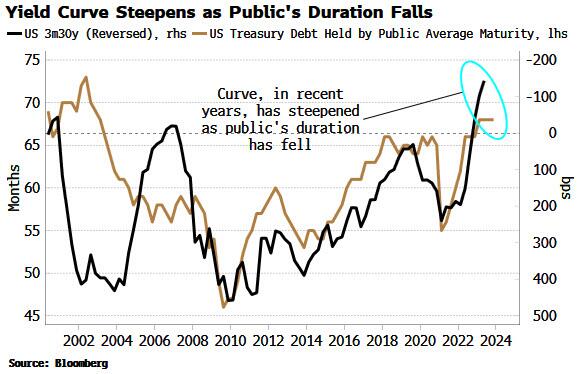

Moody’s Sees Problems Ahead for US Banks

Rating company issues raft of downgrades, outlook

Source: Moody’s

Shares declined for firms that had their ratings cut, including M&T Bank Corp., down 3.2%, and Webster Financial Corp., which lost 1.3%. Moody’s also adopted a “negative” outlook for 11 lenders, including PNC Financial Services Group, Capital One Financial Corp. and Citizens Financial Group Inc. Among those, PNC was down 2.2% and Capital One lost 2.4%.

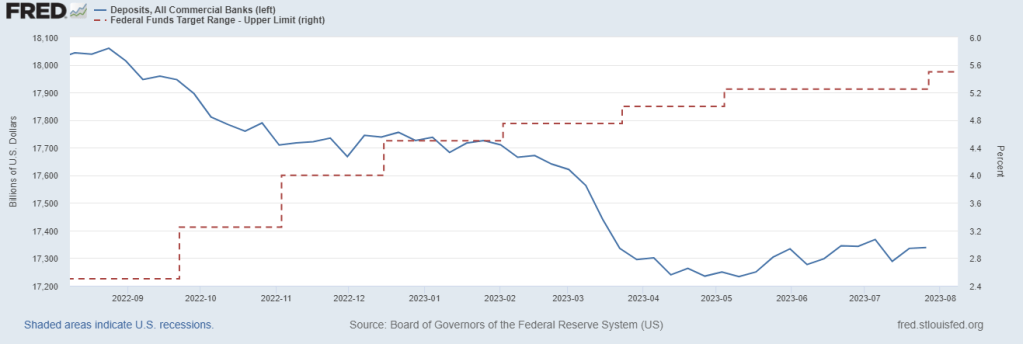

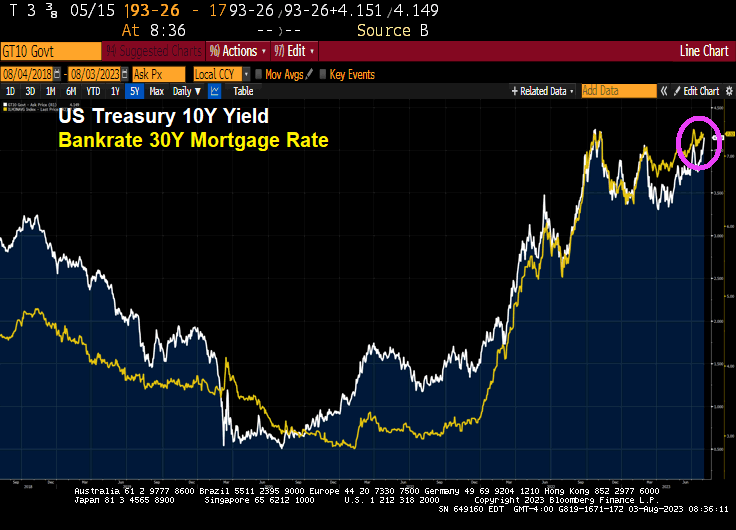

Investors, rattled by the collapse of regional banks in California and New York this year, have been watching closely for signs of stress in the industry as rising interest rates force firms to pay more for deposits and bump up the cost of funding from alternative sources. At the same time, those higher rates are eroding the value of banks’ assets and making it harder for commercial real estate borrowers to refinance their debts, potentially weakening lenders’ balance sheets.

“Rising funding costs and declining income metrics will erode profitability, the first buffer against losses,” Moody’s wrote in a separate note explaining the moves. “Asset risk is rising, in particular for small and midsize banks with large CRE exposures.”

Some banks have curbed loan growth, which preserves capital but also slows the shift in their loan mix toward higher-yielding assets, Moody’s said.

Banks that depend on more concentrated or higher levels of uninsured deposits are more exposed to these pressures, especially banks with high levels of fixed-rate securities and loans.

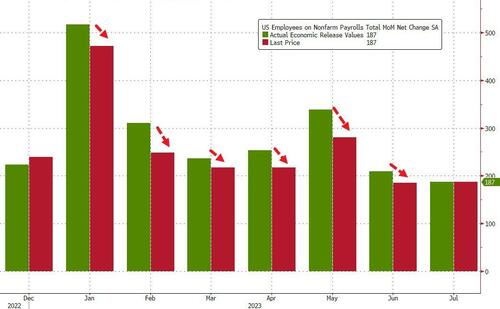

Deposits are declining as The Fed hikes rates.

So, Bidenomics reminds me of the film “Rollerball” where big corporations run the government and run a game akin to Rome’s gladiator fights.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

You must be logged in to post a comment.