As The Federal Reserve tries to fight inflation (it can’t thanks to Federal energy policies and bottlenecks), it is causing a disconnect between mortgage current coupon rate and the MBS index coupon. The disconnect is so bad that it is back to 1985 levels.

The Fed can certainly try to cool inflation, but Biden is intent on raising energy prices (leading to food price increases, and everything else) to shift us to electric cars. So, Biden is unlikely to back off.

So, The Fed is left trying to fight a war against inflation that only Biden can fight.

Meanwhile, the US mortgage market is getting pulverized

Yes, homebuyers are jumping into a generally slowing housing market to “beat the heat.” That is, beat The Fed’s monetary tightening.

Mortgage applications increased 2.0 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending May 6, 2022.

The seasonally adjusted Purchase Index increased 5 percent from one week earlier. The unadjusted Purchase Index increased 5 percent compared with the previous week and was 8 percent lower than the same week one year ago.

The Refinance Index decreased 2 percent from the previous week and was 72 percent lower than the same week one year ago.

Simply unaffordable! US housing, that is. As The Federal Reserve tries to fight inflation caused by Biden’s Medusa-like policies, mortgage rates are soaring and we are seeing an INCREASE in mortgage purchase applications ahead of Fed tightening. Panic in (Fed) Needle Park!

Mortgage applications increased 2.5 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending April 29, 2022. The Refinance Index increased 0.2 percent from the previous week and was 71 percent lower than the same week one year ago.

The seasonally adjusted Purchase Index increased 4 percent from one week earlier. The unadjusted Purchase Index increased 5 percent compared with the previous week and was11 percent lower than the same week one year ago.

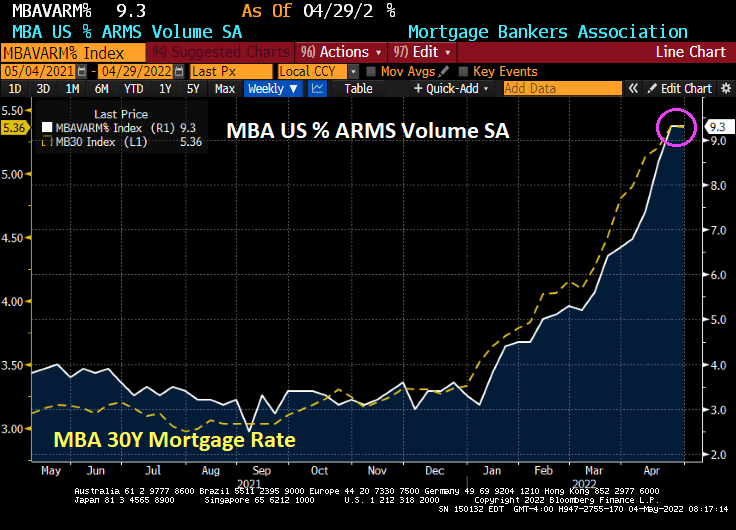

Adjustable rate mortgage (ARM) share has risen to 9.3% along with mortgage rates.

Between Biden’s energy policies, Congressional Covid relief and seemingly perpetual monetary stimulus from The Fed, we have 20% growth in home prices despite mortgage rates soaring.

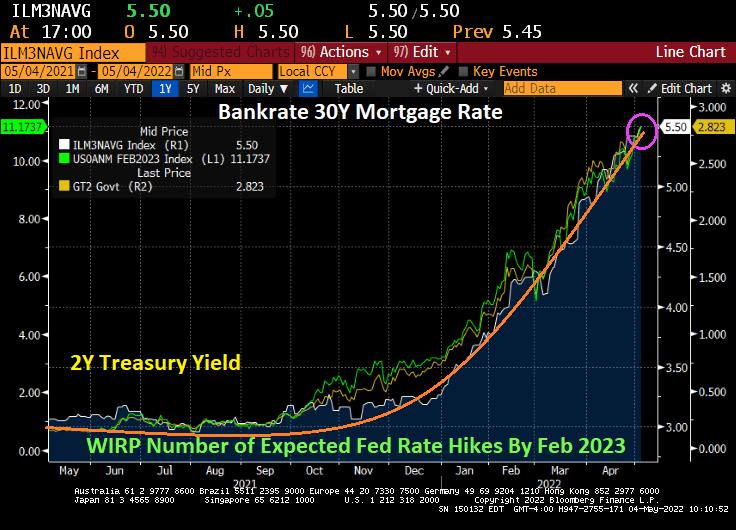

And as The Fed is expected to tighten, mortgage rates hit 5.50%.

From the MBA: Mortgage Applications Decrease in Latest MBA Weekly Survey. Mortgage applications decreased 8.3 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending April 22, 2022.

The Refinance Index decreased 9 percent from the previous week and was 71 percent lower than the same week one year ago.

The seasonally adjusted Purchase Index decreased 8 percent from one week earlier. The unadjusted Purchase Index decreased 7 percent compared with the previous week and was17 percent lower than the same week one year ago.

The percentage of adjustable-rate mortgages (ARMs) increase 9.4% from previous week.

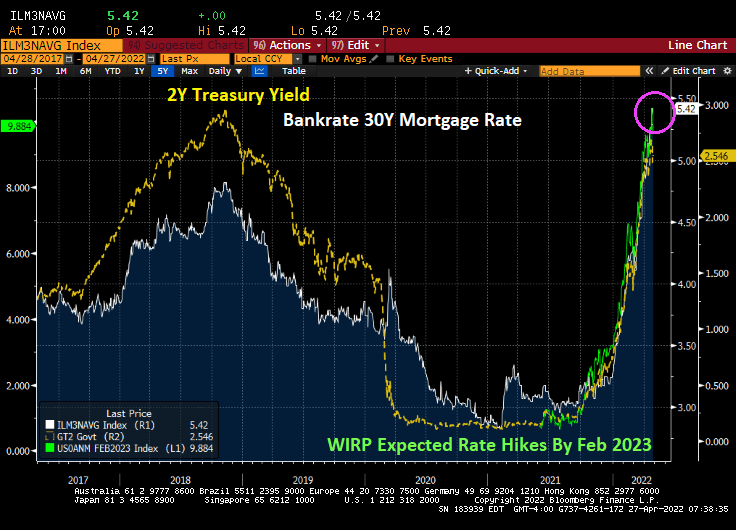

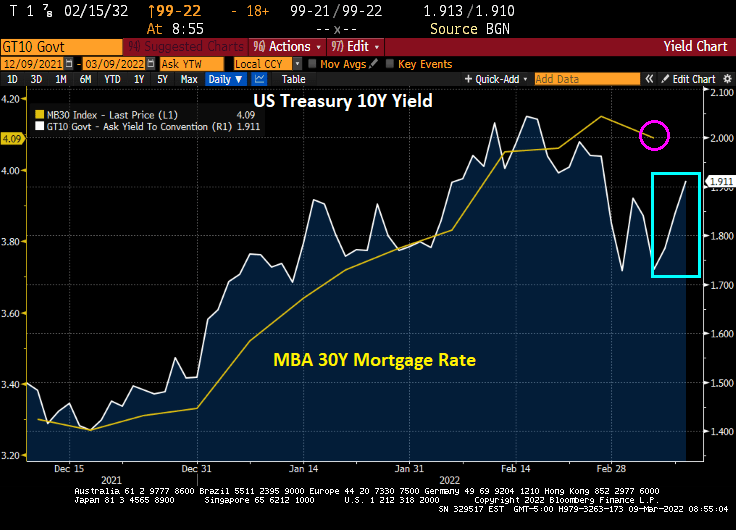

Yes, the 30-year mortgage rate is rising extremely fast.

“You’re Going Down” by Jerome Powell and The Constitution Avenue band. President Joe Biden conducting.

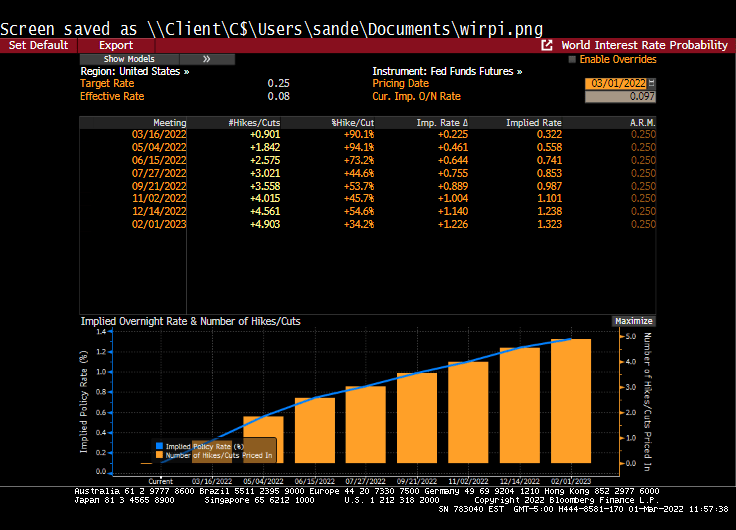

As The Fed sings “No sugar tonight” exemplified by the number of expected Fed rate hikes by February 2023 has grown to 10.4. Mortgage rates are now the highest since 2009, but inflation is the highest in 40 years. The result? The REAL 30-year mortgage rate is -3.25%.

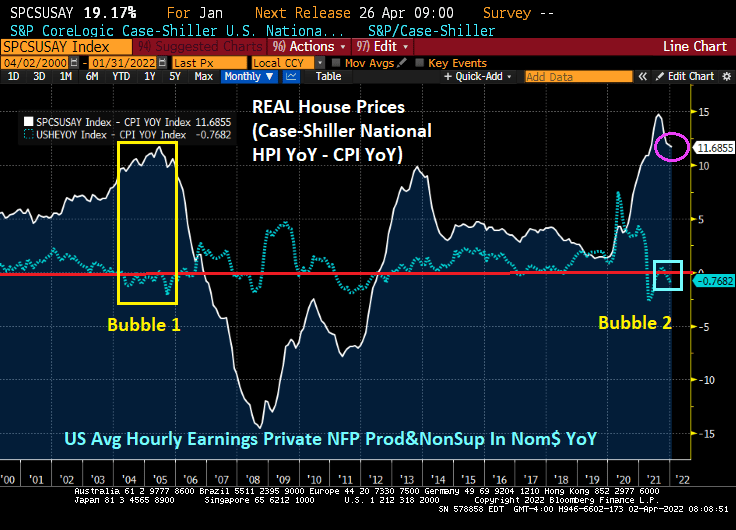

REAL average hourly earnings are now a terrible -2.99% YoY thanks to the worst inflation in 40 years. REAL home prices are growing at 11.8% YoY.

Traders are betting that even with the Fed boosting its target for the federal funds rate by 2.5 percentage points this year to 3% won’t be enough to get the inflation rate back down to 2% over the next decade from around 8.5% currently.

In nominal terms, mortgage rates are seemingly trying to rise to 2007 levels (6.5%). But the gap between the 30-year mortgage rate and Fed Funds target rates is back to 2009 levels.

Talk about Fed and Fed government OVER stimulypto! Even REAL US home prices grew at 12% YoY pace while the REAL Fed Funds Target rate is -8.04%.

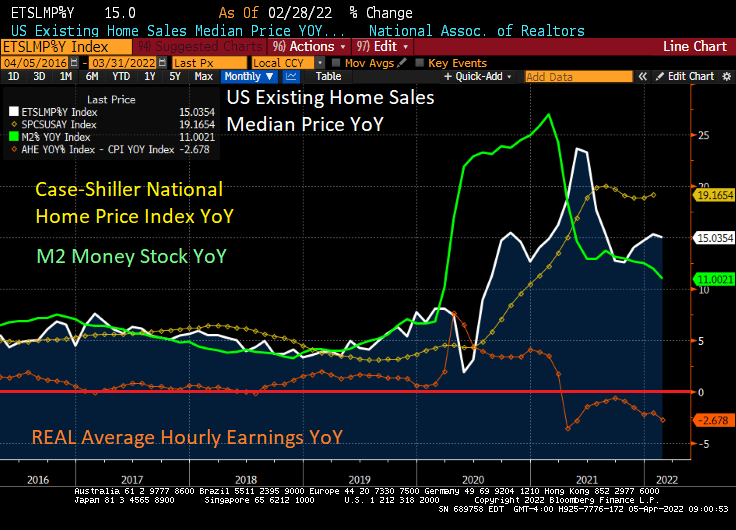

CoreLogic’s Home Price Insights revealed that home prices rose 20% YoY in February despite REAL average hourly earnings declining -2.678% YoY. THAT is euphoria! Or Stimulypto, as I like to call it.

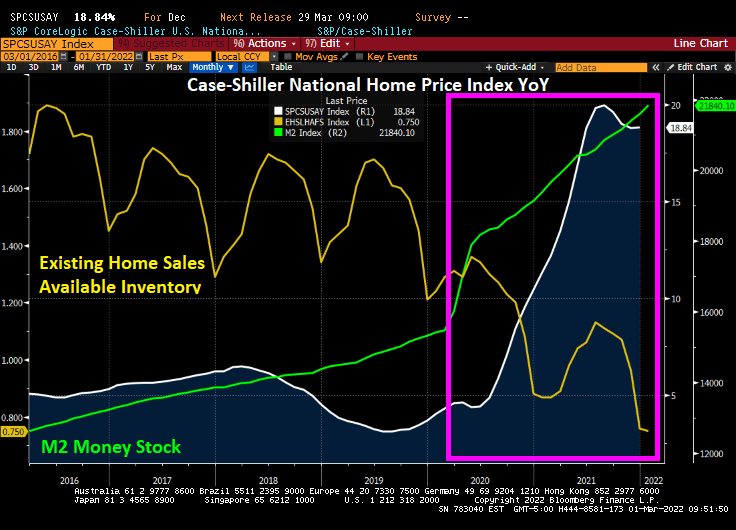

No, The Federal Reserve still hasn’t removed its staggering monetary stimulus. Notice that M2 Money Stock is still growing at a torrid 11% pace.

20% YoY home price growth in February? CoreLogic has increased their forecast of home price growth to 5%, likely because The Federal Reserve is imitating a sloth in removing its monetary Stimulypto.

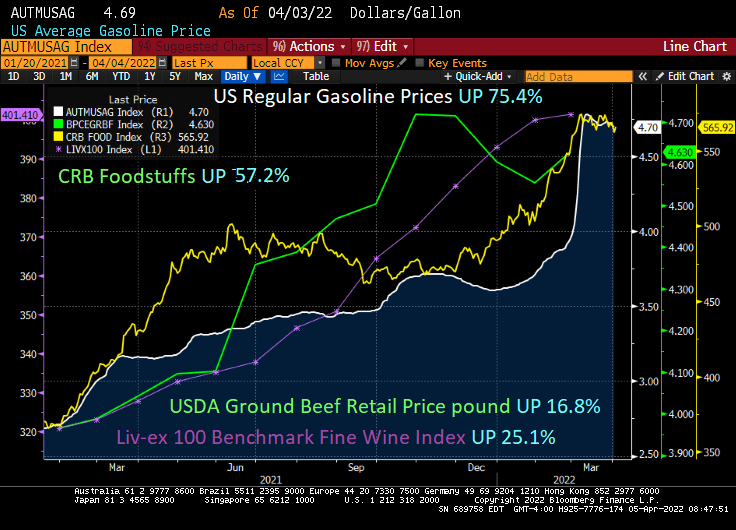

Of course, there are other assets growing at lightning speeds. US Regular gasoline prices are UP 75.4% under Biden. Foodstuffs are UP 57.2% since Biden was installed as President. At least ground beef is only up 16.8% while the fine wine index is up 25.1%.

Speaking of wine,Hitching Post II in Buellton, CA must be suffering from rising food and grape costs too (I highly recommend eating there and using their HP Magic Stuff at home). Not to mention their spectacular wines. Roast artichokes anyone??

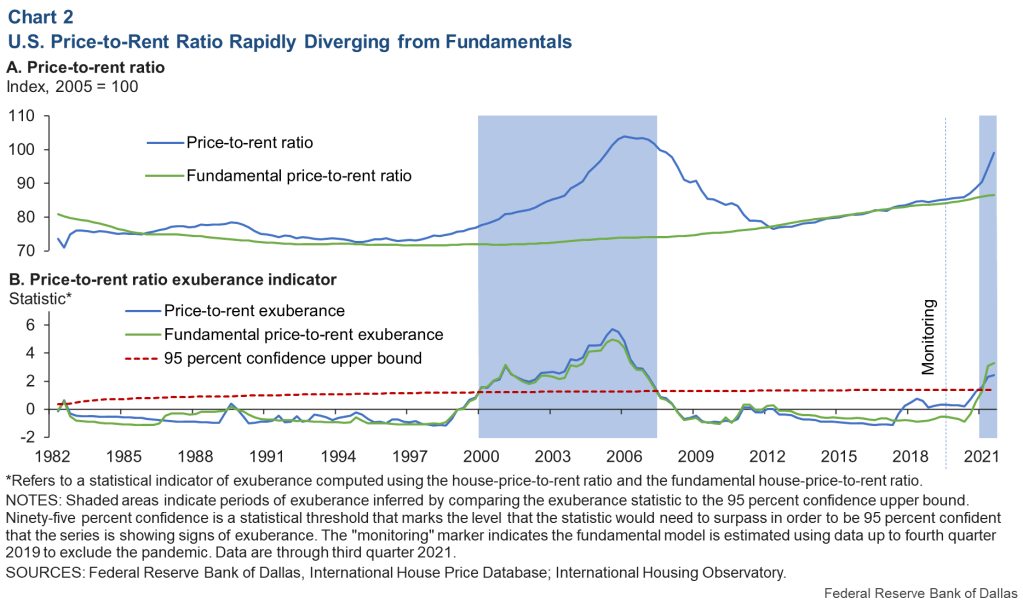

The Dallas Federal Reserve issued a warning recently that a housing bubble is brewing … after the economy drank its magic monetary elixir. We can see the housing bubble clearly (defined as the spread between REAL home price growth and REAL average hourly earnings). Notice that the current housing bubble looks similar to the infamous 2005 housing bubble. And the US is seeing several months of the spread between REAL home price growth and REAL hourly earnings be even higher than the peak of the 2005 bubble.

The Federal Reserve is starting to slow down its asset purchases, so we should see a cooling of the housing bubble. Unless, of course, The Fed changes its tune from quantitative tightening (QT) back to quantitative easing (QE) … again.

The Dallas Fed has a measure of housing “exuberance” which shows a bubble forming, but not there yet. I like the spread between real house price growth and real hourly earnings better.

The Dallas Fed also has a price-to-rent chart also showing growing exuberance.

But if we look at the Case-Shiller National HPI YoY to US CPI Urban Consumers Owners Equivalent Rent of Residences YoY we see that the US is currently experiencing a price-to-rent ratio higher than the peak of the 2005 house price bubble. What is the culprit? The vast expansion of monetary and fiscal Stimuylpto surrounding the Covid outbreak in early 2020.

So, the Dallas Fed thinks that is a house price bubble is brewing, but it has actually been in the works since QE3 in 2013 (bubble 2), but really took off with The Fed’s stimulypto and Federal COVID spending surrounding the COVID outbreak in early 2020.

The mayhem caused by the Russian invasion of Ukraine is helping drive down interest rates … for the time being … and this is helping push down mortgage rates and increase mortgage applications.

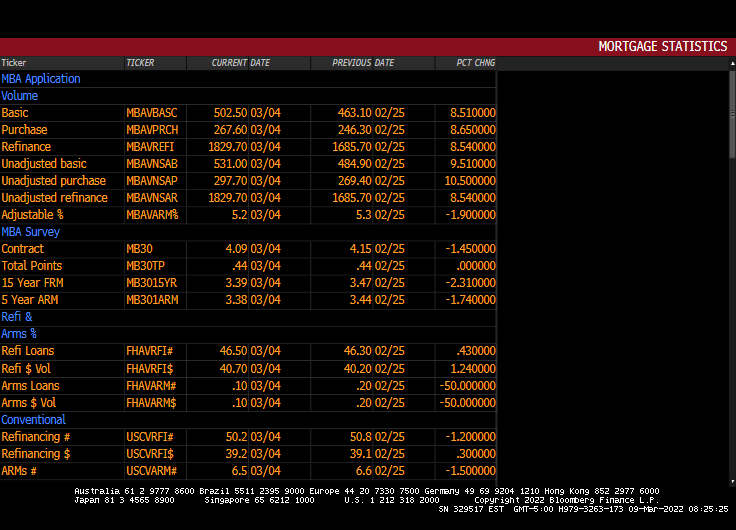

Mortgage applications increased 8.5 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending March 4, 2022.

The seasonally adjusted Purchase Index increased 9 percent from one week earlier. The unadjusted Purchase Index increased 11 percent compared with the previous week and was 7 percent lower than the same week one year ago.

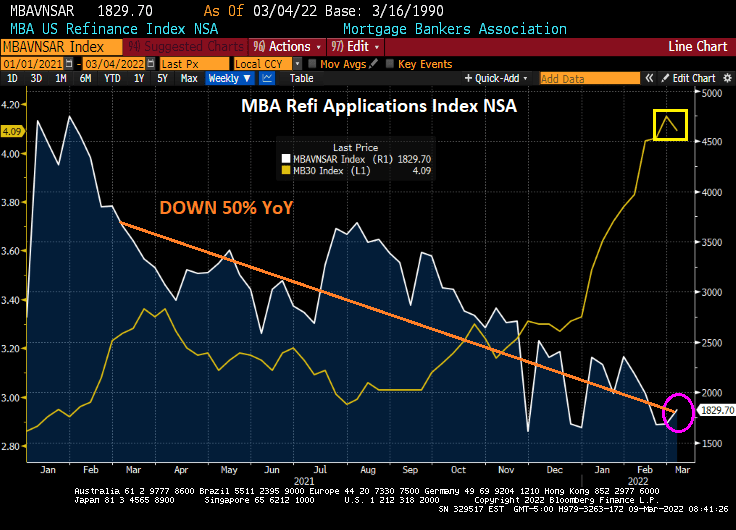

The Refinance Index increased 9 percent from the previous week and was 50 percent lower than the same week one year ago. Diane Olick at CNBC has the hilarious headline “Brief drop in mortgage rates sparks mini refinance boom.” The slight rise in refi applications from the previous week is more of a firecracker going off than a boom given that refi apps are still down 50% from the same week last year.

Bear in mind that the US Treasury 10-year yield is up since the MBA’s reporting week ended on March 4, 2022. So, look for Olick’s mini-refi boom to end as quickly as it started.

Here is the rest of the MBA story.

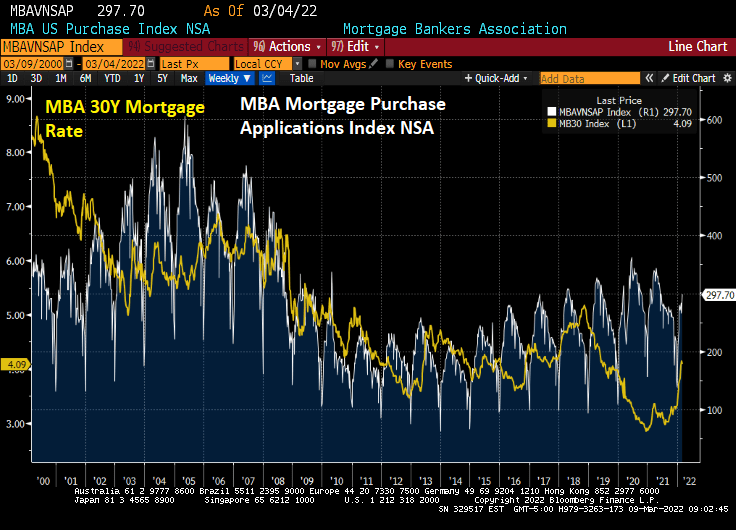

The MBA Mortgage Purchase applications index typically peaks in mid-to-late April, so we still have another month (seasonality) until purchase applications begin declining again.

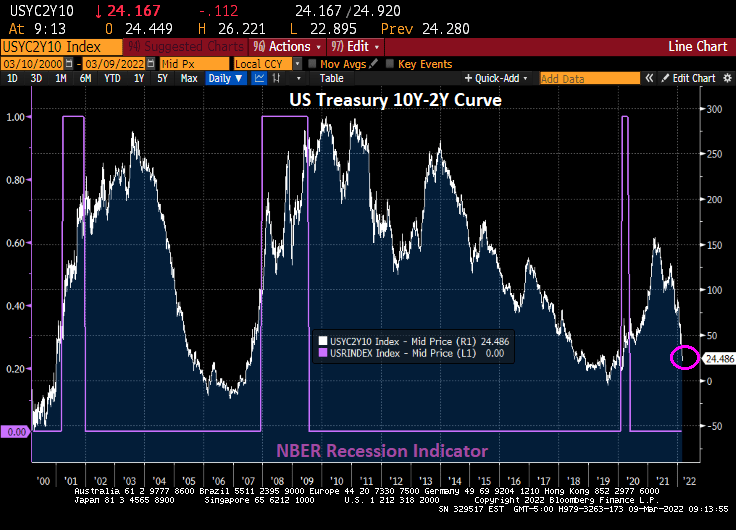

The US Treasury 10Y-2Y curve continues to flatten and is the worst curve recovery in modern history.

The general rise in US mortgage rates is more closely tied to expectations of Fed rate increases than Fed Agency MBS holdings.

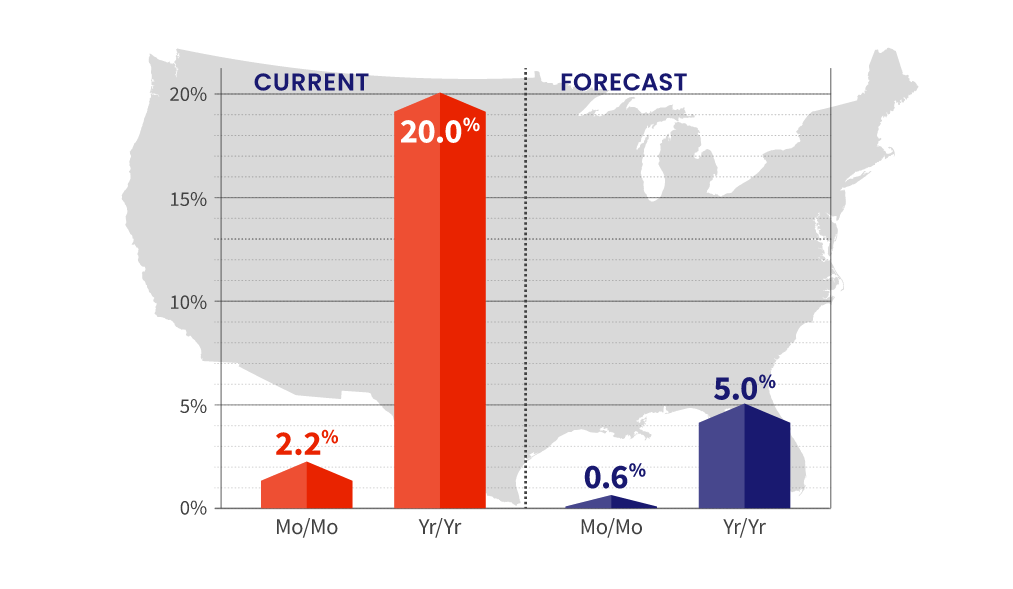

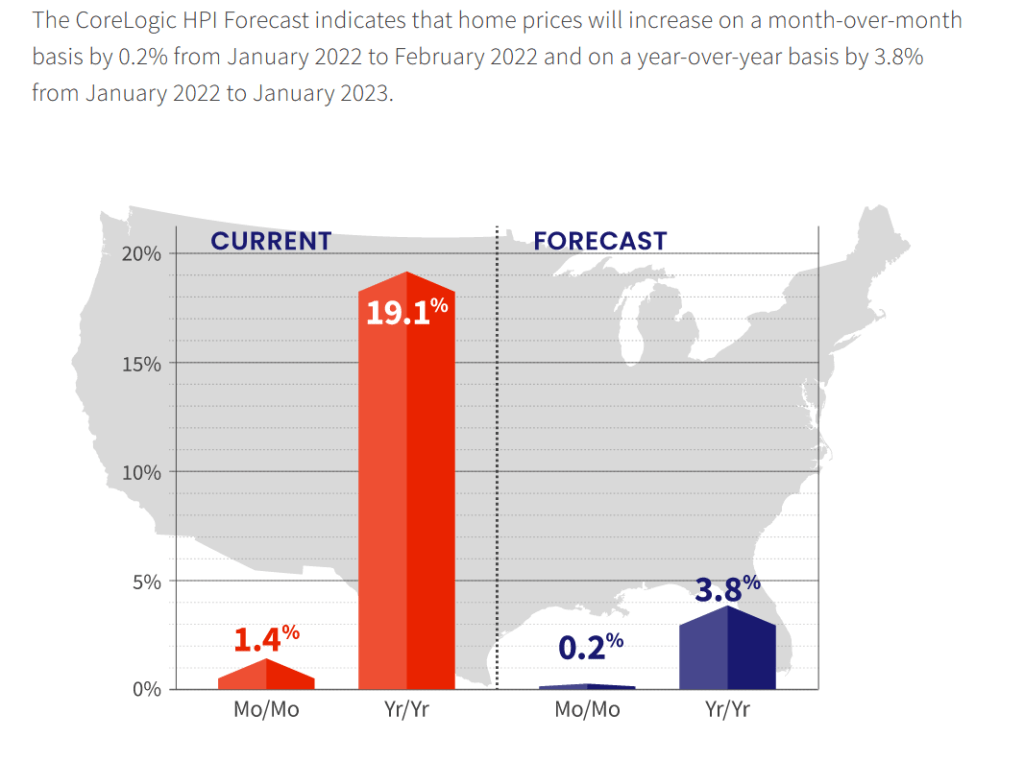

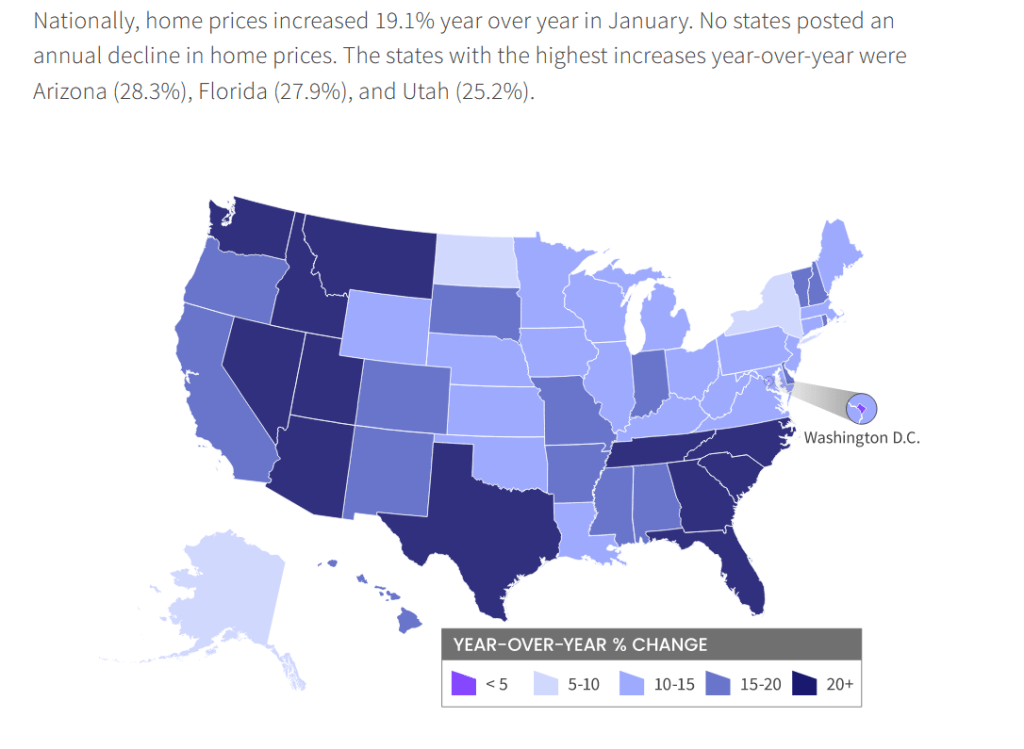

Home prices nationwide, including distressed sales, increased year over year by 19.1% in January 2022 compared with January 2021. On a month-over-month basis, home prices increased by 1.4% in January 2022 compared with December 2021 (revisions with public records data are standard, and to ensure accuracy, CoreLogic incorporates the newly released public data to provide updated results).

But Corelogic is still forecasting only 3.8% YoY growth in 2022.

Home prices are hot, hot, hot in all states except North Dakota and New York. The fastest growing states are lower taxes, higher growth states.

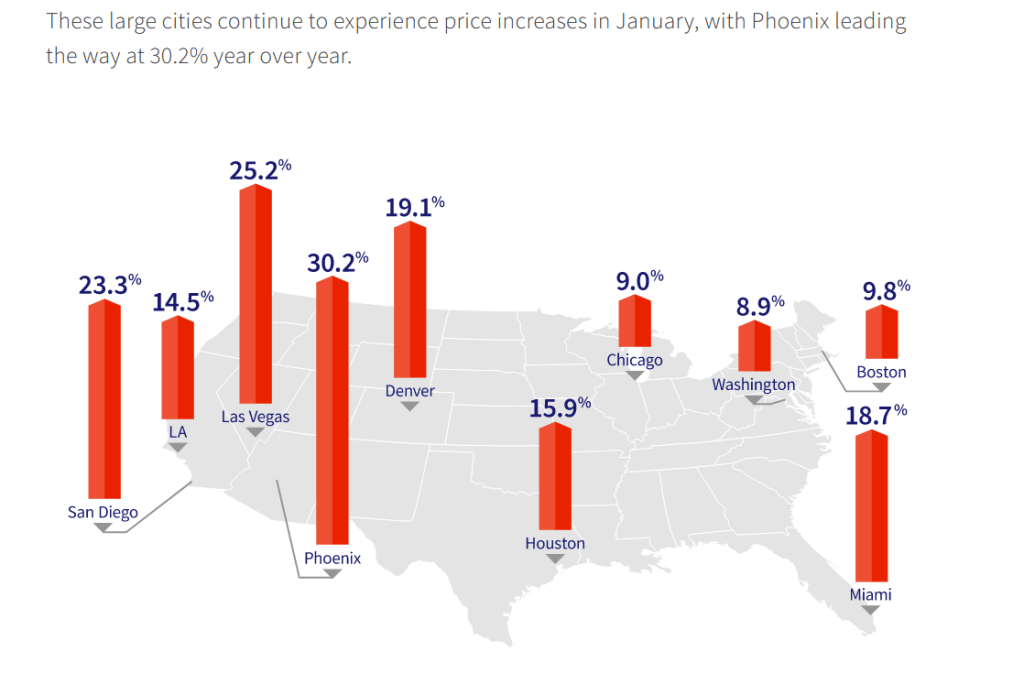

Phoenix, Las Vegas and San Diego are booming. But Chicago and Washington DC are growing at near 9% YoY.

Case-Shiller’s December report show home prices growing at 18.84% YoY thanks to Fed stimulypto and historic low inventory of homes available for sale.

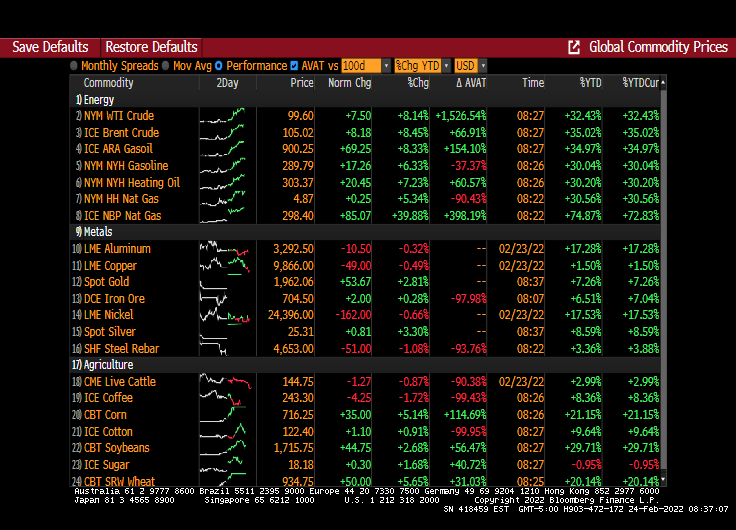

I admit, I follow market data to get a signal of what is happening to mortgage rates and I got one. With Putin and Russia invading Ukraine, markets are in turmoil

WTI Crude is up 8.14% this morning, Brent Crude is up 8.45% and NBP (UK) Natural gas is up 40%.

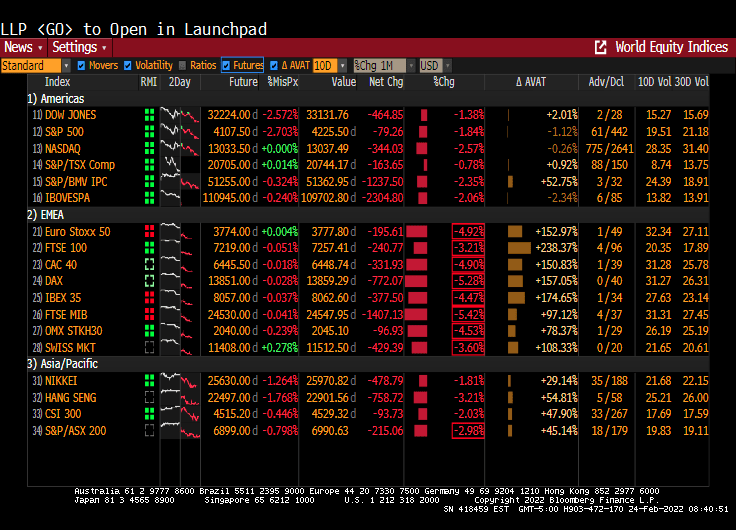

Europe is having a bad day equity market-wise. Eurostoxx 50 was down 4.92%. The US Dow is braced for a 2.5% opening.

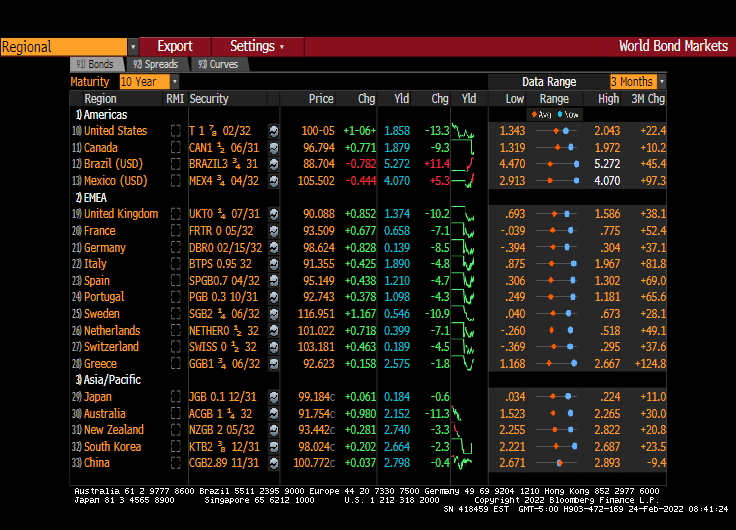

Now to bonds. The 10-year Treasury yield is down 13.3 bps this morning. Sweden and UK are down 10 bps as well.

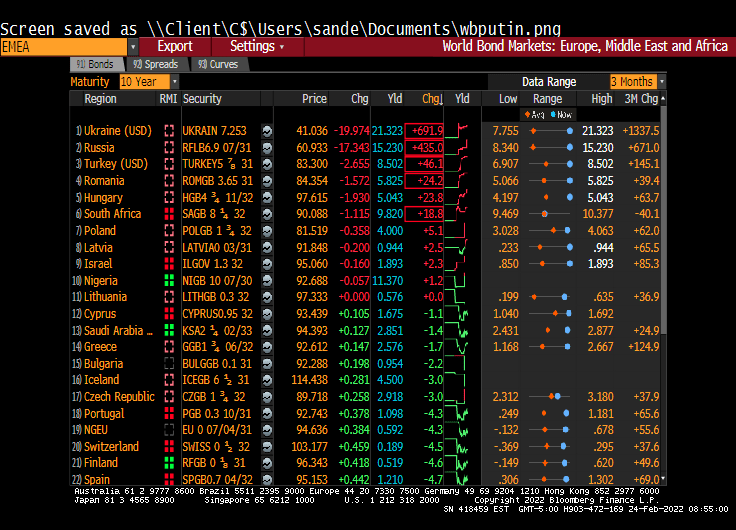

How about the new Russian front? Ukraine’s 10y yield rose 691.0 bps while Russia’s 10Y yield rose 435 bps.

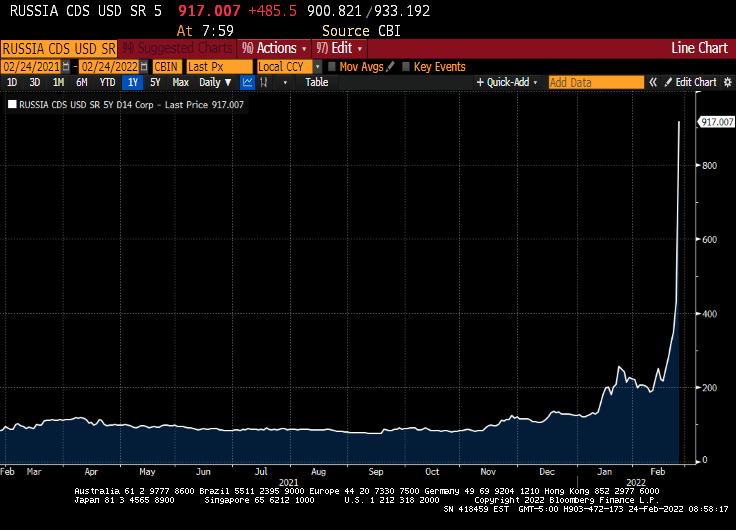

Russian 5Y Credit Default Swaps (CDS) leaped to a Greek-like 917.

Well, it looks like the sanctions imposed by Winken (US VP Harris), Blinken (US Secretary of State) and Nod (US President Biden because he always looks half-asleep) apparently didn’t work as intended.

You must be logged in to post a comment.