Only in today’s Kafkaesque (having a nightmarishly complex, bizarre, or illogical quality) Federal government would Biden, Schumer and Pelosi cheer about passing a bill hilariously called “The Inflation Reduction Act” that not only will NOT reduce inflation, but also raises taxes on most Americans.

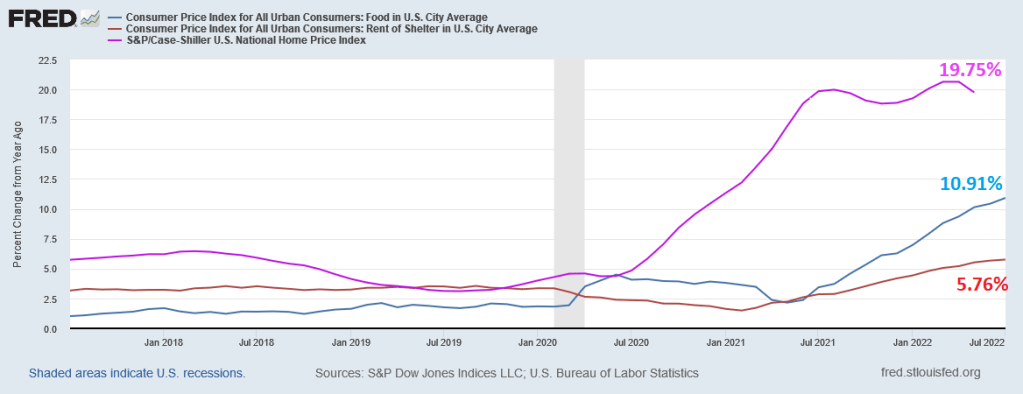

In terms of the inflation tax on the middle class and low-wage workers, we see that FOOD inflation was 10.91% YoY in July and the BLS’s low-ball estimate of “rent” at 5.76% YoY. Odd, since home price growth is 19.75% YoY.

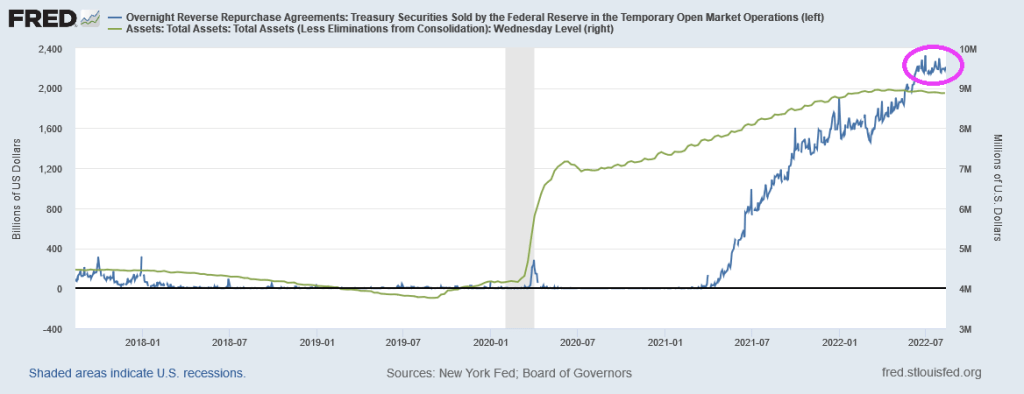

The Fed’s monstrous balance sheet is still near $9 TRILLION (over stimulus) and The Fed’s Overnight Repo Facility remains near $2 TRILLION.

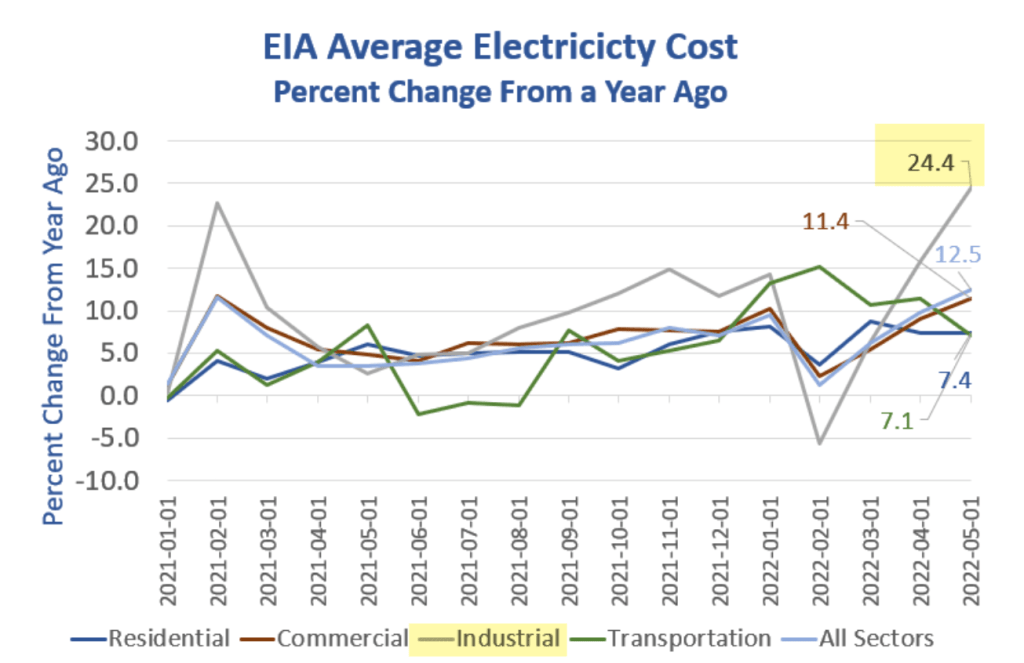

Industrial electricity costs (to be passed on to consumers in the form of higher prices) is up 24.4% YoY. Residential electricity cost is up “only” 7.4% YoY. (Source: Mish GEA)

Somehow I doubt if Biden, Harris and Jean-Pierre (Biden’s Press Secretary) will go on the talk show circuit talking about the Producer Price Index Final Demand at 9.8% YoY, meaning that inflation is still raging.

But the curious thing about the PPI Final Demand numbers. While lower than June’s reading of 11.3% YoY, it also coincides with declining gasoline prices and declining growth in M2 Money stock. Which is still growing at 5.9% YoY. The probability of recession is rising (even though technically the US is in recession after 2 consecutive quarters of negative GDP growth.

Here is the more striking chart.

So is the US “improving” on prices because of brilliant Biden strategies (I just laughed at my own “bon mot”)? Or are prices (PPI, gasoline) slowing because of declining demand as the US slips into recession?

Lawrence Summers was once again in the news saying that the way to cool inflation is to raises taxes (and cool demand). Only a true Statist would say something like that. Larry, how about Biden and Congress stop spending so much money that is helping to fuel inflation?

One Washington DC types would rest their hopes on cooling inflation by having the US slip into recession AND raises taxes.

Fannie Mae’s Home Purchase Sentiment index has declined from 81.7 shortly after Biden was sworn-in as President to a meager 62.8 in July 2022.

Of course, mortgage rates have risen quite rapidly and home price growth remains elevated as The Fed still has not trimmed its balance sheet as promised.

While President Biden is technically correct (CPI didn’t increase from June to July), he left out that headline inflation was still painful at 8.5% YoY and core inflation was 5.9% YoY. He also left out that CORE inflation rose 0.3% in July. And he left out that REAL earnings growth was still negative.

The midterm elections are approaching fast and, of course, Biden and his crew have to put the best face of his and the Democrats accomplishments. But seriously Joe, REAL weekly earnings growth is negative meaning that inflation is crushing wage growth. Meanwhile, CPI rent is skyrocketing and was 5.8% YoY in July.

As we know, the CPI measure of rent is terrible and does not reflect the actual rise in rents. Zillow’s Rent index YoY is slowing, but remains at 14.75% YoY, far higher than the CPI rent measure of 5.8%.

So, the Federal Government and Federal Reserve keeps pumping trillions into the economy, so it is not surprising that we have rampant inflation crushing renters.

The US July inflation report remains hot, hot, hot! While mortgage purchase and refinancing applications are not, not, not.

The US consumer price index rose 8.5% in July. And real average weekly growth remains burned by horrid inflation, at -3.6% YoY.

Source of inflation?

Headline inflation above estimates in 14 of last 16 months.

Data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending August 5, 2022 revealed that … the Refinance Index increased 4 percent from the previous week and was 82 percent lower than the same week one year ago. The seasonally adjusted Purchase Index decreased 1 percent from one week earlier. The unadjusted Purchase Index decreased 2 percent compared with the previous week and was 19 percent lower than the same week one year ago.

The 10Y-2Y yield curve hit the worst inversion since 2000 as the curve slope hit -47.7 basis points, inverting another -2.267 basis points today.

Yes, the 10Y-2Y Treasury yield curve is SCREAMING RECESSION.

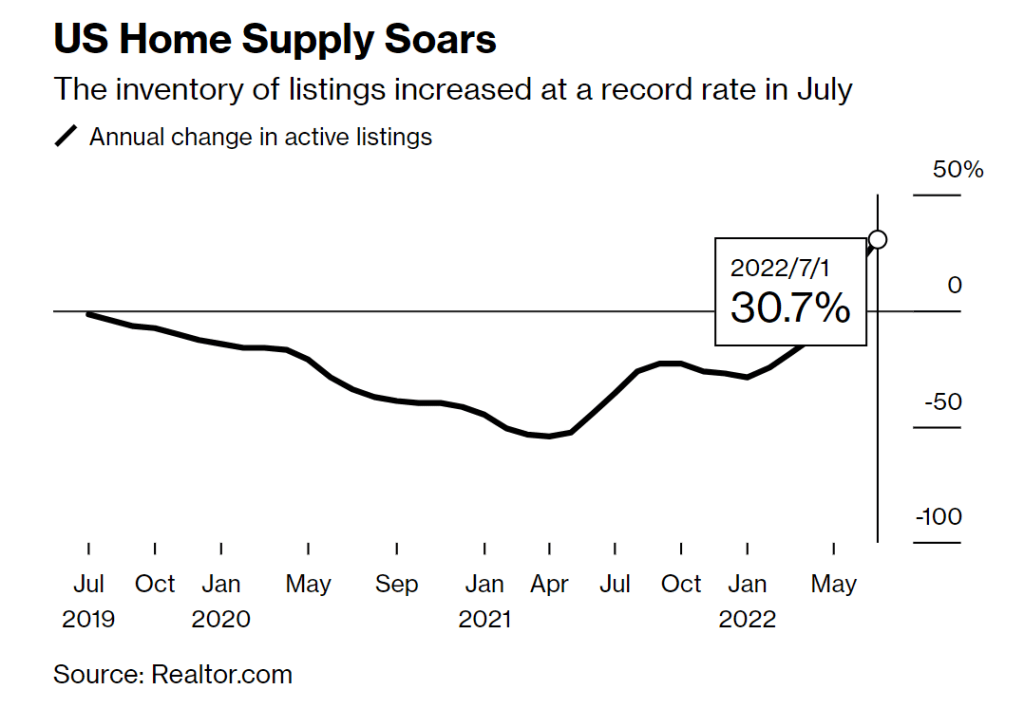

(Bloomberg) – Prashant Gopal – The supply of homes for sale across the US grew at a record rate last month, another sign that higher mortgage costs are cooling down the housing market.

The number of active listings nationwide jumped 31% from a year earlier, a record-high increase for a third straight month, according to a report Tuesday by Realtor.com.

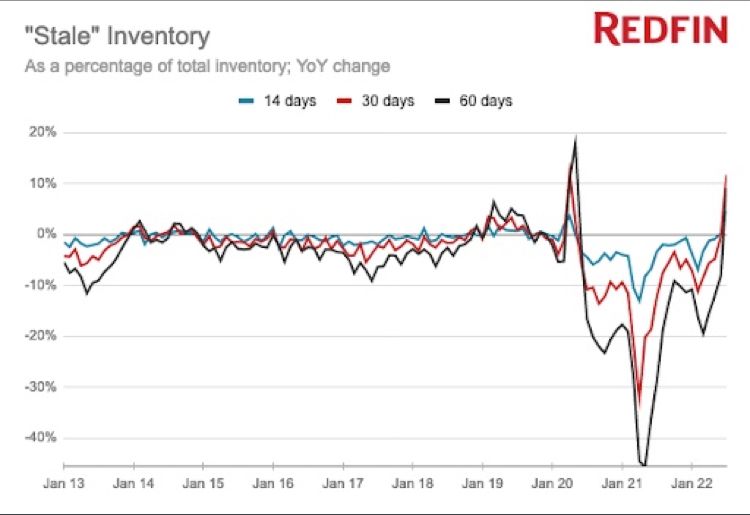

And according to Redfin, stale inventory is accelerating.

The US housing market is simply unaffordable for millions of Americans. To illustrate the problem, here is a chart of the Case-Shiller National home price index less CPI YoY graphed against Average Hourly Wages less CPI YoY.

The gap between the REAL national home price index YoY and REAL US average hourly earnings YoY is near the largest since 1988. Inflation is making matters far worse since REAL average hourly earnings growth continues to decline.

The only thing positive to say is that REAL home price growth YoY is lower now than at the peak of the 2005 home price bubble that burst catastrophically.

Another “positive” is that the REAL 30-year mortgage rate has fallen to -3.23%. At the peak of the house price bubble in June 2005, the REAL 30-year mortgage rate was +2.58%. THAT is one big difference between the pre-2008 recession and today’s impending recession.

The media is thrilled with today’s jobs report showing a sizzling 528k jobs added to the US economy. And with that, the media is cheering that recession fears are shrinking.

But hold on a second.

First, while 528k jobs were added in July (great news!), REAL average hourly earnings growth YoY fell to -3.8173. Why? Because the rate of inflation is greater than nominal average hourly earnings YoY of 5.2%. That is BAD.

This charts shows that inflation-adjusted (or real) wage growth is the worst in recorded history.

And the “sizzling” jobs report isn’t feeling any love in the bond market where the US Treasury yield curve (10Y-2Y) deepened its inversion to -37.593 basis points, a drop of -1.331 BPS. Note that the 10Y-2Y curve falls below 0% just prior to every recession.

Labor force participation actually fell to 62.1% from 62.2% in June.

I am assuming that The Fed will misread the jobs report and argue for LESS COWBELL.

The US economy may need to undergo a deeper and longer recession than investors currently anticipate before inflation can be brought under control, according to Zoltan Pozsar of Credit Suisse Group AG.

Markets expect the surge in consumer prices will soon peak and central banks will become less hawkish, but there’s a high risk that global cost pressures will remain elevated, Pozsar, global head of short-term interest-rate strategy at Credit Suisse in New York, wrote in a client note.

The world is being wracked by an economic war that’s undermining the deflationary relationships that have prevailed in recent decades where Russia and China supplied cheap goods and services to more developed nations such as the US and those in Europe, he said.

“War is inflationary,” Pozsar wrote. “Think of the economic war as a fight between the consumer-driven West, where the level of demand has been maximized, and the production-driven East, where the level of supply has been maximized to serve the needs of the West.” That pattern held “until East-West relations soured, and supply snapped back,” he said.

The result is that inflation is now a structural problem, rather than a cyclical one. Supply disruptions have arisen from the changes in Russia and China, along with tighter labor markets due to immigration restrictions and a reduction in mobility caused by the coronavirus pandemic, Pozsar said.

There’s now a risk the Federal Reserve under Chair Jerome Powell has to raise interest rates to 5% or 6% and keep them there to create a substantial and sustained reduction of aggregate demand to match the tighter supply profile, he said.

‘More Misguided’

Connect the dots on the biggest economic issues.Connect the dots on the biggest economic issues.Connect the dots on the biggest economic issues.

Dive into the risks driving markets, spending and saving with The Everything Risk by Ed Harrison.Dive into the risks driving markets, spending and saving with The Everything Risk by Ed Harrison.Dive into the risks driving markets, spending and saving with The Everything Risk by Ed Harrison.

Sign up to this newsletter

Pozsar’s warning that inflation will stay elevated puts him at odds with the Treasury market, which rallied last month as investors switched their focus to recession risks from inflation concern. While an economic slowdown typically weighs on consumer prices, the latest annual US inflation reading of 9.1% for June remains far above the Fed’s 2% goal, although the price surge is forecast to slow for the first time in three months to 8.8% in July according to a Bloomberg poll of economists.

The bond market is more misguided now than at any other time this year as traders wager the US central bank will start cutting rates in early 2023, Bloomberg Economics’ chief US economist Anna Wong and her colleagues said this week. Money markets are wagering on almost one percentage point of hikes by year-end followed by a quarter-point cut by June.

“Interest rates may be kept high for a while to ensure that rate cuts won’t cause an economic rebound (an ‘L’ and not a ‘V’), which might trigger a renewed bout of inflation,” Pozsar wrote in his note. “The risks are such that Powell will try his very best to curb inflation, even at the cost of a ‘depression’ and not getting reappointed.”

Speaking of “recession,” the US Treasury 10Y-2Y yield curve has inverted even further to -31.69 BPS.

We are seeing a slowing of the US economy. For example, the JOLTs (job openings) numbers are out for June and they are down -5.5% from May. And from April to May, JOLTs declined -3.2% MoM. That is a clear slowing trend.

And on the housing front, the CoreLogic HPI Forecast indicates that home prices will increase on a month-over-month basis by 0.6% from June 2022 to July 2022 and on a year-over-year basis by 4.3% from June 2022 to June 2023. But rose +18.3% YoY in June. Also a clear cooling trend.

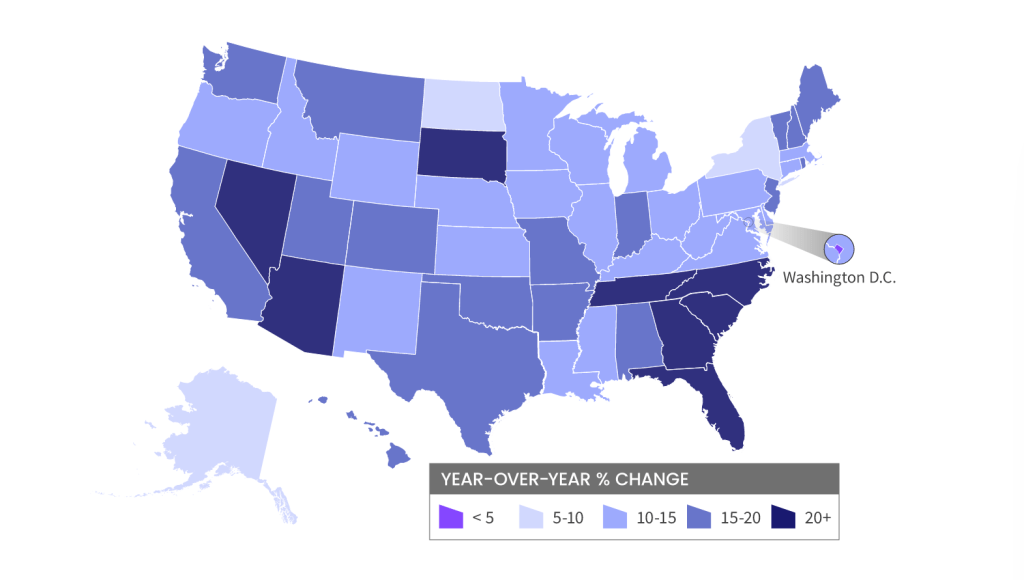

And its “Escape From Blue States” (perhaps a new Kurt Russell movie), with home prices rising fastest in red states (primarily The South). And contiguous migration from California to Nevada and Arizona.

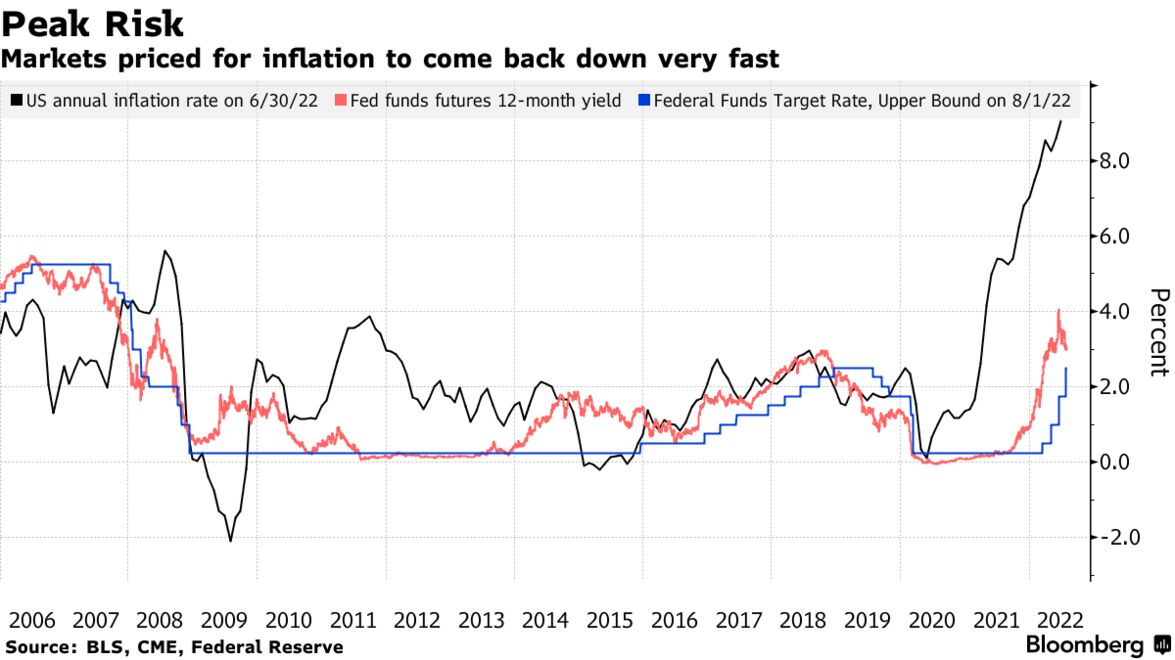

The Fed Funds Futures market is pricing in rate hikes until the March 2023 FOMC meetings. After all, Prince Imhotep (aka, Minneapolis Fed’s Neel Kashkari) is screaming for more rate hikes to fight inflation … caused by 1) loose monetary policies since late 2008 and 2) insane Federal government spending.

Let’s see if “Mr. Freeze” (aka, Jerome Powell) relents on Fed rate increases before the March 2023 FOMC meeting.

You must be logged in to post a comment.