I used to think that The Kabuki Theater surrounding the raising of the US debt limit and passing a Federal budget would be over by now. But since Biden is being controlled by the hard left “Progressives” in Washington DC, he may be reckless enough to let the US default just so he can blame Republicans. And with our useless and deeply-biased main street media (MSM) just repeating Democrat talking points blaming Republicans, we may actually see a US debt default.

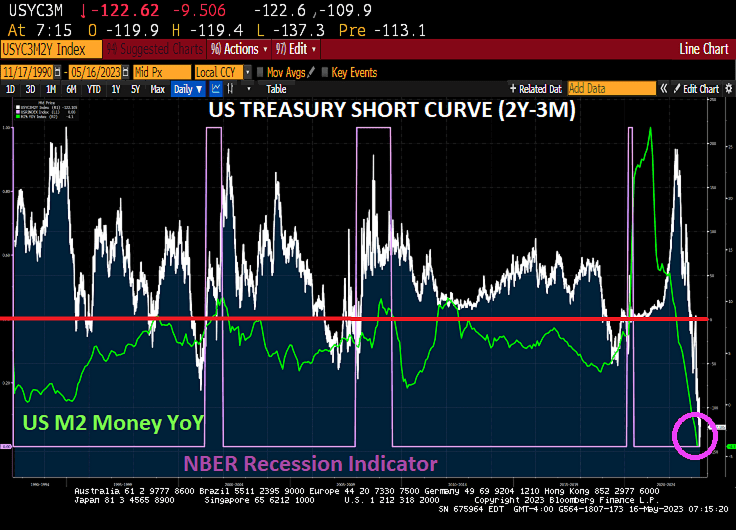

So while Yellen is warning that time is running out, notice she never encourage Blaming Biden to negotiate his insane budget downwards, we see a deeply inverted US Treasury short curve (2Y-3M).

(Bloomberg) Treasury Secretary Janet Yellen warned that “time is running out” to avert an economic catastrophe from failing to raise the debt ceiling, in remarks released as President Joe Biden and congressional leaders prepared to meet on the standoff.

Speaker Kevin McCarthy issued his own notice Monday evening ahead of Tuesday’s 3 p.m. gathering, saying, “We only have so many days left to deal with this.”

The two sides showed little signs of agreeing on much else other than the countdown in the runup to the second White House encounter on the debt ceiling in two weeks. While senior staff have been negotiating for days, Republicans are still pressing for sweeping spending cuts, while Democrats are determined to protect the president’s legislative achievements.

“We are already seeing the impacts of brinksmanship: investors have become more reluctant to hold government debt that matures in early June,” Yellen said in remarks prepared for delivery to a banking conference on Tuesday. “The impasse has already increased the debt burden to American taxpayers.”

The Treasury chief issued a fresh letter to congressional leaders Monday restating that the Treasury risks running out of sufficient cash for all federal obligations as soon as June 1. The livelihoods of millions of Americans “hang in the balance,” she said in excerpts of her speech to the Independent Community Bankers of America Capital Summit released by the Treasury.

There is the evil Hobbit! Sending a letter to Congress essentially blaming McCarthy for the fiasco when Biden could downsize his budget request to reasonable levels. But Yellen is an authoritarian Statist, not a free market type.

You must be logged in to post a comment.