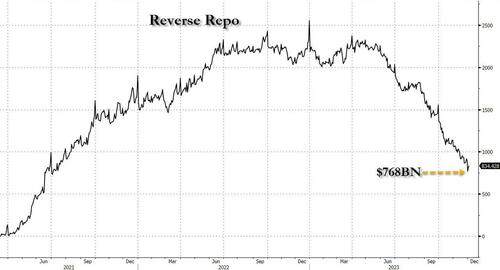

We didn’t have long to wait because just a few days later, on December 1 (just after the customary month-end window dressing period) when reverse repo tumbled to a fresh multi-year low of $765 billion…

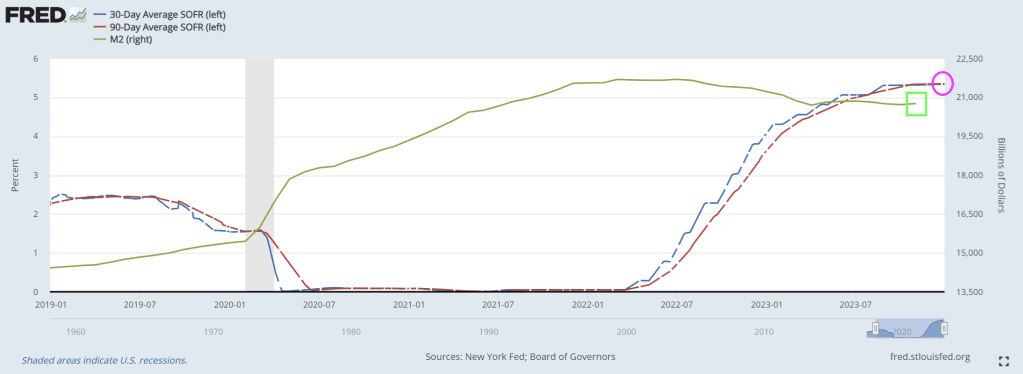

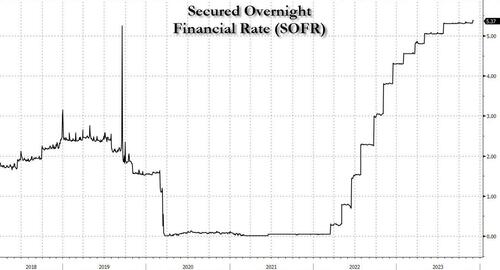

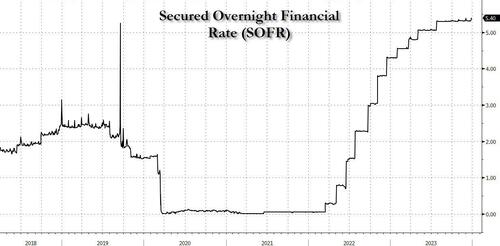

… things indeed broke as we explained in “Sudden Spike In SOFR Hints At Mounting Reserve Shortage, Early Restart Of QE” (in which we correctly previewed the coming Fed pivot at a time when most were still dead certain that Powell would only care about inflation for months to come): that’s when the the all-important SOFR rate (i.e., the new Libor) unexpectedly jumped 6bps to 5.39%, the highest on record…

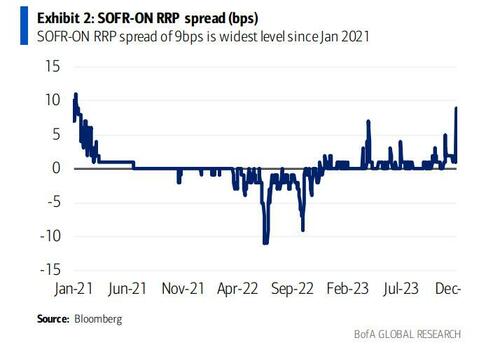

… also resulting in the largest SOFR spike vs ON RRP since Jan ’21, which hit 6bps.

The spike caught almost everyone by surprise, even such Fed-watching luminaries as BofA’s Marc Cabana because it was with “no new UST settlements, lower repo volumes, and lower sponsored bi-lateral volumes.” More ominously, and confirming our take from three weeks ago, Cabana warned at the time (full note here) that “the move is consistent with the slow theme of less cash & more collateral in the system” – i.e., growing reserve scarcity – and “may have been exacerbated by elevated dealer inventories, bi-lateral borrowing need, and limited excess cash to backstop repo. If funding pressure persists, it risks Fed re-assessment of ample banking system reserves & potential early end to QT.”

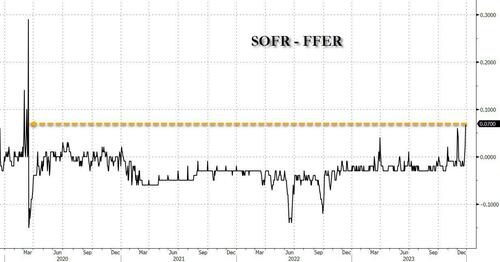

Then, the mini liquidity crisis disappeared almost as fast as it emerged, as SOFR rates eased off and the SOFR-Fed Funds spread normalized once GSE cash entered the market as it does every month….

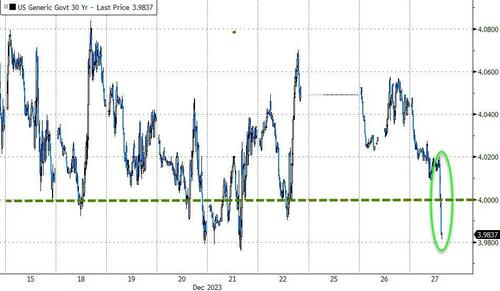

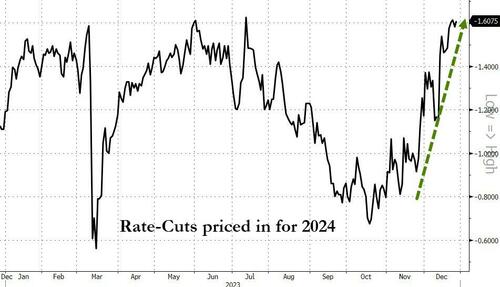

… until today when not only did SOFR hit a new record high, ironically at a time when the market is pricing in more than 6 rate cuts in 2024…

… but the spread between the SOFR and the effective Fed Funds rate just spiked to the highest level since the March 2020 repo crisis…

.. with a similar move also observed in the spread between SOFR rate and the O/N Reverse Repo which similarly blew out to the widest since the start of 2021.

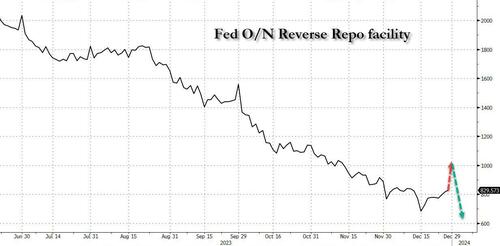

While there was no specific catalyst behind the sudden spike, two factors are the likely culprits: the year-end liquidity crunch, and the recent sharp increase in the Fed’s reverse repo facility, which has increased from a multi-year low of $683 billion on Dec 15 to yesterday’s $830 billion, and which STIR strategists expect will shoot up above $1 trillion in today’s final for 2023 reverse repo operation as a whopping $300+ billion in short-term liquidity in pulled from markets in just days.

That’s the bad news.

The good news is that come 2024 in a few hours, and specifically the first day of trading on Jan 2, we expect the reverse repo facility to plummet back to $700 billion once the year-end window dressing is over (especially with total US debt rising above $34 trillion to start the year), and floods the system with fresh liquidity which will stabilize the monetary plumbing at least until reverse repo dips below that key level of $700 billion at which point we expect the SOFR spikes to become a daily occurrence, and one which the Fed will no longer be able to ignore.

Indeed, one can already see traces of this in the repo market, where the rate on overnight GC repo first surged to 5.625% at the open on the final trading day of December before dropping to 5.45%, according to ICAP. It has since climbed back to 5.50%. But that’s still lower than where repo rates for Dec. 29 were trading during the prior session, as markets now start frontrunning the coming reverse repo liquidity flood.

Of course, once reverse repo eventually tumbles to $0 some time in March, all bets are off and the narrative shift to the next QE will begin.

“Say, can I sniff you if you take Trump off of Maine’s Presidential ballot??”

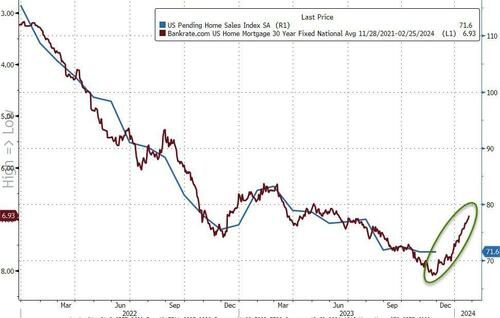

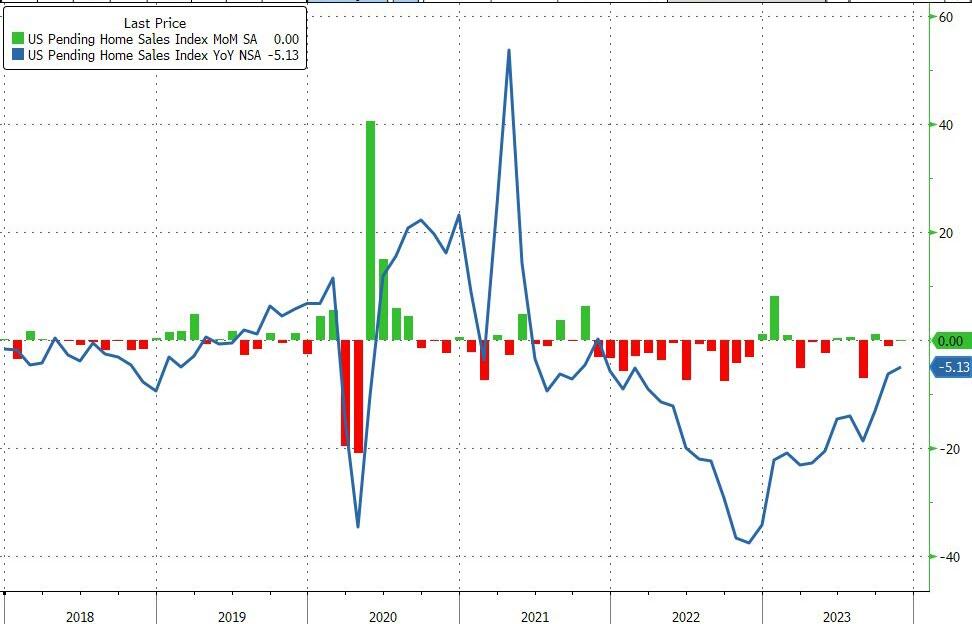

Alarm! With rampant inflation, The Federal Reserve has raised rates to tame inflation. And with the rate increases, US pending home sales have fallen -5% since last year.

That left Pending Home Sales Index still down over 5% YoY…

Source: Bloomberg

That leaves the Pending Home Sales Index at a new record low…

Source: Bloomberg

The index of contract signings for existing homes declined in the South, the biggest US housing market, to the lowest level on record.

Pending sales climbed in the other three regions.

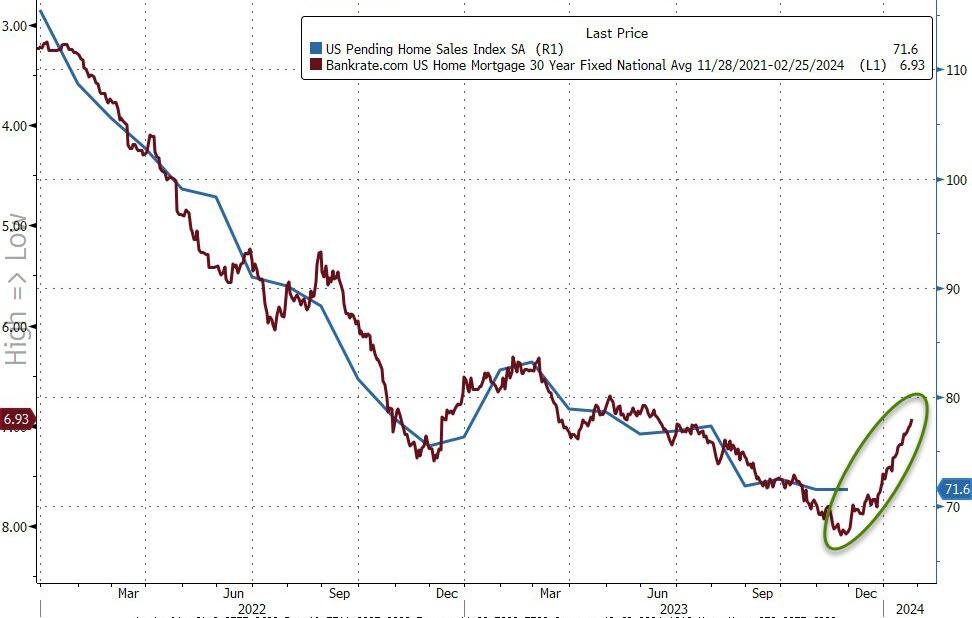

The trend in pending home sales appears to tracking mortgage rates (with about a one-month lag), suggesting things may be about to pick up more solidly in the next few months…

Source: Bloomberg

“Although declining mortgage rates did not induce more homebuyers to submit formal contracts in November, it has sparked a surge in interest, as evidenced by a higher number of lockbox openings,” Lawrence Yun, NAR’s chief economist, said in a statement.

“With mortgage rates falling further in December – leading to savings of around $300 per month from the recent cyclical peak in rates – home sales will improve in 2024,” Yun said.

Optimism – from a realtor – whoever would have thought!?

C’mon Joe. The media has always reported bad news. Warm and fuzzy doesn’t anger people, but bad news does! And under Bidenomics, there has been a lot of bad news.

President Biden railed against corporate media before he and several family members headed by helicopter to Camp David, the presidential retreat in the mountains of western Maryland.

Before boarding the presidential helicopter, Biden was asked by one reporter: “What’s your outlook on the economy next year?”

The president responded: “All good,” adding, “Take a look. Start reporting it the right way.”

Sounds like Biden watched the Travola/Jackson flick “Basic” where the infamous line was uttered “Tell the story right.”

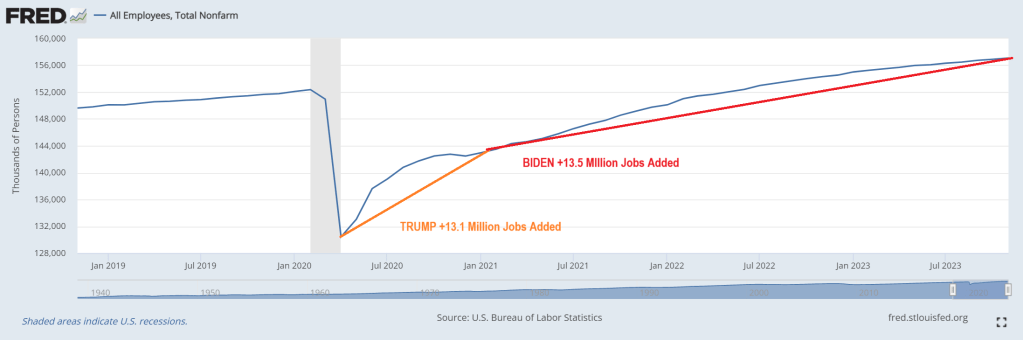

OK Joey, let’s tell the story right. After the horrendous economic shutdowns of local economics and schools in 2020, 15.1 million jobs were added after the shutdowns ended in just 10 months. Wow, that was simple! But under Biden’s Reign of Economic Error, only 15.5 million jobs were added over the next 34 months.

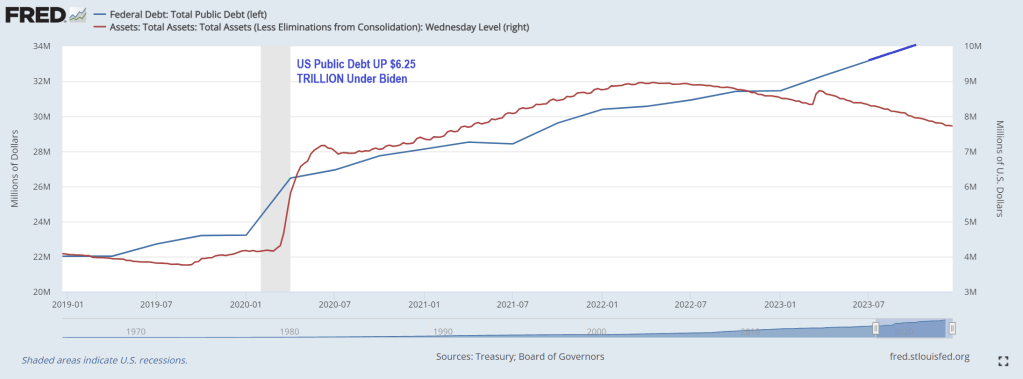

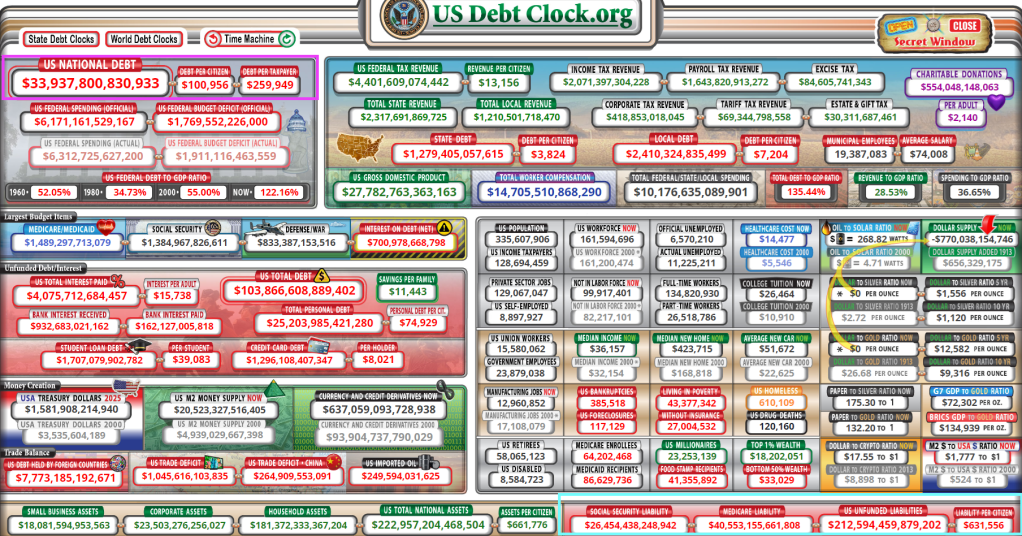

But Biden’s record on jobs comes at the expense of an additional $6.25 TRILLION IN PUBLIC DEBT.

With $34 trillion and rapdily growing debt and budget deficits, it is hard to find good news about Bidenomics.

So much for “The Fed killed inflation” narrative. Inflation is still alive and well in housing prices. Particularly in cities like Miami and Detroit? Maybe the Lions winning their division for the first time in 30 years helped!

The S&P CoreLogic Case-Shiller U.S. National Home Price NSA Index, covering all nine U.S. census divisions, reported a 4.8% annual change in October, up from a 4% change in the previous month. The 10-City Composite showed an increase of 5.7%, up from a 4.8% increase in the previous month. The 20-City Composite posted a year-over-year increase of 4.9%, up from a 3.9% increase in the previous month. Detroit reported the highest year-over-year gain among the 20 cities with an 8.1% increase in October, followed again by San Diego with a 7.2% increase. Portland fell 0.6% and remained the only city reporting lower prices in October versus a year ago.

The Case-Shiller National Home Price index was up 4.8% in October as The Federal Reserve keeps its monstrous foot on the balance sheet pedal.

Home prices in America’s 20 largest cities rose for the 9th straight month in October (the latest data released by S&P Global Case-Shiller today), up 0.64% MoM (slightly better than the +0.60% MoM expected).

That pushed the YoY rise in prices up 4.87% – the fastest pace since Dec ’22…

Source: Bloomberg

…but as the chart shows the MoM gains are slowing rapidly.

“U.S. home prices accelerated at their fastest annual rate of the year in October”, says Brian D. Luke, Head of Commodities, Real & Digital assets at S&P DJI.

“We are experiencing broad based home price appreciation across the country, with steady gains seen in nineteen of twenty cities.”

Miami and Detroit saw the biggest MoM gains while the West Coast dominated the MoM price declines with San Francisco, Portland, and Seattle worst.

But, judging by the resumption of the rise of mortgage rates since the Case-Shiller data was created, we would expect prices to also resume their decline…

Source: Bloomberg

So prices are up, mortgage rates are actually falling again now (lagged)… so The Fed is re-blowing the same bubble?

Well, at least Detroit is near the top! Playing in Rocket Mortgage stadium.

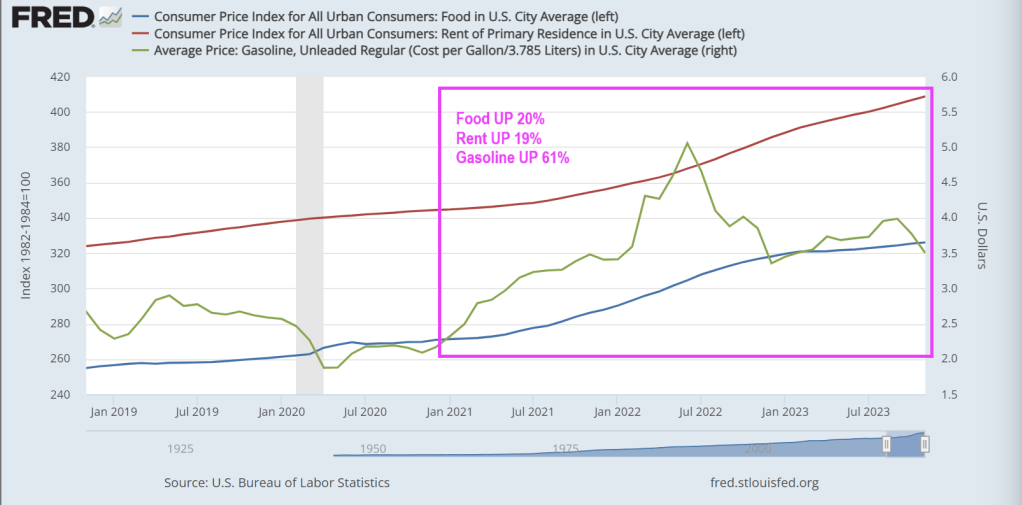

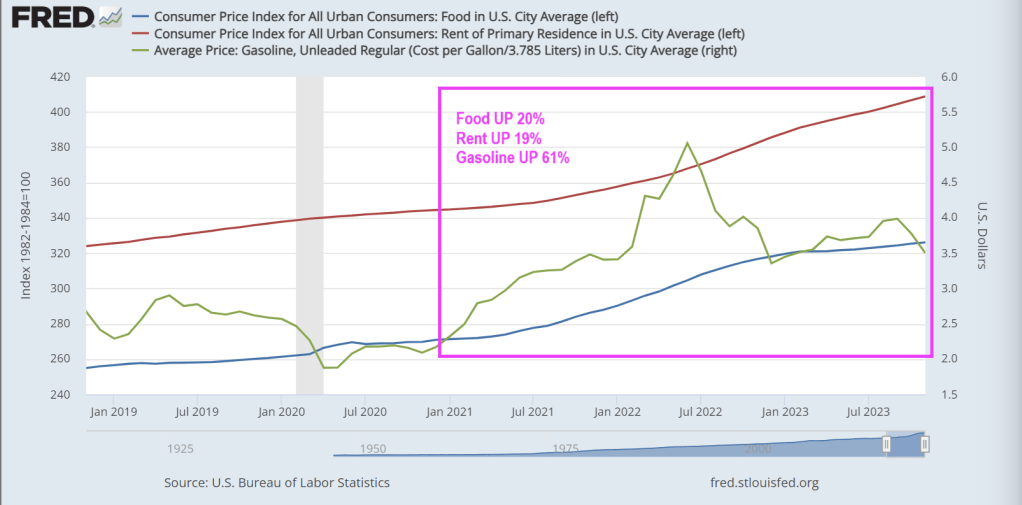

The ‘Misery Index’ is near its lowest level since pre-COVID, but Misery Index masks the true horrors of Bidennomics: 20% higher food prices, 19% higher rents and 61% higher gasoline prices under Bidenomics.

The sum of U.S. unemployment and inflation – known as the “misery index” – fell to 6.8% in November from 7.5% the previous month. That’s the lowest since the summer and fast approaching pre-Covid levels.

The misery index is calculated by adding up the current unemployment rate (3.7%) and the inflation rate (3.1%). The formula provides a simple way to gauge whether the well-being of Americans is improving or not.

Misery peaked in April 2020 when the index spiked to 15%, the highest since 1982. Conditions have improved since the early onset of Covid, but it hasn’t been smooth sailing.

After falling back to 7.7% in January 2021, the index re-accelerated over the next two years as inflation surged. The misery index was 12.5% in June 2022—the same month that annual inflation hit 9.1%.

The unemployment component of the index has been faring well since Covid emergency measures were lifted back in 2021. The unemployment rate has remained below 4% for nearly two years—even as the economy begins to slow.

But economists warn that the misery index doesn’t offer a complete picture of how the average American is doing.

You can tell just by asking them how they feel about the economy and personal finances.

How do Americans really feel?

Economist Greg Ip, who heads economic commentary at The Wall Street Journal, compared the misery index to the University of Michigan’s consumer sentiment index—one of the most closely-watched consumer surveys.

“Based on historic correlations, sentiment has been more depressed this year than you would expect given the level of economic misery,” Ip wrote, arguing that consumers are more pessimistic than the misery index would suggest.

A deeper dive into the sentiment data reveals that Americans are still frustrated about inflation and the impact of high interest rates on their finances. And while the consumer sentiment index rose in December—breaking a four-month skid—some economists attributed it to a temporary holiday boost ahead of Christmas.

“Consumer spirits are perking up for the holiday season which is a sign Christmas is still coming this year,” said Christopher Rupkey, chief economist at FWDBONDS, a New York-based financial research company.

A separate sentiment survey from LSEG/Ipsos paints an even less enthusiastic picture of the average consumer.

The December primary consumer sentiment index—which measures Americans’ attitudes toward jobs, investments, the economy, and personal finances—declined from November and was only up slightly compared to 12 months earlier.

According to the survey, attitudes toward the current situation, investments, and jobs “showed significant declines this month.”

The impact of cumulative inflation

As Creditnews Research reported in a recent study, Americans aren’t celebrating the slowdown in inflation because they’re still reeling from the cumulative price increases of the past three years.

While inflation has fallen to 3.1%, consumer prices have increased by a cumulative 19% since the start of 2020. Food prices are up a whopping 25% over that period.

Americans spent the better part of two years—April 2021 to January 2023—seeing inflation grow faster than their paychecks. That trend reversed in February of this year.

But even with stronger purchasing power this year, the vast majority of Americans (92%) said they reduced their spending in the six months through September, according to a Morning Consult survey for CNBC.

A majority of respondents across all wage brackets said current economic conditions negatively impacted their finances.

So, while the Misery Index indicates that the inflation RATE has slowed, it masks the fact that Americans are far worse off under Bidenomics.

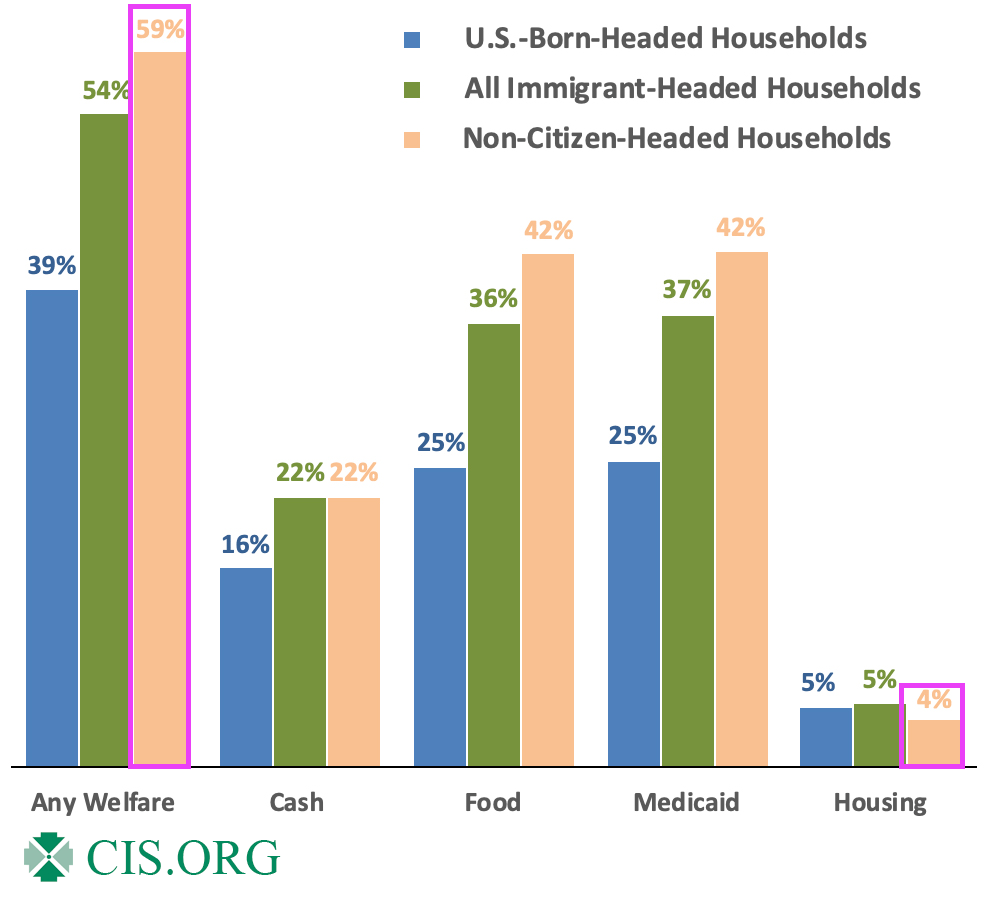

Biden is lucky in that many portray him as a senile, dumb US Senator who happens to be President. Perhaps Biden is actually insidious allowing for open borders in the hopes of crashing the US economy by overloading the welfare system and driving national debt through the roof?

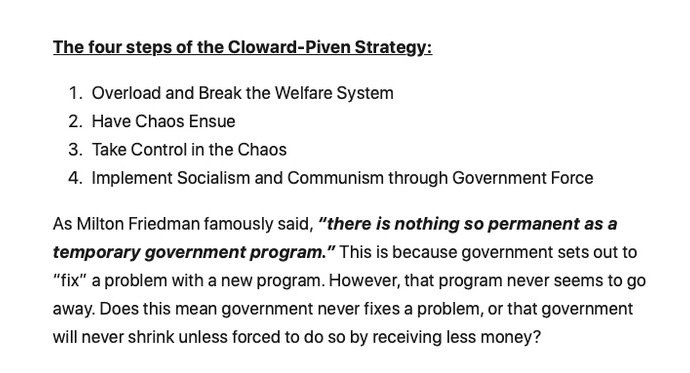

Biden, like Clinton and Obama before him, has been a Cloward-Piven discipile. Who are Cloward and Piven you ask? Two sociologists at Columbia University. (Cloward pass away in 2001, while Piven is still living). Here are Cloward and Piven attending the Voter Registration (aka, Motor Voter Law) Act signing by President “Willie Slick” Clinton.

The Cloward-Piven strategy is to overload the welfare system to the point of chaos, take control and implement Marxism through government force. To that extent, Biden and his incoherent sidekick, Kamala Harris, have been wildly successful. Sociology and Political Science are two of the most worthless college degrees (with Management in the Business School being a close third). Taking advice from Sociologists or Political Science majors or faculty is insane.

Biden should be familiar to Latin American, African and Chinese immigrants who are used to Marxist dictators who try to have their political opponents taken of the ballots and prosecucted.

Yes, the US welfare rolls are overflowing with illegal immigrants and unfunded liabilities are out of control. Perhaps Biden and Harris should be replaced with Cloward and Piven (even though Cloward is dead). But Newsom, Hillary Clinton and Michelle Obama share the idiocy of the Columbia sociology faculty members. Hillary even teaches a course at Columbia!

What about compassion for immigrants? Great! Let’s close the borders and return to LEGAL immigration to halt human trafficking, Fentanyl imports, and cartels controlling the border. But Cloward-Piven’s strategy is best accomplished with open borders and weak-willed politicians.

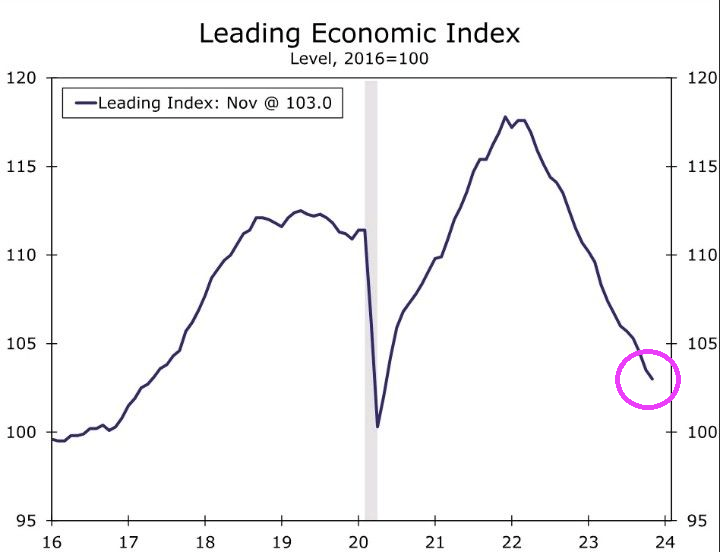

The Conference Board Leading Economic Index® (LEI) for the U.S. declined by 0.5 percent in November 2023 to 103.0 (2016=100), following a (downwardly revised) decline of 1.0 percent in October. The LEI contracted by 3.5 percent over the six-month period between May and November 2023, a smaller decrease than its 4.3 percent contraction over the previous six months (November 2022 to May 2023).

Of course, investors don’t care about actual fundamentals, rates are down so ‘buy buy buy’ the builders…

Source: Bloomberg

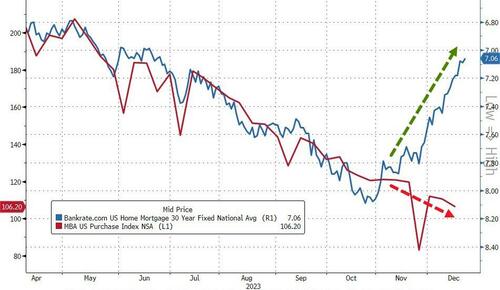

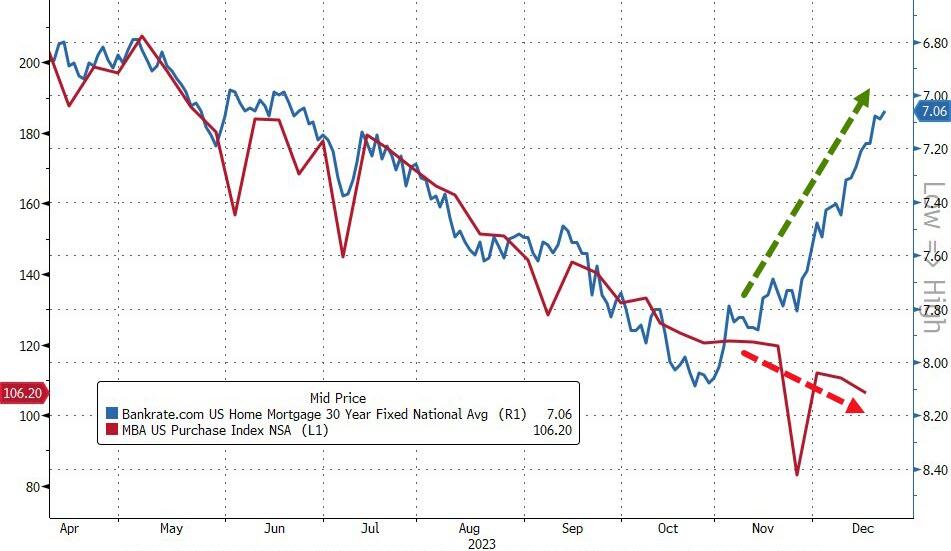

Trouble is, even as mortgage rates have plunged recently, applications for home purchases has continued to decline…

Source: Bloomberg

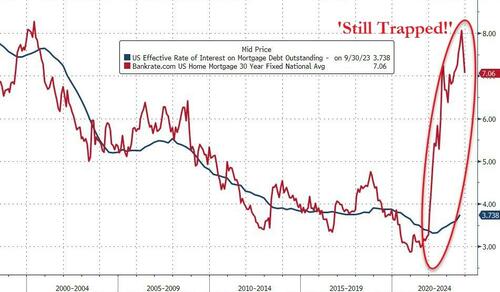

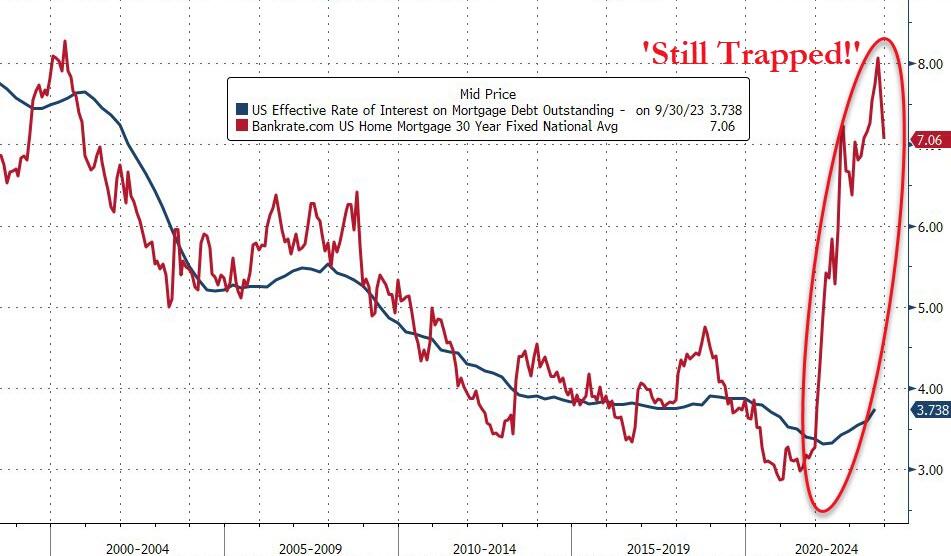

And while mortgage rates have declined (rapidly), they remain massively high relative to the effective mortgage rate for all Americans. That difference is the ‘subsidy‘ that homebuilders have to fill to enable buyers – and it’s still yuuuge!

Source: Bloomberg

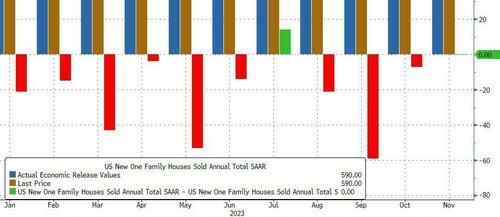

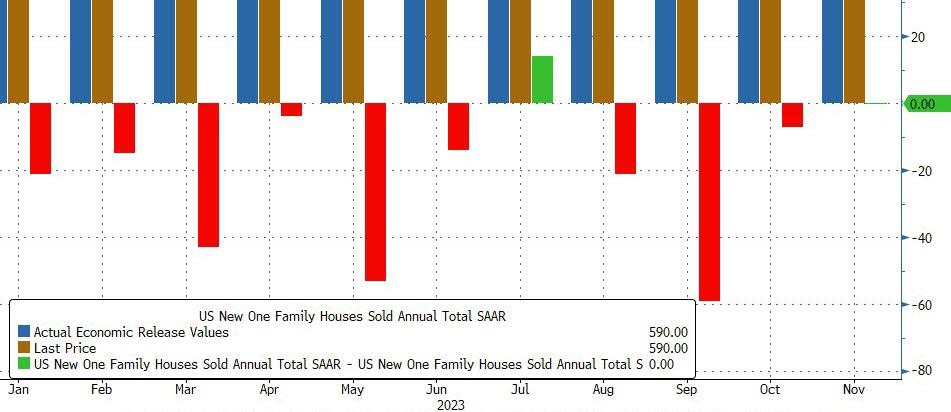

So, just how many new homes were sold in November?

The last few months have been very choppy for new home sales but November clarified that homebuilders just hit a wall on their subsidization!

New home sales crashed 12.2% MoM – the biggest MoM drop since April 2022. That dragged the YoY change to just 1.4%…

Source: Bloomberg

9 of the last 10 months have seen downward revisions to the new home sales SAAR!

Source: Bloomberg

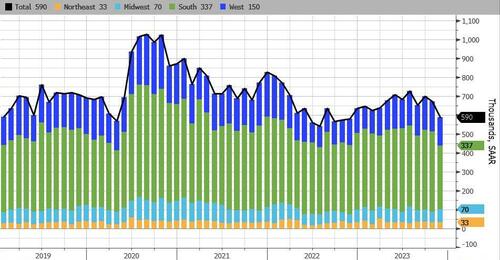

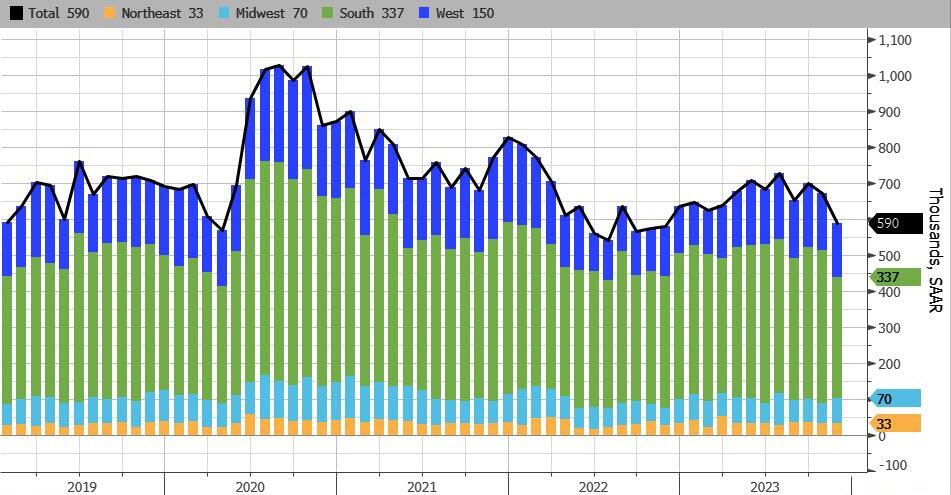

New home sales fell in the South by the most, followed by the West. The Northeast and Midwest saw increased sales…

Source: Bloomberg

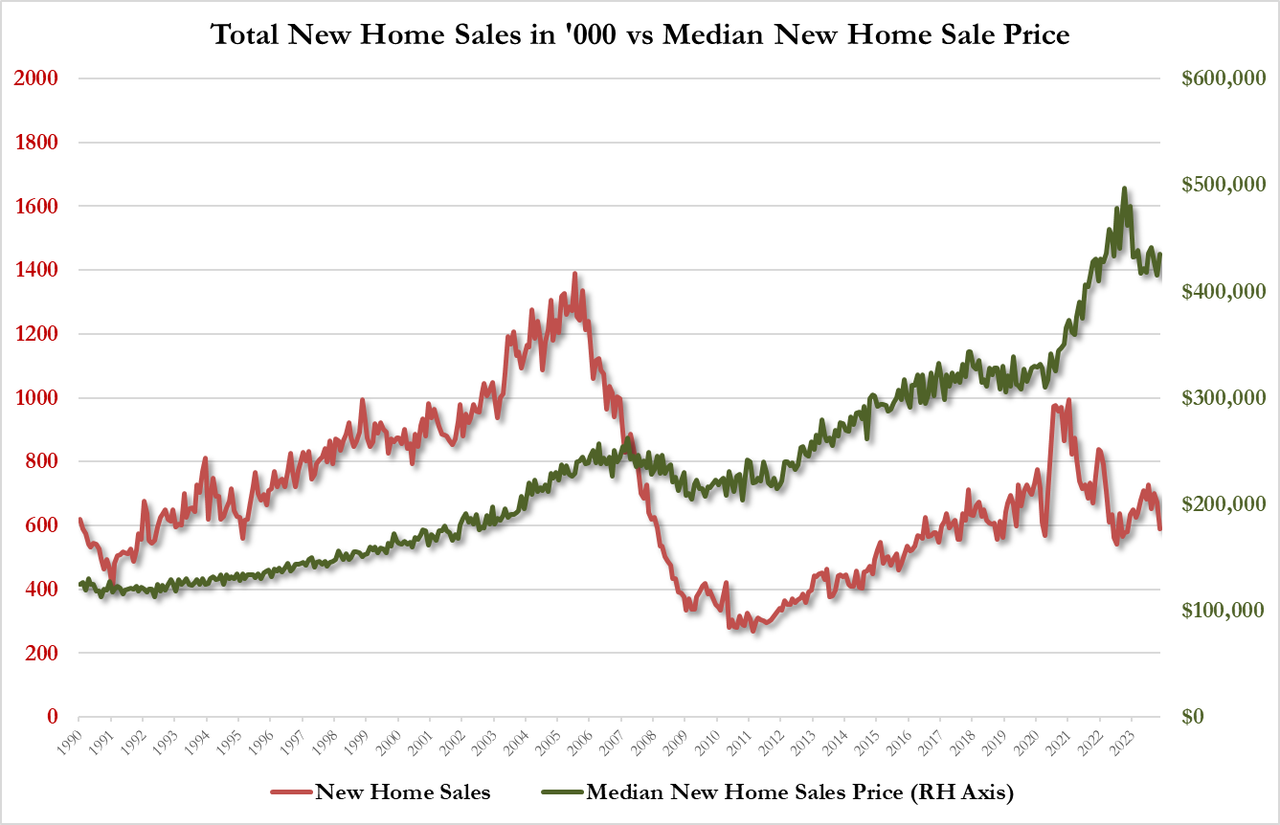

The new home sales SAAR printed 590k (well below the 690k exp) – the lowest since Nov 2022… catching down to existing home sales reality…

Source: Bloomberg

And another catch-up to reality for sales, even as rates tumble…

Source: Bloomberg

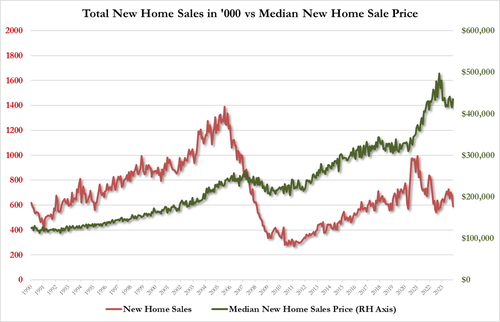

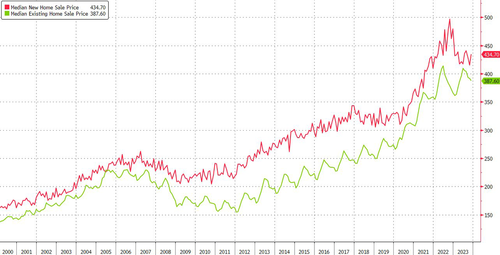

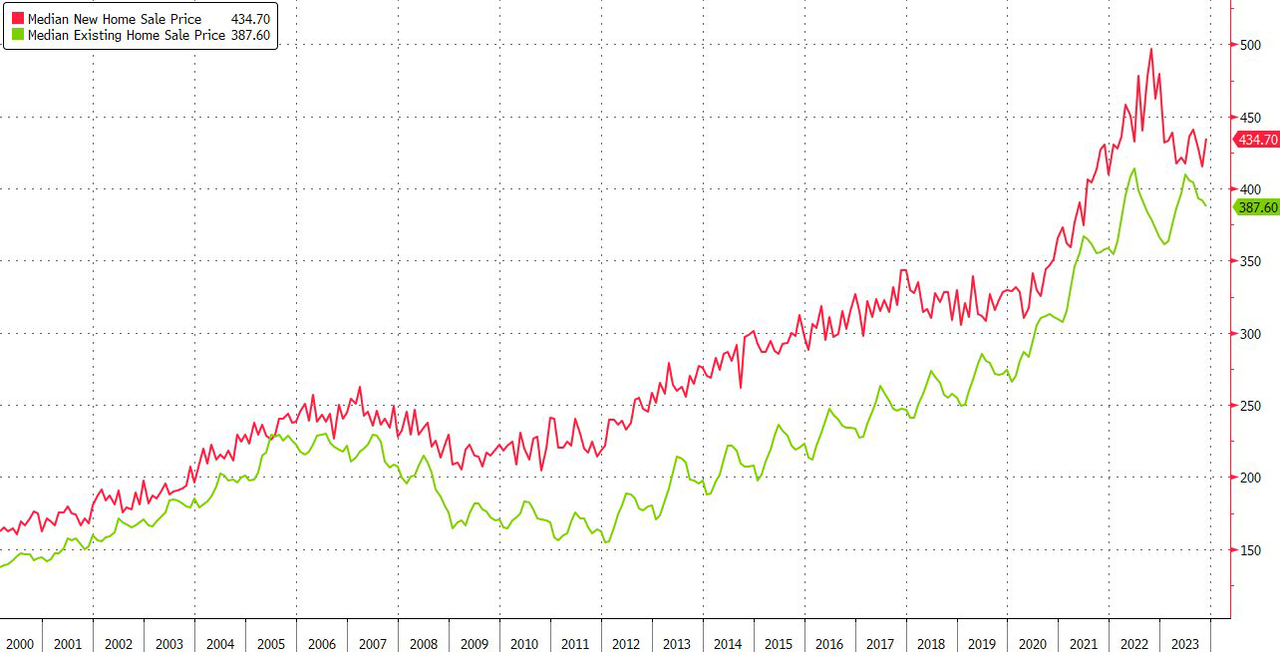

Finally, we note that the median new home priced jumped to $434.7k from $414.9k…

Source: Bloomberg

The median existing home price dropped to lowest since April while median new home price jumped to highest since August

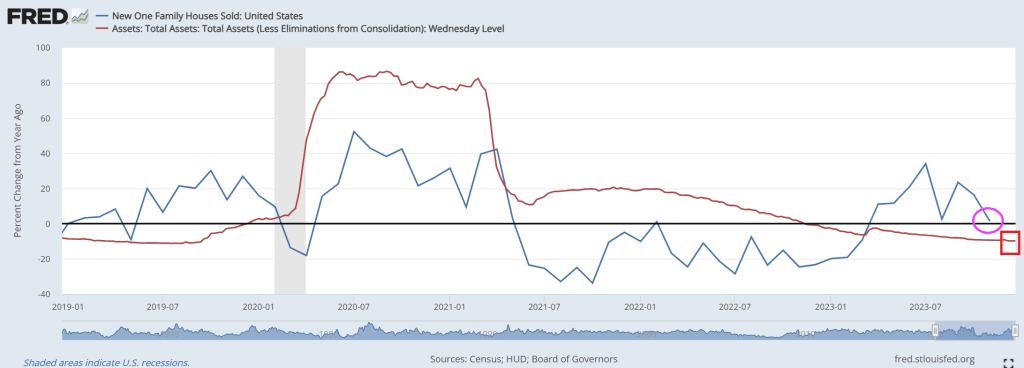

Odd that these ‘actual’ new home sales are plunging as ‘soft survey’ data shows homebuilder sentiment rising, and housing starts.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

You must be logged in to post a comment.