Major cryptocurrencies erased losses and turned higher after Binance Holdings Ltd.’s Chief Executive Officer Changpeng Zhao said the world’s largest digital-asset exchange plans to set up an industry recovery fund.

Zhao said Monday the goal was to “reduce further cascading negative effects” of the bankruptcy of rival exchange FTX, adding the fund will assist otherwise strong projects that are facing a liquidity squeeze.

So, cryptos are up today with Cronos up 24% overnight. Of course, Cronos is trading near zero, so any upturns in price register as large turns.

But across the board, cryptos are up. Of course, if Zhao changes his mind, look out.

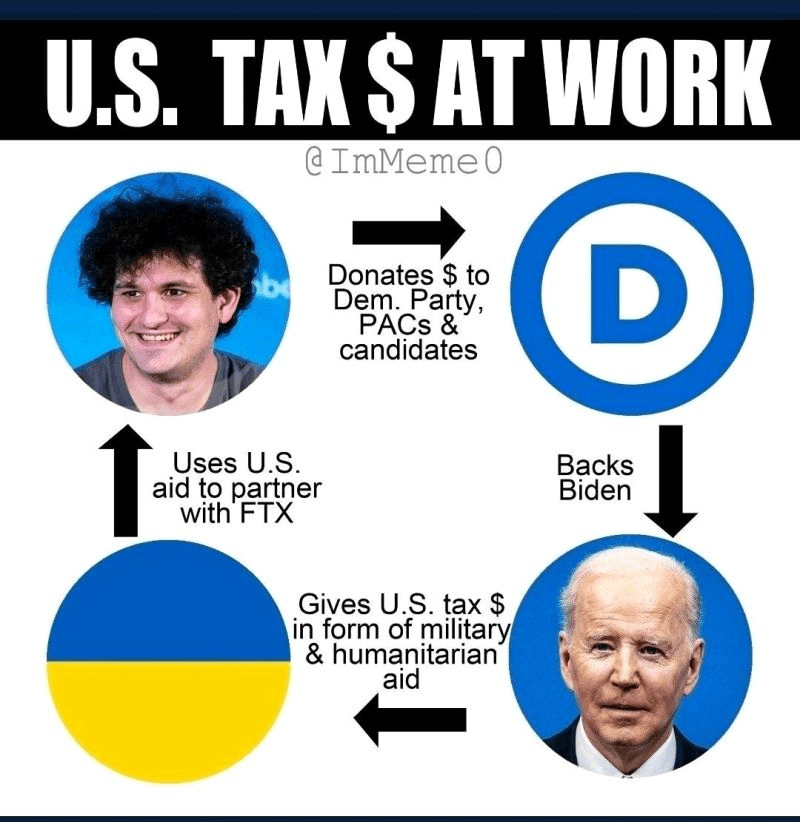

I am waiting for the list of pension funds that invested in Sam Bankman-Fried’s schemes.

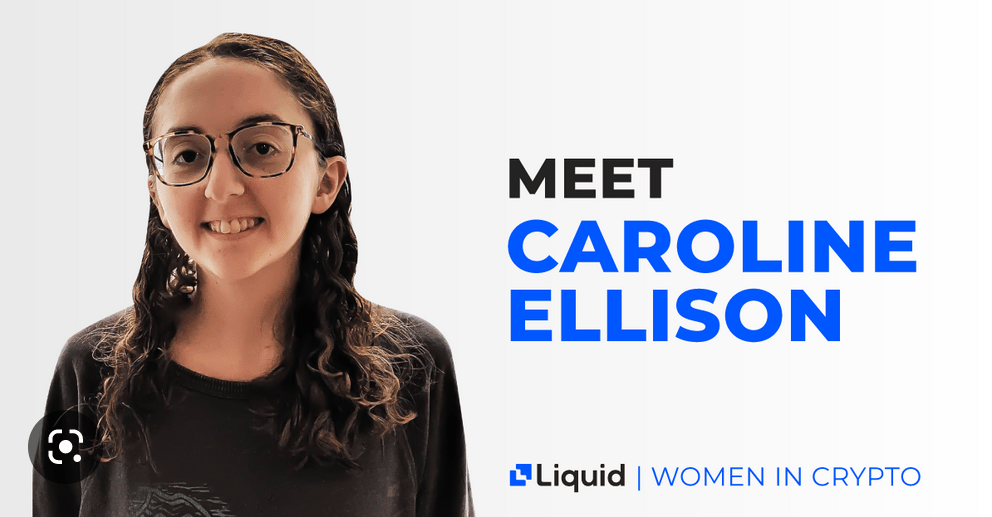

Let’s see if Alameda Research’s CEO Caroline Ellison faces any wrath from the DOJ or SEC. I doubt it.

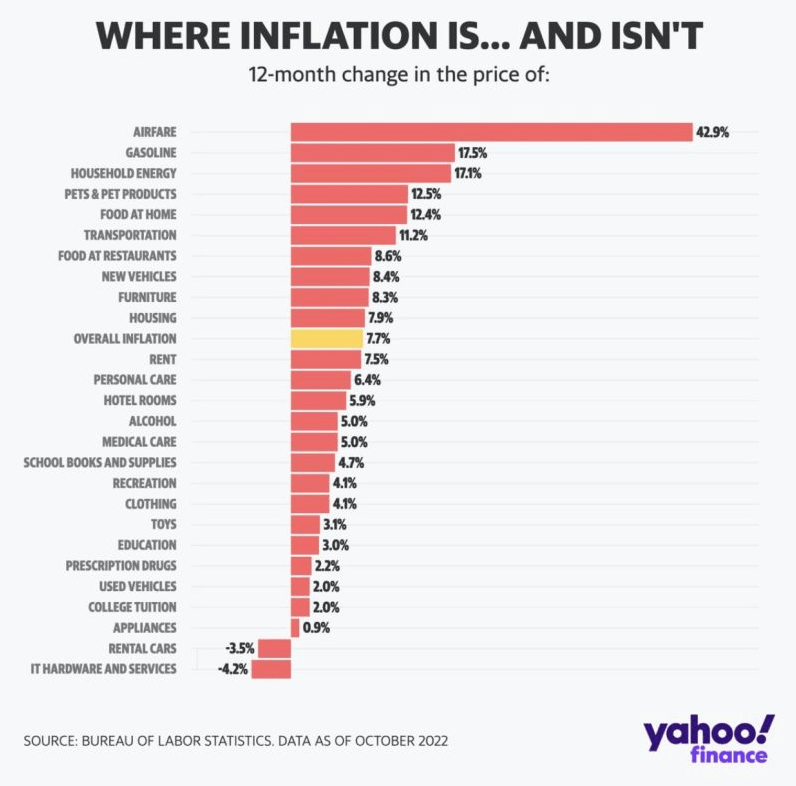

The inflation numbers are out for October and they still stink (headline inflation still sizzling at 7.7% YoY).

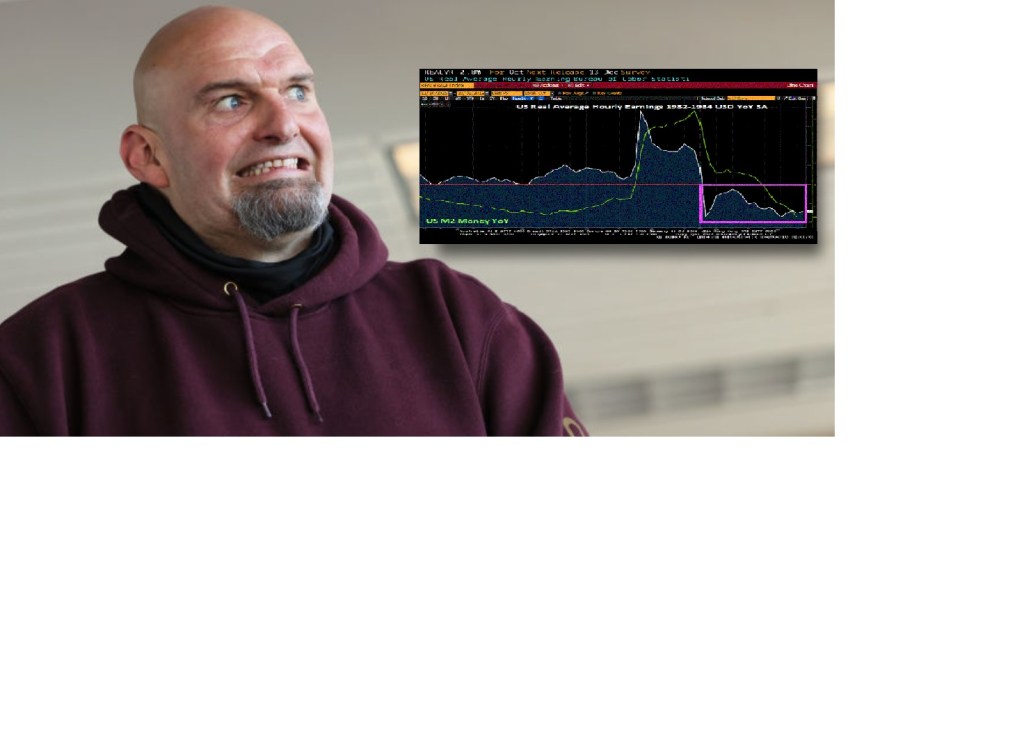

But the number that really irks me is … REAL average hourly earnings growth is at a horrifying -2.8% YoY because of Biden’s terrible policies (aka, Bidenflation).

Real average hourly earnings growth YoY has been negative since March 2021. That is 19 straight months of negative earnings growth under Biden/Pelosi/Schumer’s reign of error.

Overall, airfares are leading followed by gasoline and household energy.

So, Pennsylvania elects this guy to perpetuate Biden/Pelosi/Schumer’s awful policies?

According to Real Clear Politics, the generic Republican polling data FAVORABLE (red line) is at 47.9% while Democrat polling data favorable polling data (yellow line) is at 45.4%, advantage Republicans.

Biden has been a disaster as President (energy mandates, Afghanistan debacle, endless funding of Ukraine, highest inflation in 40 years, and every time he opens his mouth. But it is the “kitchen table” issues where Biden is getting clobbered: inflation, rising gas, food and diesel prices. One Democrat Congressman, Sean Patrick Maloney, said “Let them eat Chef Boyradee.” I can’t believe how tone deaf some politicians can be.

Biden’s UNFAVORABLE polling numbers (orange line) are directly related to the US headline inflation rate. Inflation was 1.4% YoY when Biden became President and it is now 8.2% YoY (blue line).

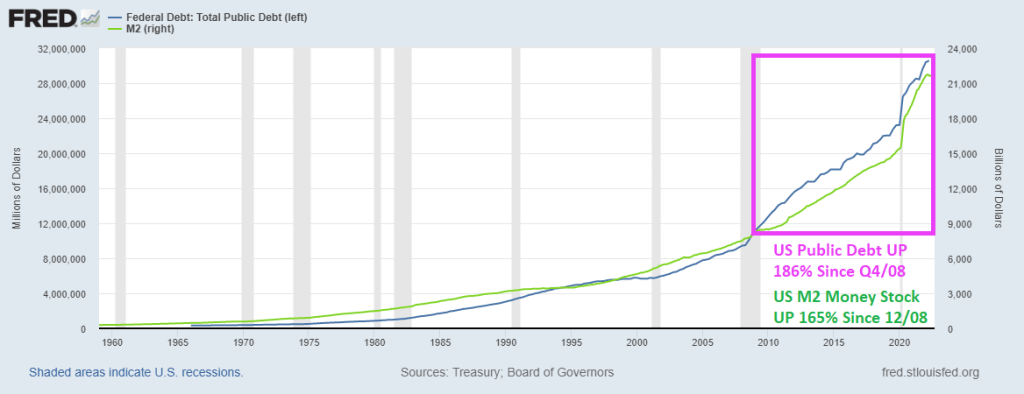

Ever since the financial crisis of 2008 and the election of President Obama and a Democrat Congressional sweep, the US has embraced Modern Monetary Theory (MMT or borrow, print and spend without consequence). And between the financial crisis and the Covid crisis of 2008, we have seen an increase in US public debt from $10.7 trillion in Q4 2008 to a staggering $30.6 trillion as of Q2 2022. That is a staggering increase of 186% in only 14 years.

How about US Money stock? M2 Money stock has grown by 162.5% since the beginning of 2009 and the “Blue Wave” of 2008. And nothing has been the same.

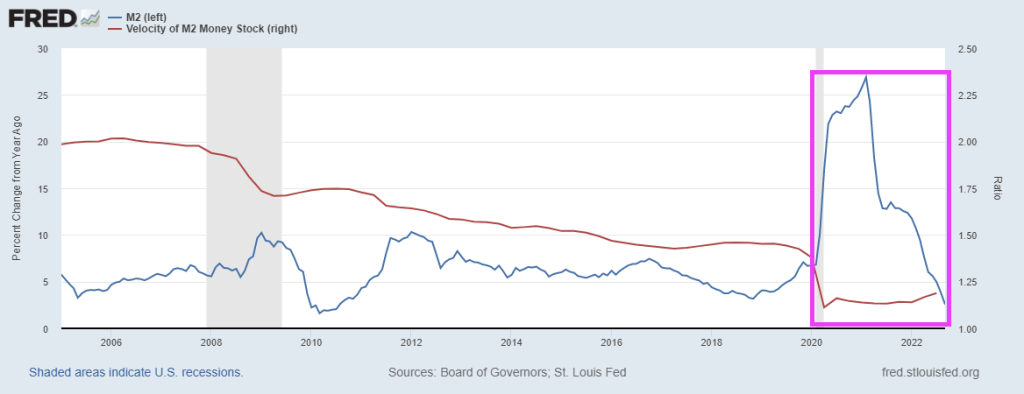

The Covid outbreak in early 2020, we saw Fed money printing that has never seen before … or since. But one thing is for sure, M2 Money Velocity (GDP/M2) is near all-time lows.

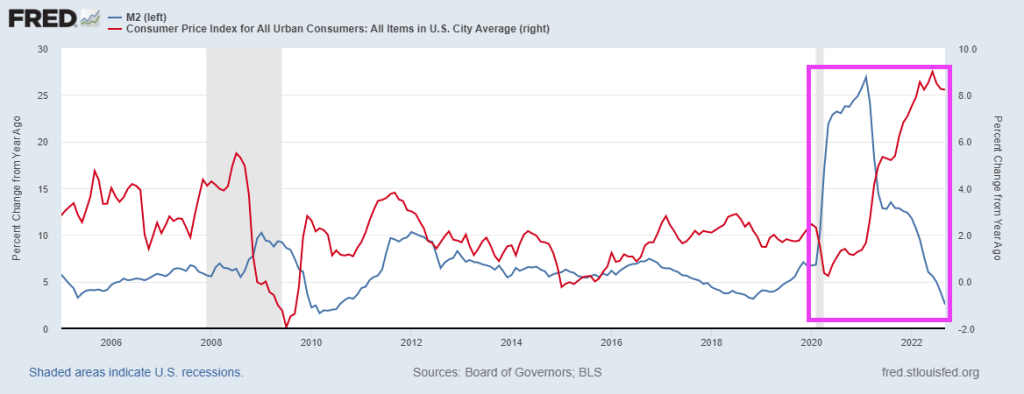

Then we have headline US inflation as a function of M2 Money growth YoY.

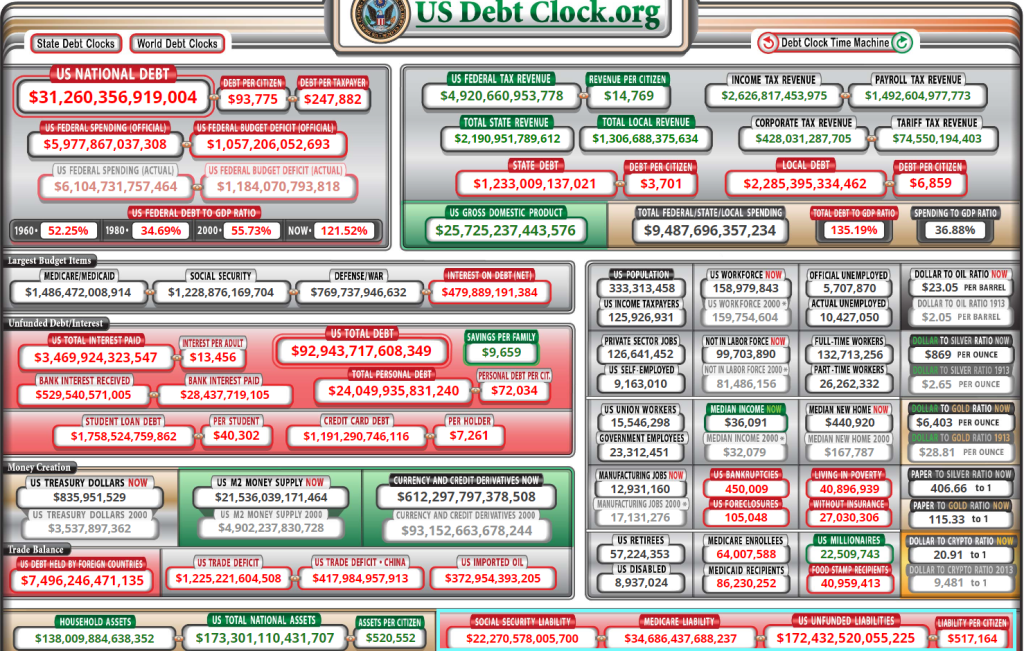

And it is the midterm election “silly season” where no politician will discuss the complete and utter mess they have made. According to US Debt Clock, US national debt is already up to $31.26 trillion (OMG!), but the REALLY scary number that not a single politician will address is UNFUNDED LIABILITIES OF $172.4 TRILLION.

Can we go back to the gold standard? Or silver standard? Or ANY standard for that matter??

Instead, we have porous borders and patently UNSOUND money, thanks to MMT.

The Bank of England followed the Fed’s 75 basis-point increase with an equivalent hike on Thursday, but strongly pushed back against market expectations for the scale of future increases, warning that following that path would induce a two-year recession. The pound fell 1.8% to $1.1183.

Stocks and bonds fell as Jerome Powell’s warning that the Federal Reserve would raise interest rates more than previously anticipated sapped risk appetite. The dollar gained.

Futures on the S&P 500 fell 1% in the wake of Wednesday’s 2.5% drop. The selloff spread to Europe and Asia, where China’s affirmation of its Covid-Zero stance dashed hopes of a reopening. Lumen Technologies Inc., Peloton Interactive Inc., Moderna Inc. and Qualcomm Inc. tumbled in premarket trading, while Etsy Inc. and EBay Inc. rose.

So, the BofE, Fed and ECB are back to 2008/2009 era central bank rates.

But the US Fed is slow to shrink its enormous balance sheet.

The S&P 500 index tanked -2.35% after Powell and The Fed failed to pivot.

Federal Reserve Chair Jerome Powell opened a new phase in his campaign to regain control of inflation, saying US interest rates will go higher than previously projected, but the path may soon involve smaller hikes.

Addressing reporters Wednesday after the Fed raised rates by 75 basis points for the fourth time in a row, Powell said “incoming data since our last meeting suggests that ultimate level of interest rates will be higher than previously expected.”

Powell said is it would be appropriate to slow the pace of increases “as soon as the next meeting or the one after that. No decision has been made,” he said, while stressing that “we still have some ways” before rates were tight enough.

“It is very premature to be thinking about pausing,” he said.

Fed Funds Futures data point now to a June peak in the target rate of 5.055%, then a decline.

The next Federal Reserve Open Market Committee (FOMC) meeting in on Wednesday, November 2nd. Let’s see what The Fed does with its BIG GREEN BAG … OF MONEY.

As I set here on Sunday morning waiting to see how the Cleveland Browns will lose to cross-state rival Cincinnati Bengals, I see that both the US Treasury 10yr-2yr and 10yr-3mo yield curves are inverted (below zero).

Core inflation (CPI less food and energy) YoY (blue line) was only 1.3% in February 2021 shortly after Biden was sworn-in as President and is now 6.6% in September 2022. That is over a 400% increase in core inflation!

We have this tantalizing headline on Bloomberg:

Goldman Sachs Now Sees Fed Rates Peaking at 5% in March By Simon Kennedy(Bloomberg) —

Goldman Sachs Group Inc. economists said they now expect the US Federal Reserve to raise interest rates to 5%, higher than previously predicted.

The central bank will lift its benchmark rate to a range of 4.75% to 5% in March, 25 basis points more than earlier expected, economists led by Jan Hatzius wrote in an Oct. 29 research report.

The route to the new peak includes increases of 75 basis points this week, 50 basis points in December and 25 basis points in February and March, they said.

The economists cited three reasons for expecting the Fed to hike beyond February: “uncomfortably high” inflation, the need to cool the economy as fiscal tightening ends and price-adjusted incomes climb, and to avoid a premature easing of financial conditions.

Well, not exactly earth-shattering. Fed Funds Futures data point to a peak of near 5% (4.905%) for the May 2023 FOMC meeting, so Goldman Sachs is calling for an earliest peak at the March 2023 FOMC meeting,

Regardless of what Goldman Sachs thinks, Fed officials are expecting a peak in 2023 followed by a decline to 2.5%.

Brainard and Bostic are the only “doves.” Which is silly because Chicago’s Evans is a perma-dove. Let’s see how the Dots Plot changes at the November 2nd meeting.

America’s distressed debt pile is biggest since September 2020.

You must be logged in to post a comment.