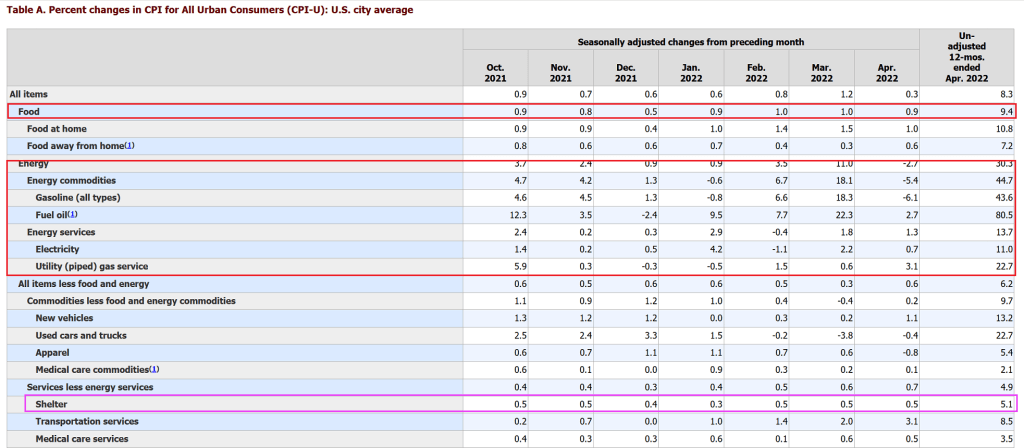

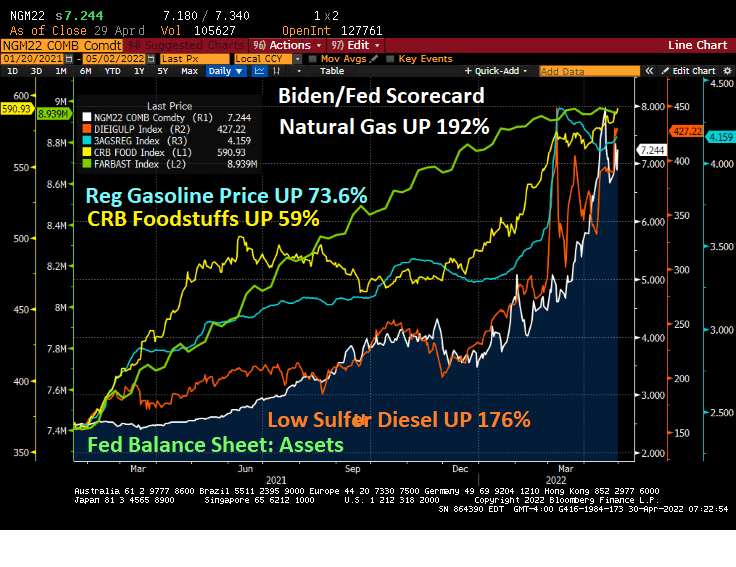

Most of us are painfully aware of rising food prices, particularly with the US fighting a proxy war with Russia. Wheat prices have doubled under Biden and the Russian invasion of Ukraine.

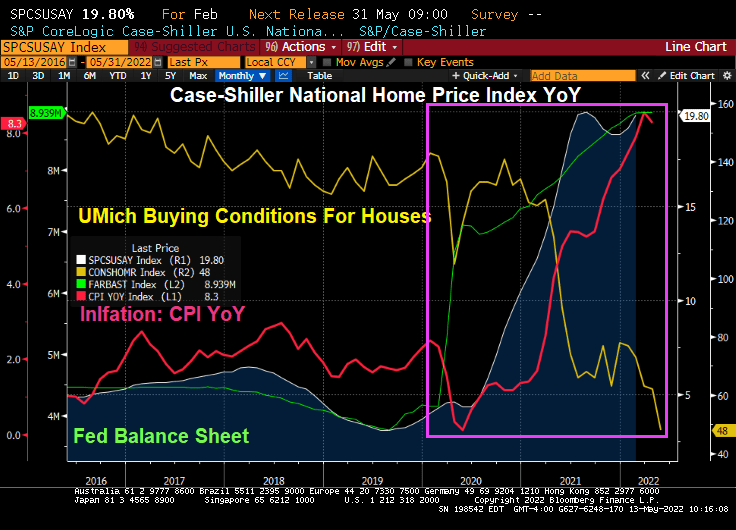

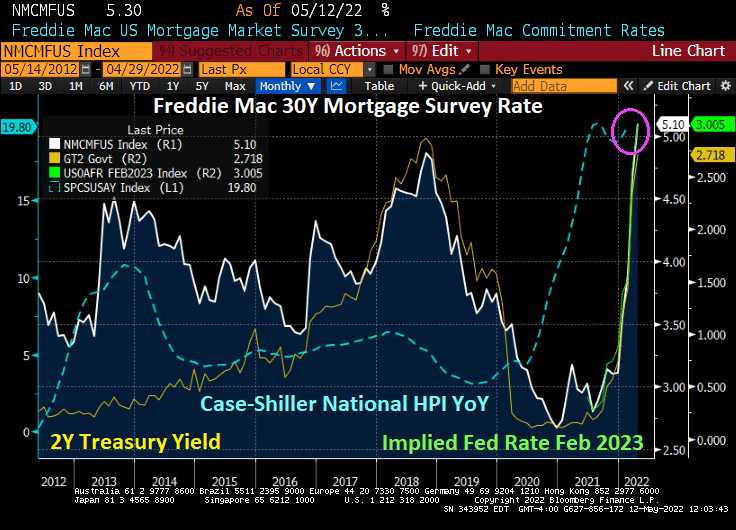

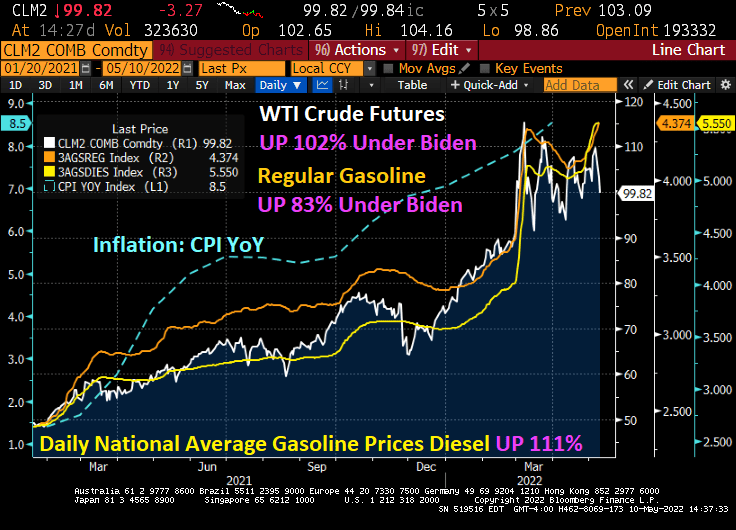

But inflation is everywhere. Rising home prices, rising gasoline and diesel prices, etc. When Jeep can see a Wagoneer for $100,000+, you know we have inflation.

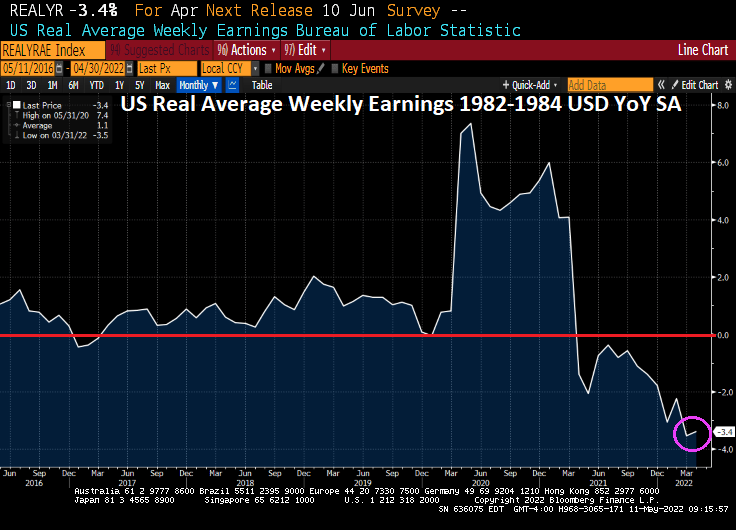

The surprise this morning was retail sales, up 0.9% MoM (though still less than expected), despite rising prices. Odd since REAL wage growth is negative.

But the other bit of good news this AM is that US industrial production rose +1.1% MoM in April. And US Capacity Utilization is rising dangerously towards 80%, it is at 79% in April.

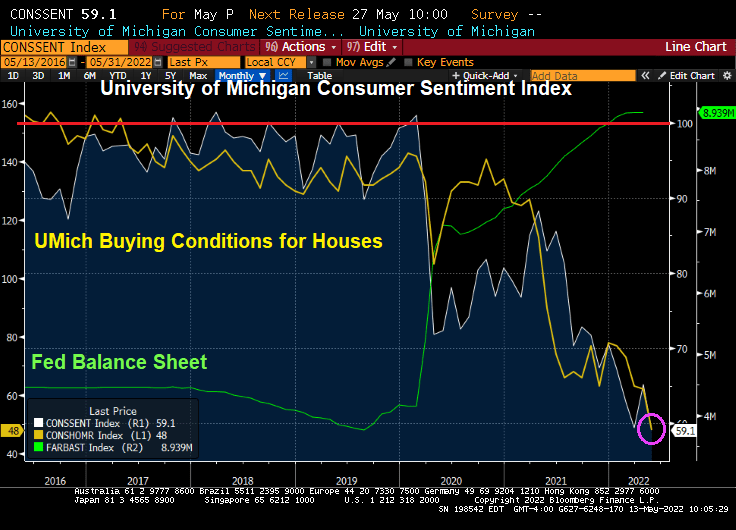

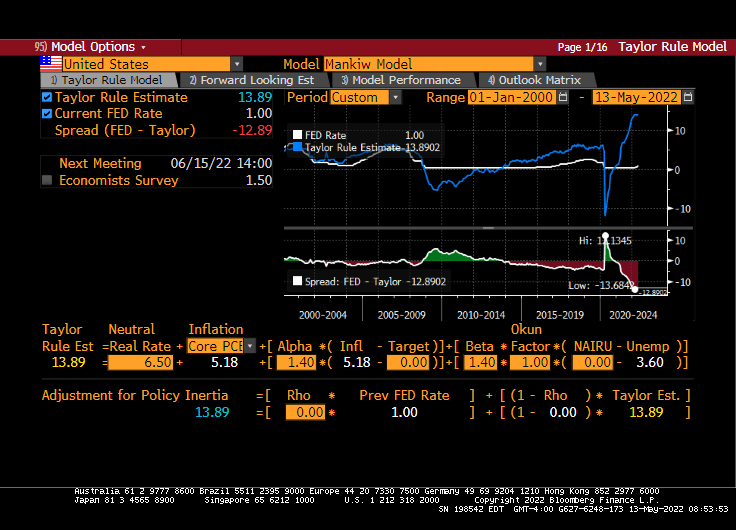

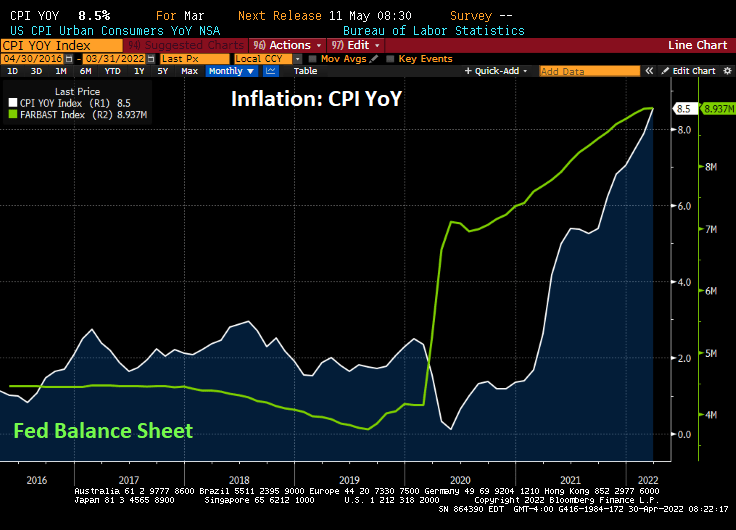

You will notice that Fed monetary tightening occurs when capacity utilization hits 80%, indicating an overheated (or OVERSTIMULATED) economy. Yes, we still have The Fed Funds Target Rate (Upper Bound) at only 1% and The Fed Balance Sheet still near $9 trillion. So, Fed stimulypto is still in play.

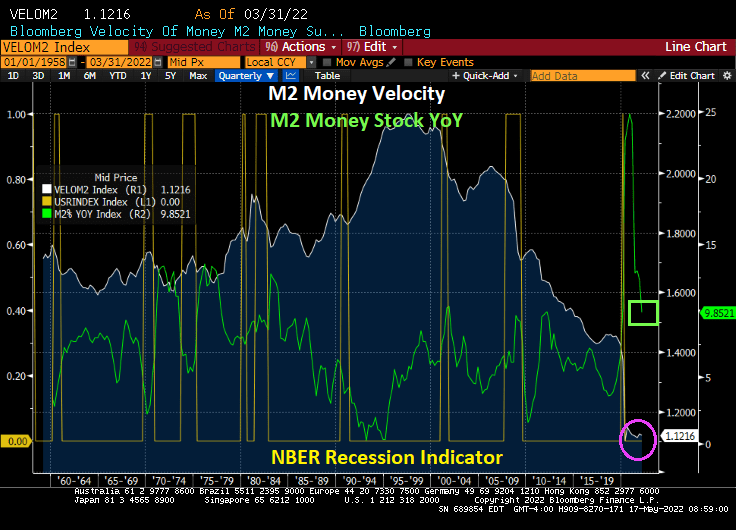

Meanwhile, M2 Money Velocity is near its historic low and M2 Money YoY is still sizzling at 9.85% YoY.

Wheat prices have doubled under Biden, and you can see how wheat futures soared when Russia invaded Ukraine.

So, despite The Fed’s intent to tighten, The Federal Reserve and Fed government are still overstimulating the economy. But what happens when the stimulus is gone?

Fear the Talking Fed!

You must be logged in to post a comment.