The Fed’s favorite yield curve measure, the implied yield on 3-month T-Bills in 18 months less the 3-month T-bill yield has inverted. Note that this curve inverts prior to a recession.

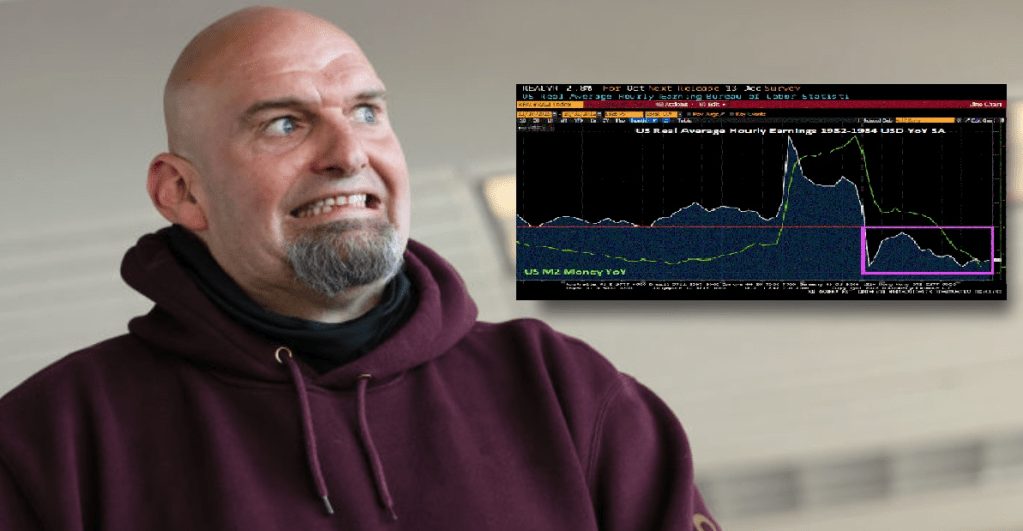

The new face of reckless Fed policy and Federal spending. 19 straight months of negative REAL earnings growth as America re-elects the same irresponsible fools that are turning the US into Venezuela.

Now that the midterm elections are over (except for counting of million of mail-in ballots, a massive moral hazard risk), President Biden has proclaimed that he isn’t changing any of his horrid policies. And apparently, neither is The Federal Reserve.

US mortgage applications declined for the sixth consecutive week despite a slight drop in rates.

Mortgage applications decreased 0.5 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending October 28, 2022. This week’s results include revised data to reflect an update to last week’s survey results.

The Refinance Index increased 0.2 percent from the previous week and was 85 percent lower than the same week one year ago. The seasonally adjusted Purchase Index decreased 1 percent from one week earlier. The unadjusted Purchase Index decreased 2 percent compared with the previous week and was 41 percent lower than the same week one year ago.

This morning’s WIRP (Fed Funds Futures data) is pointing to a 75 basis point increase from The FED FOMC (open market committee) at 2pm EST, rising to over 5% by the May 2023 meeting before declining again.

Things are getting interesting in DC, to say the least. The US is 100% likely to face a recession in the next 12 months while The Federal Reserve is on its crusade to fight inflation caused by … The Federal Reserve, Biden’s green energy shenanigans and massive, irresponsible Federal spending that even Former Obama economist Lawrence Summers warned would cause inflation. So what will The Fed do? Lower rates and expand their assets purchases to fight the impending recession OR keep tightening to fight Bidenflation? But where we are now is that the fixed-income market could be in big, big trouble.

For months, traders, academics, and other analysts have fretted that the $23.7 trillion Treasuries market might be the source of the next financial crisis. Then last week, U.S. Treasury Secretary Janet Yellen acknowledged concerns about a potential breakdown in the trading of government debt and expressed worry about “a loss of adequate liquidity in the market.” Now, strategists at BofA Securities have identified a list of reasons why U.S. government bonds are exposed to the risk of “large scale forced selling or an external surprise” at a time when the bond market is in need of a reliable group of big buyers.

“We believe the UST market is fragile and potentially one shock away from functioning challenges” arising from either “large scale forced selling or an external surprise,” said BofA strategists Mark Cabana, Ralph Axel and Adarsh Sinha. “A UST breakdown is not our base case, but it is a building tail risk.”

In a note released Thursday, they said “we are unsure where this forced selling might come from,” though they have some ideas. The analysts said they see risks that could arise from mutual-fund outflows, the unwinding of positions held by hedge funds, and the deleveraging of risk-parity strategies that were put in place to help investors diversify risk across assets.

In addition, the events which could surprise bond investors include acute year-end funding stresses; a Democratic sweep of the midterm elections, which is not currently a consensus expectation; and even a shift in the Bank of Japan’s yield curve control policy, according to the BofA strategists.

The BOJ’s yield curve control policy, aimed at keeping the 10-year yield on the country’s government bonds at around zero, is being pushed to a breaking point.

Well. Bidenflation certainly isn’t helping, but Statist Economist and Cheerleader Janet Yellen can’t bring herself to blame green energy policies, rampant Federal spending or irresponsible Federal Reserve policies for the crisis.

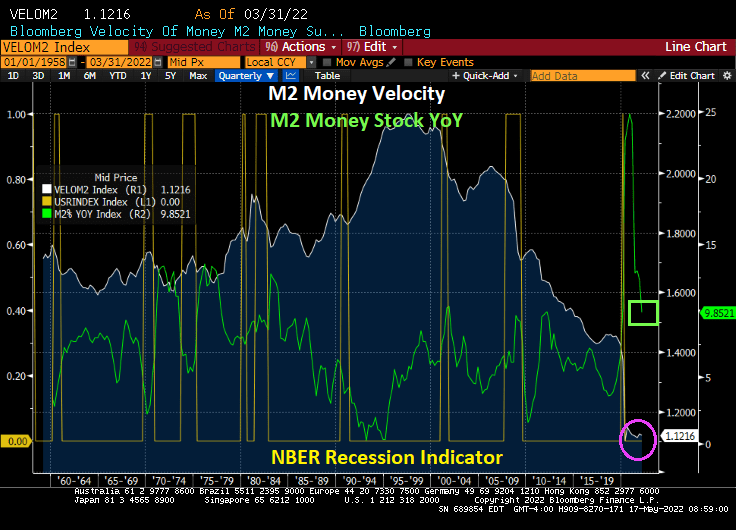

You will note the differences between today and the financial crisis of 2008-2009. The financial crisis gave us a massive surge in government securities liquidity thanks to then Fed Chair Ben Bernanke imitating Japan’s Central Bank and buying US government securities. Fast forward to today and the liquidity index hasn’t budged much since 2010 (except for a little blip around the Covid Fed intervention of early 2020), but we are now seeing near 40-year highs in inflation and a barely declining Fed balance sheet. And M2 Money YoY (mostly commercial bank deposits) are crashing.

I am guessing that The Fed will pivot given that stock futures are way up for Monday. The Dow Jones mini is up 770 points and the S&P 500 mini is up 88.75 points.

Bond market futures (specifically the US Ultra Bond) is down for Monday, meaning yields will be climbing.

I remember giving a speech at The Brookings Institute in Washington DC. Talk about stranger in a strange land. One person who I was debating got frustrated and said “You are such a … Republican!!!” As if that was the worst slur he could throw at me.

Bloomberg’s recession probability over next 12 months is … 100%.

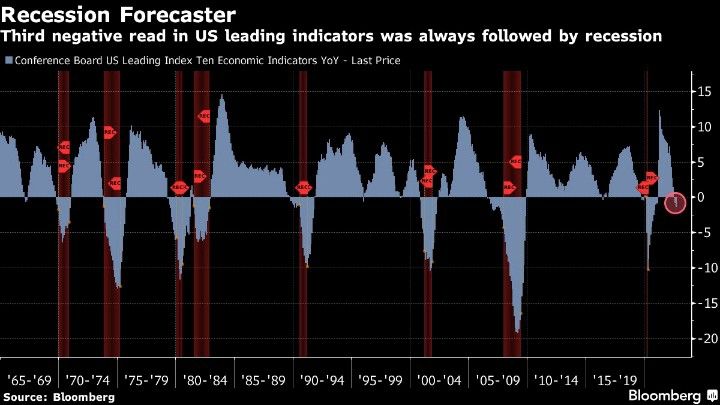

And how about the Conference Board’s Leading index of 10 economic indicators YoY? Third negative read ALWAYS followed by recession.

The Federal Reserve may be forced to pivot. This may be one reason why the Dow is up 565 points today (+1.86%) as recession and pain become ever more likely.

Look at commercial banks deposits. Wonder why liquidity is drying up?

US core inflation keeps rising and diesel fuel, the life line of the economy, is rising again and is UP 107% under Biden. And the inventory of diesel fuel is DOWN -35.2%.

Speaking of the end of the world, NAHB foot traffic has collapsed.

Bidenflation is just killing us. Now rising prices and The Fed’s counterattack are killing retail sales for American consumers.

US retail sales were sluggish last month, suggesting shoppers are becoming more guarded about discretionary purchases in the worst inflationary environment in decades.

The value of overall retail purchases were little changed in September after an upwardly revised 0.4% gain in August, Commerce Department data showed Friday. Excluding gasoline, retail sales were up 0.1%. The figures aren’t adjusted for inflation.

The median estimate in a Bloomberg survey of economists called for a 0.2% advance in retail sales. Seven of 13 retail categories declined last month, according to the report, including a drop in receipts at auto dealers, furniture outlets, sporting goods stores and electronics merchants. The value of sales at gas stations fell 1.4%, reflecting cheaper fuel prices, but they’re now climbing.

At least Export Prices YoY are down below 10%! I hope exporting inflation to the world isn’t Secretary of State Antony Blinken’s idea of good foreign policy.

My favorite headline of the day is “Macron Reminds Biden to Think Before Speaking: “Biden’s Reckless Rhetoric puts World at Risk”“

At The Fed continues to tighten to fight inflation, pending home sales in July crashed and burned. That is, pending home sales fell -22.5% in July as M2 Money growth slowed

If I was still teaching at Ohio State or Chicago, I would ask the students if they see the relation between M2 Money growth and pending home sales.

Today’s jobs report was … strange. While the US economy added more jobs than expected, we also saw labor force participation contract and real wage growth decline again.

The reaction in the bond market? US Treasury 10-year yields exploded by +14 basis points. As I used to tell my fixed-income students, any basis point jump or decline of 10 basis points or more is a BIG DEAL.

The implied target rate for The Fed (based on Fed Funds Futures) is now lower for the Jan 1, 2024 FOMC meeting (3.025%) than it is for the Sept 21, 2022 FOMC meeting (3.034%).

Mortgage rates? They will go up as The Fed removes its Brawndo, the economy mutilator.

Most of us are painfully aware of rising food prices, particularly with the US fighting a proxy war with Russia. Wheat prices have doubled under Biden and the Russian invasion of Ukraine.

But inflation is everywhere. Rising home prices, rising gasoline and diesel prices, etc. When Jeep can see a Wagoneer for $100,000+, you know we have inflation.

The surprise this morning was retail sales, up 0.9% MoM (though still less than expected), despite rising prices. Odd since REAL wage growth is negative.

But the other bit of good news this AM is that US industrial production rose +1.1% MoM in April. And US Capacity Utilization is rising dangerously towards 80%, it is at 79% in April.

You will notice that Fed monetary tightening occurs when capacity utilization hits 80%, indicating an overheated (or OVERSTIMULATED) economy. Yes, we still have The Fed Funds Target Rate (Upper Bound) at only 1% and The Fed Balance Sheet still near $9 trillion. So, Fed stimulypto is still in play.

Meanwhile, M2 Money Velocity is near its historic low and M2 Money YoY is still sizzling at 9.85% YoY.

Wheat prices have doubled under Biden, and you can see how wheat futures soared when Russia invaded Ukraine.

You must be logged in to post a comment.