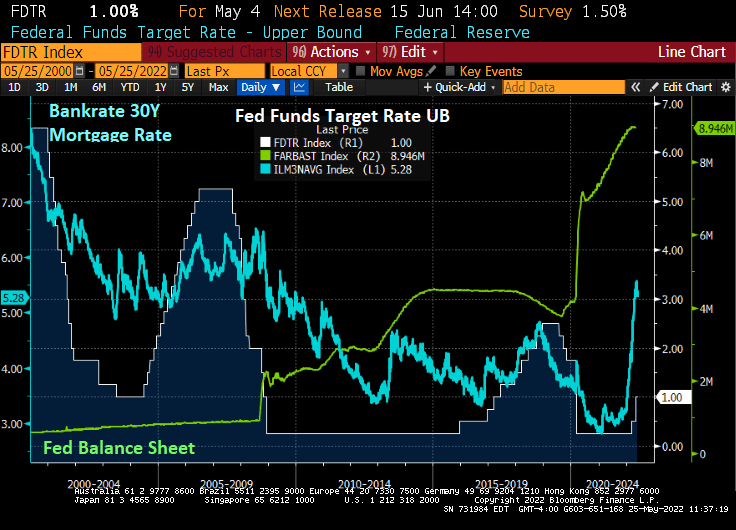

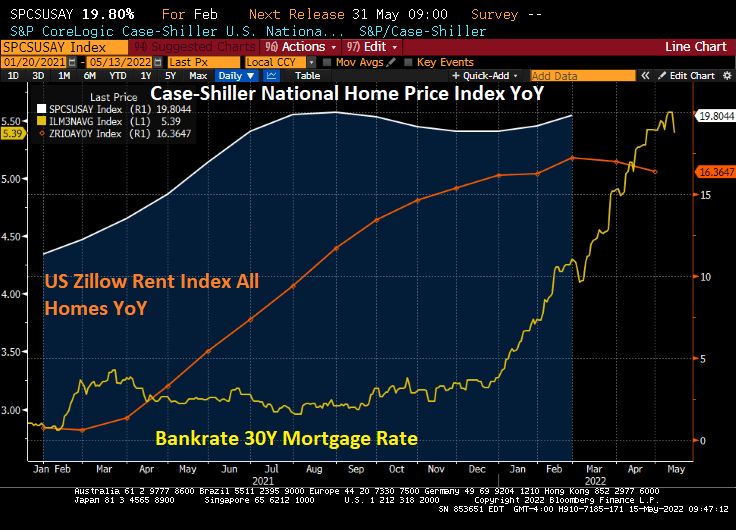

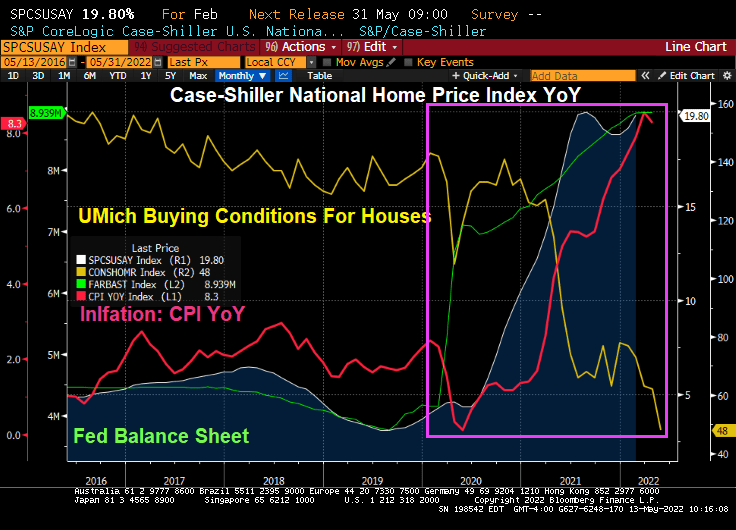

The reason why home prices are still raging at 17.3% YoY? The Fed’s monetary stimulypto is STILL in place! The Fed’s balance sheet (green line) is still staggering, and The Fed Funds target rate (white line) is a measly 1%.

Atlanta Fed President Raphael Bostic is talking about a pause in Fed tightening. Which they haven’t paused yet.

Fed Chair Jerome Powell is really “slowhand,” not Eric Clapton. Bostic is now a member of The Fed’s “Slowhand” strategy.

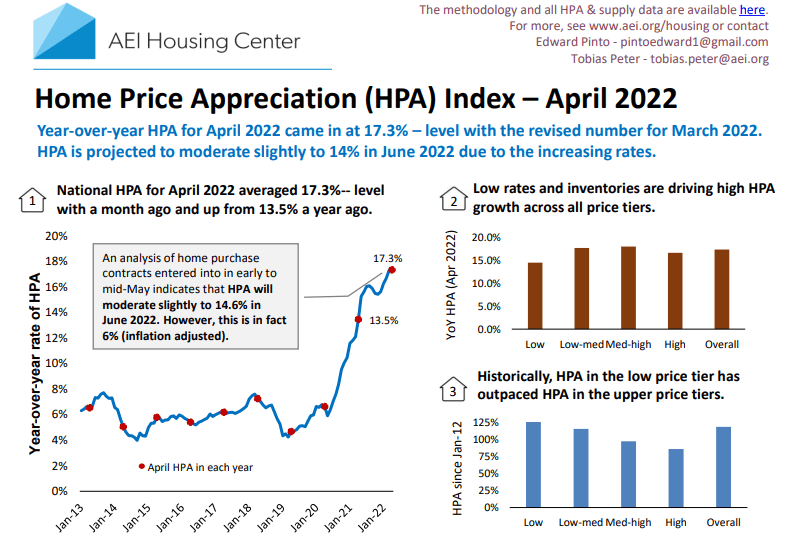

US home prices were growing at a near 20% YoY rate for the latest Case-Shiller National home price index report. But mortgage rates have soaring like a SpaceX missile shot.

Of course, I am moving to one of the metro areas in the USA where closed sales fell only -1.10% YoY in April: Columbus Ohio. I should move to San Diego CA where closed sales fell -21.4% YoY.

Of course, the US still suffers from lack of available inventory for sale.

April new listings are down -5.7% YoY. Columbus Ohio didn’t change from April ’21. San Diego is down -18.4% YoY for new listings.

Rising mortgage rates? Inflation? What a total fiasco.

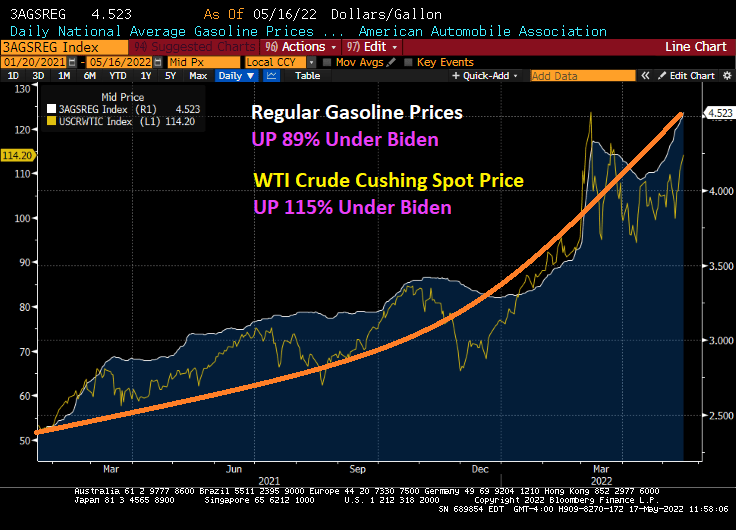

Mortgage rates have increased dramatically under “Middle Class Joe” as The Federal Reserve attempts to choke-off inflation caused by … The Fed coupled with Biden’s energy policies (hope you are enjoying those high gasoline and diesel prices!) and the Federal government’s staggering spending spree under Pelosi, Schumer and McConnell.

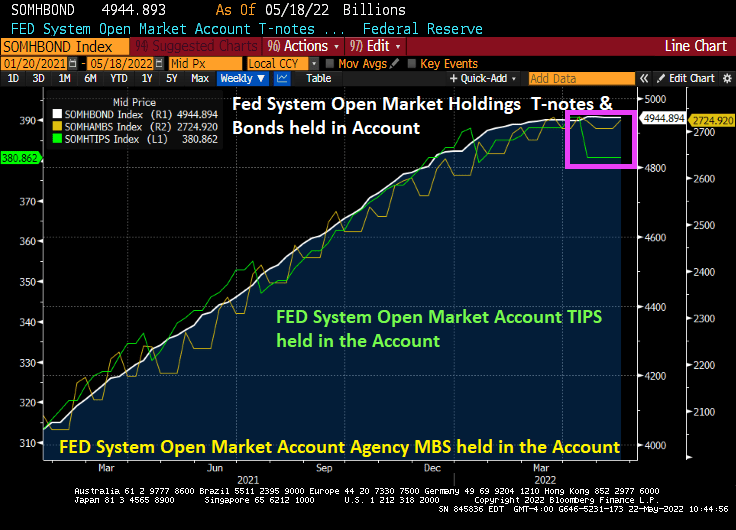

Thus far, The Federal Reserve has leveled-out out their Treasury Note and Bond purchases, increased their Agency Mortgage-backed Securities (AgMBS) holdings, but strangely have reduced their holding of Treasury Inflation-Protected Securities (TIPS) in the face of rising inflation.

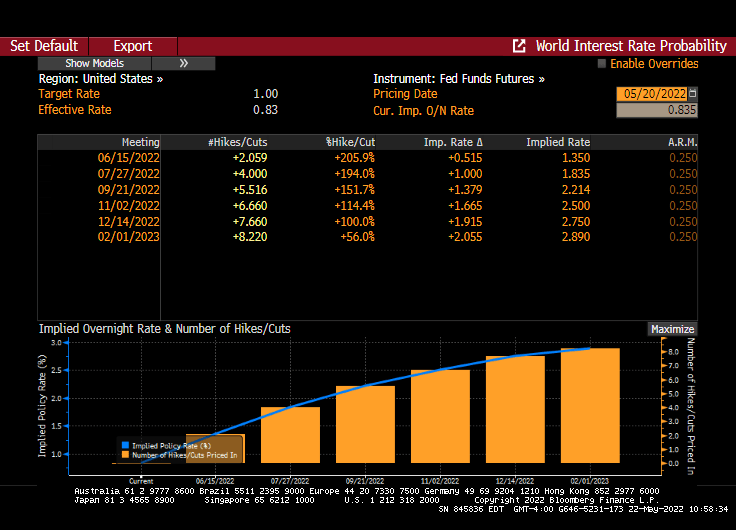

And while The Fed Funds Target rate is a lowly 1%, it is projected to rise to 2.890% by the February 1, 2023 FOMC meeting. That should send mortgage rates up.

As if mortgage rates haven’t skyrocketed already, thanks to The Fed’s jawboning about having to raise rates and extinguish inflation.

With sizzling mortgage rates (cooling a bit as the global economy slows), home mortgage payments have risen +43.4% YoY.

Now we have President Biden trying to scare us about the Monkey Pox, yet leaves the southern border wide open. One would think that Biden would shut the borders (as if the surge in Fentanyl, sex trafficking and other diseases aren’t reason enough. But I do predict another massive spending bill from Biden/Congress to combat Monkey Pox and the resurgence of Covid variants.

Meanwhile The Fed jawbones fighting inflation with monetary tightening in the future, even if they jawboning causes mortgage rates to soar and mortgage payments to spiral.

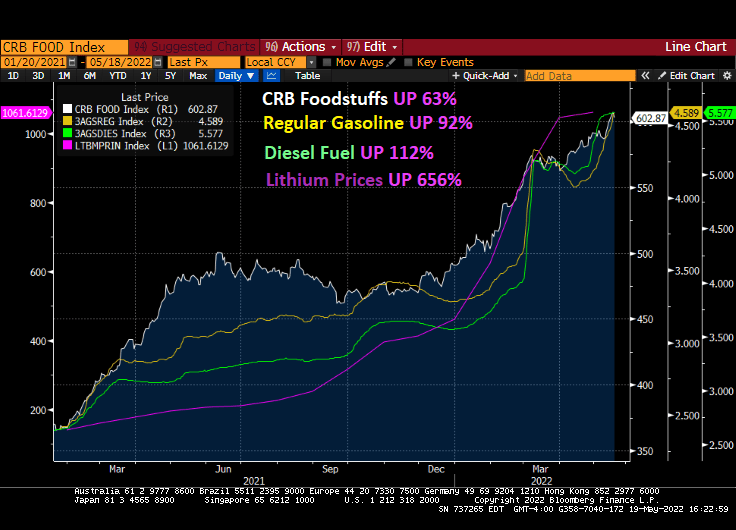

The inflation that is crushing Americans is due to energy and food price increases. That is, the non-core inflation. Under Biden, food is up 63%, gasoline is up 92% and diesel prices are up 112%. But The Fed doesn’t consider food and energy prices, per se.

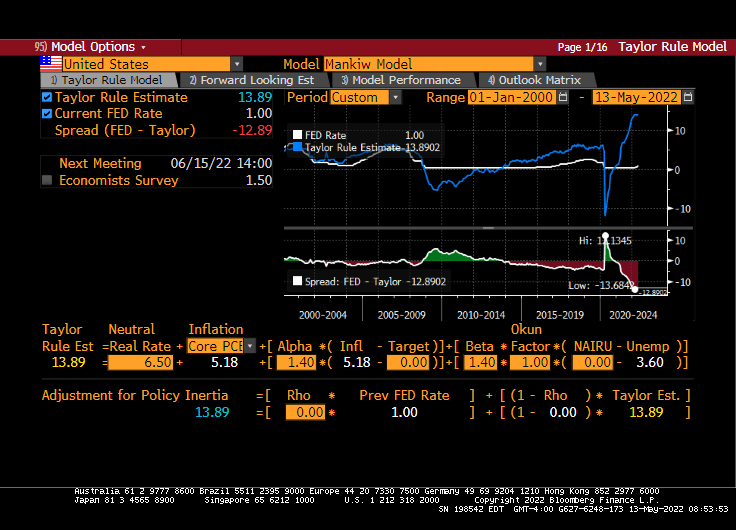

If we look at the Taylor Rule considering fighting inflation including food and energy, The Fed would have to raise their target rate to … 21.38%.

Now, The Fed can clearly cool-off the housing market by raising rates. In fact, my fear is that they go too far and crash the housing market. The Fed will NEVER get to 20% again like we last saw under Volcker in 1981. 20% rates certainly cooled home prices back then and Fed rate hikes helped crash the housing market in 2008.

So, when The Fed says they want to be the inflation-fightin’ Fed, we must be aware what The Fed can and cannot do. They can’t tame the inflation beast in the form of food and energy prices (unless they crash the economy), but they can crush home prices.

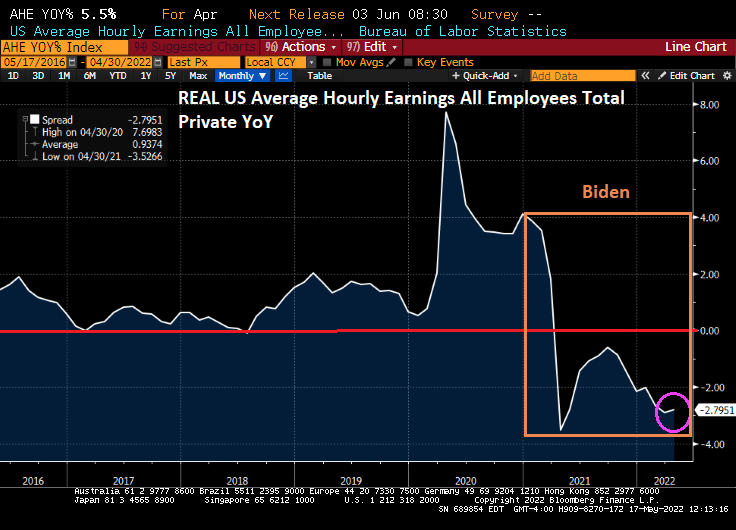

Seriously, with soaring energy prices and soaring EVERYTHING prices (except for real wage growth), it is difficult to see how the US will avoid a recession.

Yes, everything is seemingly rising in price, yet REAL average hourly earnings growth keeps falling. Rising price + declining real earnings growth = eventual recession.

Goldman Sachs Senior Chairman Lloyd Blankfein urged companies and consumers to gird for a US recession, saying it’s a “very, very high risk.”

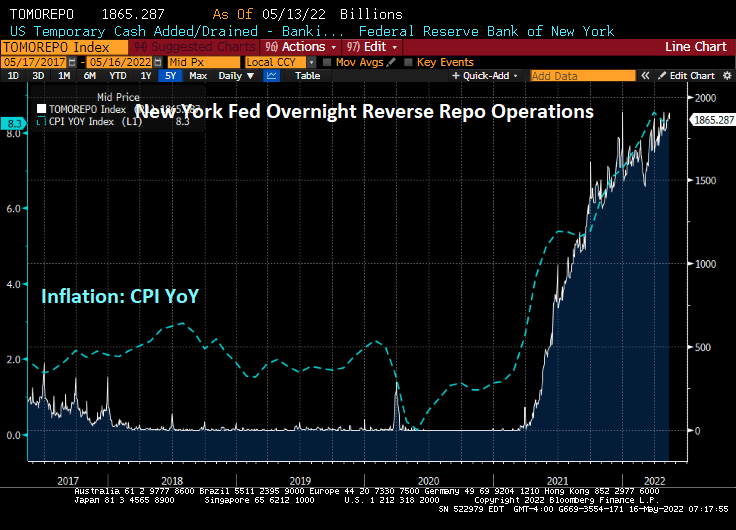

I am not surprised. Take a look at The Fed’s Overnight Reverse Repo operations. As inflation surged in 2021 and 2022, banks are parking more funds at The Fed. Fear?

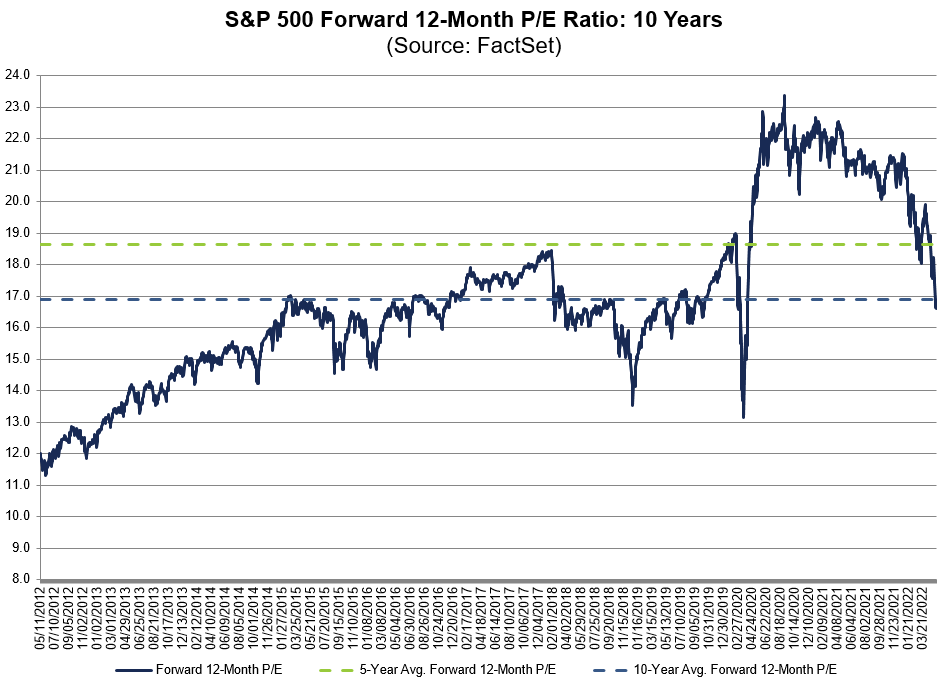

We are seeing the S&P 500 futures down today after a nice rally on Friday. The &P 500 forward 12-month P/E ratio is back to pre-Covid, pre Federal spending surge, pre Fed monetary Stimulypto of 2016.

Goldman Sachs see the 10-year Treasury yield rising to 3.3%. That bodes ill for 30-year mortgage rates, perhaps push mortgage rates up another 40 basis points to 5.80%.

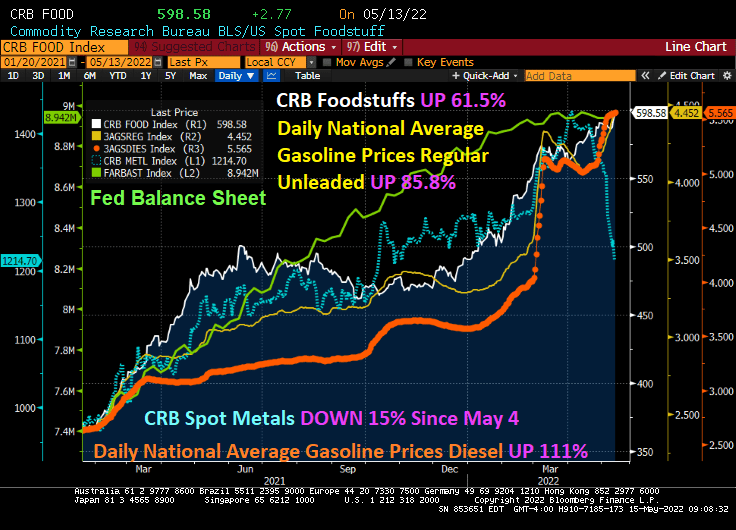

Foodstuff are up 61.5% under Biden’s Reign of Error. Gasoline prices are up 85.8%, diesel prices are up 111%. Yet the government inflation index (aka, CPI) is up only 8.3% in April.

But while energy and food prices are soaring, the CRB Spot Metals Index has plummeted -15% since May 4 as Covid is ravaging the Chinese economy. Recession alter anyone?

And then we have soaring home prices and rents. But notice that Zillow’s Rent index is slowing down as mortgage rates soar.

We have a stalling Chinese market, down 28% since October. Is Biden President of China??

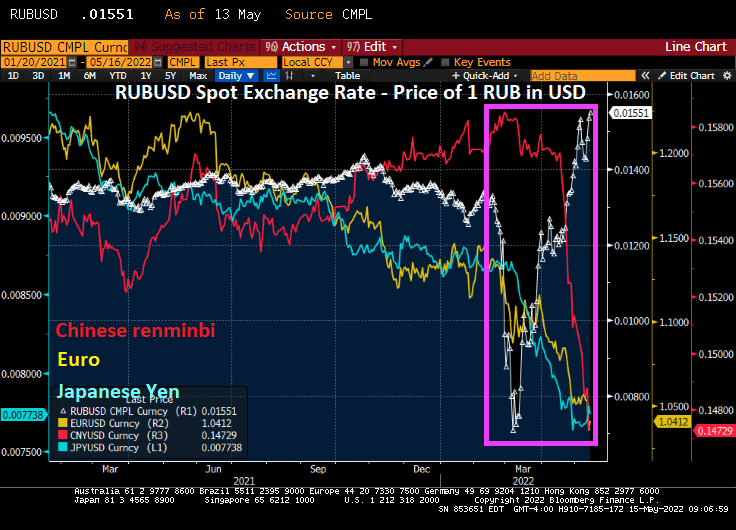

On the currency front, the Russian Ruble is soaring relative to the US Dollar while the Chinese Renminbi, the Japanese Yen and the Euro (or in this case, the Gyro) are sinking like a rock.

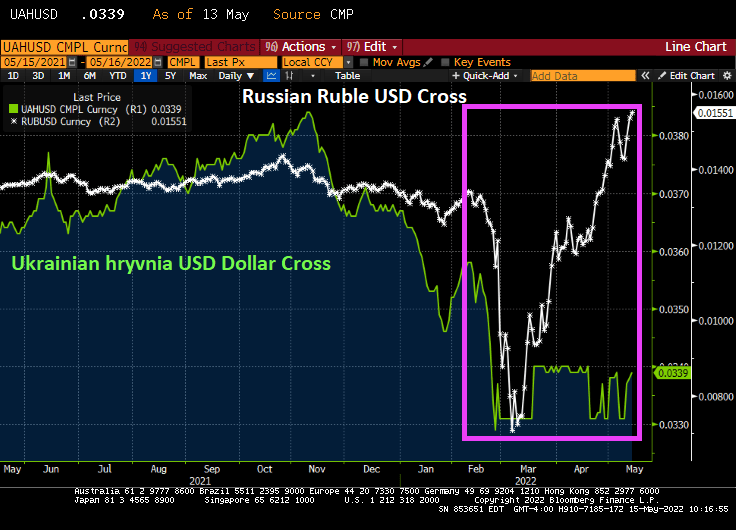

If I compare the Russian Ruble and Ukrainian Hryvnia, you can see Ukraine is losing the currency war with Russia.

Inflation Inferno thanks to Biden’s misguided energy executive orders and cancellation of Alaskan and Gulf of Mexico drilling leases.

Biden’s economic mismanagement team: American Gothics Treasury Secretary Janet Yellen and Fed Chair Jay Powell.

Nothing has been the same since Covid and The Federal Reserve’s massive overreaction to the government shutdowns of the economy.

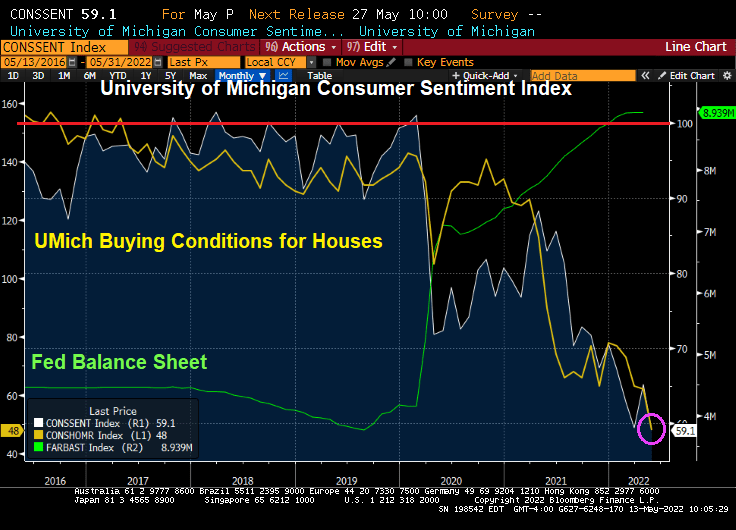

Notice how the University of Michigan Consumer Sentiment Index (white line) has plunged since Covid and the ensuing rise in inflation. University of Michigan’s Buying Conditions for Houses has also plunged to new depths.

Rising inflation (highest in 40 years) and hottest home price bubble (even hotter than the infamous housing bubble of 2005-2007) AND rising mortgage rates have placed a damper on home buying sentiment.

The US Senate yesterday confirmed the reappointment of Jerome “Slowhand” Powell as Federal Reserve Chairman.

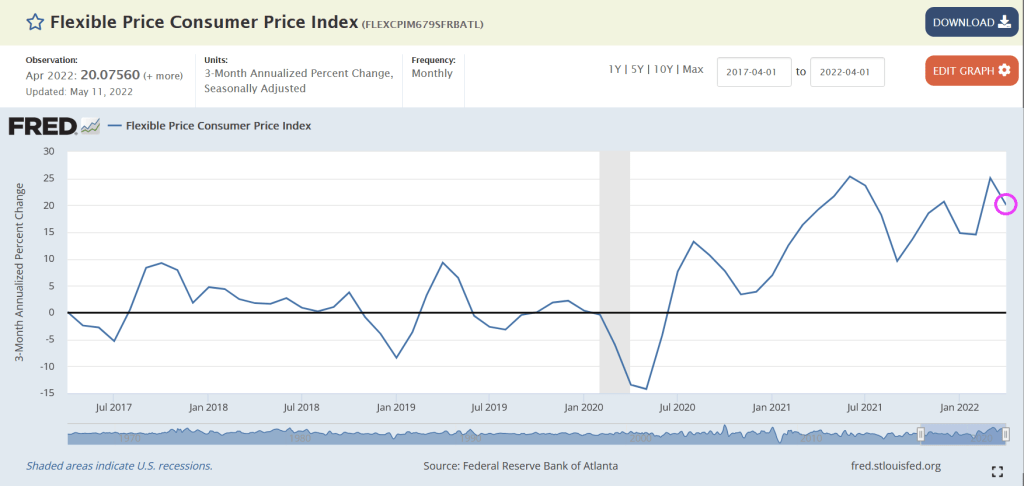

The good news? Atlanta Fed’s Flexible CPI YoY cooled to 20% in April. The bad news? Flexible prices are still growing at 20% while wages are growing at 5.5% YoY.

On the export front, export prices are cooling and were at 18% YoY in April, down slightly from March. Import prices cooled to 12% YoY as The Federal Reserve has slowed asset purchases.

I would have preferred President Biden appoint a serious Federal Reserve Chairman liked Stanford University’s John Taylor (of Taylor Rule fame). In his honor, here is the Mankin version of the Taylor Rule which calls for a Fed Funds Target Rate of 13.89% while the current Fed Funds Target Rate under Powell and the Gang is … 1%.

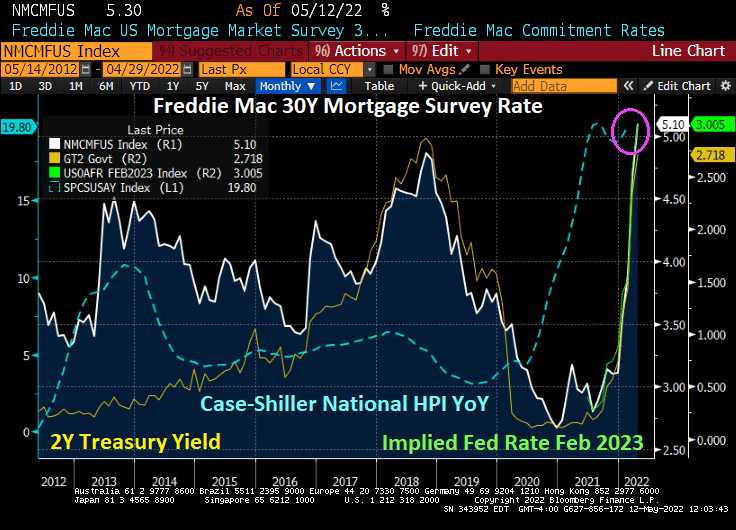

The Freddie Mac 30-year mortgage rate is rising faster than a SpaceX moonshot!

I’m telling your now that The Fed is killing the dreams of millions of Americans by pricing them out of the housing market. Home price growth is lethal as is the increase in mortgage rates.

You must be logged in to post a comment.