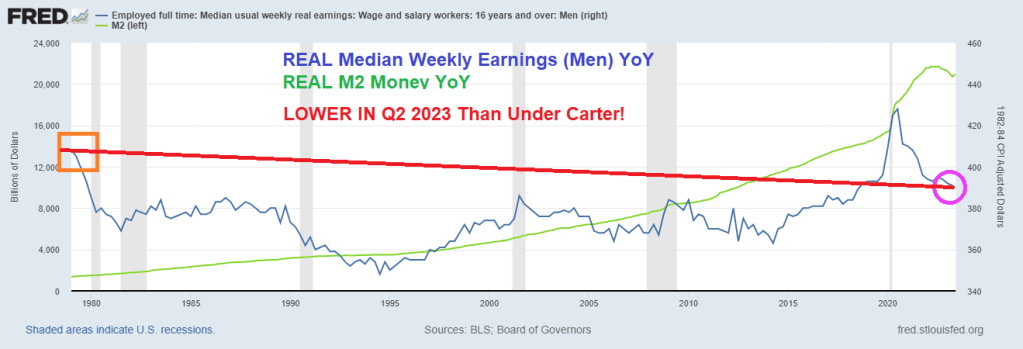

I wonder which season the US economy is in, according to President “Chance the Gardener” Biden.

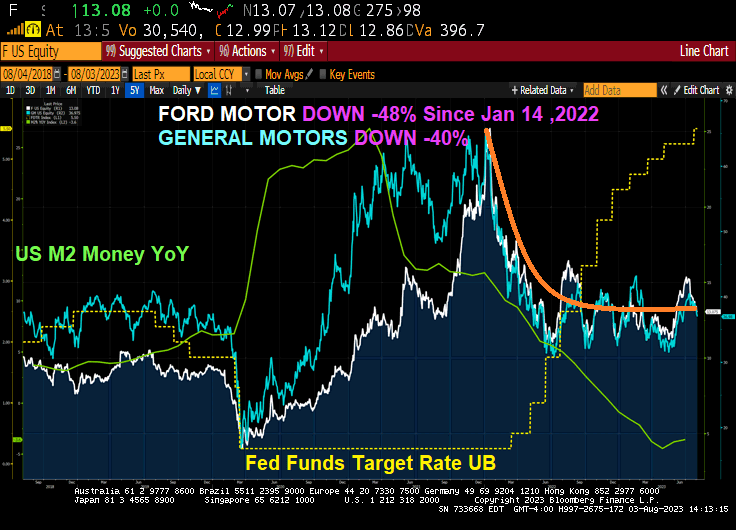

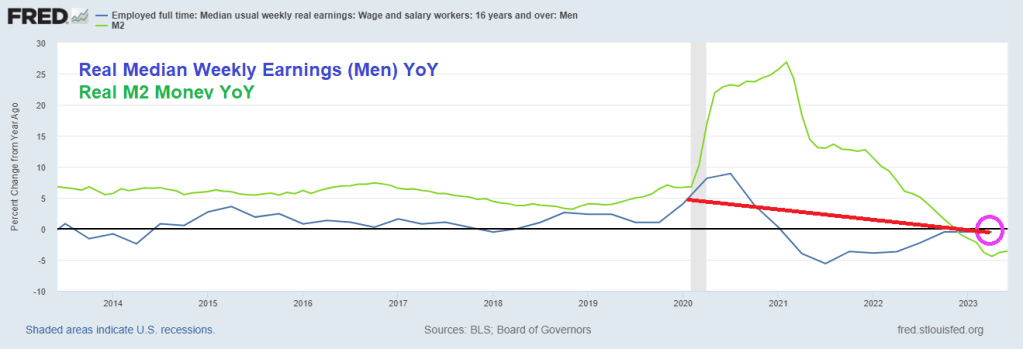

If you believe the recovery talk (from the reckless Covid economic and school shutdowns of 2020), all is well in the (economic) garden. For example, M2 Money Velocity (GDP/M2), is almost back to where it was just prior to the 2020 Covid outbreak and resulting government-caused recession. M2 Velocity was 1.425 in Q4 2019 and was 1.289 for Q2 2023. But ever since The Federal Reserve became hyper intervention in the economy (let’s just start with Bernanke’s massive intervention in late 2008 (red line) and the Fed balance sheet expansion), and it was increased dramatically during the Covid shutdown. And is STILL above $8 trillion!

Before Bernanke and the financial crisis of 2008-2009, M2 Money Velocity was above 2.0. But it has been below 2.0 ever since The Fed’s intervention in 2008.

On the energy front, US Energy Secretary Jennifer Granholm, whose catastrophic handling of US energy policy will be one of the most memorable and dire consequences of the Biden era, engaged in multiple conversations with the Chinese government’s top energy official just days before the Biden administration announced it would tap the Strategic Petroleum Reserve (SPR) to combat high gas prices in 2021, the same China whose Hunter Biden-linked energy giant Unipec, which we previously learned had bought millions of barrels from the SPR release.

Granholm called China National Energy Administration Chairman Zhang Jianhua, a longstanding senior member of the Chinese Communist Party, for a half-hour one-on-one conversation on Nov. 21, 2021. Granholm’s calendar also shows an earlier phone call had been scheduled with Jianhua for Nov. 19 but a rep for the former Michigan governor said the first call never took place. Then, on Nov. 23, 2021, the White House announced a release of 50 million barrels of oil from the SPR, the largest release of its kind in U.S. history at the time.

According to Fox News, Granholm’s previously-undisclosed talks with China National Energy Administration Chairman Zhang Jianhua — revealed in internal Energy Department calendars obtained by Americans for Public Trust (APT) and shared with Fox News Digital — reveal that the Biden administration likely discussed its plans to release oil from the SPR with China before its public announcement in the US: yes, China’s Communist Party learned what Biden would be doing before the US did.

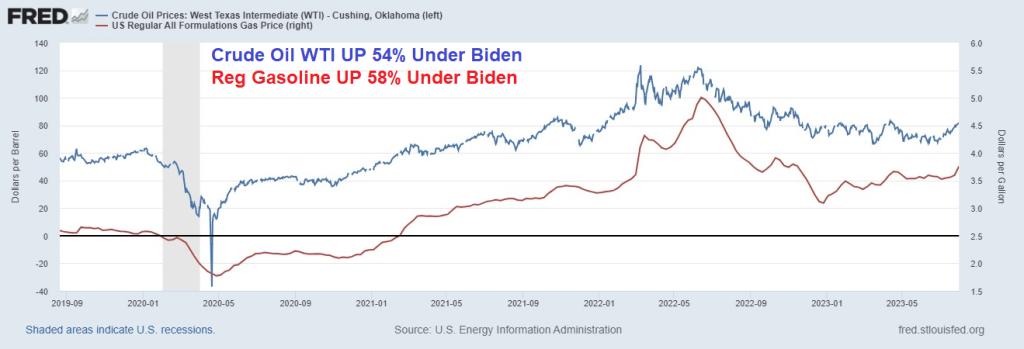

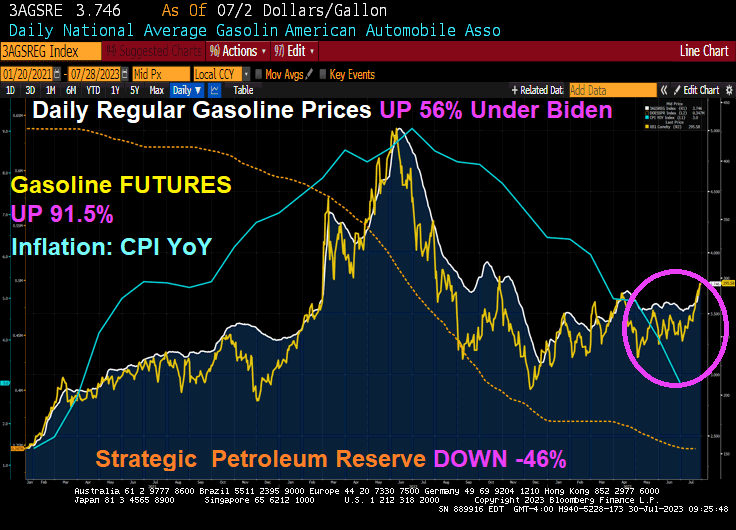

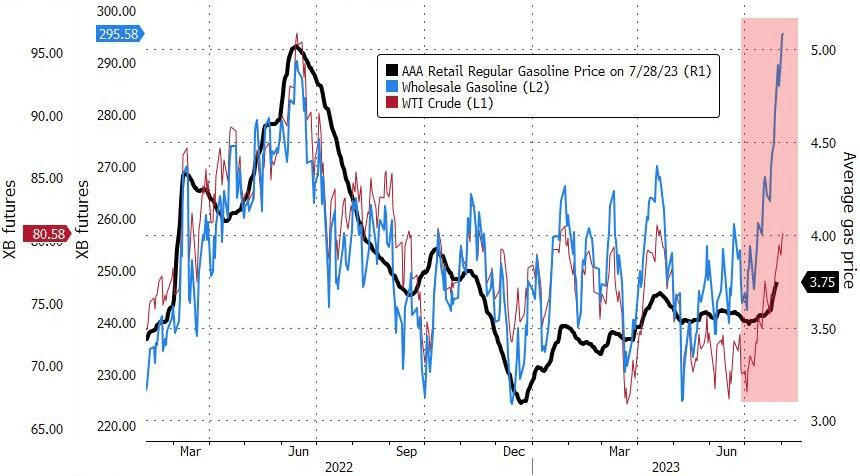

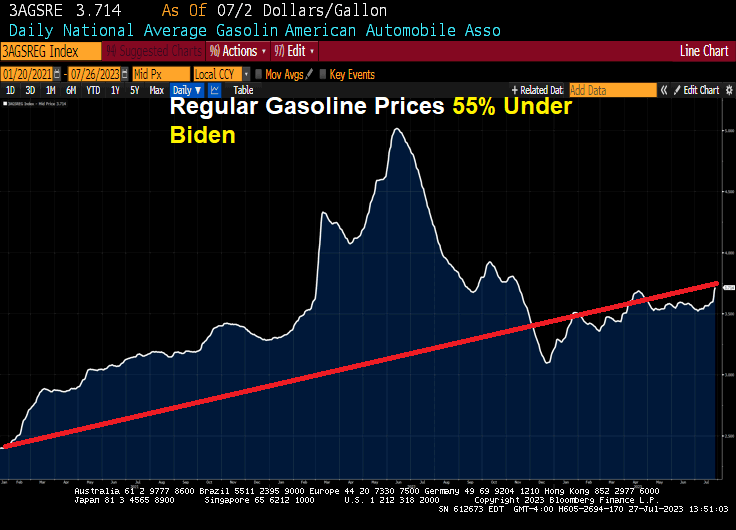

While Biden/Granholm are merrily draining the Strategic Petroleum Reserve, we see that West Texas Intermediate Crude Oil (Cushing) prices are up 54% under Biden and regular gasoline prices are up 58%.

All is sort of well in the garden because The Federal Reserve still has its massive interventionist foot on the gas pedal. Yet, America is on an economic suicide course with its green energy hype.

Frankly, Biden talks like Chance The Gardener from the film “Being There.” Except that Chance the Gardener is a nice person and Biden is reputed to have been the nastiest member of the US Senate. Not to mention the stupidest member of the US Senate. Although I don’t think Chance the Gardener would have taken millions in bribes from foreign countries like China and Ukraine.

Biden The Gardener should be Biden’s re-election slogan! Of course, Chance the Gardener could walk much better than Biden with his dementia shuffle. And Chance was a great gardener, all Biden knows how to do is sell the “Biden Brand” of political influece peddling to foreign countries.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

You must be logged in to post a comment.