Like the Mel Gibson movie “Apocalypto!”, we are seeing the US middle class and low-wage workers being economically sacrificed by The Federal Reserve, the Biden Administration and Congress.

Despite the rhetoric that Fed stimulus (aka “Stimulypto!”) is being removed, the US remains plagued by NEGATIVE real 10-year Treasury yields, NEGATIVE real Fed Funds Target rate and NEGATIVE real average hourly earnings growth under Inflation Joe.

This chart demonstrates the Stimulytpo problem. Prior to Covid, US wage growth was consistently higher than headline inflation. But starting in March 2021, three months after Biden became President, headline inflation became higher than wage growth.

Even with all these negative REAL rates, the US economy is forecast to have almost no growth in 2023.

To quote Peggy Lee, Is That All There Is? Trillions in Federal spending and Fed monetary stimulus and all we get it 0.50% Real GDP??

One of the great ironies of the Sam Bankman-Fried debacle is that while SBF was a generous donor to Democrats (and a few RINOs) and President Biden, it was Biden’s green energy policies that were part of the nail in SBF’s crypto empire. As inflation exploded upon Biden taking office (and massive overspending by Congress), The Federal Reserve jumped in to cool inflation leading to the downfall of cryptos in terms of price.

M2 Money YoY (green line) shows the massive growth money with the Covid economic shutdowns in 2020. Cryptos skyrocketed after that much money was printed by The Fed. Cryptos fell shortly after peaking in April/May 2021, then peaked again in a horrific display of asset volatility in October/November 2021.

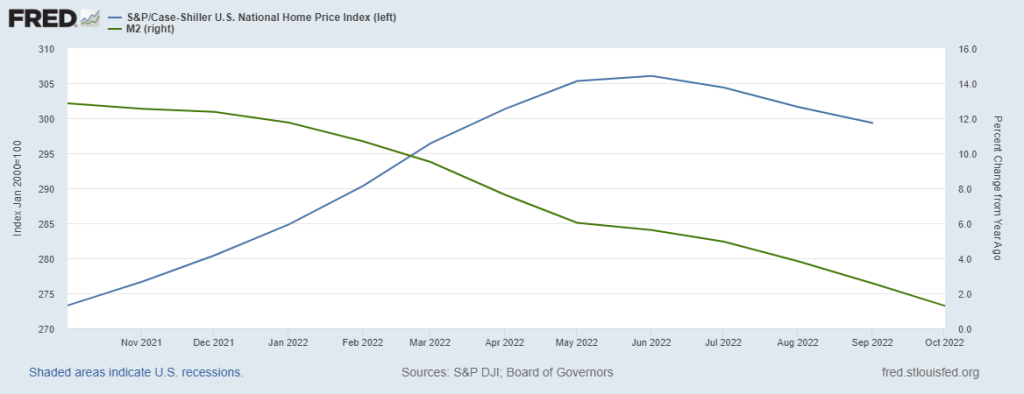

What happened in late 2021 to crush cryptos? Ah, expectations of Fed rate increases (red line) started to soar meaning the punchbowl for cryptos was being taken away. The Fed giveth and The Fed taketh away.

The risk management question is … how did SBF and Alameda Research’s Caroline Ellison didn’t notice the relationshop between crypto prices and changing Federal Reserve monetary policy? Even worse, why didn’t investors ask questions??

Take a gander at Bitcoin relative to US diesel fuel prices (orange line) and The Fed’s inflation counterattack (red line). Sam and Sweet Caroline (who was seen walking free in NYC) must not have been monitoring how rapidly rising diesel prices would permeate the entire economy in terms of price increases. M2 Money YoY (green line) has been declining as the expectations of Fed rate tightening (red line) has increased.

SBF donated a huge amount to the midterm elections, the party that went along with Biden’s war on fossil fuels. Then inflation ensued as energy and food prices skyrocketed, leading The Federal Reserve to fight inflation by removing the monetary punchbowl. So, in a sense, SBF donations led to his own collapse.

Apparently, SBF, Caroline Ellison and the other FTXers were engaged in orgies and not paying attention to the impact of inflation and Fed policies on cryptos.

Lastly, how did Gary Genslar and the SEC not see any of this? In the same way that Fed Chair Ben Bernanke didn’t see the financial crisis as it was rapidly unfolding: eyes wide shut.

I read that Nicole Kidman underwent psychiatric treatment after filming “Eyes Wide Shut.” I saw it and was bored out of my mind.

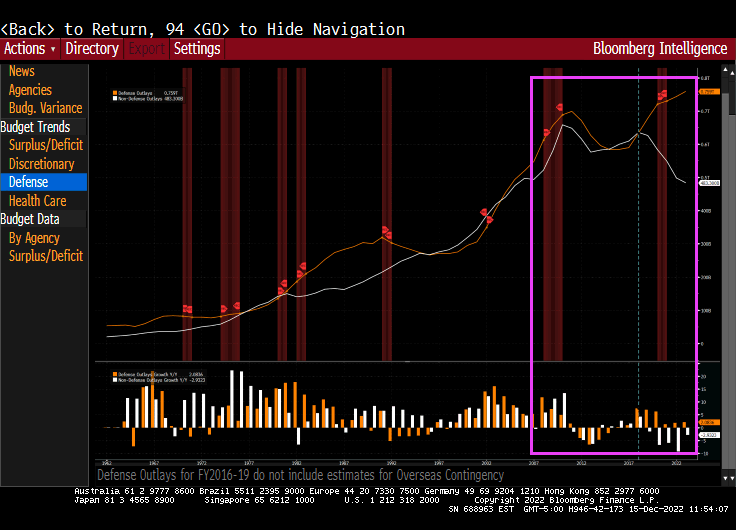

Nancy Pelosi is passing her gavel to someone else (most likely McCarthy R-CA), but her legacy like that of fellow spendaholic John Boeher (RINO-Ohio) and Paul Rino (RINO-WI) is reckless spending and debt load.

Since 2007 when Pelosi took the gavel as Speaker of the US House, Federal debt has risen from $5.8 trillion in Q4 2006 to $31.4 trillion today, an increase of over 250%. Pelosi’s spending spree was continued by RINOs Boehner and Ryan before SanFranNac retook the gavel and continued Congress’ spend-a-holic ways.

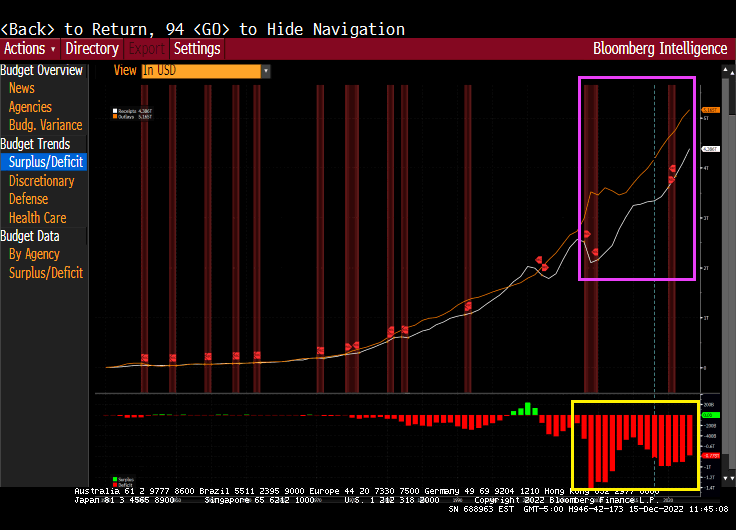

Nothing has been the same since the financial crisis and Pelosi became Speaker in 2007. Notable is the wild spending with the gap between spending and tax revenue soaring.

Since 2007 and SanFranNan, Medicare spending has exploded along with Medicaid.

Under peace-loving Pelosi, defense spending has exploded.

And then we have unfunded liabilites from the Federal government at a staggering $173.3 trillion, which is 452% of Federal debt. What did Pelosi (or Boehner/Ryan) do to fix this problem? Nothing. She kept spending like crazy.

It would be nice if Biden told every illegal immigrant that on becoming a citizen, you owe $519,286 in terms of unfunded liabilities and a $94,240 for their share of Federal debt. But, of course, that will never happen.

The S&P 500 index is down -2.44% today as M2 Money growth crashes.

The numbers coming out today are not good. November numbers were 1) US Industrial Production was down -0.2% MoM, 2) manufacturing production is down -0.6%, 3) retail sales advanced down -0.6% (most in 11 months) and …

The Empire State Manufacturing outlook was down -11.2% and the Philadelphia Fed (or Phed) business outlook was down -13.8% in November.

And with all this bad news, global equity markets are dropping like a paralyzed falcon.

But at least Biden traded a dangerous international arms dealer for WBNA star Brittney Griner. Possilby the worst trade in history after the Chicago Cubs traded future Hall of Famer Lou Brock for sore-arm pitcher Ernie Broglio. Griner is Ernie Broglio.

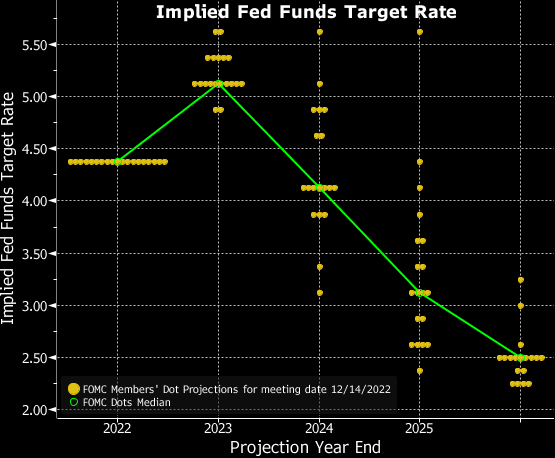

As expected, The Federal Reserve raised their target rate by 50 basis points to 4.50%, the highest Fed target rate since November 2007.

The only thing interesting that happened was Powell’s hawkish statements about The Fed wanting to keep tightening to fight inflation caused under “Inflation Joe” Biden.

But the NEW Fed Dots plot looks like an Olympic Ski jump with expectations of DECLINING Fed target rates.

My take on the steeply downward sloping Dot Plot is a tacit acknowledgement that a recession is headed our way in 2023.

Here is the Lillehammer Olympic ski jump that resembles today’s Fed Dots Plot.

Apparently, despite the denials from the Biden Administration, someone at Bureau of Labor Statistics or someone in Congress or the Federal Reserve or the Biden Admininstration itself likely tipped the wink on the soft CPI report on Tuesday.

Treasuries were well on the front-foot in the lead up to the below-estimate November CPO print, as a surge of buying took place seconds before the official 8:30 am New York release time. Over a 60 second period before the data, 13,518 March 10-year futures traded as the contract moved from 114-04+ up to 114-22. Gains were then extended up to 115-11 session highs once the data was released.

On the equity side, stock futures suddenly spiked more than 1%. Trading in Treasury futures surged, pushing benchmark yields lower by about 4 basis points. Those are major moves in such a short period of time — bigger than full-session swings on some days. And they should get scrutinized by regulators, long-time market observers say, even if a leak is only one of several possible explanations for why traders suddenly started buying right before the report was published.

Remember that current Treasury Secretary Janet Yellen was accused of leaking information to a NY hedge fund ahead of the Fed Open Market Committee meeting? And then we have the Wolf of Wall Street.

I wonder if the REAL Wolf of Wall Street did this?

Mortgage applications increased 3.2 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending December 9, 2022.

The Refinance Index increased 3 percent from the previous week and was 85 percent lower than the same week one year ago. The unadjusted Purchase Index decreased 1 percent compared with the previous week and was 38 percent lower than the same week one year ago.

You can see the impact of seasonalilty on mortgage purchase applications (white line). They peaked in the week of May 6, 2022 and have been generally declining since. While refi applications (orange line) increased over the past week, they have been pummelled by The Fed tightening.

It is quiet today as investors wait for The Fed to announce a 50 basis point rate increase. Fed Funds Futures point to almost another 100 basis point hike by May 5, 2023, then a slow decline in The Fed Funds target rate (upper bound).

And here is Sam Bankman-Fried and his high-powered legal defense.

In August 2020, the Federal Reserve unveiled its new strategic framework. One major objective of the Fed was to address its concerns over the potential consequences for the conduct of monetary policy when the policy rate was constrained by its effective lower bound. This article concludes that there are significant flaws in the new strategy and that it encourages a more discretionary approach to monetary policy and increases the risks of policy errors. The new framework is an overly complex and asymmetric flexible average inflation targeting scheme that introduces a significant inflationary bias into policy and expands the scope for discretion by broadening the Fed’s employment mandate to “maximum inclusive employment.” In a postscript, the article describes how quickly the flaws have been revealed and urges a reset toward a more systematic and coherent strategy that is transparent and broadly understood by the public.

I attended a speech by macoeconomist Gershon Mandelker at the National Association of Realtors where he called on the Federal Reserve to follow some observable rule rather than the complex (or seat of the pants) approach to monetary policy.

With today’s inflation report (core inflation YoY of 6%) results in a Taylor Rule estimate of The Fed Funds Target Rate of 12.07%. We are struggling to reach 5% as a “terminal” Fed target rate (currently at 4% and likely to rise 50 basis points at tomorrow’s Fed meeting).

The matrix of CPI and unemployment under the Taylor Rule shows that The Fed’s target rate isn’t at even 5% for any relevant combination of core CPI (inflation) and unemployment rate.

Note that since the financial crisis the Fed’s target rate (white line) has been consistely below the Taylor Rule implied rate (blue dashed line).

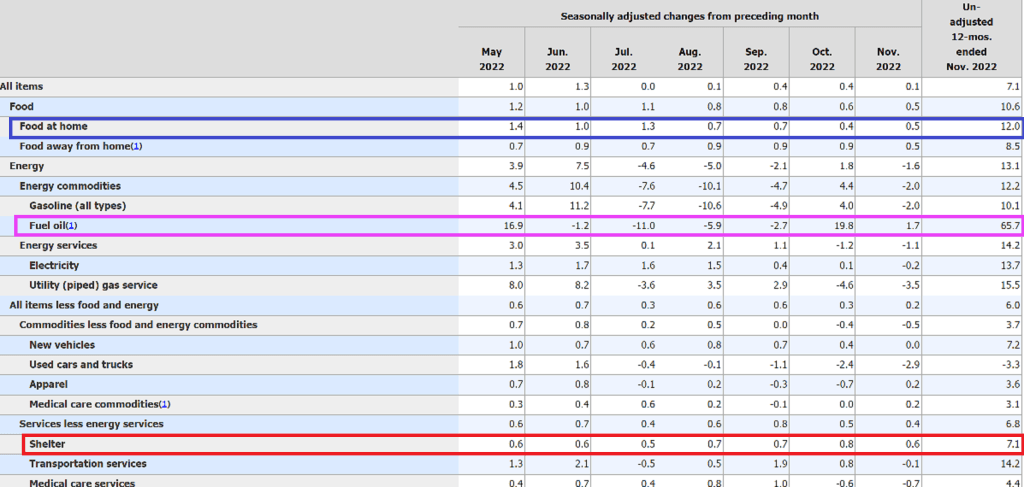

Is inflation “gone in November”? Nope. Slowing, yes, but at 7.1% YoY and core inflation at 6.0% YoY, it is still considerably higher than The Fed’s target of 2%.

And the American middle class and low wage workers are still suffering with REAL average hourly earnings growth at -1.9% YoY.

You must be logged in to post a comment.