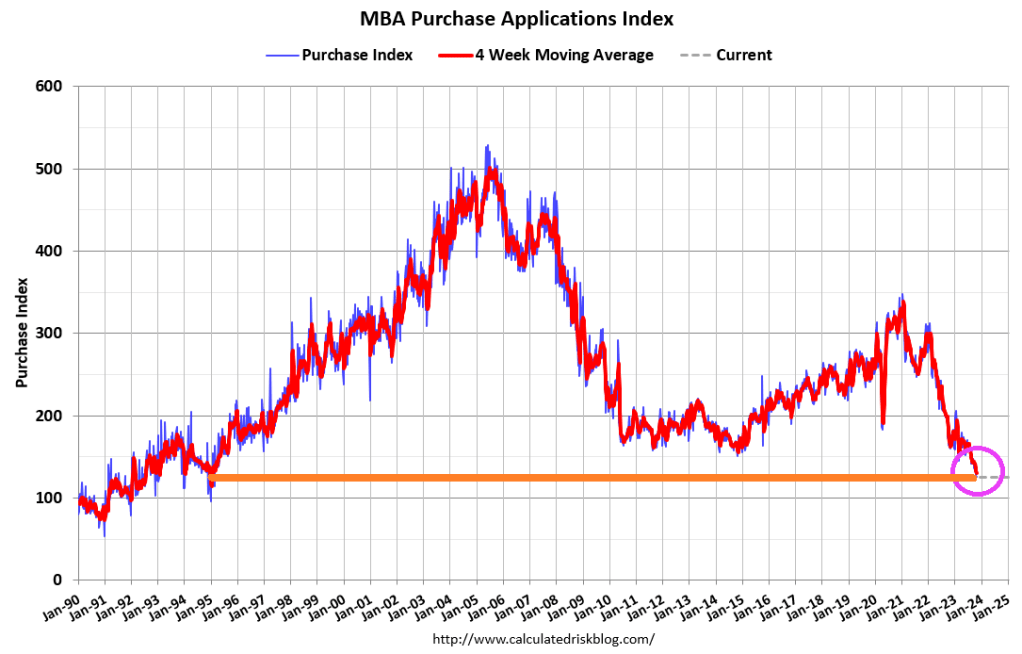

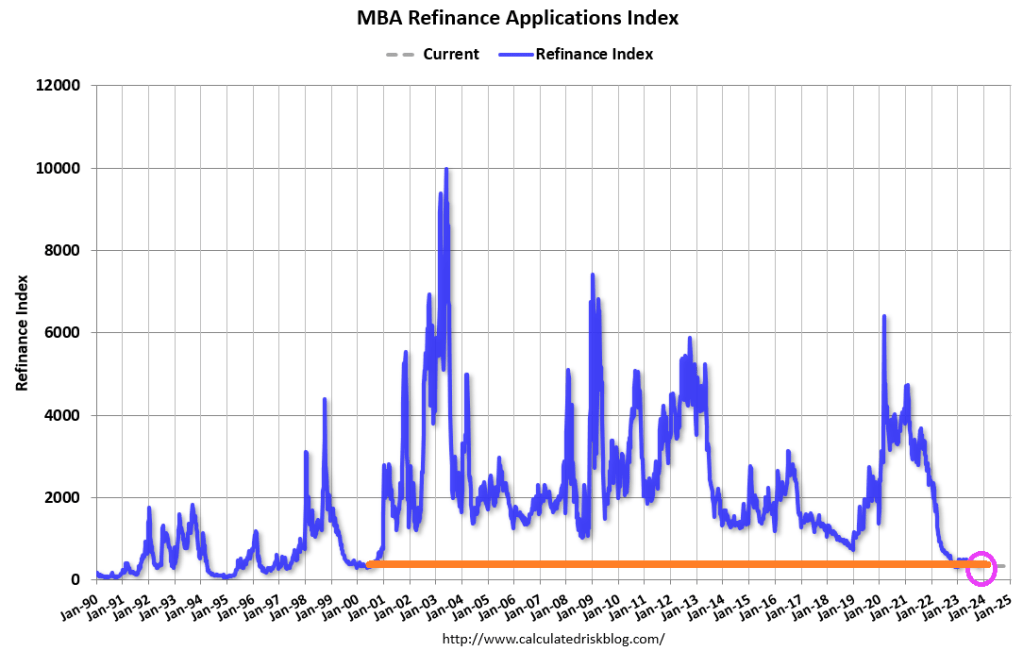

The Market Composite Index, a measure of mortgage loan application volume, decreased 2.1 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index decreased 3 percent compared with the previous week. The Refinance Index decreased 4 percent from the previous week and was 12 percent lower than the same week one year ago. The seasonally adjusted Purchase Index decreased 1 percent from one week earlier. The unadjusted Purchase Index decreased 2 percent compared with the previous week and was 22 percent lower than the same week one year ago. Back to 1995 levels.

At least mortgage refinancing applications are back to only 2001 levels.

Two-year yields have risen 5%.

At least it looks like Powell will pause rate hikes … for the moment.

I want a new drug, other than Biden’s top-down, big-donor friendly Soviet-style command economy. How about a free market without Fed interest rate manipulation??

Bidenomics is best represented by the novel “The Guns of August” since American’s middle class is getting blasted by Biden’s economic policies and The Fed’s rate rate hikes. Find out where Texas Governor Abbot is bussing illegal immigrants and buy in the market!!

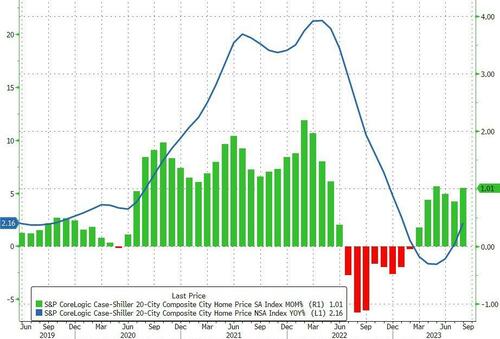

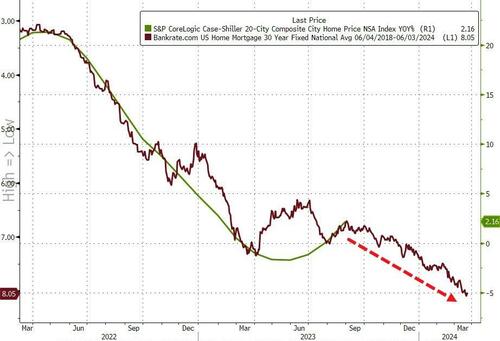

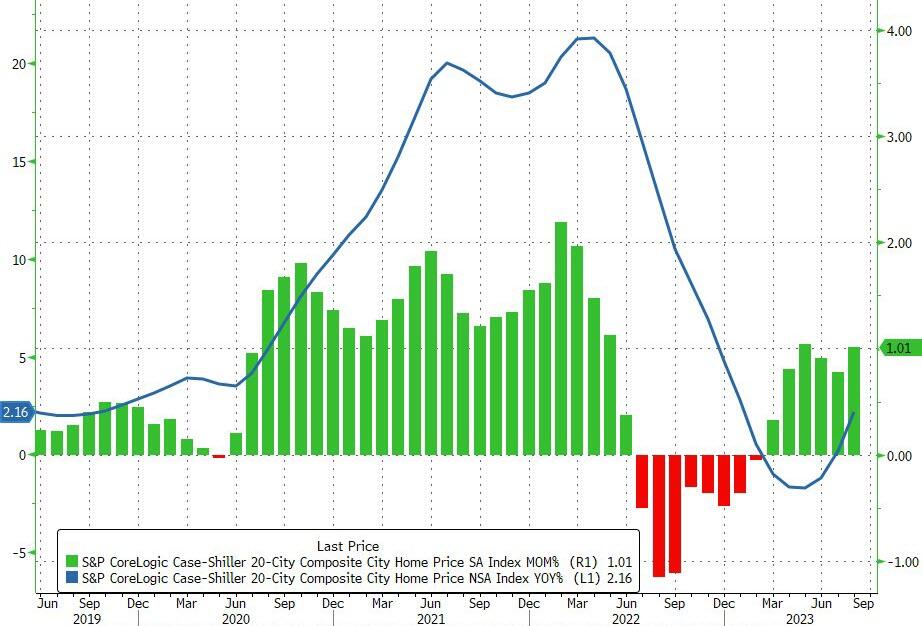

The ongoing MoM rises pushed the YoY gain in home prices at America’s 20 largest cities up 2.16%, the most since January 2023. The National Home Price index rose even faster at 2.57% YoY.

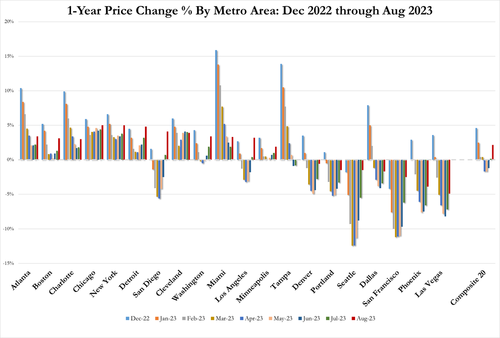

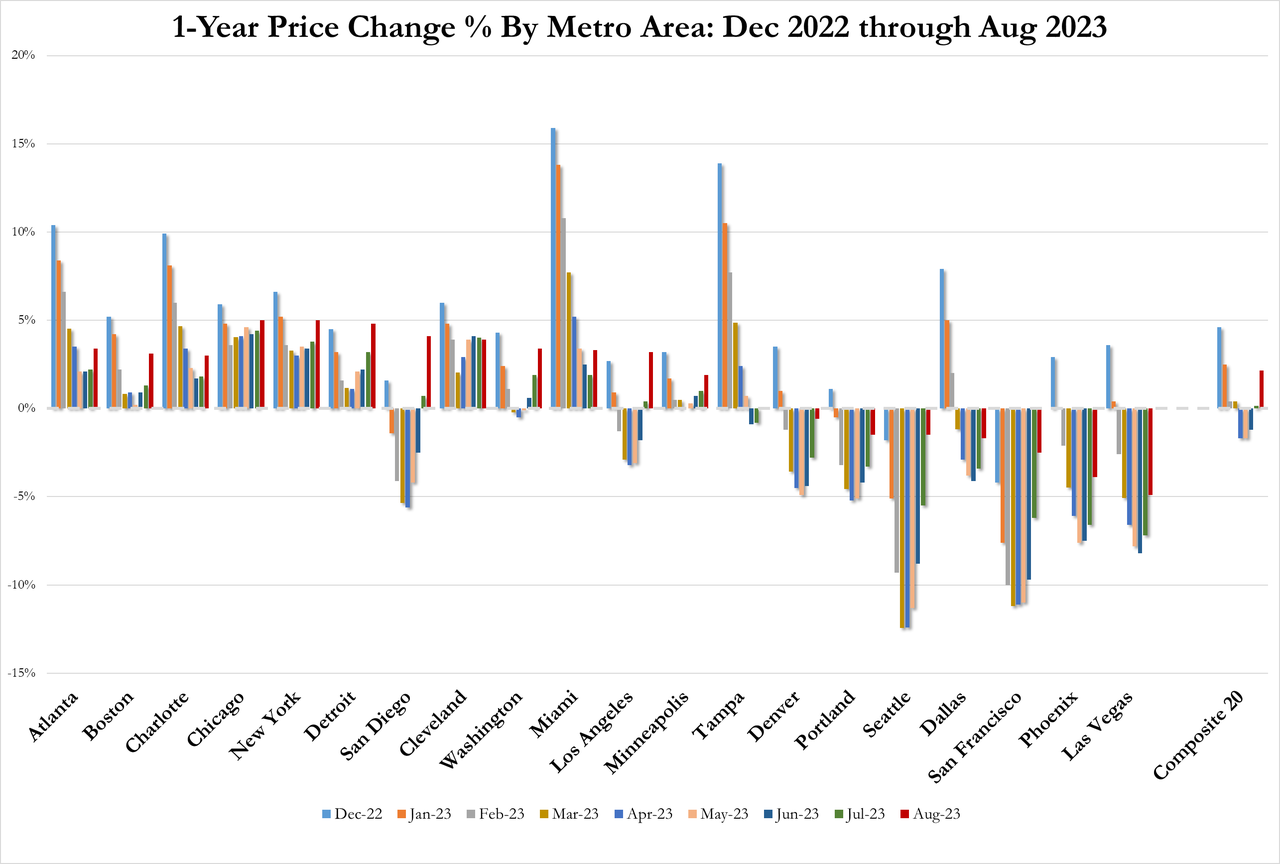

Illegal immigration destinations Chicago, New York, and Detroit all saw major home price rises (+5.0%, +4.9%, and +4.8% YoY respectively). Las Vegas, Phoenix, and San Francisco remain lower YoY (-4.9%, -3.9%, -2.5% respectively).

But, judging by the resumption of the rise of mortgage rates since the Case-Shiller data was created, we would expect prices to also resume their decline…

Source: Bloomberg

Inventory is going nowhere, buyers and sellers are stuck (affordability for the former and the mortgage cost gap for the latter), and The Fed isn’t cutting rates any time soon. Not pretty…

Ford EV sales are almost nonexistant. High prices, big losses per vehicle sold, a dearth of charging stations for travel.

At least Biden will say the pain he is causing actually “hurts so good.”

Here is California governor and greaseball Gavin “Gruesome” Newsom test driving a Chinese EV on his trip to China to undercut Biden’s dying reelection prospects.

The benchmark small cap index, the Russell 2000, has hit the lowest levels since November 2020, when the world was still without a vaccine and shut down from Covid. And before Biden’s/Congress wild spending spree and debt volume explosion creating massive inflation causing The Fed to hike rates.

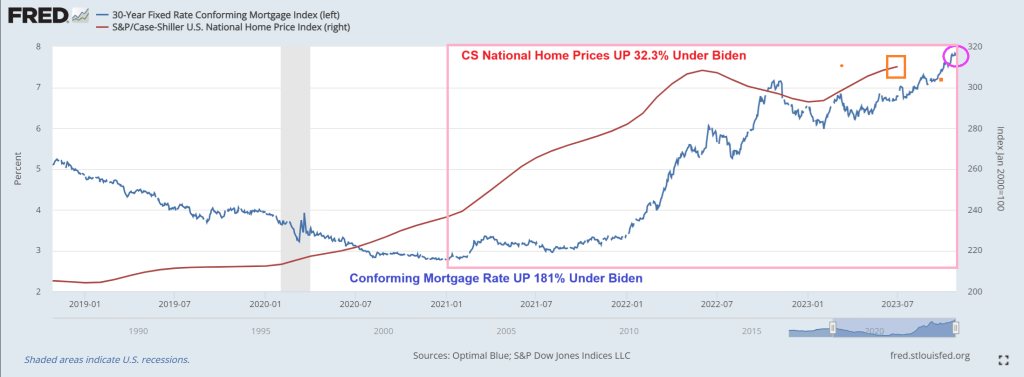

Speaking of over, under, sideways, down under Bidenomics, mortgage rates are up 181% and home prices are up 32.3% under Biden.

Bidenomics is a windfall for the donor class (high rate of return on campaign contributions) while the middle class gets beaten to a pulp. Waiting for Biden to lean over and creepily whisper “It’s working!” Even though it is clearly not working, at least for the middle class.

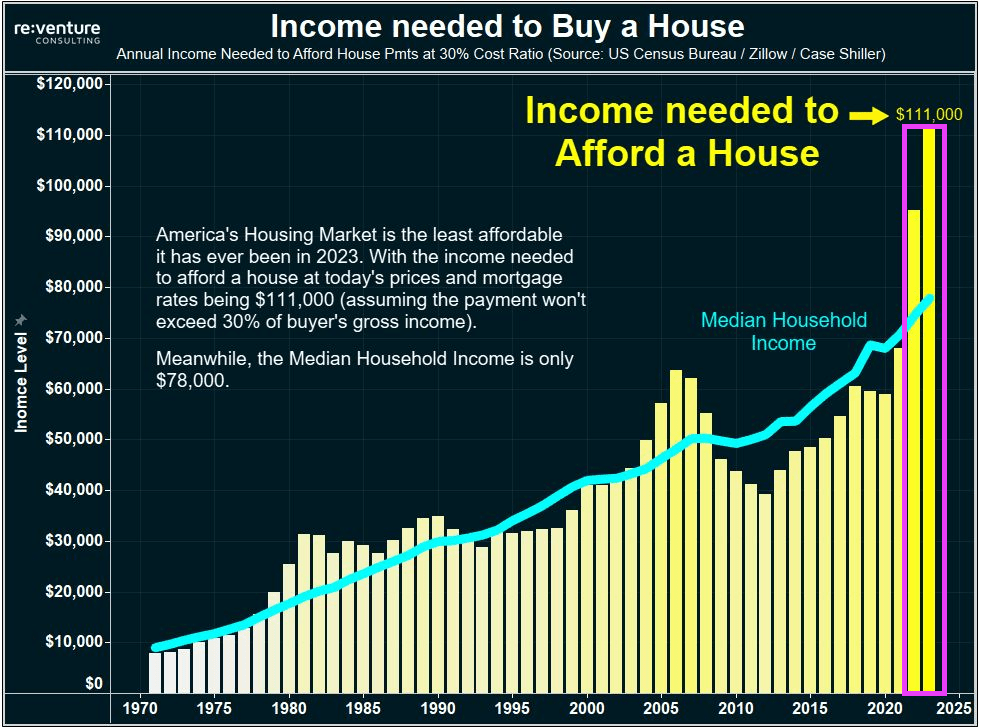

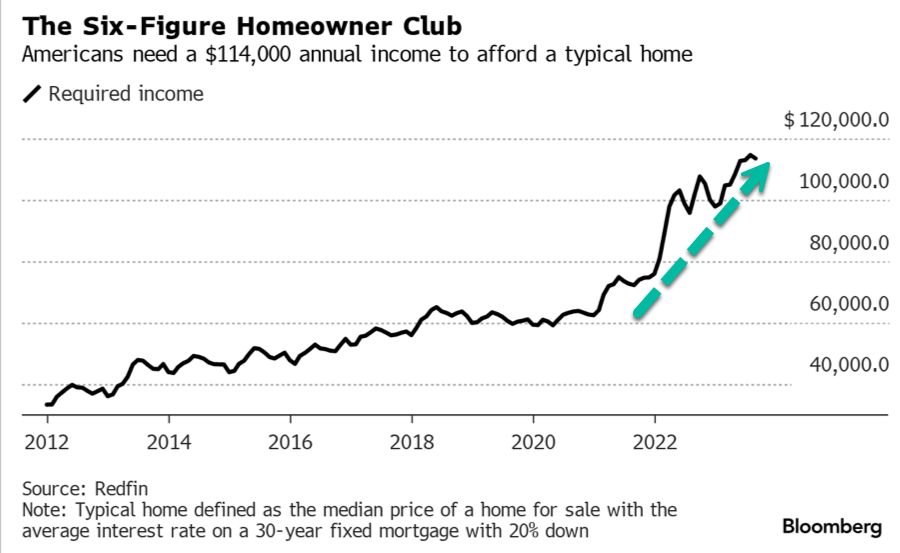

Evidence that Bidenomics is not working and destructive? Try the surging income needed to buy a house under Biden. Home prices are rising faster than median household income. As in $111,000 income needed to buy a house, while median household income is only $78,000. So, housing is simply unaffordable under Bidenomics. The Biden era is outlined in pink.

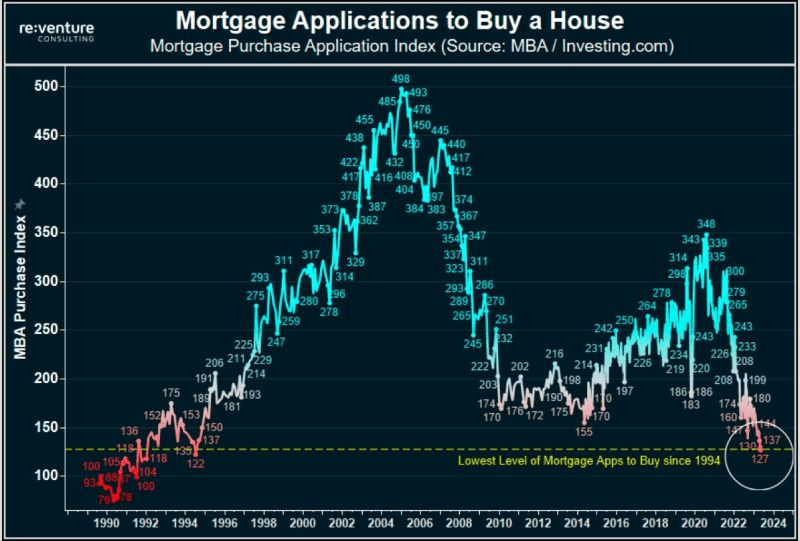

Mortgage purchase applications have collapsed to 1994 levels.

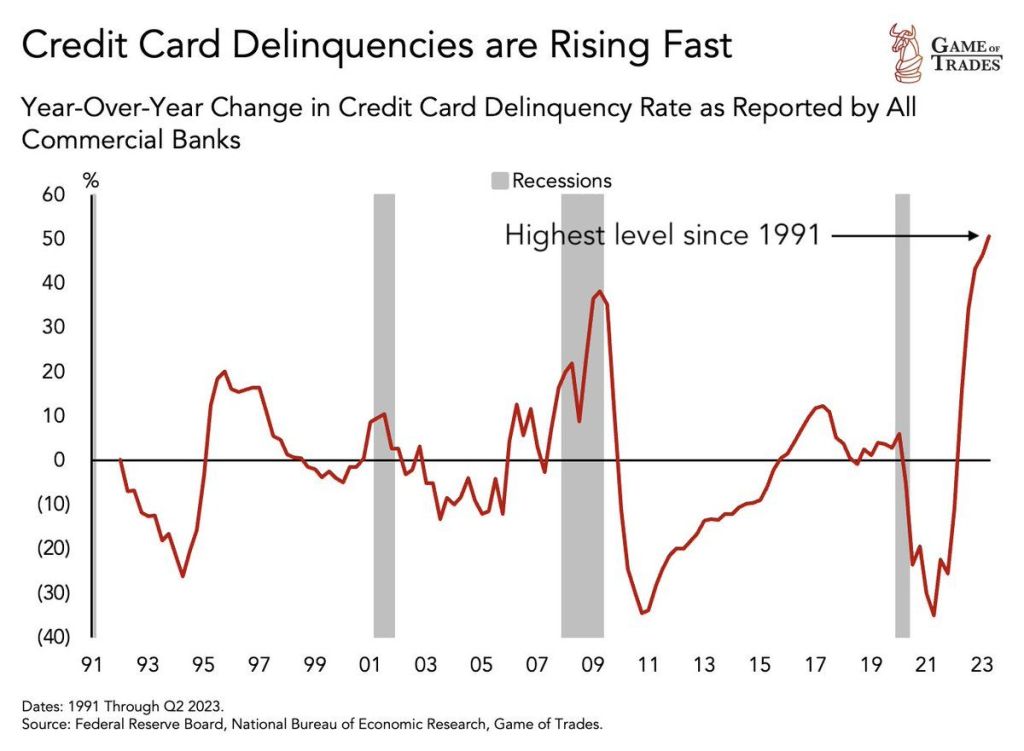

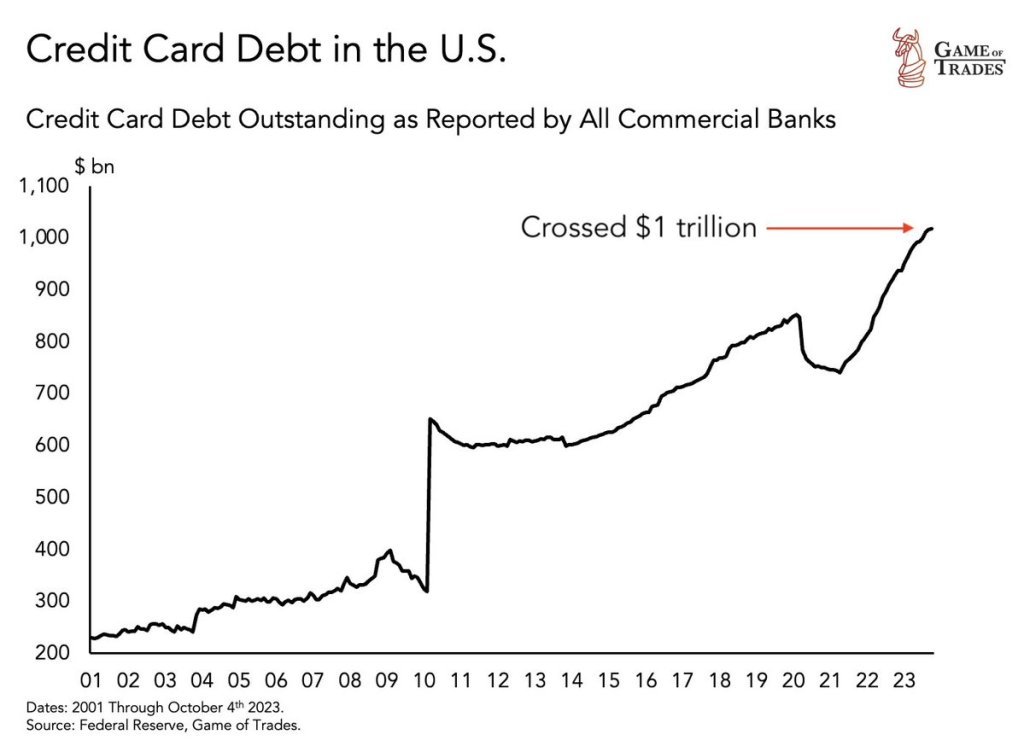

Meanwhile, stressed households are seeing credit card delinquencies at the highest level since 1991.

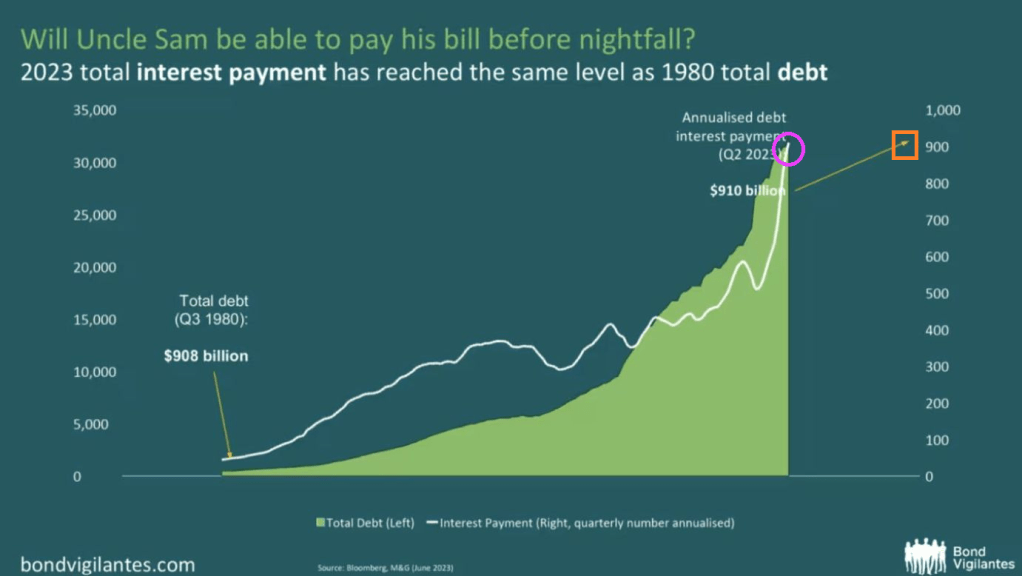

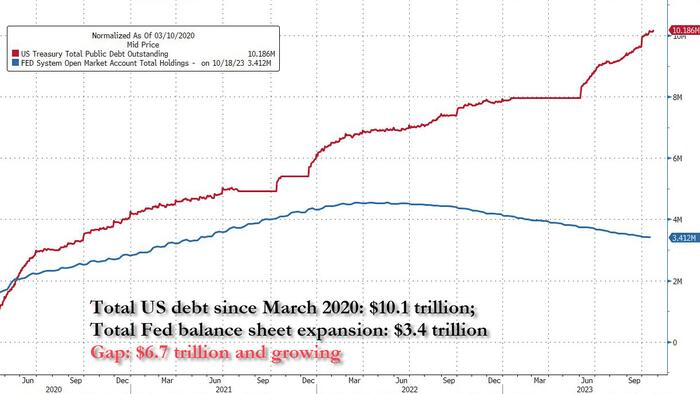

And thanks to Uncle Spam (given how Uncle Sam is destroying the middle class it is now Uncle Spam), 2023 interest payments are the same as the total debt from 1980! Spam, which the Federal government has devolved into, is very high in fat, calories and sodium and low in important nutrients, such as protein, vitamins and minerals.

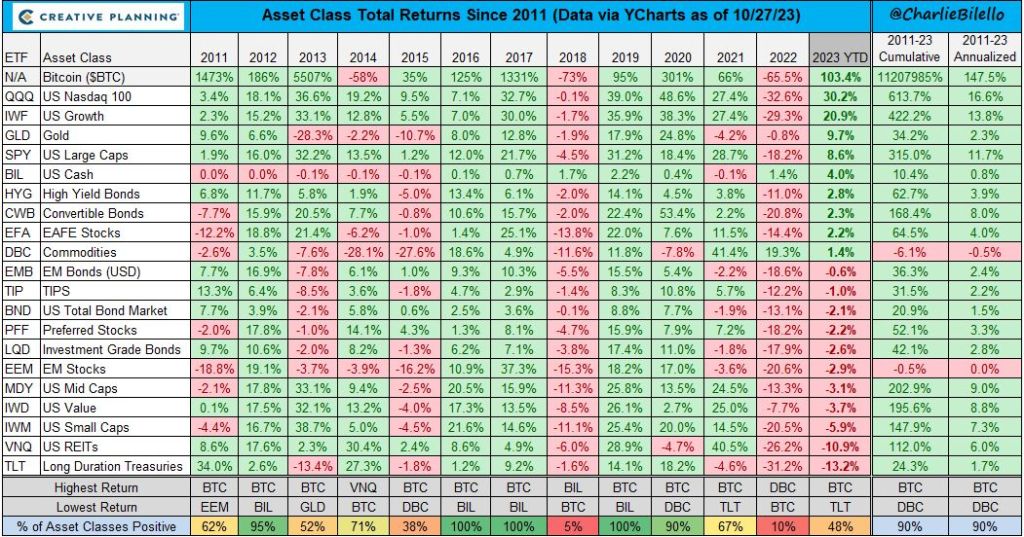

2022 was a bad year for investments under Bidenomics. 2023 year to date is showing huge gains for Bitcoin, the NASDAQ and gold. Bringing up the rear are long duration Treasuries and REITs (real estate investment trusts), both earning negative returns thus far of less than -10%.

Let’s start with personal savings as a percentage of disposable income. It has been in the red (meaning very low) under Billions Biden.

And The Fed is really in the red under Biden’s inflation rattling spending with losses leading to a surge in remittances.

And then we have the growth in the Federal deficit as a % of GDP in the red.

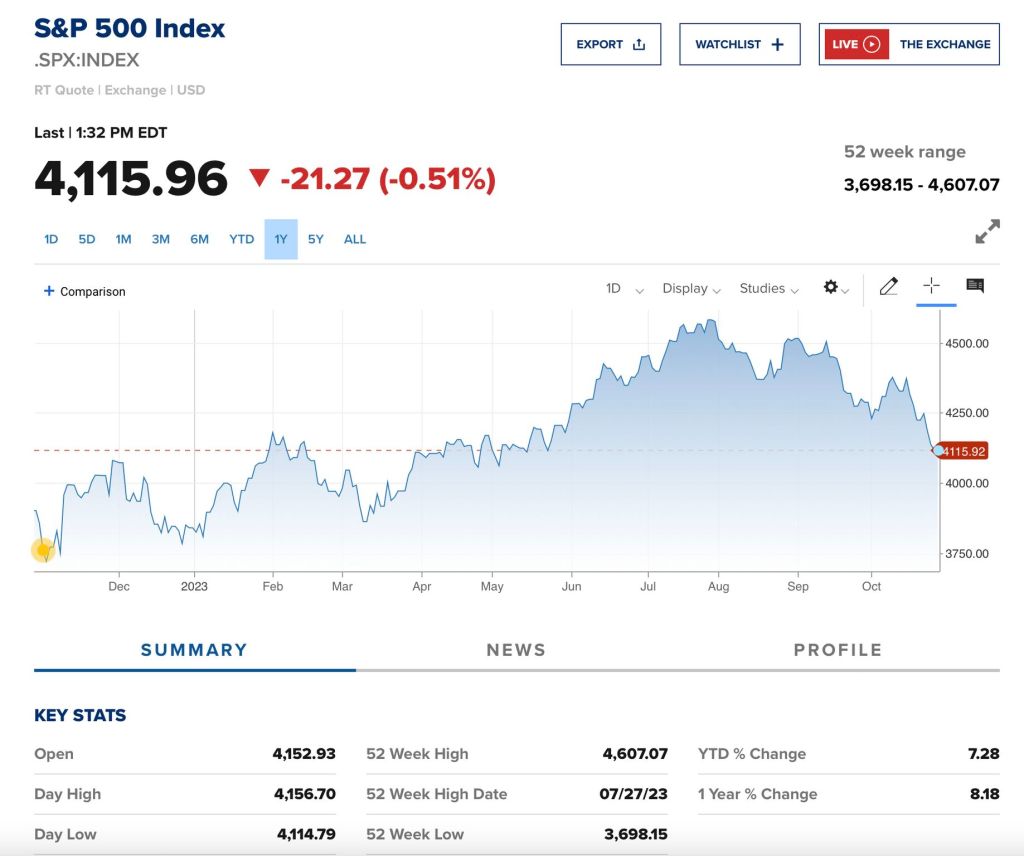

And the S&P 500 is in the red since August.

Even Biden’s pro-censorship buddies in the tech world are in the red since July.

On the black side of the ledge, Bitcoin (along with gold) are through the roof.

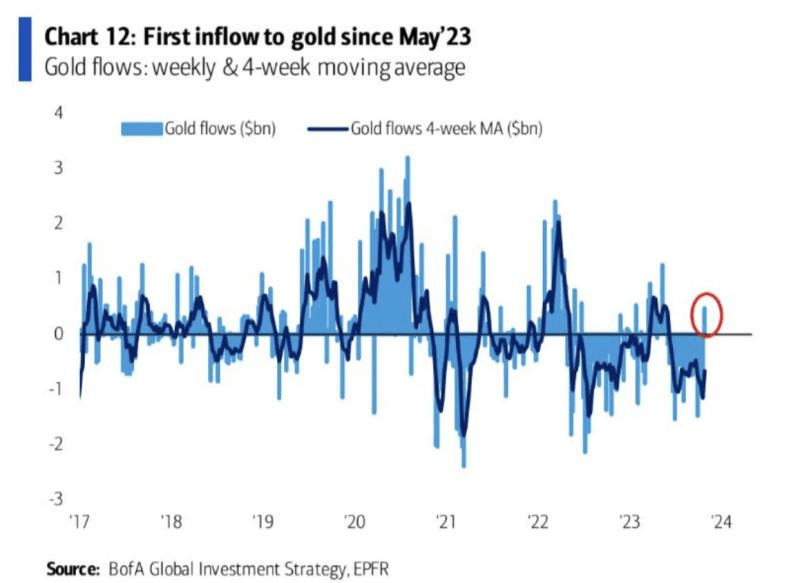

The first inflow to golf since May ’23.

But at least Bidenomics has helped the donor class get wealthier and has helped the lessers get part-time jobs.

Yes, Bidenomics is a highway to hell for the 99%. But a stairway to heaven for the donor class and 1%. And the donor class (and defense/banking/tech/drug industries) have Biden under their thumbs.

My foolish US Senator Sherrod “The Mad Marxist” Brown claimed that he hasn’t noticed illegal immigrants.

Of course, Senator Brown could travel with Biden to the border to witness military age men crossing the border under Biden/Mayorkis “:Operation US Chaos.”

Bidenomics new theme song is “Addicted To Gov.” Bidenomics needs lots of Federal spending and borrowing to survive. But all this spending and borrowing is causing rapid price increases and other distortions.

The US is teetering on World War III with tensions soaring in the Middle East, Ukraine, and southeast Asia. And Biden wanders off to Rehobeth Beach Delaware to relax … while over 200 Americans are still held hostage by terrorist group Hamas. The bad news? Biden is back in Washington DC trying to make the border crisis even worse by demanding funding for “border security” in the form of transporting illegal immigrants to US cities. Is The Squad running The White House??

But on the housing/mortgage front, we have another week of declining mortgage demand/applications as mortgage rate hit almost 8%.

Mortgage applications decreased 1.0 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending October 20, 2023.

The Market Composite Index, a measure of mortgage loan application volume, decreased 1.0 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index decreased 1 percent compared with the previous week. The Refinance Index increased 2 percent from the previous week and was 8 percent lower than the same week one year ago. The seasonally adjusted Purchase Index decreased 2 percent from one week earlier. The unadjusted Purchase Index decreased 2 percent compared with the previous week and was22 percent lower than the same week one year ago.

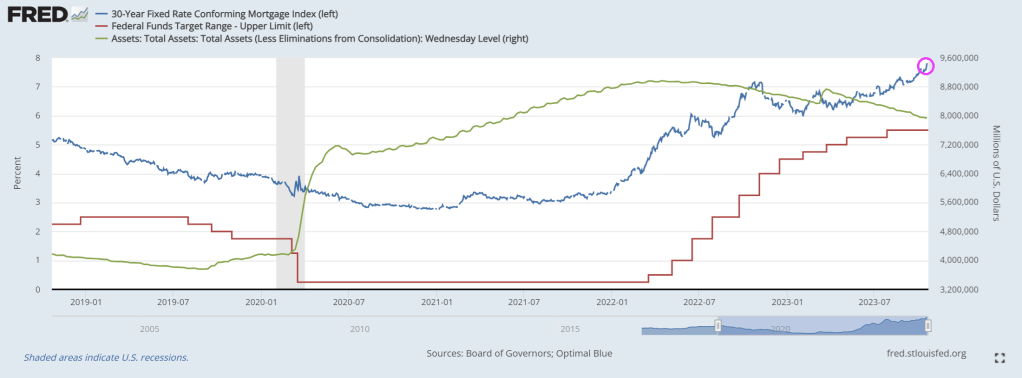

Mortgage rates followed Treasuries higher, with the 30-year fixed mortgage rate jumping 20 basis points to 7.9 percent – the highest since 2000. Rates have now risen seven consecutive weeks at a cumulative amount of 69 basis points.

Hey Joe, I’ll bet those 200+ US hostages held by Hamas aren’t enjoying ice cream cones.

Back in red? As US fiscal policy deteriorates further thanks to endless Federal spending (not to mention seemingly endless wars under Biden and Nobel Peace Prize winner Obama), we are seeing pain in the bank lending business.

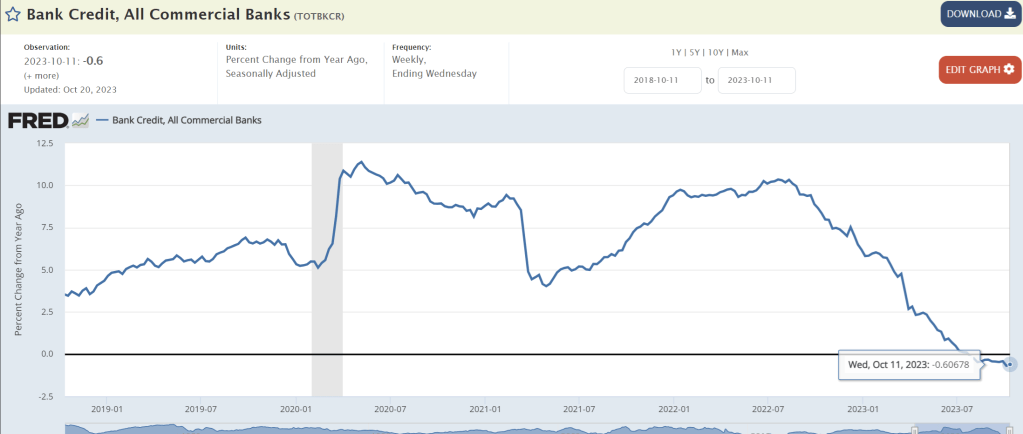

Commercial and industrial (C&I) loan lending standards is tightening (blue line) to levels typically seen in recessions. Even though Barclays HY-10Y spreads remains low.

Bank credit growth remains negative for the twelve straight week.

Billions Biden’s spending spree has led to the budget gap has doubled in the last year.

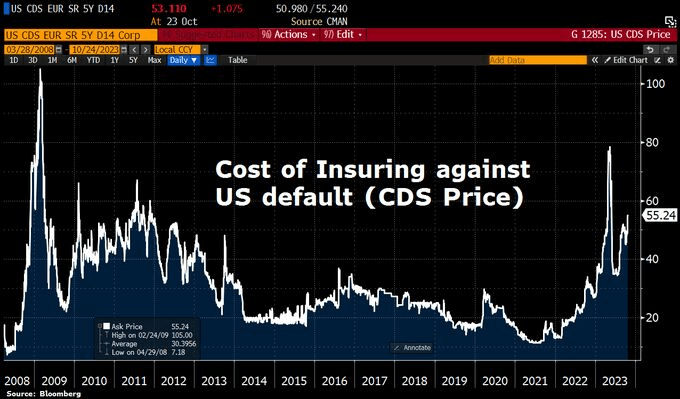

CDS is now at 55.24, highest after the Covid shock.

Under Biden/Yellen’s economic model, the appropriate themesong is “Hell’s Bells.”

Bidenomics has been a massive windfall for the top 1% of households in terms of wealth due to the emphasis on green energy transformation. But for the 99%, Bidenomics has been a disaster (unless you consider low-paying job creation a victory).

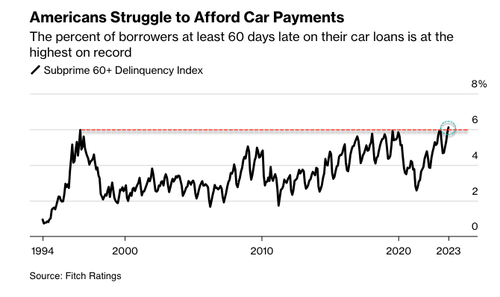

The auto sector, considered a leading economic indicator, pinpoints the arrival of the crushing auto loan crisis and even the possibility of the onset of the next recession. In late January, we Fitch revealed tat consumers are falling behind on auto payments – the most since the peak of the Great Financial Crisis. Fast forward nine months later, to September, that rate just hit the highest level in nearly three decades.

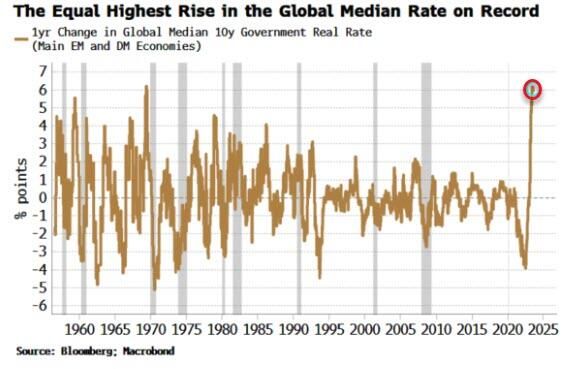

And with interest rates rising the fastest in history,

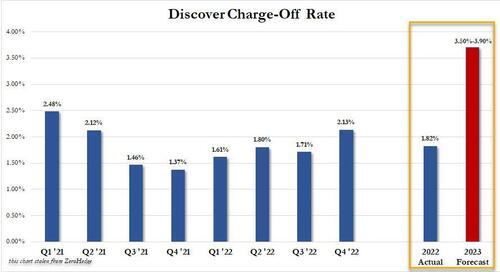

And Discover projected charge off rate for 2023 would more than double from its current 1.82% to as much as 3.90%!

In what could be the early innings of the auto loan crisis, something we called a “perfect storm” earlier this year, Bloomberg cites new Fitch data:

The percent of subprime auto borrowers at least 60 days past due on their loans rose to 6.11% in September, the highest in data going back to 1994, according to Fitch Ratings.

Source: Bloomberg

“The subprime borrower is getting squeezed,” said Margaret Rowe, senior director with Fitch.

Rowe said, “They can often be a first line of where we start to see the negative effects of macroeconomic headwinds.”

What has been widely known is the consumer has been funding car purchases with even more debt to afford record-high prices, with many monthly payments exceeding $1,000. Factor in the Federal Reserve’s most aggressive interest rate hiking cycle in a generation, elevated inflation, and the restarting of the federal student loan payments, tens of millions of consumers are under immense pressure this fall.

An endless stream of retailers, such as Walmart, Nordstrom, Macy’s, and Kohl’s – all of whom have recently warned about a consumer slowdown. Banks have also raised concerns, such as Morgan Stanley’s Mike Wilson, who believes the consumer is ‘falling off a cliff.’ And the latest high-frequency data from Barclays shows card spending has taken another leg down.

As delinquencies rise, Cox Automotive forecasts that 1.5 million vehicles will be seized this year, up from 1.2 million in 2022. That’s still below pre-pandemic levels, but the numbers could soar if a recession materializes in 2024.

Bloomberg cited Bankrate data that shows consumers with excellent credit can lock in an average interest rate of around 5.07% for a new car and 7.09% for a used vehicle. Those with bad credit should expect a new car rate of 14.18% and 21.38% for a used car.

The perfect storm we described earlier this year is unfolding.

At least residential mortgage delinquency rates remain low. With elevated home prices, the incentive to default on a loan is limited.

So The Perfect Storm hasn’t hit residential real estate … yet. But with households needing $114,000 in annual income to afford a typical home …

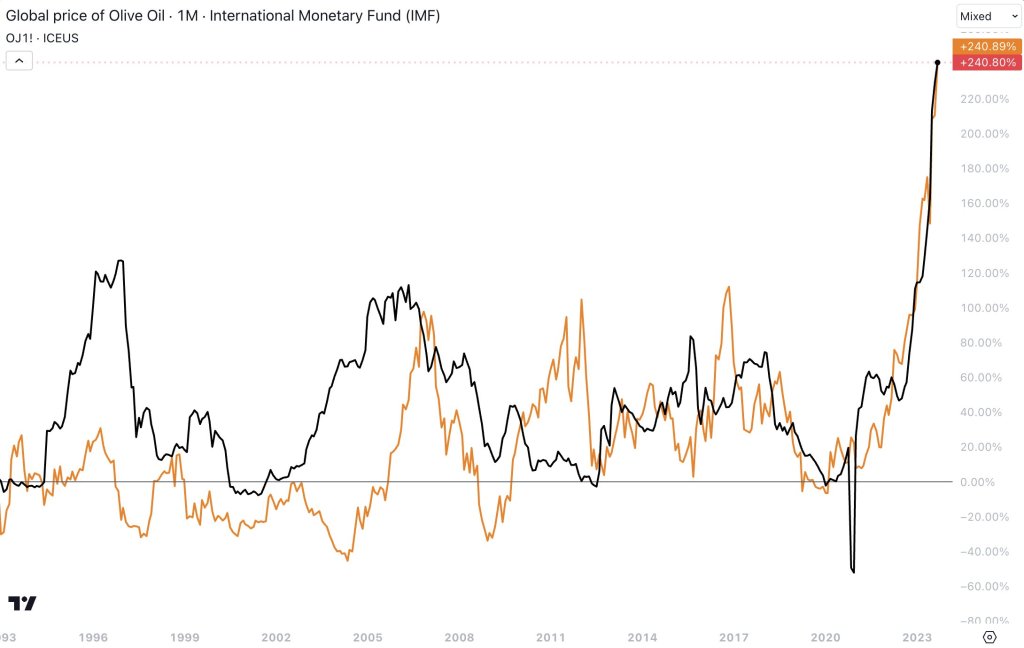

But at least home prices aren’t rising as fast as olive oil and orange juice!! Wow, that excesssive stimulypto by The Fed and Federal government is really screwing things up in the economy.

Biden is like George Clooney in “The Perfect Storm” sending the US out into stormy, violent seas while obessing about Ukraine and protecting Iran/Hamas.

{kind=link}

{kind=link}

{kind=link}

You must be logged in to post a comment.