The Silicon Valley Bank failure (along with NY’s Signature Bank) are sending shock waves through the global economy. Not because of the incompetence of bank regulators, but because of the reaction function from the FDIC and Fed.

The 10-year Treasury yield is down -26 basis points in the AM. And the Fed Funds Target Rate is expected to drop to 4.7%.

Its not just the US Treasury yield that declined -26 basis points. European sovereign yields are down too (Germany 10-year is down -32.9 basis points).

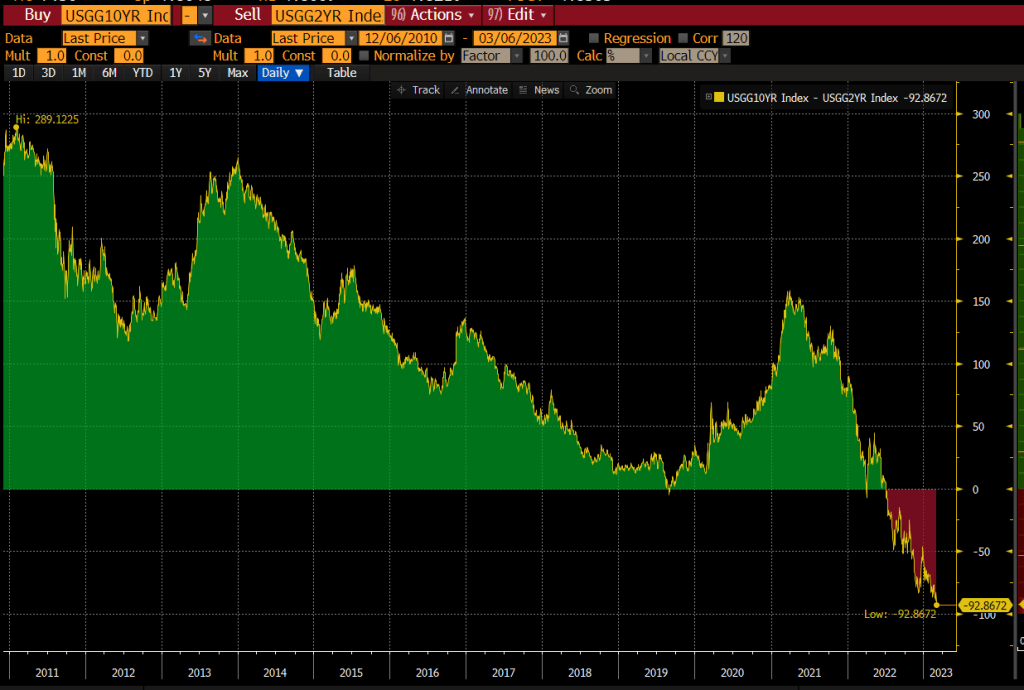

Look at the 2-year Treasury yield. Its down -54.6 basis points.

On a sad note, Resident Biden is calling for stricter regulations for the banking industry, already one of the most regulated sectors of the economy. How about less politics and just make them do their ^*T^R jobs!

Despite cries from Summers, Yellen and other the DC illuminati (Biden is oddly silent), US banks are NOT fine. In fact, banks in general are suffering from Fed rates increases due to holding of long-term Treasuries and MBS.

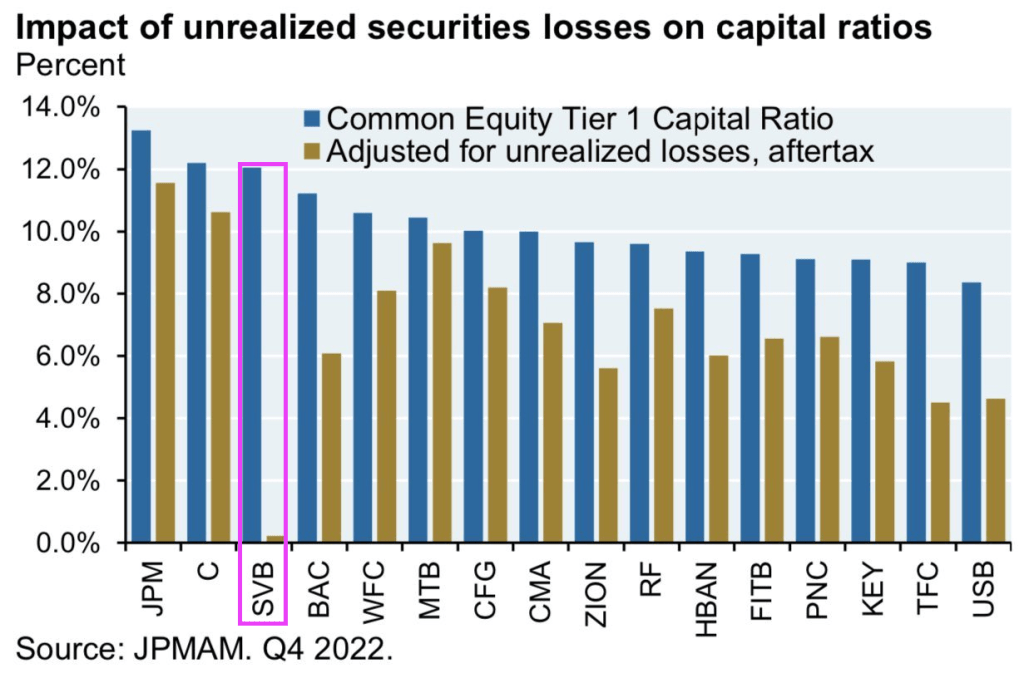

In fact, The Federal Reserve’s fight against inflation is causing serious problems, as exemplified by AOC. No, not THAT AOC. but bank Accumulated Other Comprehensive Income.

Accumulated Other Comprehensive Income (AOCI) are special gains and losses that are listed as special items in the shareholder equity section of a company’s balance sheet. The AOCI account is the designated space for unrealized profits or losses on items that are placed in the other comprehensive income category.

On the regulatory call reports, AOCI is added to regulatory capital. Since SVB’s AOCI was negative (because of its unrealized losses on AFS securities) as of Dec. 31, it lowered the company’s total equity capital. So a fair way to gauge the negative AOCI to the bank’s total equity capital would be to divide the negative AOCI by total equity capital less AOCI — effectively adding the unrealized losses back to total equity capital for the calculation.

Getting back to our list of 10 banks that raised similar red margin flags to those of SVB, here’s the same group, in the same order, showing negative AOCI as a percentage of total equity capital as of Dec. 31. We have added SVB to the bottom of the list. The data was provided by FactSet:

Or this chart of vulnerable banks from Morningstar of unrealized losses and liquidity risk.

Here is a snapshot of SVB’s balance sheet. Or UNbalanced sheet.

After Congress passed the greatly flawed Dodd-Frank banking legislation, bailouts of banks are prohibited. But bank BAIL-INs still exist. Banks use money from their unsecured creditors, including depositors and bondholders, to restructure their capital to stay afloat. Put simply, they can convert their debt into equity to increase their capital requirements. Although depositors run the risk of losing some of their deposits, banks can only use deposits in excess of the $250,000 protection provided by the Federal Deposit Insurance Corporation (FDIC).

In any case, the FDIC and Fed are weighing a special vehicle after SVB swiftly collapses. Special vehicle? Sounds an awful like the mega bank bailout of 2008 under Hank Paulson.

Silicon Valley Bank (SVB), the nation’s 16th largest bank, got caught in Ben Bernanke and Janet Yellen’s bear trap, the trap set when Bernanke/Yellen kept interest rates 25 basis points for too long (from December 2008 through December 2015) and then raising rates only once during Obama’s Presidency, only to raise rates 8 times after Trump was elected President. Then Covid struck in early 2020 and Powell dropped rates to 25 basis points again until inflation struck and Powell started raising rates at the fast pace in history.

Of course, banks got clobbered with interest rate increases, such as Silicon Valley Bank.

SVB’s collapse into Federal Deposit Insurance Corp. receivership came suddenly on Friday, following a frenetic 44 hours in which its long-established customer base of tech startups yanked deposits. But its fate was sealed years ago — during the height of the financial mania that swept across America when the pandemic hit.

US venture capital-backed companies raised $330 billion in 2021 — almost doubling the previous record a year before. Cathie Wood’s ETFs were surging and retail traders on Reddit were bullying hedge funds.

Crucially, the Federal Reserve pinned interest rates at unprecedented lows. And, in a radical shakeup of its framework, it promised to keep them there until it saw sustained inflation well above 2% — an outcome that no official forecast.

SVB took in tens of billions of dollars from its venture capital clients and then, confident that rates would stay steady, plowed that cash into longer-term bonds.

In doing so, it created — and walked straight into — a trap. Set by Fed Chair Ben Bernanke and now US Treasury Secretary Janet Yellen. To be sprung by current Fed Chair Jay Powell.

Becker and other leaders of the Santa Clara-based institution, the second-largest US bank failure in history behind Washington Mutual in 2008, will have to reckon with why they didn’t protect it from the risks of gorging on young tech ventures’ unstable deposits and from interest-rate increases on the asset side.

Outstanding questions also remain about how SVB went about navigating its precarious position in recent months, and whether it erred by waiting and failing to lock down a $2.25 billion capital injection before publicly announcing losses that alarmed its customers. Investors and depositors tried to pull $42 billion on Thursday, leaving the firm with a negative cash balance of almost $1 billion, regulators said.

The KBW Bank index shows the slaughter of most banks on Friday.

Of course, the notorious Too Big To Fail (TBTF) banks JP Morgan Chase and Wells Fargo actually rose in value on Friday while regional banks got clobbered like Signature Bank, First Republic and Western Alliance Banks all losing over 10% in price on Friday.

How did this happen? Well bets placed during Covid with The Fed keeping rates at 25 basis points got clobbered when The Fed finally started raising rates again. Modified duration, a risk measure indication the weighted-average life of a bond and mortgage-backed securities (MBS), has been increasing steadily since the initial Covid shock.

SVB’s management’s solution appears to have been to seek out yield through a lot of long-duration bonds. The bank started to lose deposits as VCs pulled cash/burnt through operating capital. Whoops!

Unrealized losses killed SVB, thanks to their long duration bet as The Fed tightened.

The most terrifying thing was when former Treasury Secretary Larry Summers and current Treasury Secretary Janet Yellen went on TV to exclaim “Remain calm! All is well … in the banking sector.” You know when they wheel out Summers and Yellen that all is NOT well.

Its just like The Fed. The Taylor Rule says that The Fed’s target rate should be 10.29%, but now the terminal rate has been lowered to 5.475%, almost half of where the target rate should be.

Today’s jobs report for February was a huge disappointment IFF you expected another blowout jobs report like the one from January (504k jobs added). February saw just 311k jobs added, a decline of -38.3% MoM.

And just like that, The Fed’s terminal rate fell to 5.475%, a far cry from the 10.29% rate according to the Taylor Rule.

Let’s see if The Fed holds course with Silicon Valley Bank collapsing in biggest failure since 2008.

Silicon Valley Bank became the biggest US lender to fail in more than a decade after a tumultuous week that saw an unsuccessful attempt to raise capital and a cash exodus from the tech startups that had fueled the lender’s rise.

Regulators stepped in and seized it Friday in a stunning downfall for a lender that had quadrupled in size over the past five years and was valued at more than $40 billion as recently as last year.

The move by California state regulators to take possession of the lender, known as SVB, and appoint the Federal Deposit Insurance Corp. receiver underscores the impact that the US’s rapid interest-rate increase is having on smaller lenders. SVB is the second regional lender to fold this week after Silvergate Capital Corp. announced it was voluntarily liquidating its bank, spurring a broader selloff in bank stocks.

The FDIC has set up a bridge bank to handle the failure of SVB. VERY rare. The last bridge bank was for IndyMac Bank from LA.

SVP is the second biggest bank failure in US history after Washington Mutual (WAMU).

Now here we are again with yet another bank contagion. First it was Silicon Valley Bank, now it is First Republic Bank (down -28% at opening).

And there is a trading halt on First Republic. But YoY growth on FRC’s earnings of -34.7% is horrendous.

At least cryptobank Silvergate isn’t down as much as Silicon Valley Bank and First Republic Bank.

And the SPDR Regional Bank index is getting clobbered as Fed withdraws stimulus.

SVB’s management’s solution appears to have been to seek out yield through a lot of long-duration bonds. The bank started to lose deposits as VCs pulled cash/burnt through operating capital.

SVB’s CEO Greg Becker saw this coming and dumped his holdings.

One indicator that the Biden Administration will herald is that average hourly earnings rose to 4.6% Year-over-year (YoY). Too bad headline inflation is still at a whopping 6.4% YoY.

More jobs were added to the US economy than forecast (311k actual versus 225k forecast). The U-3 unemployment rate rose to 3.6% from 3.4% in January.

The aftermath of the jobs report? 2-year Treasury yields are down a whopping -15.8 basis points. But Europe is seeing double digit declines in sovereign yields as well.

At the 10-year tenor, we see the US Treasury yield drop -12.8 basis points. Much in line with European sovereign yield declines.

Mortgage applications increased 6.9 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending March 3, 2023.

The Market Composite Index, a measure of mortgage loan application volume, increased 6.9 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index increased 9 percent compared with the previous week. The Refinance Index increased 9 percent from the previous week and was 76 percent lower than the same week one year ago. The seasonally adjusted Purchase Index increased 7 percent from one week earlier. The unadjusted Purchase Index increased 9 percent compared with the previous week and was 42 percent lower than the same week one year ago.

Today, we saw mortgage rates climb further to 7.11% as the US Treasury yield curve (10Y-2Y) descends into Mortgage Mordor as The Fed continues to tighten.

The last US debt crisis occured in 2013 when Congress finally raised the debt ceiling … and kept on borrowing and spending, But if you thought that a debt crisis would scare Congress (and the Administration) into balancing the Federal budget, you would be wrong. In fact, since the 2013 debt crisis, Federal debt is up 88% (+$14.7 TRILLION over the last 10 years).

And with the massive growth in Federal debt under Obama, Trump and Biden has resulted in an explosion in interest payments on the Federal debt.

Interest rates are an important driver of the economy and financial markets. And what has happened to the S&P 500 index since The Federal Reserve started raising their target rate on May 4, 2023 to fight surging inflation?

Since that fatal day, the S&P 500 index has fallen -6% and equity REITs (commercial real estate) has fallen -16%.

What about returns on US Treasuries and Mortgage-backed Securities (MBS)? Same thing. PAIN!

Although The Fed has pledged to keep raising rates to fight inflation (and further decimate retirement accounts), investors are pointing to a peak (terminal) Fed rate of 5.44% at the September 2023 FOMC meeting. Then rate cuts following the September 2023 meeting.

Of course, much of the blame belongs to former Fed Chair Ben (QE) Bernanke and current Treasury Secretary Janet “Too Low For Too Long” Yellen who never met a Fed rate hike that she liked. But Yellen LOVES giving away US taxpayer dollars … to Ukraine.

You must be logged in to post a comment.