The Federal Reserve is some hard thinking to do. Inflation came in hotter than expected, so raise rates to fight inflation or lower rates to prevent bank contagion. Similar to Kevin Malone’s “Double fudge brownies or Angela” debate.

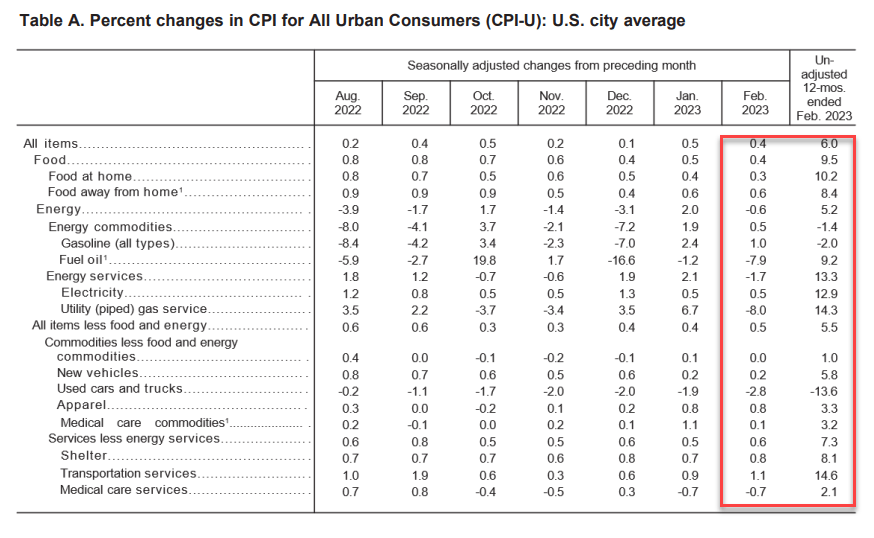

While headline inflation (CPI) came in a 6% (considerably higher than The Fed’s 2% target), core inflation came in at 5.5% year-over-year (YoY), which was expected.

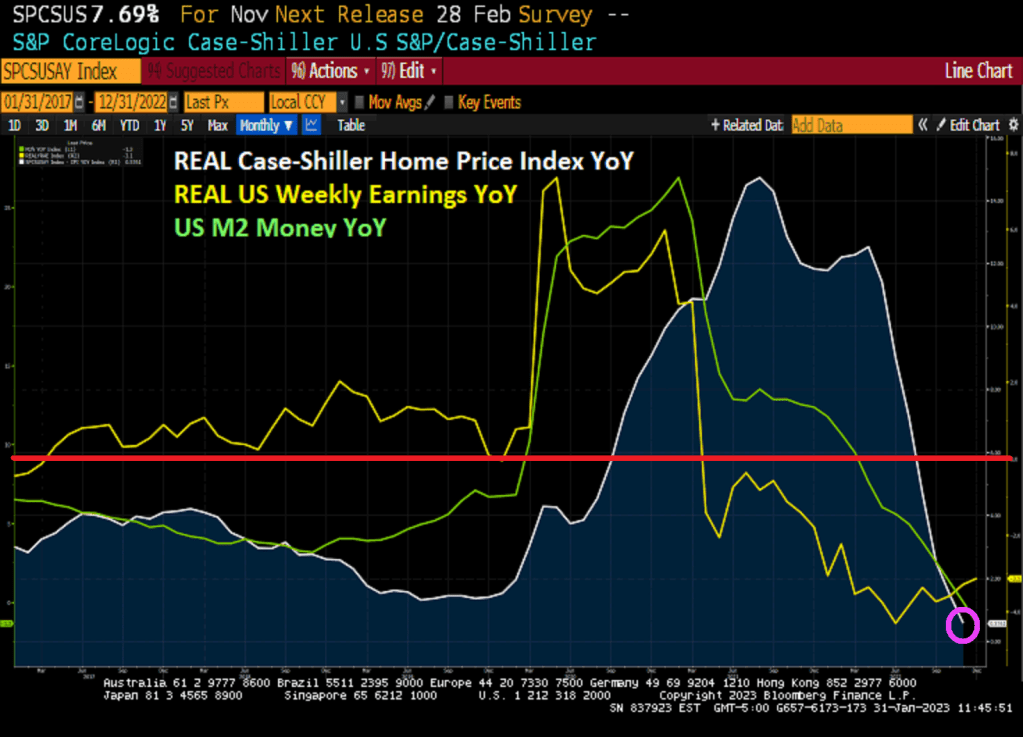

The truly nasty number is today’s inflation report is that weekly earnings YoY remained the same at a terrible -1.9%. Meaning that inflation is higher than nominal wage growth. This is the 23rd straight month of negative real weekly earnings. Well done, Fed and Biden!

Food is up 10.2% YoY. Electricity up 12.9%, shelter up 8.1%.

On the news, the US Treasury 2-year yield rose 34.3 basis points.

Somehow I doubt that Biden’s press secretary will tout 23 straight months of negative weekly earnings growth as one of Biden’s economic accomplishments.

You must be logged in to post a comment.