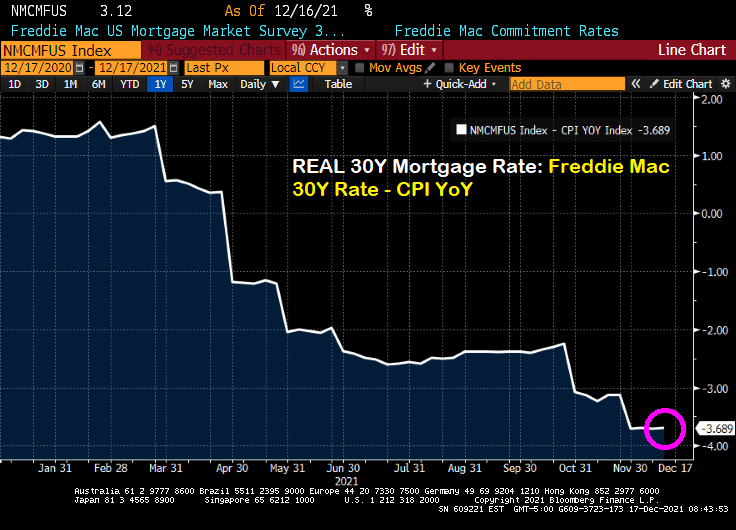

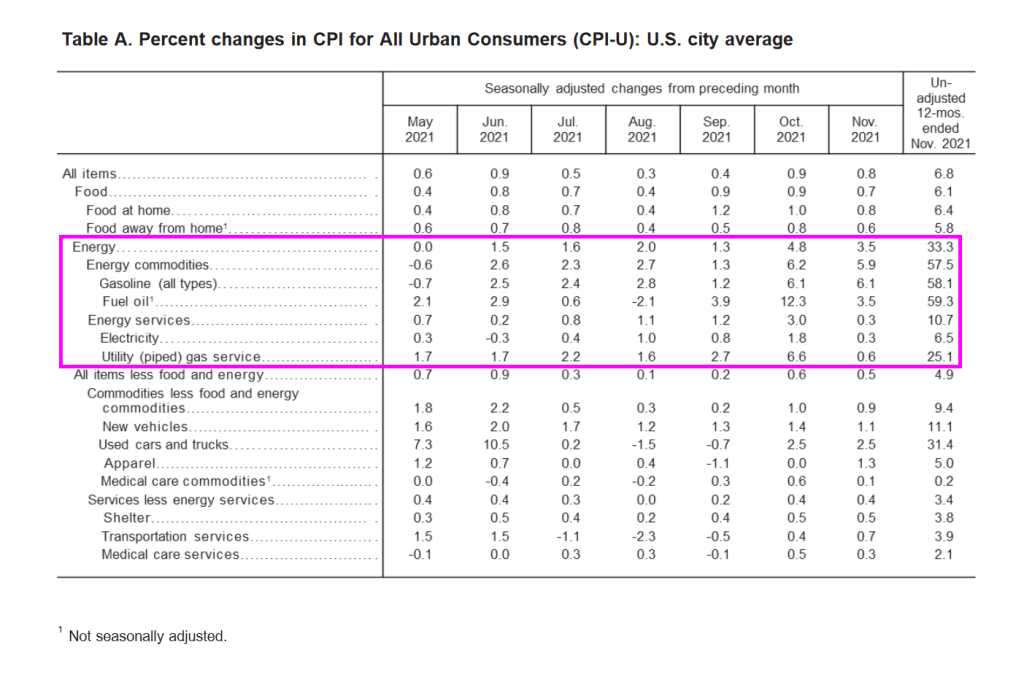

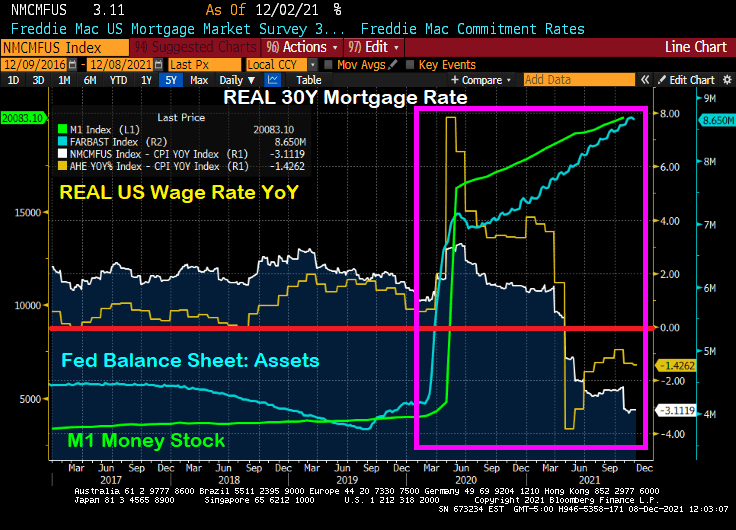

The Freddie Mac 30-year mortgage commitment rate rose to 3.12%. But once we subtract the gut-wrenching inflation rate, the REAL 30-year mortgage rate is -3.689%.

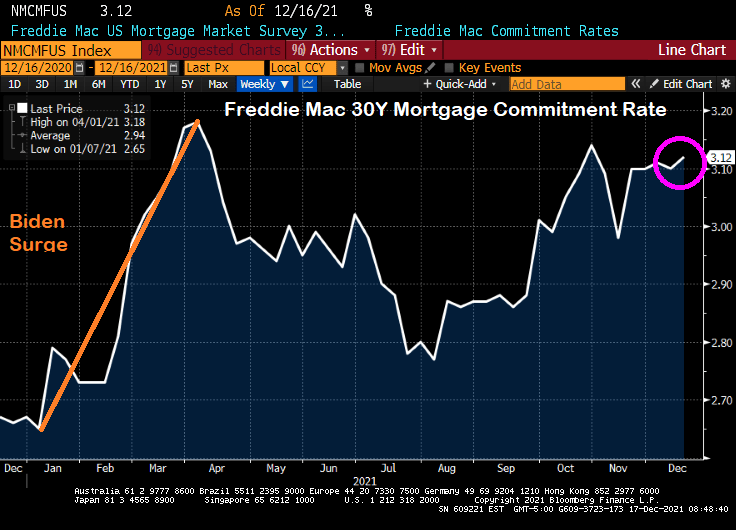

The nominal Freddie Mac 30-year commitment rate rose to 3.12% which is still lower than 3.18% back on April 1, 2021 after surge in rates following Biden’s taking the office of Presidency in January.

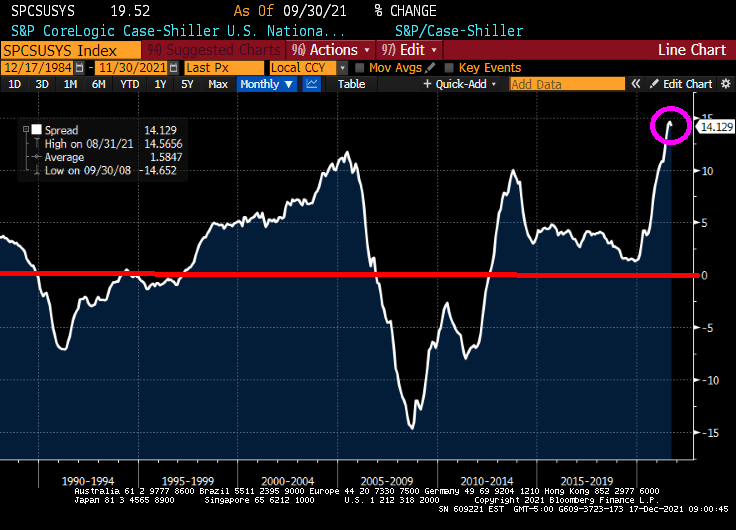

Meanwhile, the REAL Case-Shiller National home price index (CS National YoY – CPI YoY) is growing at the fastest rate in history. Great if you already own a home, but lethal if you are renting and want to move to homeownership.

Meanwhile, REAL wage growth is at -1.94% YoY.

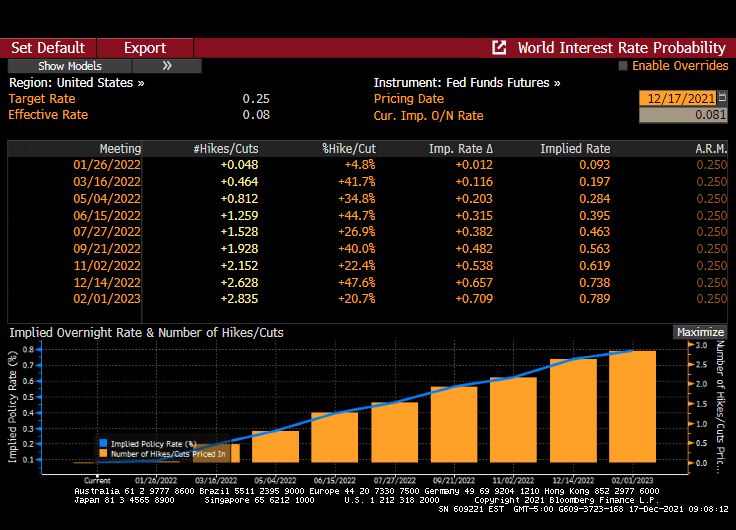

Well, Chairman Powell and The Gang failed to raise the Fed Funds Target Rate yet again, but let us know that they will tighten someday soon. The Fed Funds Futures are signalling a rate hike at the June 2022 meeting and another at the November meeting.

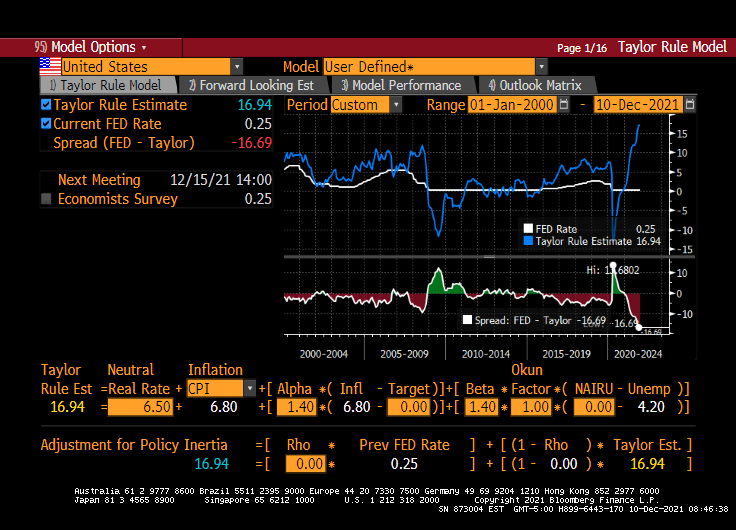

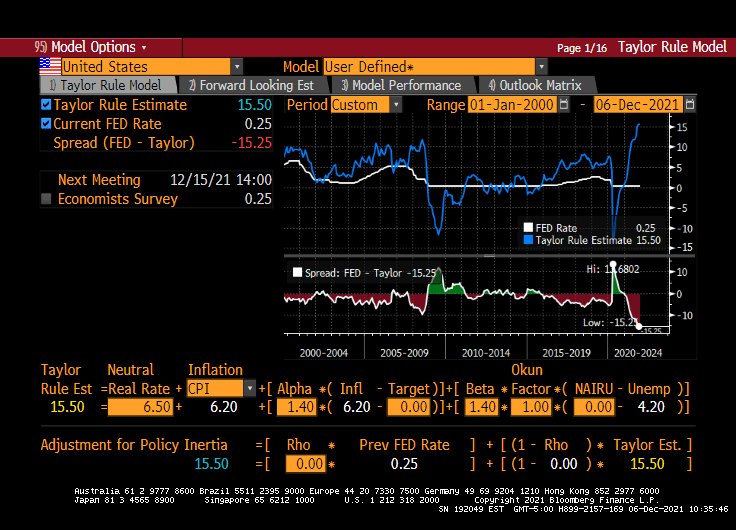

While The Fed couldn’t care less about the Taylor Rule, it is still interesting to note just how out of touch The Fed FOMC is with reality. The Taylor Rule indicates that their target rate should be 16.94% rather than the current target rate of 0.25%.

Keeping the target rate unchanged in the face of gut-wrenching inflation is a bold strategy, Cotton.

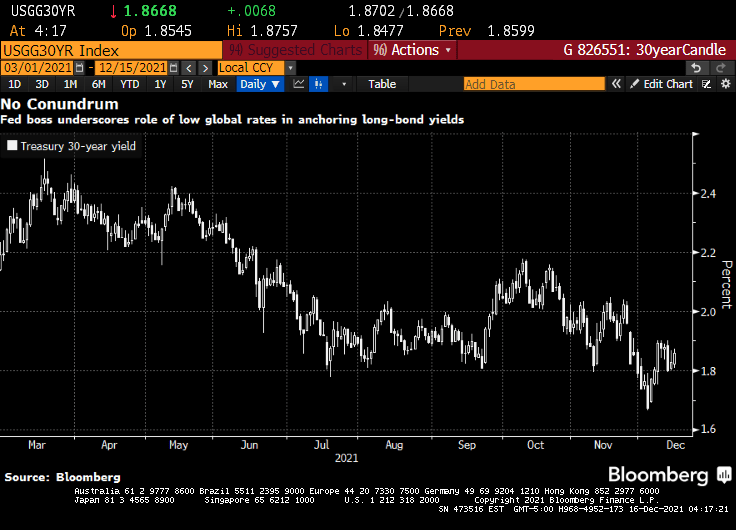

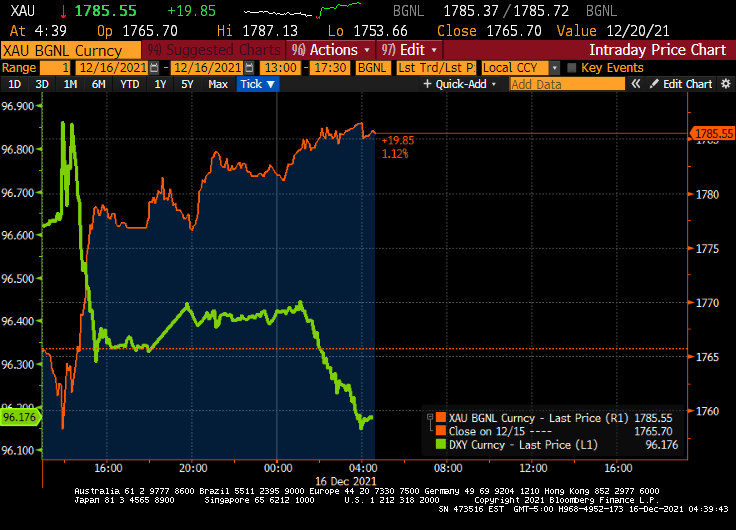

Like John Belushi from The Blues Brothers, Fed Chair Jerome Powell is saying that the markets lackluster response in terms of bond yields to his “hawkish” announcement yesterday “isn’t his fault.”

(Bloomberg)Federal Reserve boss Jerome Powell appears unperturbed by the fact that longer-term bond yields remain low even as officials lay the ground work for tighter policy and inflation is ticking higher.

While the drop in longer-term rates may be viewed by some as indicative of where so-called terminal rates for U.S. policy might ultimately lie, Powell on Wednesday emphasized the impact of ultra-low yields in places like Japan and Germany in helping to keep them anchored.

“A lot of things go into the long rates and the place I would start is just look at global sovereign yields around the world,” Powell said at a news conference following the Fed’s final scheduled policy meeting for the year, which saw officials ramp up the pace of stimulus withdrawal and boost predictions for rate hikes in 2022. The Fed Chair noted that rates on Japanese and German government bonds are “so much lower” than those on Treasuries and that with currency hedging taken into account American debt provides investors with a higher yield. “I’m not troubled by where the long bond is,” he said.

This stands as something of a contrast to the view expressed back in 2005 by one of Powell’s predecessors. Back then, Fed chief Alan Greenspan described a decline in long-term bond yields even in the face of six policy rate increases as a “conundrum.”

Or it could be that no one REALLY believes that Central Banks will ever cut interest rates, despite surging inflation.

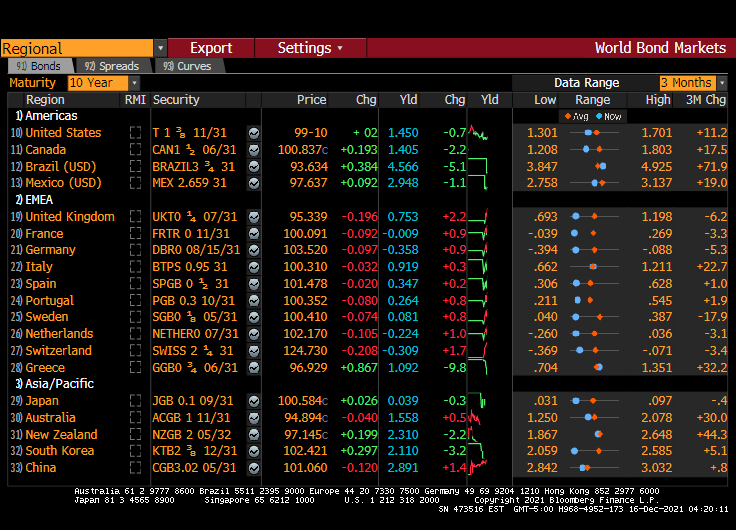

The US Treasury 10-year yield dropped 7 basis points overnight and remains just south of 1.50%. The Eurozone remains below 1% (with Germany at -0.358% and France at -0.009% at the 10-year mark). Japan is at 0.039%. This is what Powell means by low global rates keeping US long-term rates down.

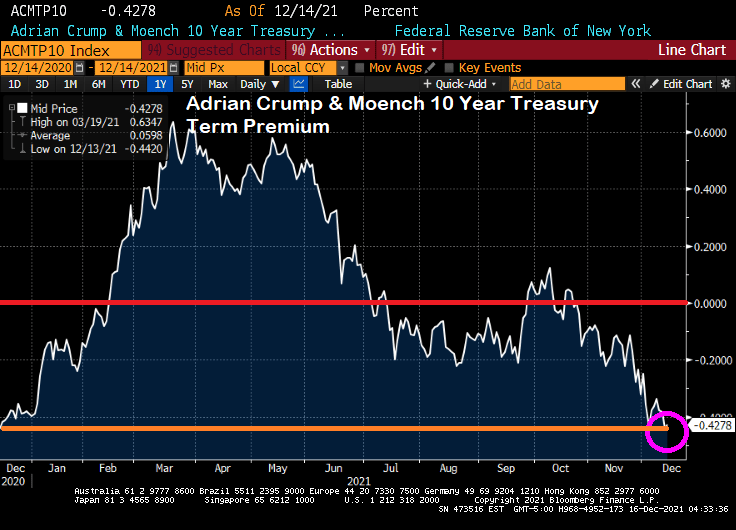

The 10-year Treasury term premium (measured before Powell’s head fake on raising rates) has returned to pre-Biden levels.

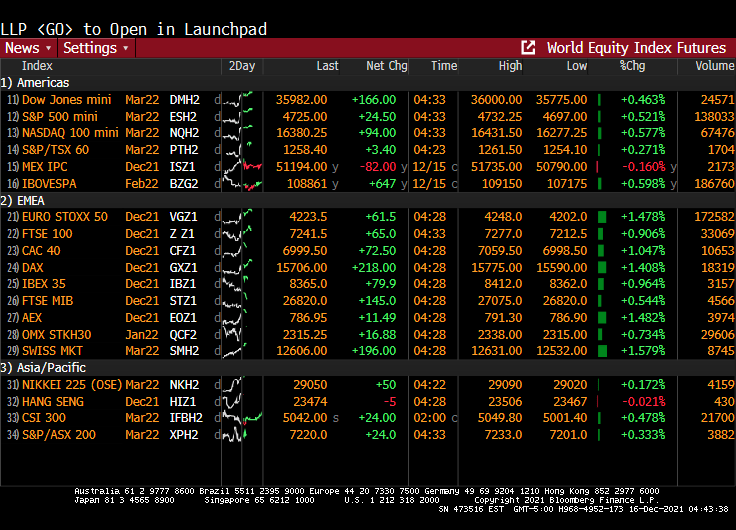

Meanwhile, global equities futures are up across the board (well, except for Mexico).

The Fed could have raised their target rate if they were REALLY interested in cooling inflation. The Taylor Rule remains at 14.94% while The Fed is stalled at 0.25%. Even if you don’t like the Taylor Rule, it still highlights how ridiculous Fed Stimulypto is.

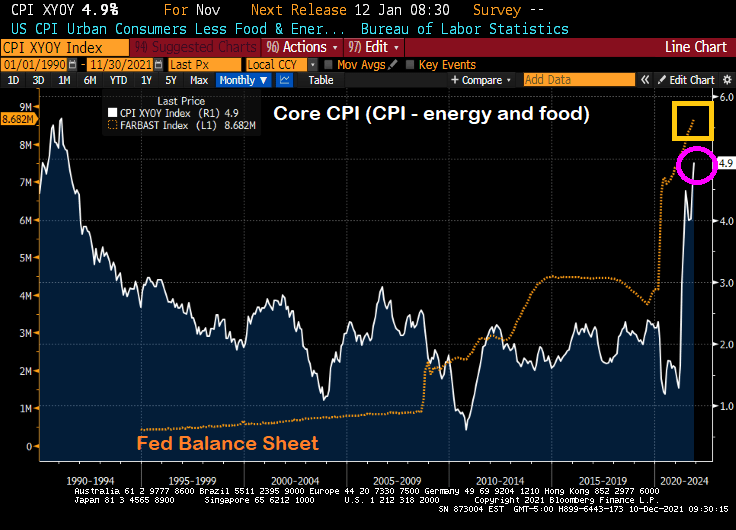

Well, we do have a government-propelled economic recovery, but at a cost of declining REAL wages thanks to the highest inflation rate in 40 years.

The Fed’s new theme song is “Hold That Tiger” meaning that despite soaring inflation rates, The Fed kept their target rate at 0.25%. Way to really pull a Volcker and raise rates to choke off inflation. … NOT!

However, The Fed doubled the pace of tapering to $30 billion a month. Median forecast shows three rate hikes in 2022, three in 2023.

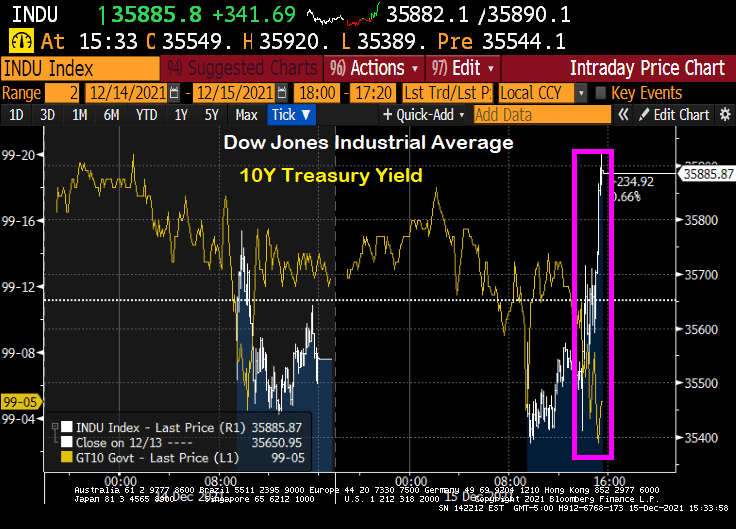

The reaction? The Dow rose 363 points as of 3:36pm EST and the 10-year Treasury yield rose a measly 1.9 bps as markets celebrate The Fed DOING NOTHING TO CURB INFLATION.

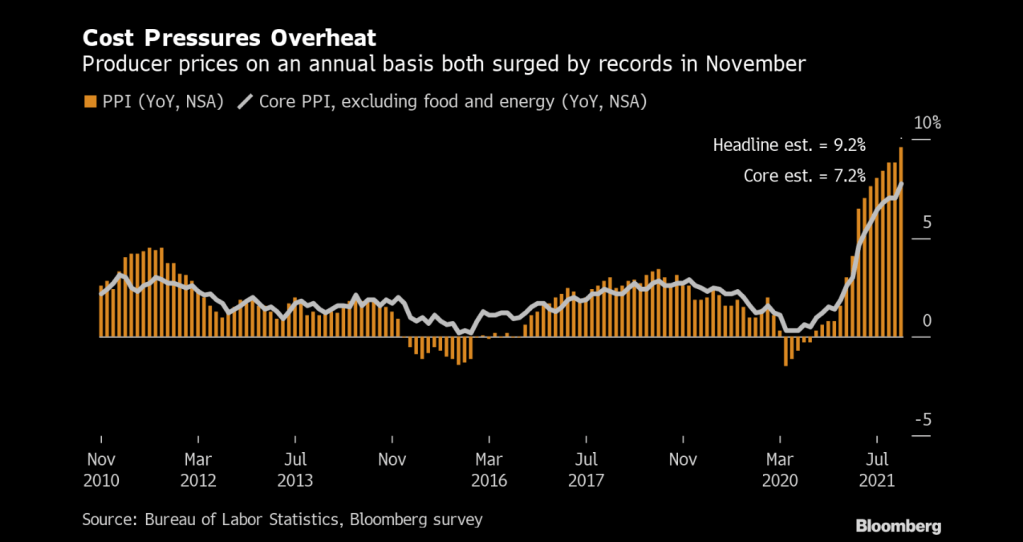

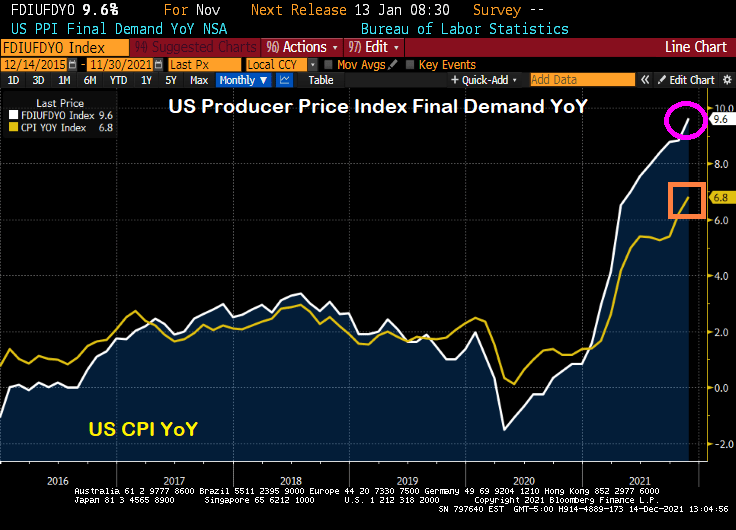

Prices paid to U.S. producers posted a record annual increase of almost 10% in November, a surge that will sustain a pipeline of inflationary pressures well into 2022.

The producer price index for final demand increased 9.6% from a year earlier and 0.8% from the prior month, Labor Department data showed Tuesday. Both advances topped economists’ forecasts.

Even more interesting (or frightening) is that PPI Final Demand YoY is soaring faster than CPI YoY. If CPI catches up to PPI, then we have serious trouble.

With inflation seemingly growing out of control, Powell and Biden should sing “76 Trillion Dollars” which will be the US national debt after Biden and Congress get done with their spending splurge.

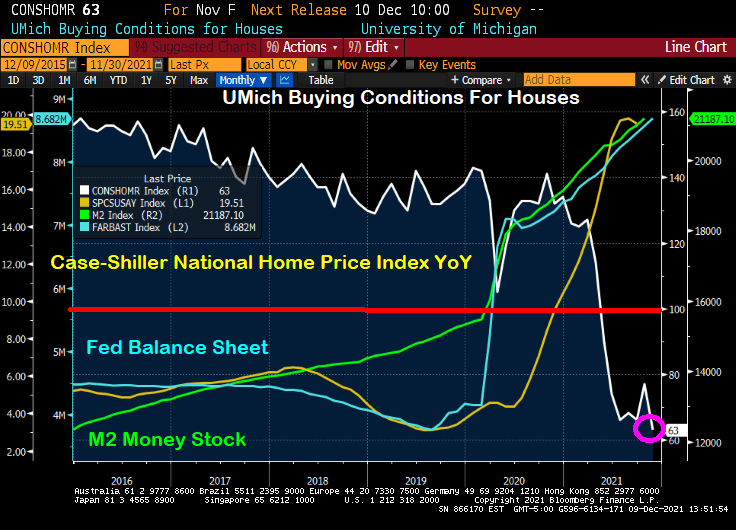

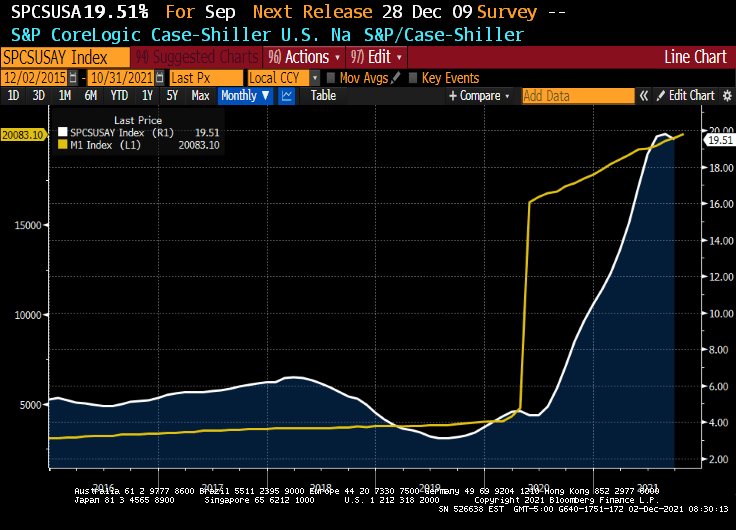

Just look at this chart of the University of Michigan Buying Conditions For Houses index. It was positive (meaning above 100) until shortly after COVID struck and The Federal Reserve rode to the rescue. National home price growth was already at 4.57% YoY in March 2020, then ballooned to 19.51% YoY at the last reading.

Here is the same chart with the broader M2 Money stock and The Fed’s Balance sheet. Same results, just not as dramatic as M1.

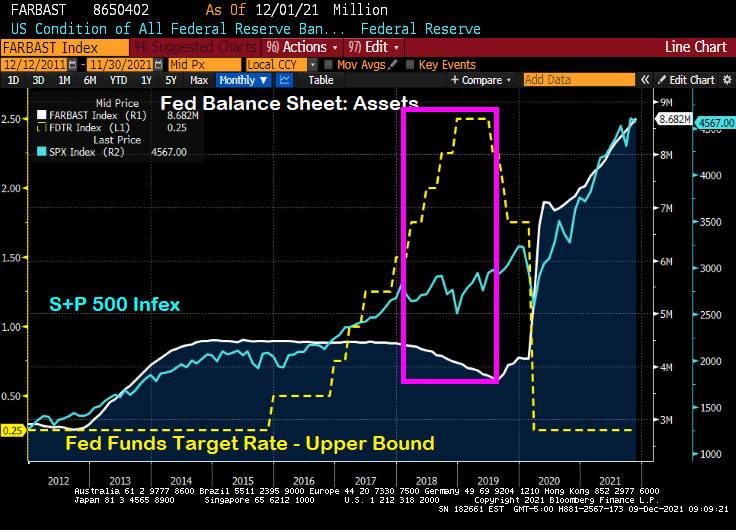

We will soon find out if The Federal Reserve will announce a rate hike or taper news. They are likely to confirm tapering, particularly if they believe that tapering won’t roil markets. After all, then Fed Chair Janet Yellen and the FOMC decided to let the Fed’s balance sheet taper (white line) while, at the same time, increasing the Fed’s target rate (yellow line). The S&P 500 index rose 9.5% over the taper/rate increase period of 12/29/2017 to 8/30/2019.

But since Stimulypto (2/28/2020 to 11/30/2021), the Fed’s balance sheet doubled+ from $4,158,637 to $8,681,771. And The Fed Funds Target Rate (UB) immediately fell from 1.75% in February 2020 to 0.25% in March 2020 … and has stayed there ever since. The S&P 500 index rose 54.6% over this Stimulypto period.

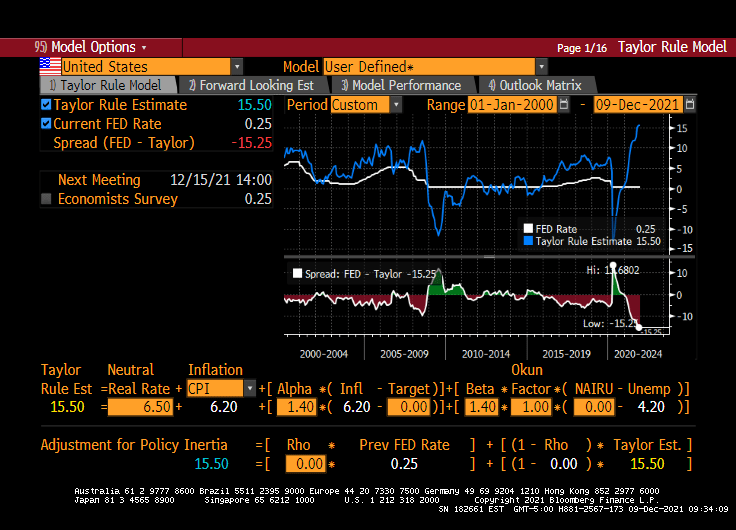

But The Fed’s upcoming decision on December 15, 2021 may be a Yellen-pivot (taper balance sheet, but raise The Fed Funds Target rate). But, then again, maybe not. The Fed is getting really bad about forward guidance and choose instead to surprise us. Hence, this is why an a-political rule is preferred (such as the Taylor Rule).

Unfortunately, the Taylor Rule infers a Fed Funds Target rate of 15.50% (using CPI YoY running at 6.20% YoY. If The Fed raises their target rate by 25-50 basis points at the December 15th meeting, color me surprised.

So, the Powell Pivot may just be the Yellen Pivot after all.

As The Federal Reserve tries to drain-off the extraordinary growth in its balance sheet since COVID without raising its target rate (good luck with that!), it is time to appraise where we are sitting. First, liquidity.

(Bloomberg) Buying and selling large quantities of U.S. government debt without substantially moving the market is about the hardest it’s been since the pandemic sent markets reeling in March 2020. Volatility has jumped, failed trades have increased — and Wall Street analysts warn that the Federal Reserve’s exit from bond-buying is set to make matters worse.

When markets seized up last year, liquidity in most Treasuries vanished, forcing the Fed to embark on massive asset purchases and other measures to avert a full meltdown. Now, the U.S. central bank is scaling back that buying, which has targeted the least-liquid Treasuries, and is poised to quicken the wind-down. At the same time, new government borrowing is ebbing, with the combination setting the stage for more fireworks.

OK, liquidity isn’t as bad as COVID and March 2020, but it is near the highest level since March 2020. The question is … will the numerous asset bubbles around the globe burstLet’s look at the ongoing saga of Chinese conglomerate Evergrande (mainly known as a large real estate developer). Their 8.25% bond has plunged to $23.481 on speculation of a catastrophic default on their bond payments. Then we have Invesco’s Golden Dragon China ETF (measuring a diversified market cap of US-listed companies headquartered or incorporated in China & derive a majority of their revenues from the People’s Republic of China). This ETF has crashed and burned back to pre-COVID (and Stimulytpo) levels.

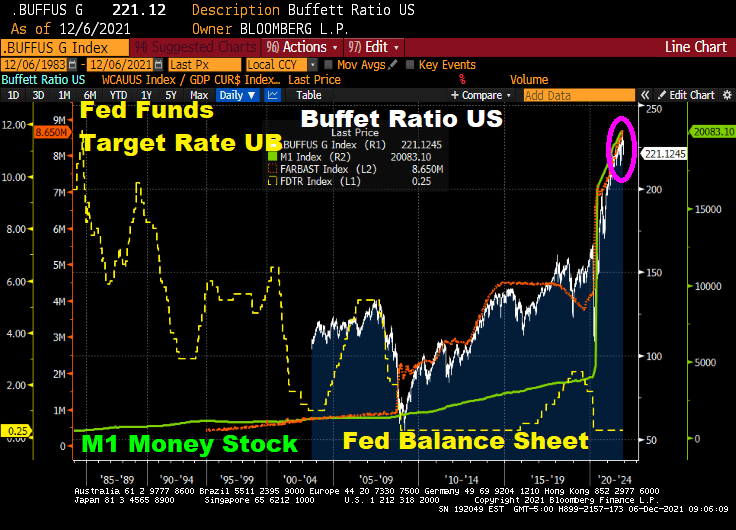

Speaking of cracks, how will the Buffett Ratio US react to a reduction in The Fed’s balance sheet (orange line) and M1 and M2 Money stock? Given that the Fed Funds target rate is WAY below where it should be (according to the Taylor Rule).

As I mentioned yesterday, the Shiller CAPE ratio is at its highest level since the Dot.com debacle of 2000. How will the Shiller CAPE ratio react to The Fed’s tapering?

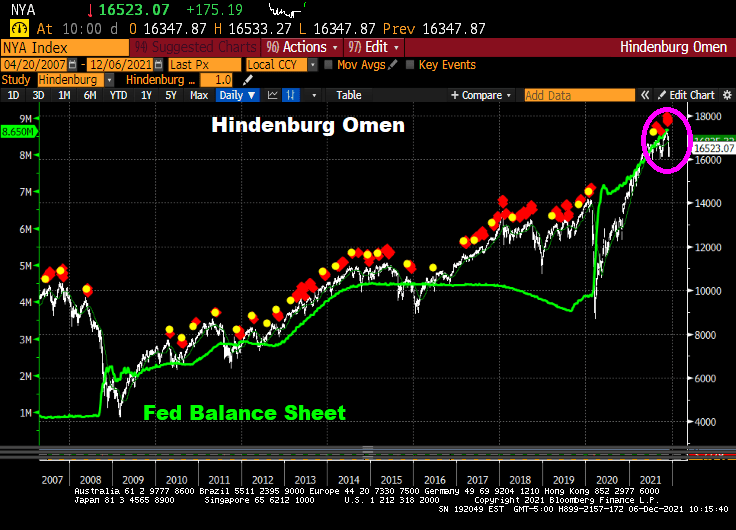

Even the Hinderburg Omen is flashing red … again.

Now, the Dow is up 600 points today, primarily on the news that the Omicron Variant is about as harmful as the common cold.

A major shift is underway at the Federal Reserve to begin to remove the central bank’s massive pandemic easing policies, and could see it hike rates sooner than is priced in by markets.

Comments by Fed officials suggest the central bank is likely to decide to double the pace of its taper to $30 billion a month at its December meeting next week. Initial discussions could also begin as soon as the December meeting about when to raise interest rates and by how much next year with Fed officials set to submit a fresh round of economic forecasts and projections for the fed funds rate.

There is no consensus yet on when to begin hikes, but it’s clear that the faster taper is designed to give the Fed flexibility to raise rates as soon as the spring. The markets do not appear to expect the first rate hike until the summer of 2022.

Uh-huh. Let’s see what happens when and if The Fed starts to taper. Is economic growth so strong that it can continue without Federal Stiumulypto? THAT is the right question.

Look at the above charts and tell me if The Fed will actually raise their target rate more than twice. Despite the Taylor Rule suggest a target rate of 15.50% to cool inflation.

Treasury Secretary Janet Yellen said yesterday that “It’s Fed’s Job to Avoid Any Wage-Price Spiral.” Well, The Fed is helping to avoid a wage increase in real terms, since the November jobs report revealed that REAL US Average Hourly Earnings growth YoY fell to -1.378%. In other words, inflation is greater than hourly earnings.

And in other jobs related news, nonfarm payrolls rose by only 210k versus expectations of 550k jobs to be added. Even NOMINAL hourly earnings growth (4.8% YoY) was less than expected (5.0%).

Labor force participation rose a bit to 61.8%, still well below the pre-COVID levels of 63.4% in January 2020.

The U-3 unemployment fell to 7.8%. Still higher than the pre-COVID rate of 7.0% in February 2020, but getting close! As for what this means for The Fed, the new target rate implied by the Taylor Rule is 15.50%.

After this lousy jobs report, 10-year Treasury yields dropped … like Biden’s approval ratings.

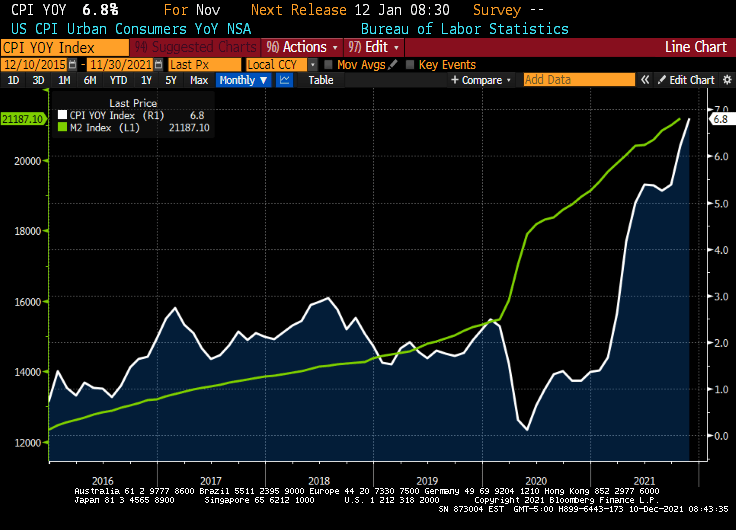

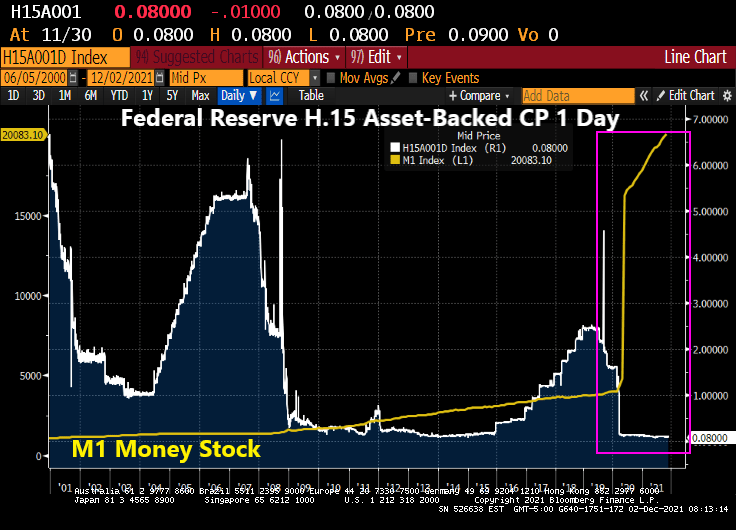

The Dream Team (Fed Chair Jay Powell and Treasury Secretary Janet Yellen) just can’t believe that inflation struck even after M1 Money Stock increased by 369% from March 2020 to today while interest rates remained near zero.

From The Hill: Federal Reserve Chairman Jerome Powell and Treasury Secretary Janet Yellen on Wednesday said they underestimated how quickly the U.S. economy would rebound from the COVID-19 recession and strain supply chains.

During a Wednesday hearing before the House Financial Services Committee, the top two U.S. economic policymakers acknowledged that high inflation has risen higher and lingered much longer than they expected.

“We understood demand would be strong,” Powell said. “We didn’t understand [the] significant problems of the supply side.”

Both Yellen and Powell said substantial fiscal and monetary stimulus played a role in stoking the higher demand that fueled inflation, but they called it a challenging side-effect of an otherwise fast recovery.

Seriously? The Fed and the Federal government dumped trillions of dollars into an economic system and didn’t think there would be negative consequences??

Look at the surge in M1 Money Stock at the same time asset-backed commercial paper rates are 0.08%. That is, about 1/3rd The Fed Funds Target rate (upper bound). None of this concerned The Dream Team?

An example of what The Dream Team didn’t see happening was the explosion of home prices. Home price growth was about 4% YoY prior to COVID, and is now 19.51% YoY.

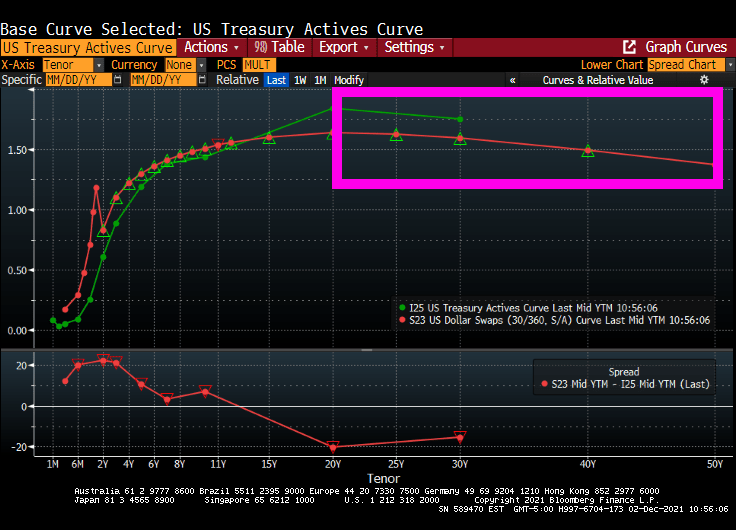

Now we have the US Treasury Actives curve inverting like the US Dollar Swaps curve after 20 years.

You must be logged in to post a comment.