Lots of volatility in markets culminating in a 15 basis point drop in the US Treasury Note yield.

Since the 10-year Treasury yield dropped only -2.7 basis points, the 10Y-2Y yield curve rose slightly to -38.87 basis points.

Confounded Interest – Anthony B. Sanders

Financial Markets And Real Estate

Lots of volatility in markets culminating in a 15 basis point drop in the US Treasury Note yield.

Since the 10-year Treasury yield dropped only -2.7 basis points, the 10Y-2Y yield curve rose slightly to -38.87 basis points.

The US July inflation report remains hot, hot, hot! While mortgage purchase and refinancing applications are not, not, not.

The US consumer price index rose 8.5% in July. And real average weekly growth remains burned by horrid inflation, at -3.6% YoY.

Source of inflation?

Headline inflation above estimates in 14 of last 16 months.

Data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending August 5, 2022 revealed that … the Refinance Index increased 4 percent from the previous week and was 82 percent lower than the same week one year ago. The seasonally adjusted Purchase Index decreased 1 percent from one week earlier. The unadjusted Purchase Index decreased 2 percent compared with the previous week and was 19 percent lower than the same week one year ago.

Mortgage applications are NOT hot, hot, hot.

The US Treasury 10Y-2Y yield curve is descending further into darkness (aka, inversion).

The 10Y-2Y yield curve hit the worst inversion since 2000 as the curve slope hit -47.7 basis points, inverting another -2.267 basis points today.

Yes, the 10Y-2Y Treasury yield curve is SCREAMING RECESSION.

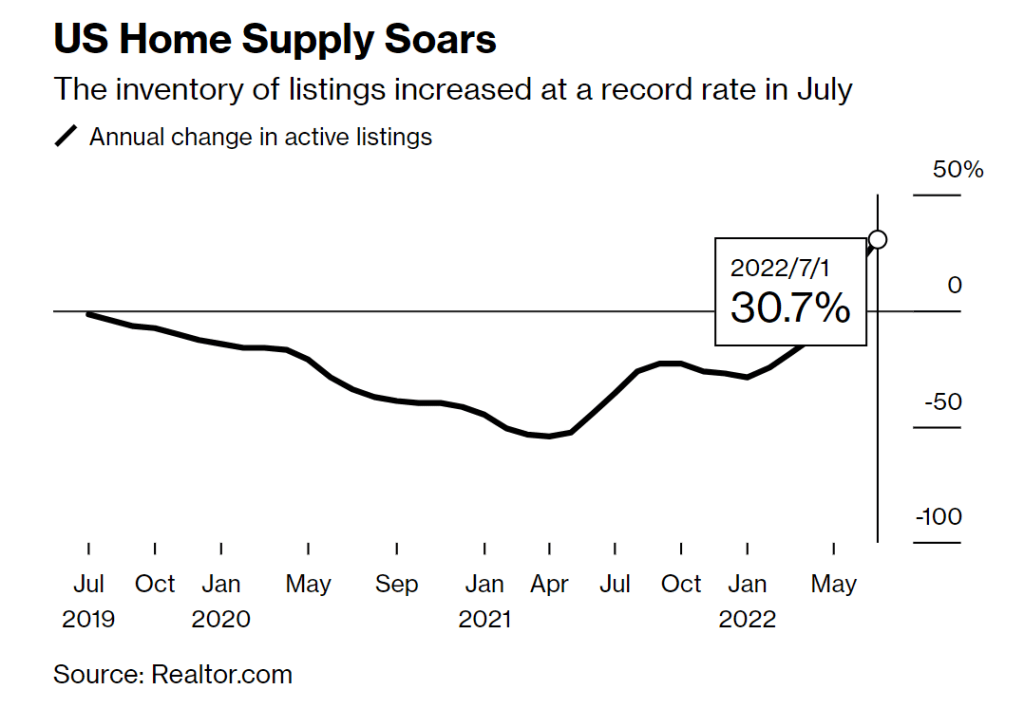

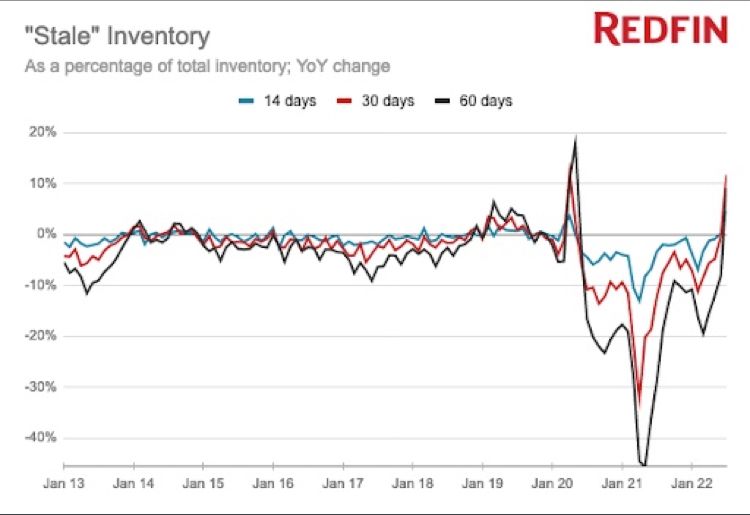

(Bloomberg) – Prashant Gopal – The supply of homes for sale across the US grew at a record rate last month, another sign that higher mortgage costs are cooling down the housing market.

The number of active listings nationwide jumped 31% from a year earlier, a record-high increase for a third straight month, according to a report Tuesday by Realtor.com.

And according to Redfin, stale inventory is accelerating.

The Federal Reserve is no friend of the US middle class and low wage worker.

US labor productivity declined in Q2, down -4.6% since Q1. At the same time, unit labor costs continue to soar at a rate of 10.8%.

You can see that The Federal Reserve has begun to SLOWLY reduce it balance sheet.

Somehow, I don’t think Biden’s team will be discussing today’s news, other than report that “It’s A Beautiful Day Today.”

The US housing market is simply unaffordable for millions of Americans. To illustrate the problem, here is a chart of the Case-Shiller National home price index less CPI YoY graphed against Average Hourly Wages less CPI YoY.

The gap between the REAL national home price index YoY and REAL US average hourly earnings YoY is near the largest since 1988. Inflation is making matters far worse since REAL average hourly earnings growth continues to decline.

The only thing positive to say is that REAL home price growth YoY is lower now than at the peak of the 2005 home price bubble that burst catastrophically.

Another “positive” is that the REAL 30-year mortgage rate has fallen to -3.23%. At the peak of the house price bubble in June 2005, the REAL 30-year mortgage rate was +2.58%. THAT is one big difference between the pre-2008 recession and today’s impending recession.

Here is your weekend update on Treasury and Mortgage markets.

The current US Treasury 10Y-2Y yield curve just slipped further into reversion at -40.299 basis points, screaming impending recession. Oddly, The Federal Reserve has been leaving its balance sheet of Agency Mortgage-backed Securities (MBS) in tact (green line).

On the mortgage front, Bankrate’s 30-year mortgage rate index rose to 5.60% while the affordability-friendly 5/1 Adjustable Rate Mortgage (ARM) rate rose to 4.21%.

Currently, a 5/1 ARM borrower can save 139 basis points over the traditional 30-year mortgage rate.

Have a wonderful weekend!

Today’s jobs report was … strange. While the US economy added more jobs than expected, we also saw labor force participation contract and real wage growth decline again.

The reaction in the bond market? US Treasury 10-year yields exploded by +14 basis points. As I used to tell my fixed-income students, any basis point jump or decline of 10 basis points or more is a BIG DEAL.

The implied target rate for The Fed (based on Fed Funds Futures) is now lower for the Jan 1, 2024 FOMC meeting (3.025%) than it is for the Sept 21, 2022 FOMC meeting (3.034%).

Mortgage rates? They will go up as The Fed removes its Brawndo, the economy mutilator.

The media is thrilled with today’s jobs report showing a sizzling 528k jobs added to the US economy. And with that, the media is cheering that recession fears are shrinking.

But hold on a second.

First, while 528k jobs were added in July (great news!), REAL average hourly earnings growth YoY fell to -3.8173. Why? Because the rate of inflation is greater than nominal average hourly earnings YoY of 5.2%. That is BAD.

This charts shows that inflation-adjusted (or real) wage growth is the worst in recorded history.

And the “sizzling” jobs report isn’t feeling any love in the bond market where the US Treasury yield curve (10Y-2Y) deepened its inversion to -37.593 basis points, a drop of -1.331 BPS. Note that the 10Y-2Y curve falls below 0% just prior to every recession.

Labor force participation actually fell to 62.1% from 62.2% in June.

I am assuming that The Fed will misread the jobs report and argue for LESS COWBELL.

After mortgage rates topped 6%, they settled back down with the global economic slowdown, but are on the rise again.

Bankrate’s 30-year mortgage rate index rose to 5.57% after rising above 6% in June 2022. Mortgage rates are up 92% under the team of Biden and Fed Chair Powell as The Fed tries to extinguish the inflation fire cause by 1) excessive Fed stimulus, 2) Biden’s anti-fossil fuel policies and 3) Biden/Congress’ reckless spending.

The Fed still has not shrunk its balance sheet yet and home price growth is still soaring.

The US Treasury 10Y-2Y yield curve inversion just worsened to -38.503, the most inverted since 2000.

Over the longer-term, the US Treasury 10Y-2Y yield curve is the most inverted since 2000. Remember, the 10Y-2Y yield curve inverts prior to a recession.

In terms of putting out the inflation fire, The Fed is acting more like The Three Stooges.

Federal Reserve Bank of St. Louis President James Bullard said he favors a strategy of “front-loading” big interest-rate hikes, and repeated he wants to end the year at 3.75% to 4% to counter the hottest inflation in four decades.

“We still have some ways to go here to get to restrictive monetary policy,” Bullard said in a CNBC interview Tuesday.

“I’ve argued now with the hotter inflation numbers in the spring, we should get to 3.75% to 4% this year. Exactly whether you want to do that at a particular meeting or some other meeting is a great question. I’ve liked front-loading. I think it enhances our inflation-fighting credentials.”

Federal Reserve presidents including Bullard speaking this week emphasized that inflation at a 40-year high has yet to slow, and pushed back against the perception the central bank was pivoting to a less aggressive phase of tightening monetary policy. Fed Chair Jerome Powell last week cited Federal Open Market Committee forecasts that the Fed would raise rates to 3.4% at the end of the year and 3.8% in 2023.

Bullard wants to raise rates to boost Fed credibility?? When flexible price inflation is at 20.13% and The Fed is awfully slow to shrink their balance sheet??? What credibility is he talking about????

You must be logged in to post a comment.