Surprise! Just in time for the November election, this is a negative surprise that Biden doesn’t want to hear.

The Citi Economic Surprise index crashed to -7.30, the lowest since January 2023.

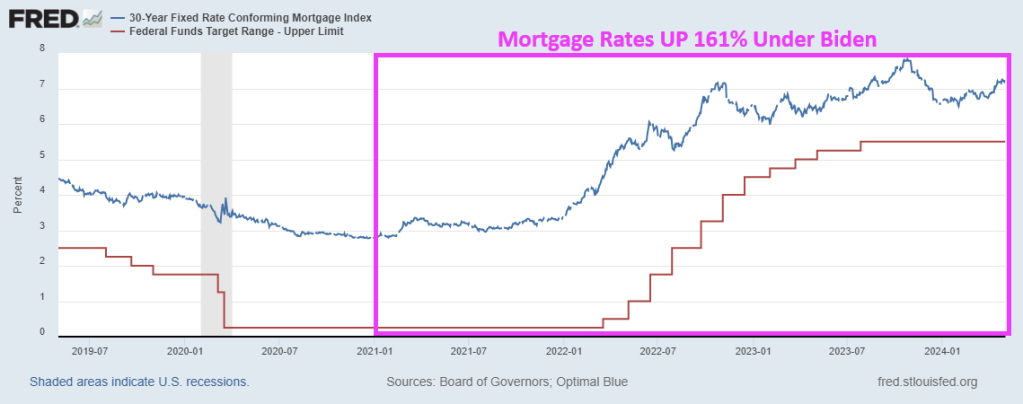

Under Biden’s leadership (hell, he and his family already own several mansions … on a Senator’s pay), home prices are up 32% under Biden and mortgage rates are up a staggering 160%.

Getting young households who rent to buy a home in this environment will require magic.

There are TWO taxes that are hitting people making under $400,000 per year. First, the INFLATION tax coming from Biden’s/Congresses spending binge, The Fed printing gobs of money, and insane regulations.

Biden and his mouthpieces like Karine Jean Pierre (KJP) claim that Biden inherited inflation from Trump. FALSE. Inflation was only 1.3% YoY in December 2020. Inflation was 3.5% YoY in March 2024, an increase of 166% over Trump’s final month in office. THAT is one heck of an inflation tax.

In House testimony, Treasury Secretary Janet Yellen (falsely) claimed that Biden’s massive tax increase won’t hit middle class households. That is a plain lie. the Tax Foundation said that someone who’s married, two kids, making $85,000 would pay $1,700 more in taxes. A married couple with two children making $165,000 annually would pay $2,450.50 more than in the previous year, while a family with three kids pulling in $200,000 per year will shell out almost $7,500 more per year.

So much for Biden’s “No one making under $400,000 will pay and additional penny of tax.” Between the inflation tax and Biden letting Trump’s Tax Cuts and Jobs Act’s (TCJA) expire, people making under $400,000 per year will get scalded. All so Biden/Congress can keep spending on Ukraine, fund endless wars, and buy countries cooperation with the US.

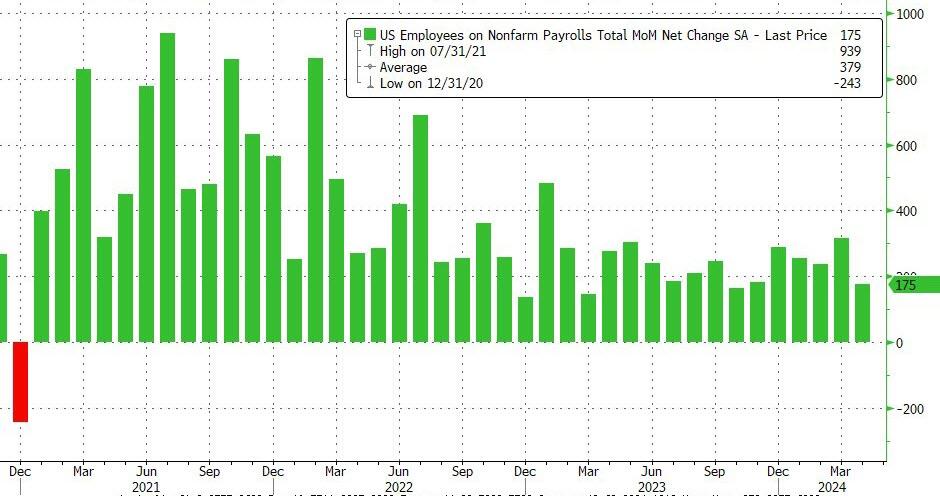

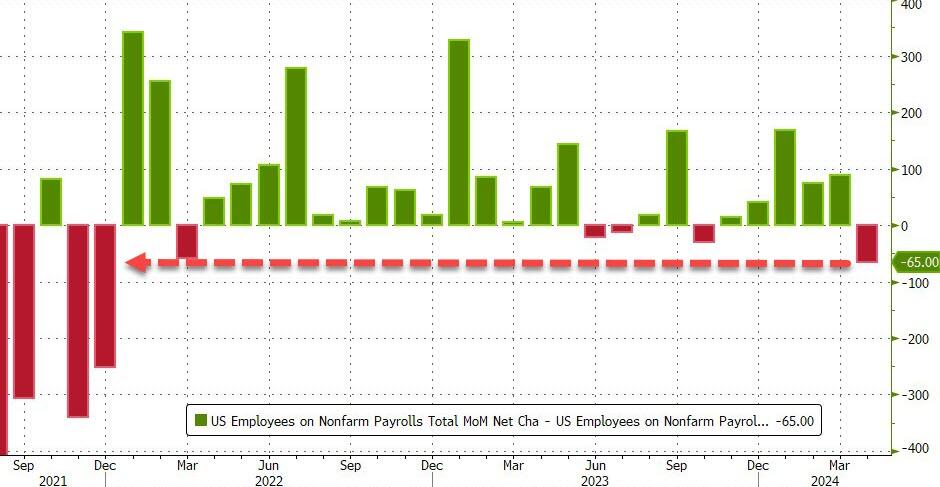

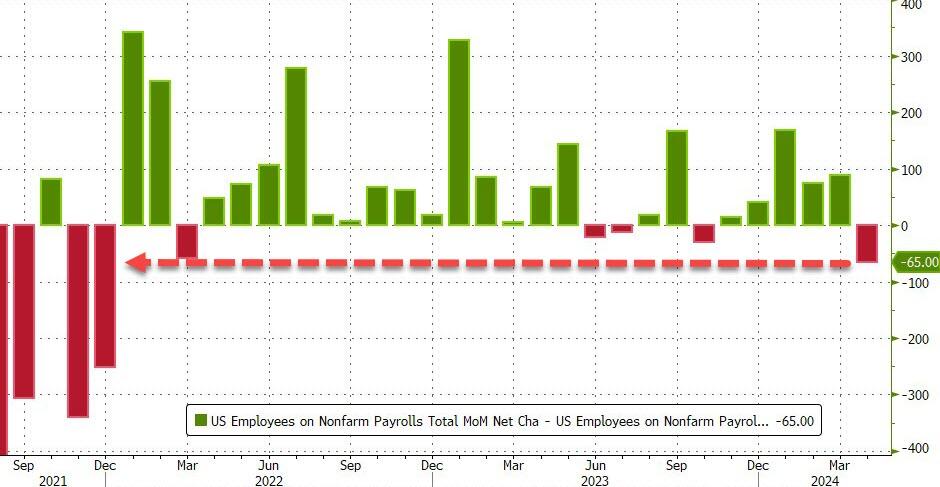

.. and a huge miss to estimates of 240K… in fact, as shown below, this was the biggest miss since Dec 2021

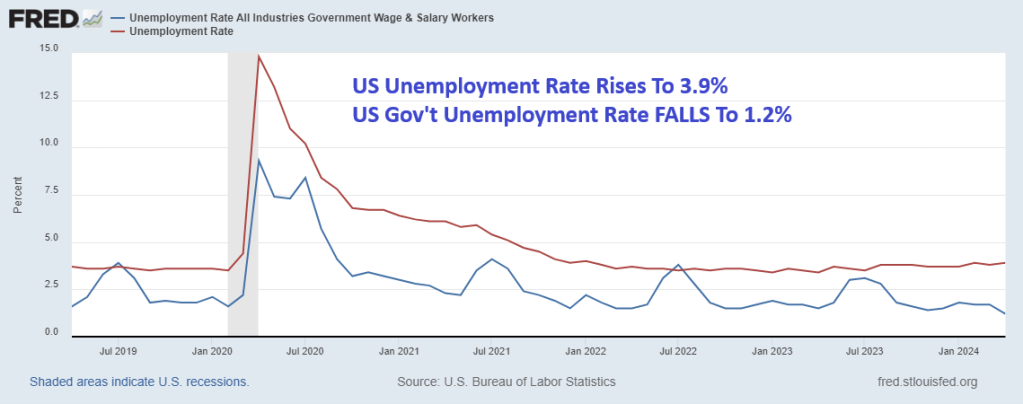

The weakness was pervasive, and while payrolls were a huge miss, the unemployment rate also rose more than expected, from 3.8% to 3.9%, vs estimates of an unchanged print.

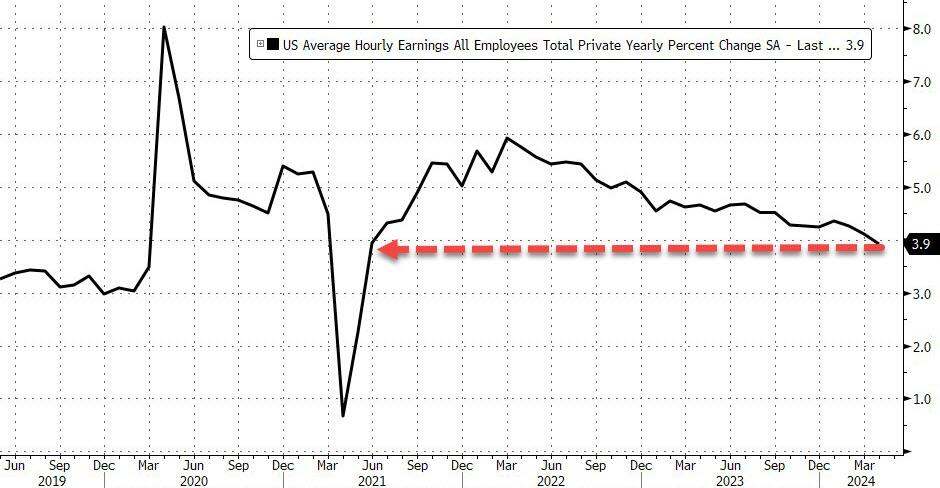

Wages also eased back with average hourly earnings rising 0.2% MoM, below the expected 0.3% increase and down from last month’s 0.3% print. On an annual basis, earnings rose 3.9%, down from 4.1% last month and below the 4.0% estimate.

Yellen: Mortgage rates have been so low for so long that it’s created a lock-in effect where people don’t want to sell their homes to buy new ones for fear of losing their attractive rates.

That’s made it “almost impossible” for first-time homebuyers to enter the housing market, U.S. Treasury Secretary Janet Yellen said during her testimony before the House Ways and Means Committee.

Now hold on a minute, Janet. YOU were the one that kept rates too low for too long as Federal Reserve Chair.

What was her record on mortgage rates? Yellen kept the Fed target rate (upper bound) at 25 basis points under Obama/Biden until December 2015, so only one rate hike under Obama/Biden. Then came the election of Donald Trump in November 2016. Then Yellen raised The Fed target rate 4 times after Trump was elected.

Mortgage rates fell to 3.78% by November 2017, so Yellen helped keep mortgage rates low. But mortgage rates soared after Trump’s election to 4.22% by the end of her term.

There are other reasons why first-time homeownership is so difficult, like local NIMBY (not in my back yard) policies and the absolutely lousy labor market.

She added that Biden’s massive tax increase won’t hit middle class households (other than the massive INFLATION tax that was levied by Biden). That is a plain lie. the Tax Foundation says that someone who’s married, two kids, making $85,000 would pay $1,700 more in taxes. A married couple with two children making $165,000 annually would pay $2,450.50 more than in the previous year, while a family with three kids pulling in $200,000 per year will shell out almost $7,500 more per year.

So much for Biden’s “No one making under $400,000 will pay and additional penny of tax.”

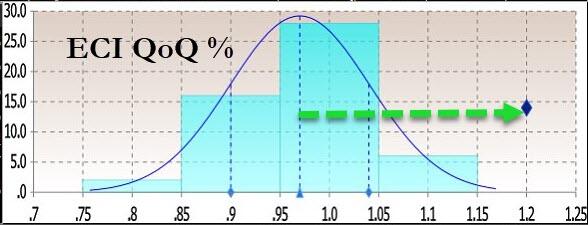

On the flip-side of that – and echoing the market-worrying ECI data earlier this week – Unit Labor Costs soared 4.7% in Q1 (well above the 4.0% expected and the 0.4% rise in Q4)…

Source: Bloomberg

So wage inflation is confirmed – rising at the fastest pace in a year – as all the gains we have been told to expect from AI just aren’t there in the data.

While quarterly productivity figures are quite volatile, a sustained slowdown represents another hurdle for the Federal Reserve’s inflation fight. With interest rates expected to stay at a two-decade high for awhile longer, business investment in equipment will likely continue to be a weak factor in overall economic growth.

Today’s data corroborates other data that showed gross domestic product cooled in the first quarter while employment costs rose by the most in a year. As a result, inflation is proving stubborn, supporting the Fed’s pivot to a more hawkish stance that will keep interest rates higher for longer than anticipated.

Of course, Fed Chair Powell told us yesterday that he “doesn’t see the stag or the flation” in US data…

Perhaps Cazadores tequila should be the official drink of the Biden Administration. It has the “stag” on the label and it is produced in Mexico … who Biden can’t (or won’t) stand up to.

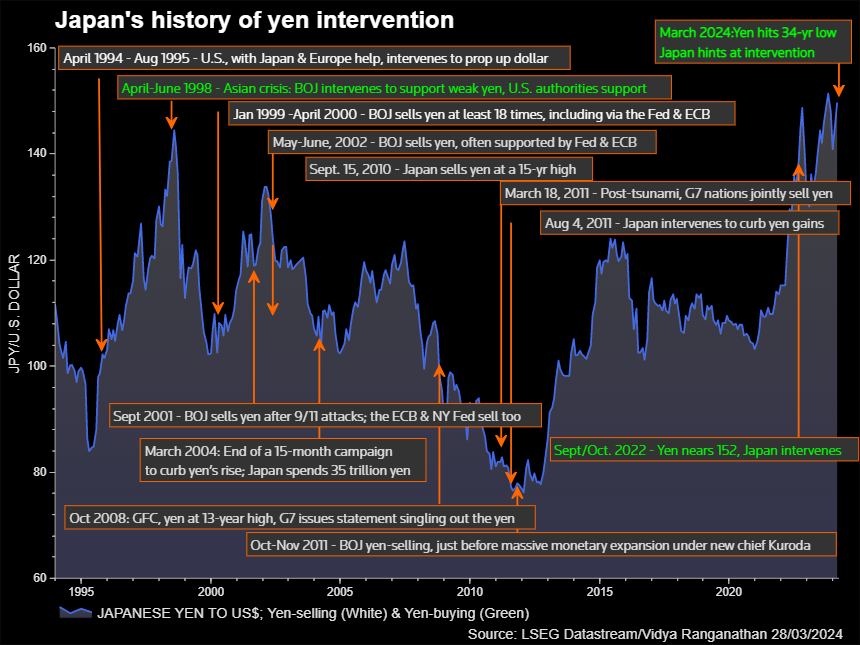

Tokyo’s latest entry into the market was likely around ¥3.5 trillion ($22.5 billion), based on a comparison of Bank of Japan accounts and money broker forecasts.

The BOJ reported Thursday that its current account will probably fall ¥4.36 trillion due to fiscal factors on the next business day of Tuesday. That compares with the ¥833 billion average forecast by money brokers of what the number would be without intervention.

The figures, released less than a day after the yen jumped sharply during US trading hours, indicate that Japanese authorities made the unusual move of stepping into the market shortly after a Federal Reserve meeting when investors were still digesting the announcement. That would signal the finance ministry is taking an increasingly aggressive stance in what could become a prolonged fight to support the yen.

“With Japanese holidays and US jobs data coming up, it was a very good time for the authorities to tackle speculators,” said Yuya Kikkawa, an economist at Meiji Yasuda Research Institute. “This will have a great impact on the market. I sense a strong determination by the authorities to defend the 160-yen-per-dollar line.”

The latest swing in the yen follows a similarly sudden jump on Monday. Central bank accounts suggested Monday’s move was likely an intervention by Tokyo worth around ¥5.5 trillion, close to the daily record of ¥5.6 trillion set in October 2022.

Ahead of the move late Wednesday in New York and early Thursday in Tokyo, Central Tanshi Co. and Totan Research Co. had forecast a ¥700 billion decline in the BOJ’s current account balance due to fiscal factors including government bond issuance and tax payments. Ueda Yagi Tanshi projected the balance to drop by ¥1.1 trillion.

The calculations based on a comparison of those estimates and the central bank accounts offer only ballpark figures rather than specific amounts. Similar analysis proved accurate in showing that a jump in the yen in jittery markets in October 2023 was not the result of Japan stepping in to buy the currency.

The calculations also estimated the size of intervention on Oct. 21, 2022 at around ¥5.5 trillion, closely matching the actual amount.

An official monthly figure for the size of intervention will come out on May 31. Traders will need to wait until August or later to see daily operation data.

Japan’s top currency official Masato Kanda declined Thursday to comment on whether the finance ministry had intervened two hours earlier in Tokyo, when the yen strengthened sharply against the dollar. Japan’s currency briefly touched 153.04 from around the 157.50 mark.

Kanda oversaw the previous cycle of interventions in 2022. The ministry bought the yen around 30 minutes after the BOJ’s governor press conference ended in September that year. Another round of moves came a month later with back-to-back business day interventions.

The pattern of Japanese officials declining to comment is aimed at keeping market participants in the dark. A lack of immediate clarity may help keep traders more on edge and less willing to bet against the yen even if the ministry hasn’t actually taken action.

“By acting right after the Fed decision and outside of Japan hours, they dished out a warning that they are in a position to intervene 24 hours a day,” said Hirofumi Suzuki, chief FX strategist at Sumitomo Mitsui Banking Corp.

“We are still waiting for US employment figures during the Golden Week holidays and depending on the outcome of that data, there is a risk of further intervention,” he said.

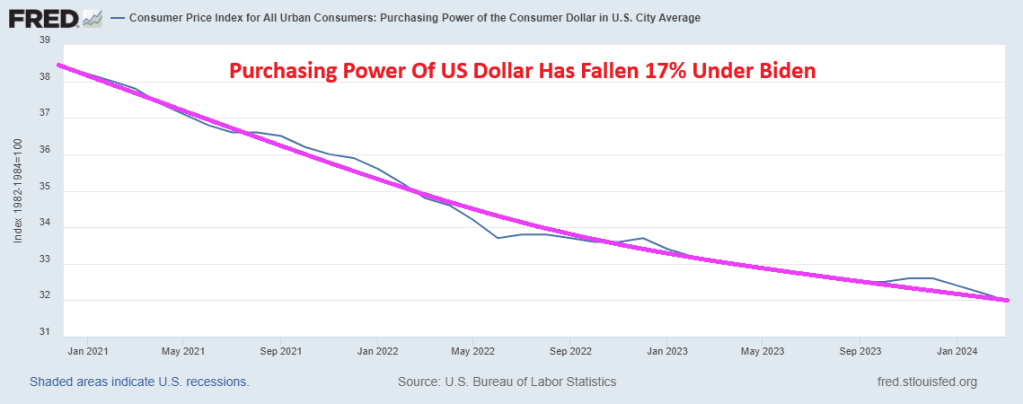

The US is having its own currency problems under Biden with its own bad fiscal and monetary polcies. The Purchasing Power of the US Dollars has fallen 17% under Biden.

Housing in the US is simply unaffordable, particularly after HUD levied new regulation rising the cost of new housing up to $31,000. Wait for this to kick into the data for mortgage demand!

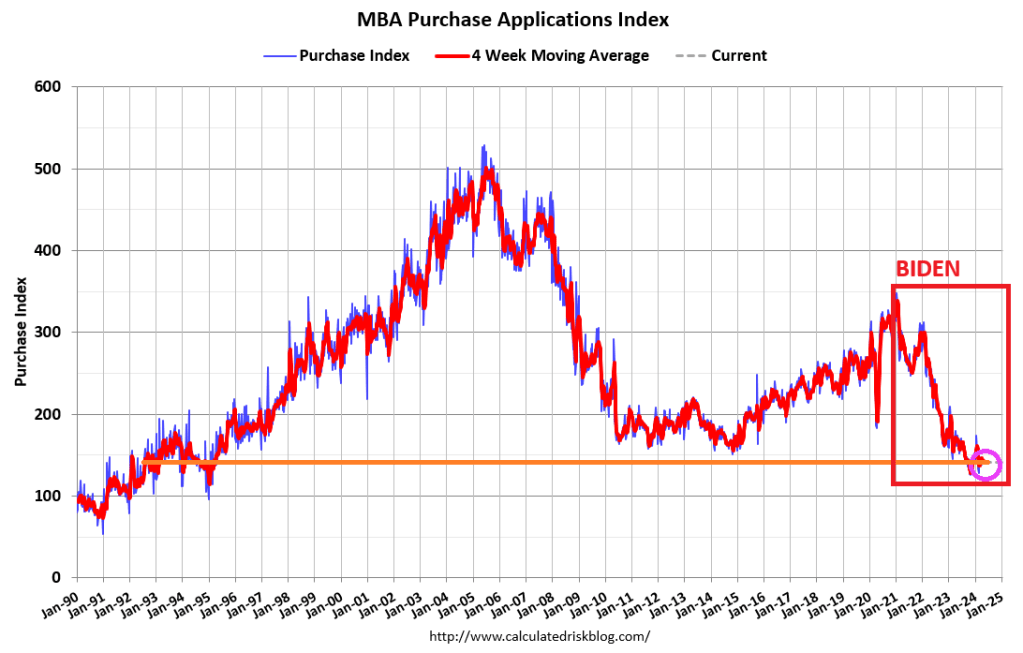

Mortgage applications decreased 2.3 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending April 26, 2024.

The Market Composite Index, a measure of mortgage loan application volume, decreased 2.3 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index decreased 1.4 percent compared with the previous week. The seasonally adjusted Purchase Index decreased 2 percent from one week earlier. The unadjusted Purchase Index decreased 1 percent compared with the previous week and was14 percent lower than the same week one year ago.

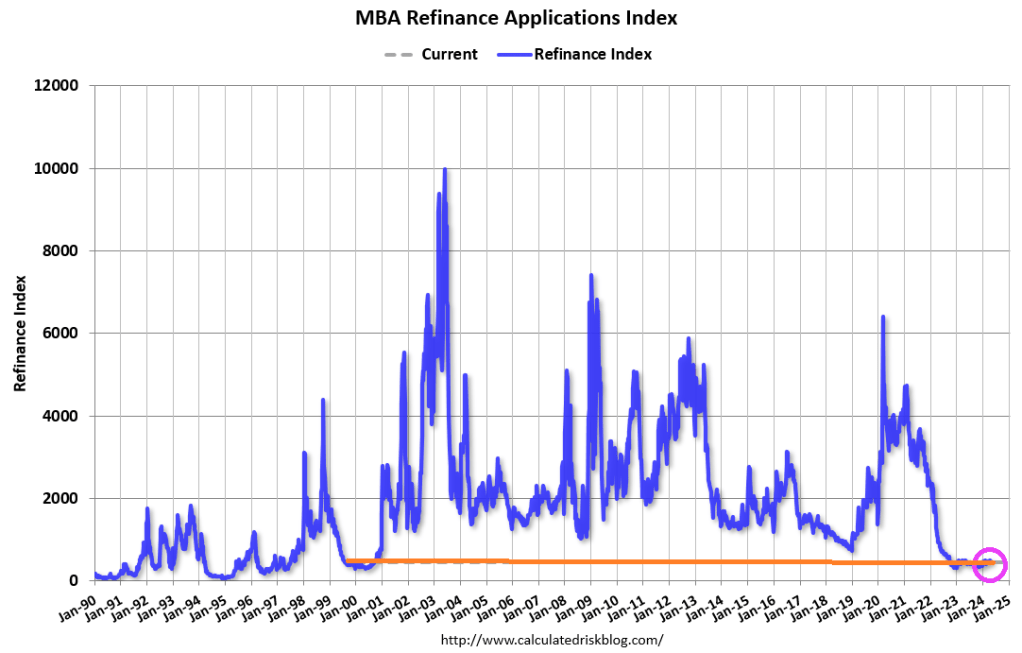

The Refinance Index decreased 3 percent from the previous week and was 1 percent lower than the same week one year ago.

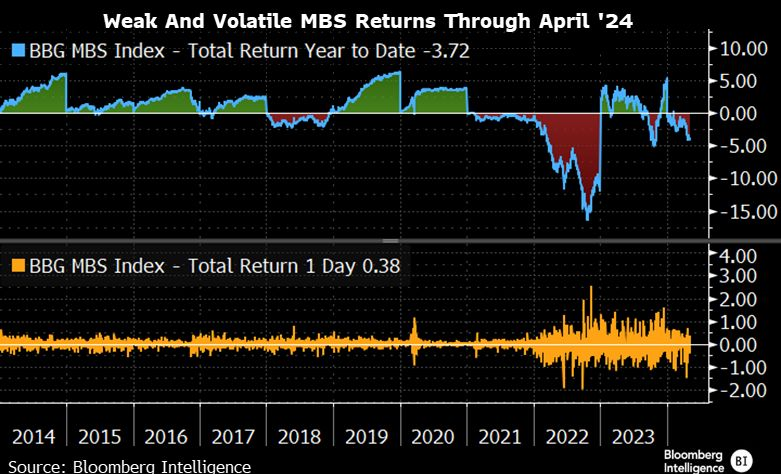

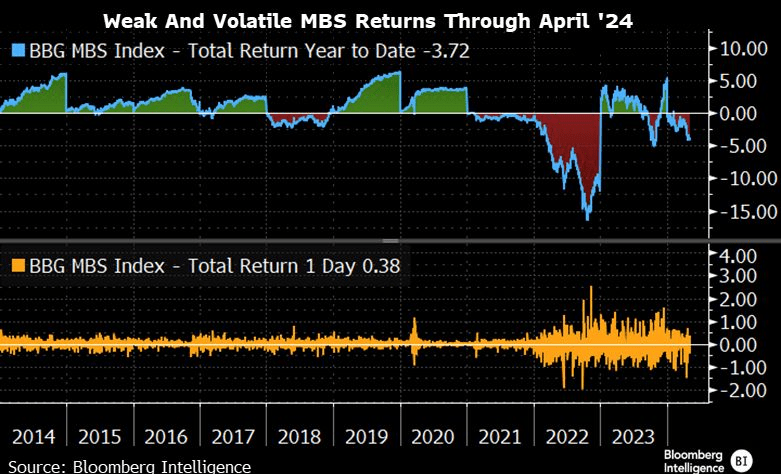

MBS returns are weak and volatile.

How is the Biden Regime making homeownership more affordable? They aren’t. The are using regulations, to drive the cost of new housing way up. New HUD energy rules will raise the cost of home construction by imposing stricter building codes. The National Association of Home Builders says the energy rules can add as much as $31,000 to the price of a new home. Payback time is 90 years (how long it will take the recoup the initial investment).

Under Biden’s “leadership” we are all addicted to gov. But at least Ukraine and Zelenskyy will be getting a guaranteed 10 years of financial support from the US … while E Palestine Ohio and Maui remain destroyed.

Janet Yellen, world class propagandist (US version of Baghdad Bob) and US Treasury Secretary under Biden, was so wrong about inflation. Instead of being “transitory”, turns out to be seemingly permanent.

Today’s Case-Shiller home price report was released for February. The National Home Price index was up 6.4% year-over-year. But look at the explosion of M2 Money and home prices. Hmm.

If we look at home prices and M2 Money on a year-over-year (YoY) basis, we can see the surge in money printing with COVID and the corresponding surge in home prices. As M2 Money growth slowed, the Case-Shiller National HPI slowed as well … until The Fed slowed the declined in M2 Money growth resulting in rising home price growth again.

So, The Fed will likely have to keep on printing. You can see Janet Yellen dancing to the thought of printing more money.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

You must be logged in to post a comment.