A picture is worth a thousand words.

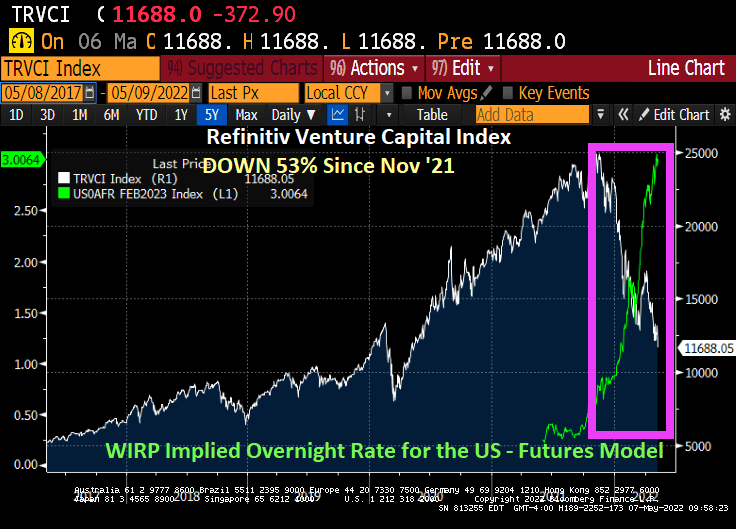

Nothing has been the same since Covid and The Federal Reserve’s massive overreaction to the government shutdowns of the economy.

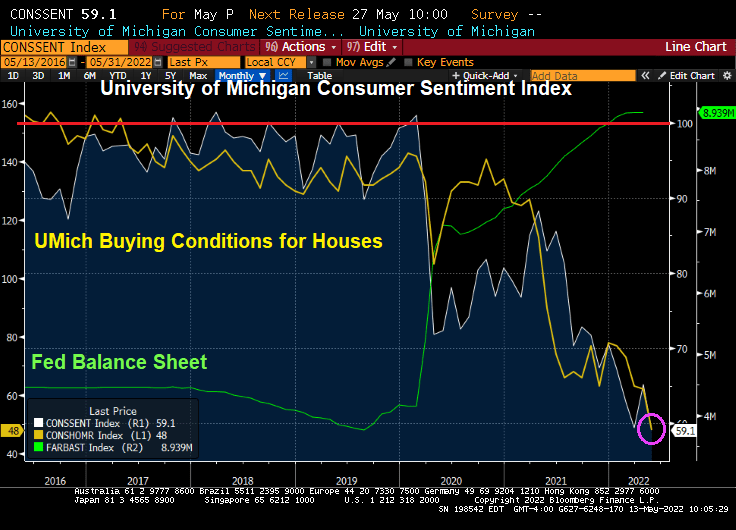

Notice how the University of Michigan Consumer Sentiment Index (white line) has plunged since Covid and the ensuing rise in inflation. University of Michigan’s Buying Conditions for Houses has also plunged to new depths.

Yes, Bidenflation is just killing us.

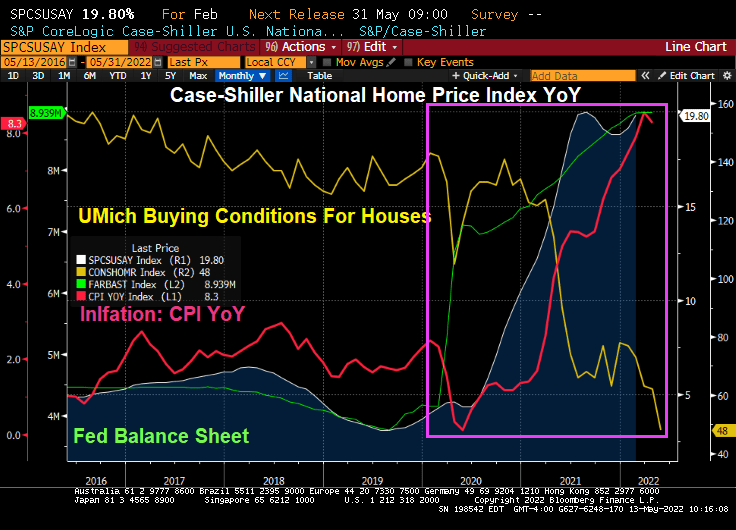

Rising inflation (highest in 40 years) and hottest home price bubble (even hotter than the infamous housing bubble of 2005-2007) AND rising mortgage rates have placed a damper on home buying sentiment.

The theme song for the Biden economy is The Blasters’ Dark Night.

You must be logged in to post a comment.