Calamity Jay Powell testified in front of the US Senate Banking Committee. He rattled markets by going hawkish about inflation, then gave The Fed an out by playing the COVID CARD (the latest Omicron Variant). Aka, the DEATH CARD.

Federal Reserve Chair Jerome Powell said the strong U.S. economy and elevated inflation could warrant ending the central bank’s asset purchases sooner than planned next year, though the new omicron strain of Covid-19 poses a fresh risk to the outlook.

“It is appropriate, I think, for us to discuss at out next meeting, which is in a couple of weeks, whether it will be appropriate to wrap up our purchases a few months earlier,” Powell said Tuesday. “In those two weeks we are going to get more data and learn more about the new variant.”

Powell made the comment in response to questions during a Senate Banking Committee hearing in Washington. The Fed is currently scheduled to complete its asset-purchase program in mid-2022 under a plan announced at the start of November; policy makers next meet Dec. 14-15, where they could make a decision to accelerate the tapering.

On his remarks, the stock market puked.

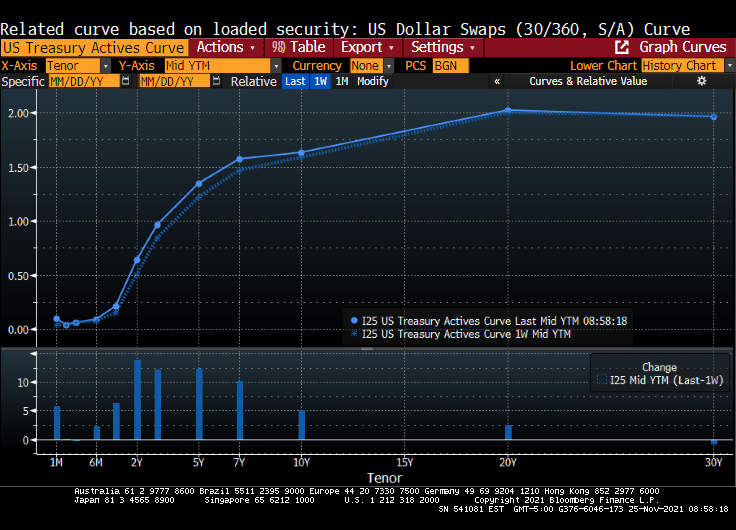

Well, if Powell followed the Taylor Rule, he would really scare Congress with raising The Fed Funds Target Rate to 14.94% based on an inflation rate of 6.20%.

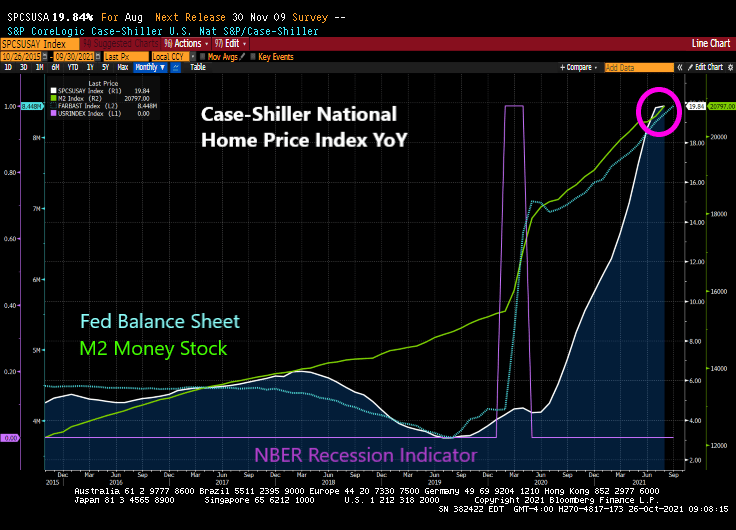

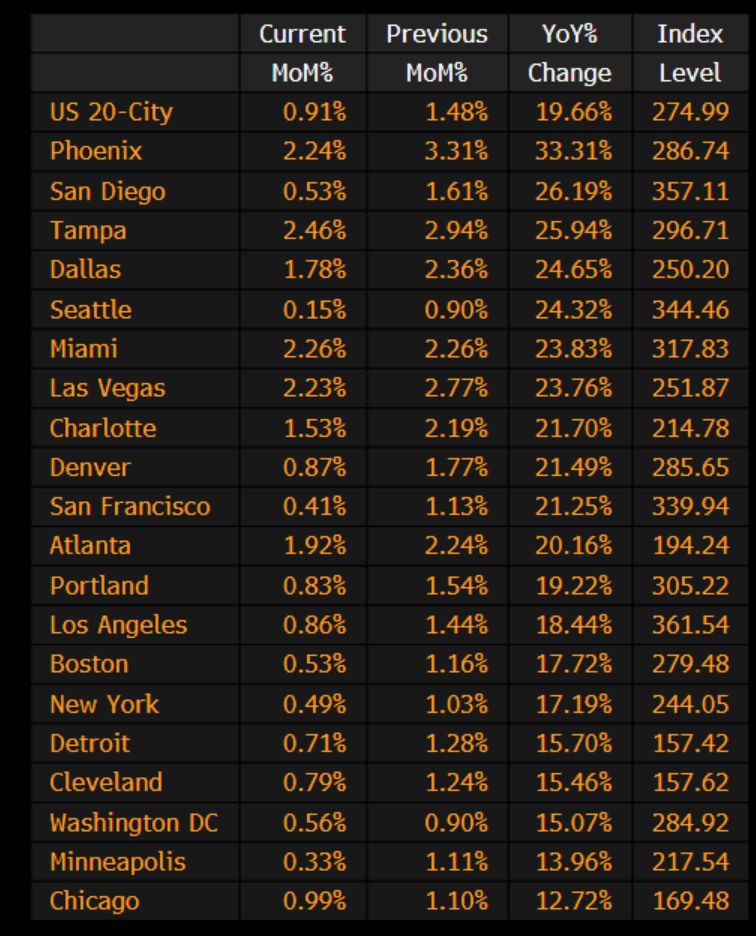

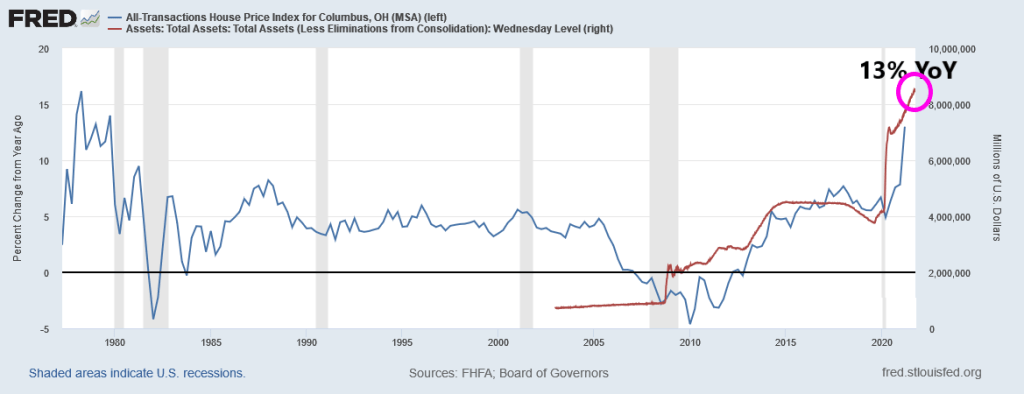

And then we have HOUSE price inflation of near 20%. But The Fed doesn’t consider than inflation.

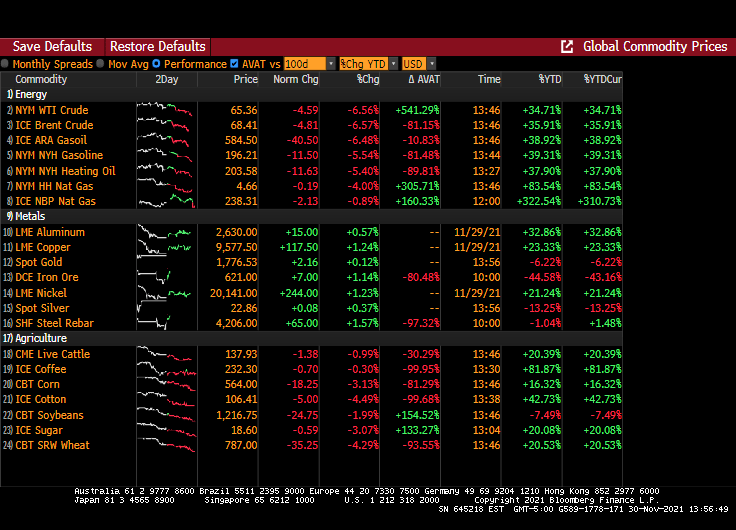

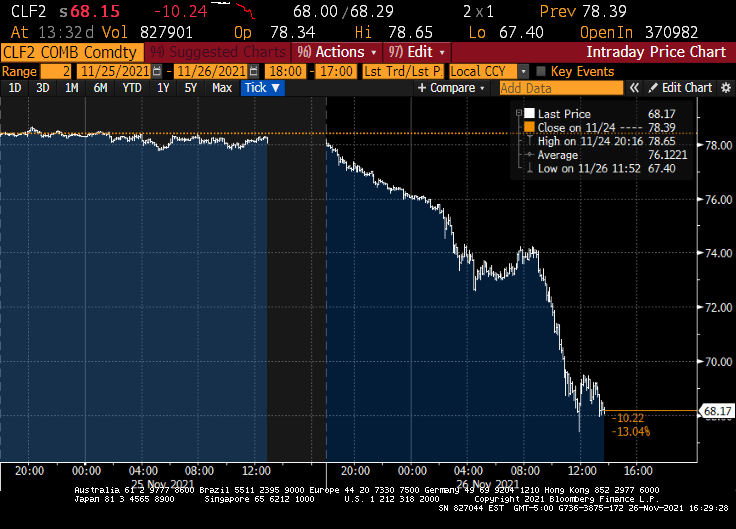

Then we have oil prices retreating -4.59%. Not, not due to Biden releasing the National Petroleum Reserve (NPR). Rather it is FEAR of The Fed raising rates and a corresponding slowdown in economic growth.

Calamity Jay Powell.

You must be logged in to post a comment.