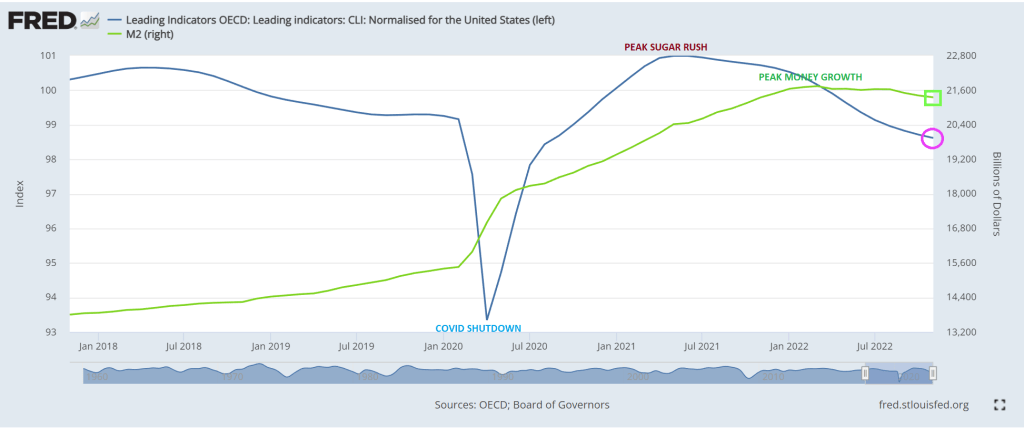

The 2020 Covid outbreak and the resulting government shutdowns and school closures begat a Washington DC spending spree and Federal Reserve monetary stimulus barrage unlike anything other time in history. Congress and Administrations love to spend other people’s money, but as Rahm Emanuel once said “You never let a serious crisis go to waste. And what I mean by that it’s an opportunity to do things you think you could not do before” And wow, did they ever binge spend and expand the M2 Money supply. I call it “The Great Dislocation” of the economy and we never recovered from it.

Or as Ray Wylie Hubbard sang, “Drinking with my low life companions, dancin’ with a woman who is not my wife.” This should be the theme song for Washington DC and their manic spending.

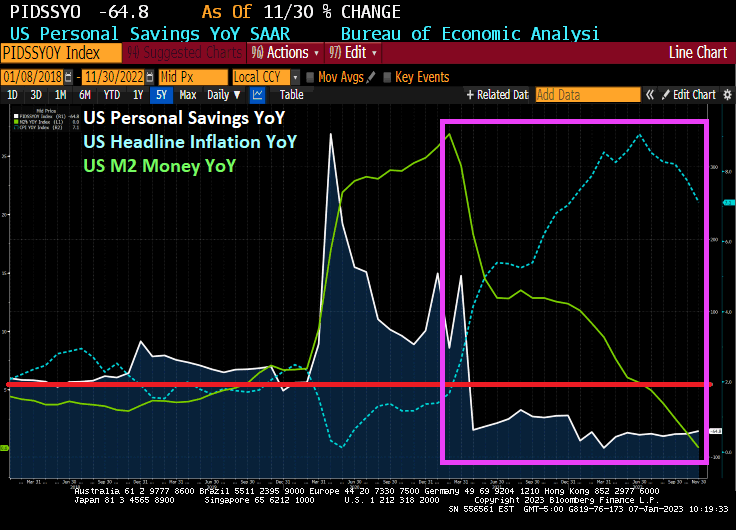

But after the massive spending splurges and Fed monetary stimultypto, The Fed finally started withdrawing “the punch bowl” to combat inflation. M2 Money growth year-over-year (YoY) is now 0%. And with inflation, US average weekly earnings growth YoY turned negativc and has been negative for 21 straight months.

After the spending explosion under Pelosi/Schumer and Powell’s monetary, M2 Money velocity (GDP/M2 Money) crashed to it lowest level in history. So now we have depressed money velocity and no M2 money growth. And the US still has 21 straight months of negative weekly earnings growth.

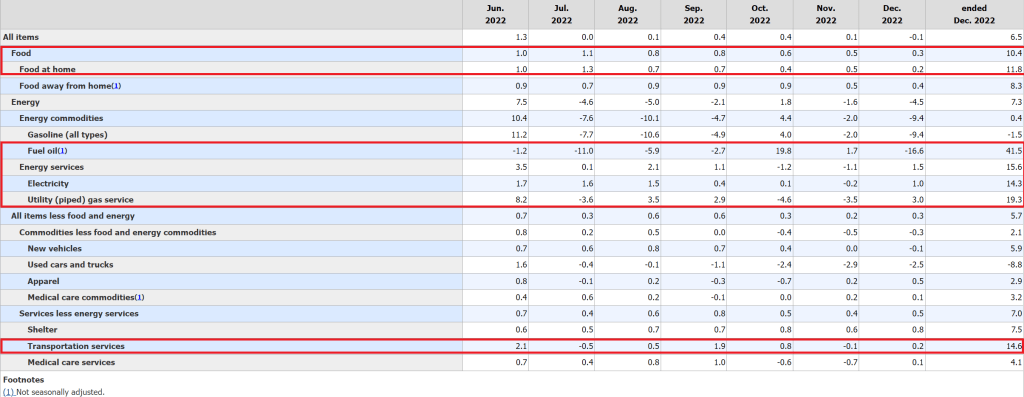

But former Fed Chair and current Secretary of Treasury Janet Yellen is pleased that inflation is FINALLY slowing which Yellen attributes to relaxing supply chains. Or is it declining M2 Money growth, Janet?

Now that the Federal government’s spending spree and The Fed’s monetary stimulypto dislocated the US economy, we are headed for a recession with no ammunition left in The Fed’s arsenal.

After all. The Federal Reserve has been destroying consumer purchasing power since 1913. And we may be at the end of The Fed’s monetary rope.

Even worse, we have Joe Biden as President, who curiously has been found to have classified documents in his possession from when he was Vice President, at least, at two locations (his Wilmington DL home that his son Hunter had access to and the now infamous Penn Biden Center in Washington DC). Even worse, Biden seems to be talking to dead world leaders like Germany’s Schmidt and France’s Mitterand.

Knowing Biden’s penchant for blatant lying and carelessness, I wouldn’t be surprised if this is a stack of classified documents on the table during his meeting with Treasury Secretary Janet Yellen.

Let’s hope Biden isn’t saying that he is talking to late Robert Kennedy, the former US Attorney General.

You must be logged in to post a comment.