Housing in the US is simply unaffordable, particularly after HUD levied new regulation rising the cost of new housing up to $31,000. Wait for this to kick into the data for mortgage demand!

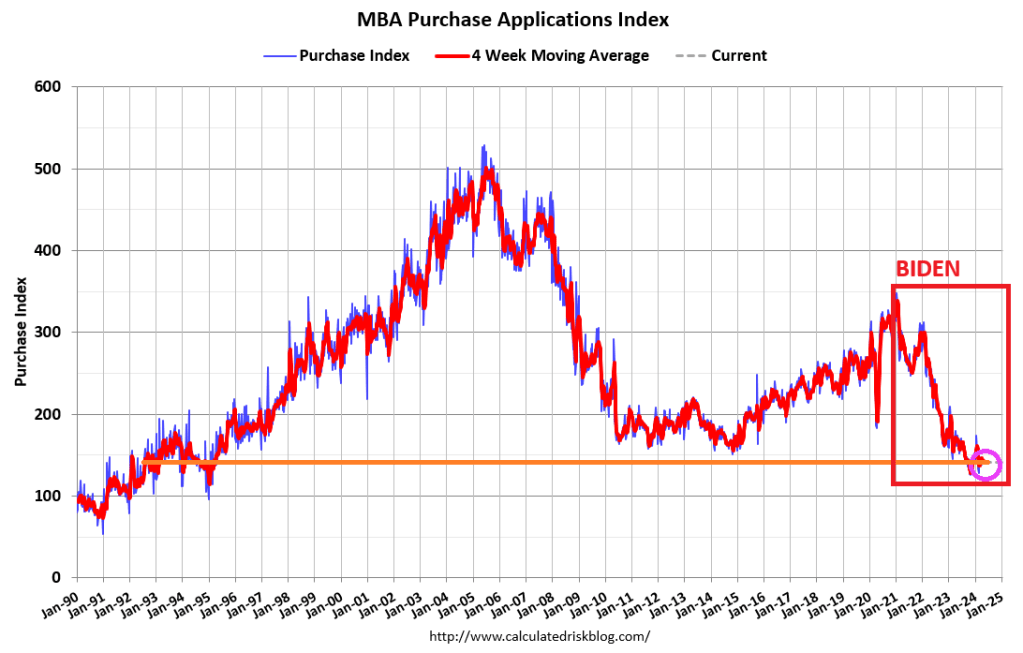

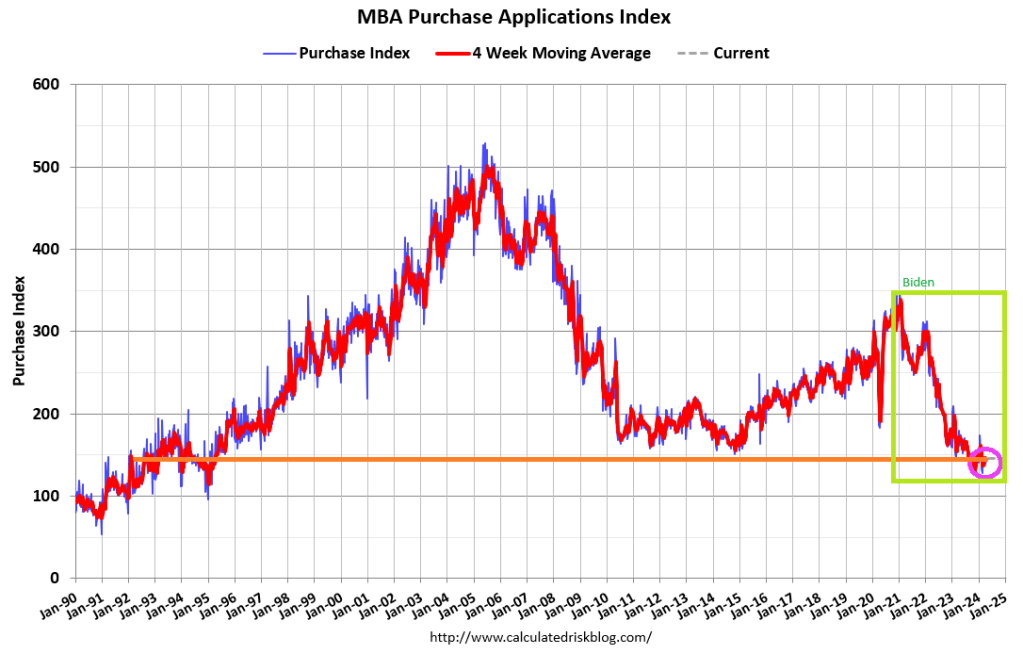

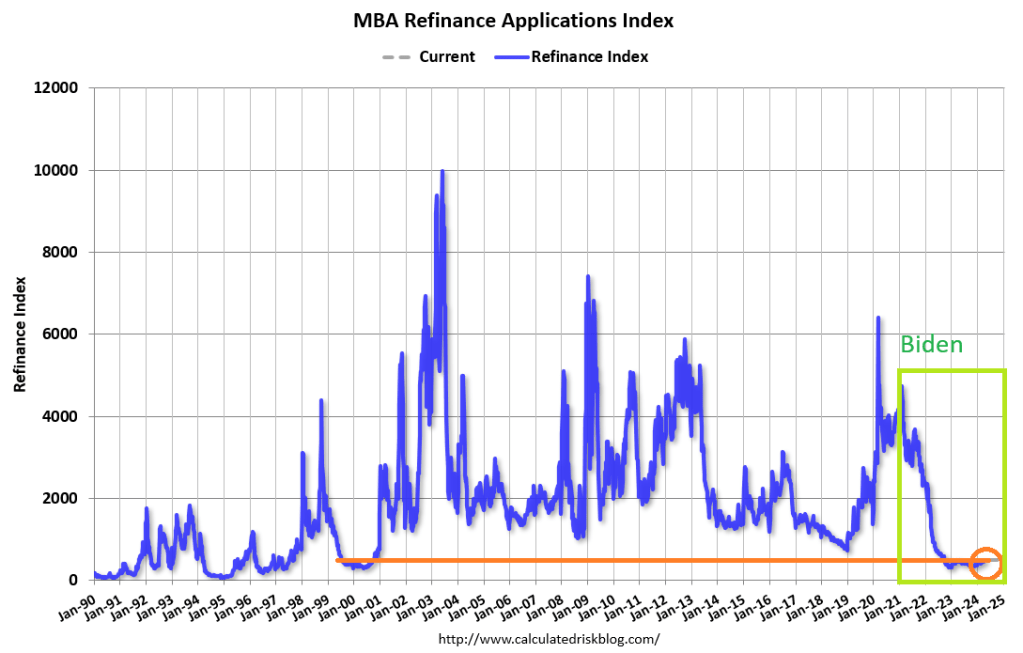

Mortgage applications decreased 2.3 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending April 26, 2024.

The Market Composite Index, a measure of mortgage loan application volume, decreased 2.3 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index decreased 1.4 percent compared with the previous week. The seasonally adjusted Purchase Index decreased 2 percent from one week earlier. The unadjusted Purchase Index decreased 1 percent compared with the previous week and was14 percent lower than the same week one year ago.

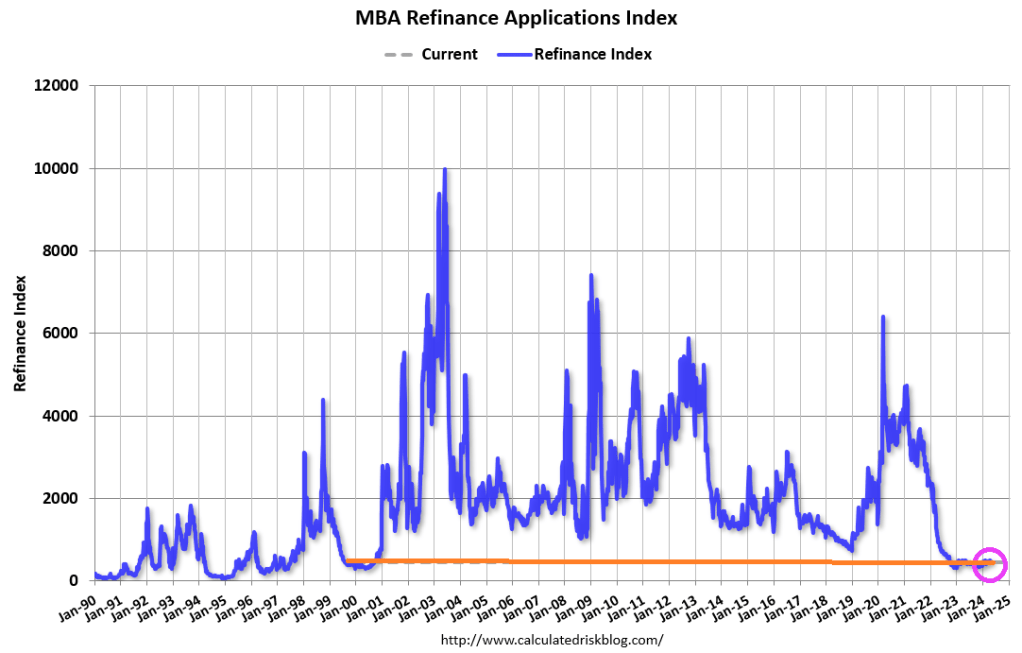

The Refinance Index decreased 3 percent from the previous week and was 1 percent lower than the same week one year ago.

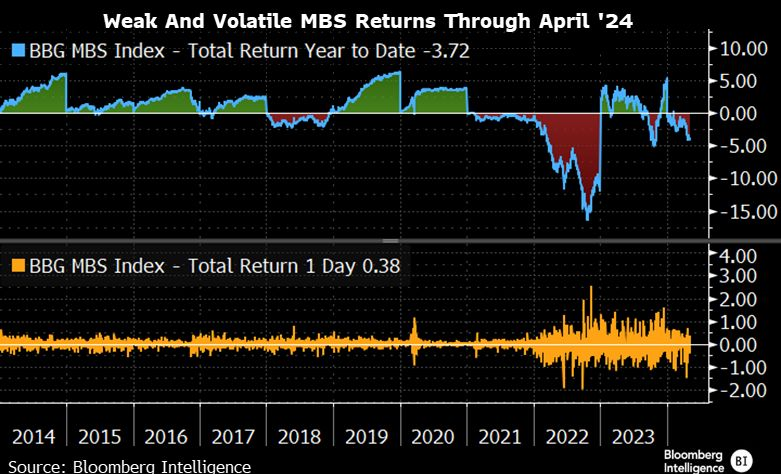

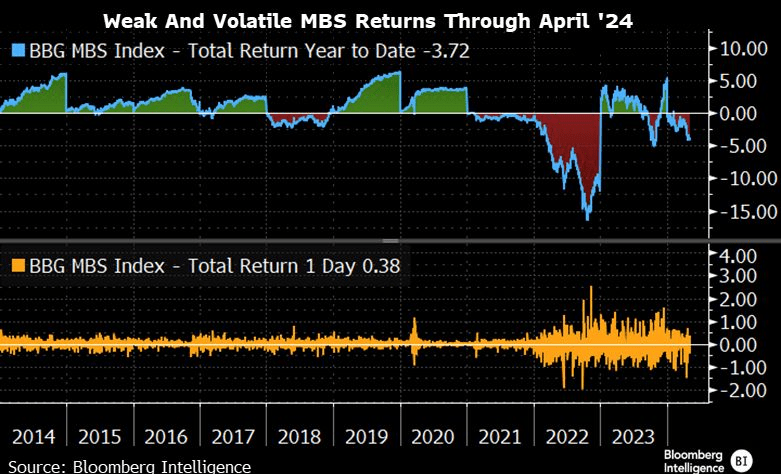

MBS returns are weak and volatile.

How is the Biden Regime making homeownership more affordable? They aren’t. The are using regulations, to drive the cost of new housing way up. New HUD energy rules will raise the cost of home construction by imposing stricter building codes. The National Association of Home Builders says the energy rules can add as much as $31,000 to the price of a new home. Payback time is 90 years (how long it will take the recoup the initial investment).

Under Biden’s “leadership” we are all addicted to gov. But at least Ukraine and Zelenskyy will be getting a guaranteed 10 years of financial support from the US … while E Palestine Ohio and Maui remain destroyed.

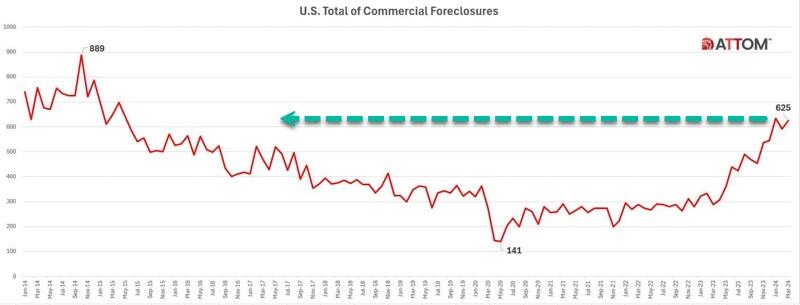

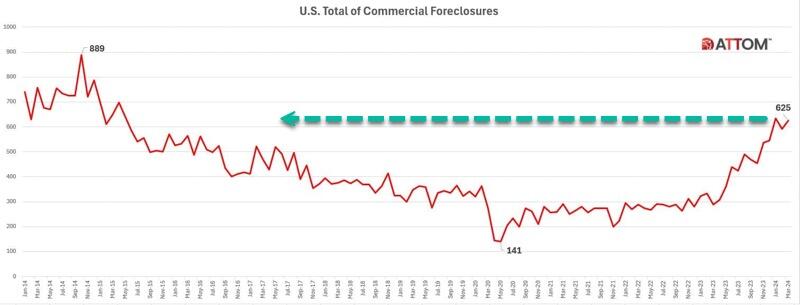

The latest report from real estate data provider ATTOM shows CRE foreclosures topped 625 in March, up 6% from February and 117% from the same period last year.

ATTOM has been tracking commercial foreclosures since 2014. The number of foreclosures is approaching the peak of 889 in October 2014.

“California began experiencing a notable rise in commercial foreclosures in November 2023, surpassing 100 cases and continuing to escalate thereafter,” the report said.

New York, Florida, Texas, and New Jersey also showed increases in CRE foreclosures last month.

Regional banks provide a bulk of the financing for the space. The ongoing mess in the lending space due to tighter conditions adds pressure to the CRE downturn. Banks are expected to set aside more money to cover potential CRE losses.

Last month, Federal Reserve Chair Jerome Powell testified on Capitol Hill, “We have identified the banks that have high commercial real estate concentrations, particularly office and retail and other ones that have been affected a lot,” adding, “This is a problem that we’ll be working on for years more, I’m sure. There will be bank failures, but not the big banks.”

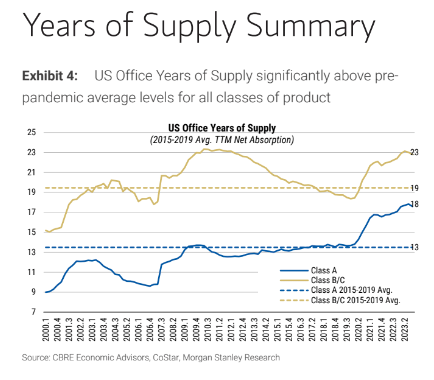

Data from a recent Treasury Department’s Financial Stability Oversight Council (FSOC) warned office vacancy rates have climbed sharply in recent years, reaching a record of 13.1% at the end of 2023.

CoStar analyst Phil Mobley recently noted the “reset in office demand has rocked US markets.”

Morgan Stanley warned earlier this year that office prices could plunge 30% due to sliding demand.

For those wondering why the excess supply of office towers can’t be converted into affordable housing, Goldman also noted that prices must drop 50% for housing conversions to make sense.

Powell has a rolling crisis on his hands. And the goal is to save the fireworks for after the election.

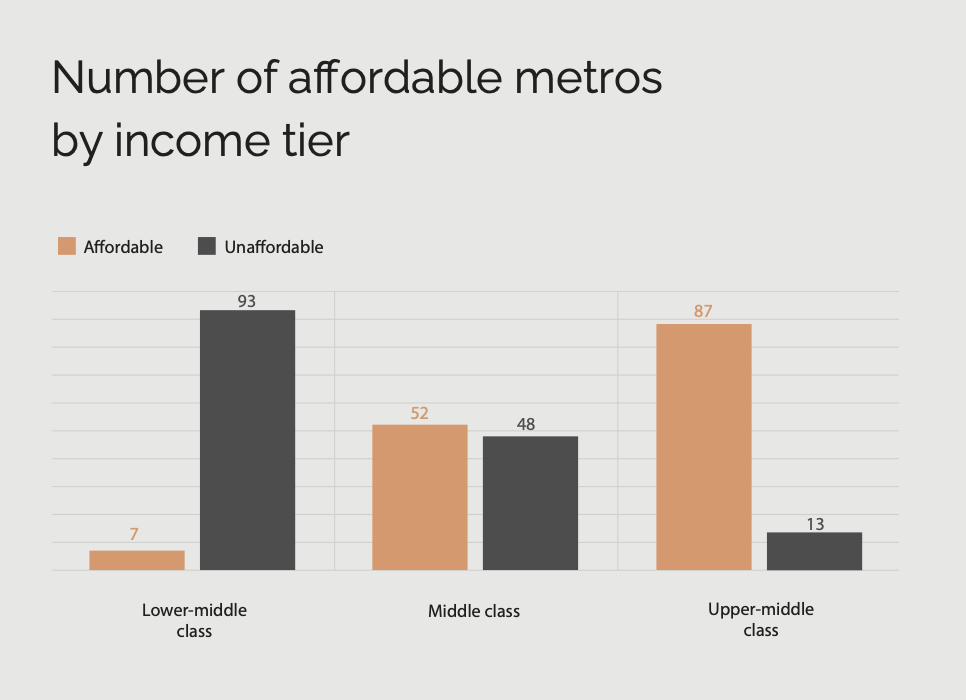

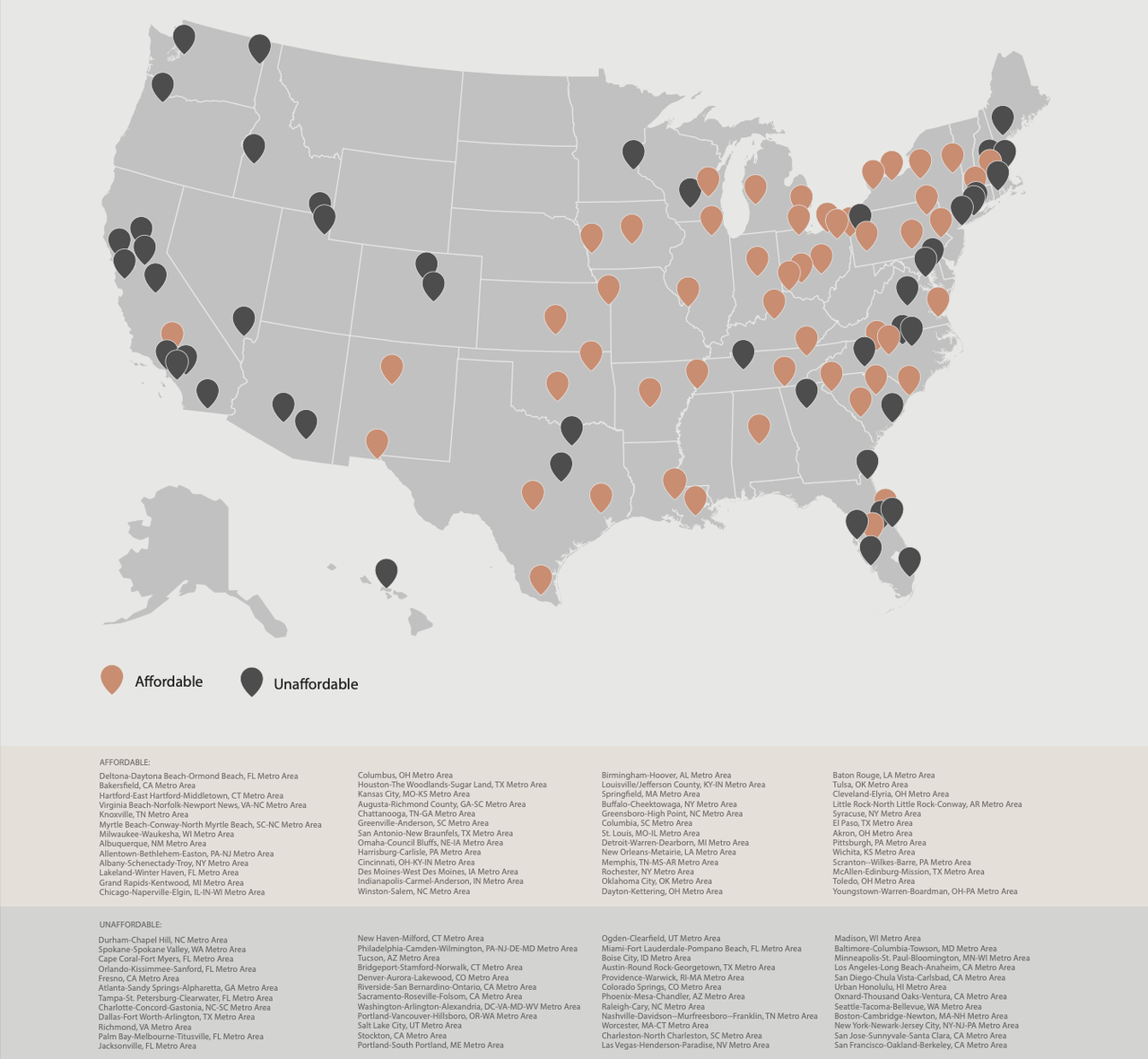

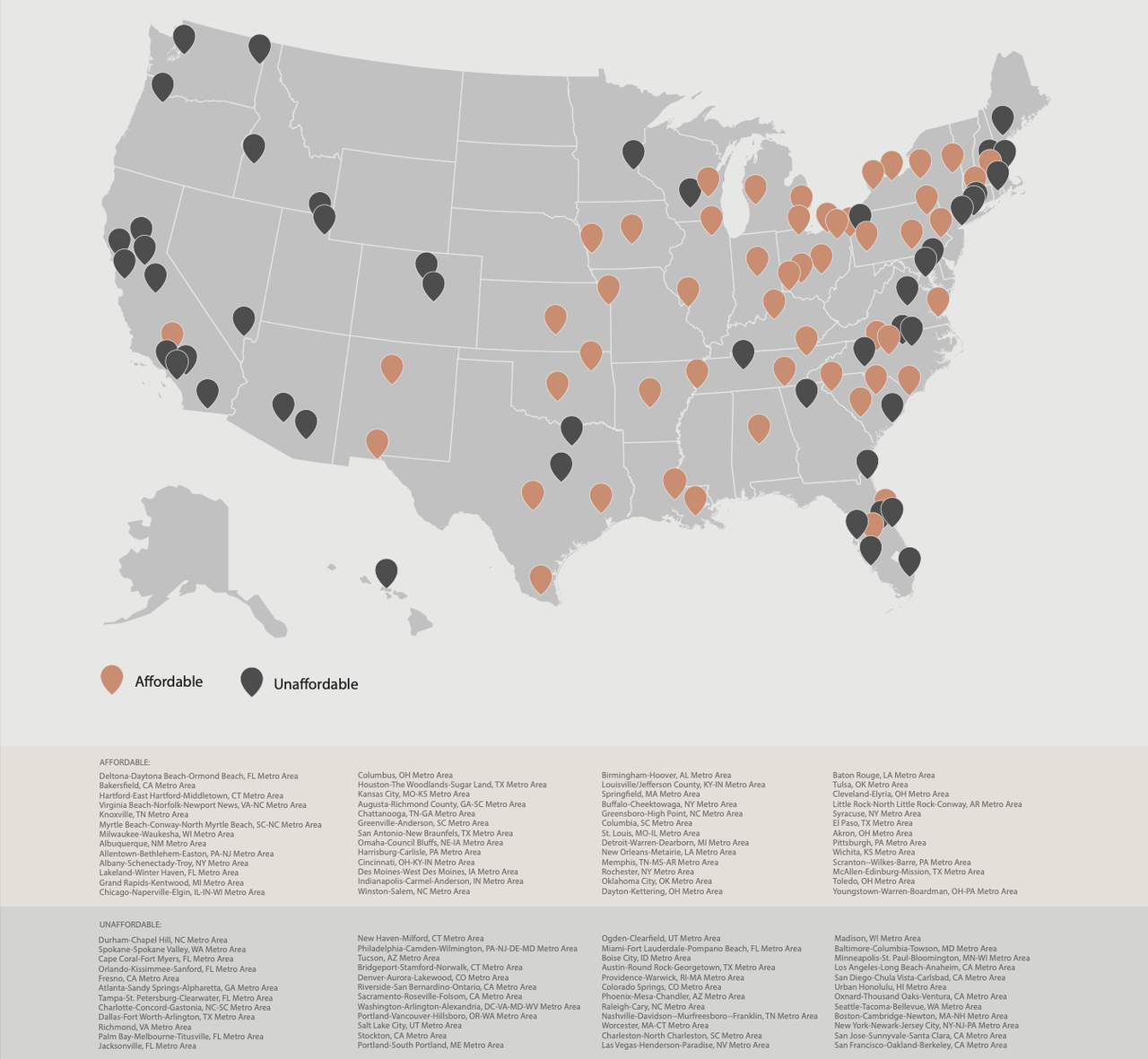

Housing is becoming an exclusively upper-class privilege in a growing number of cities.

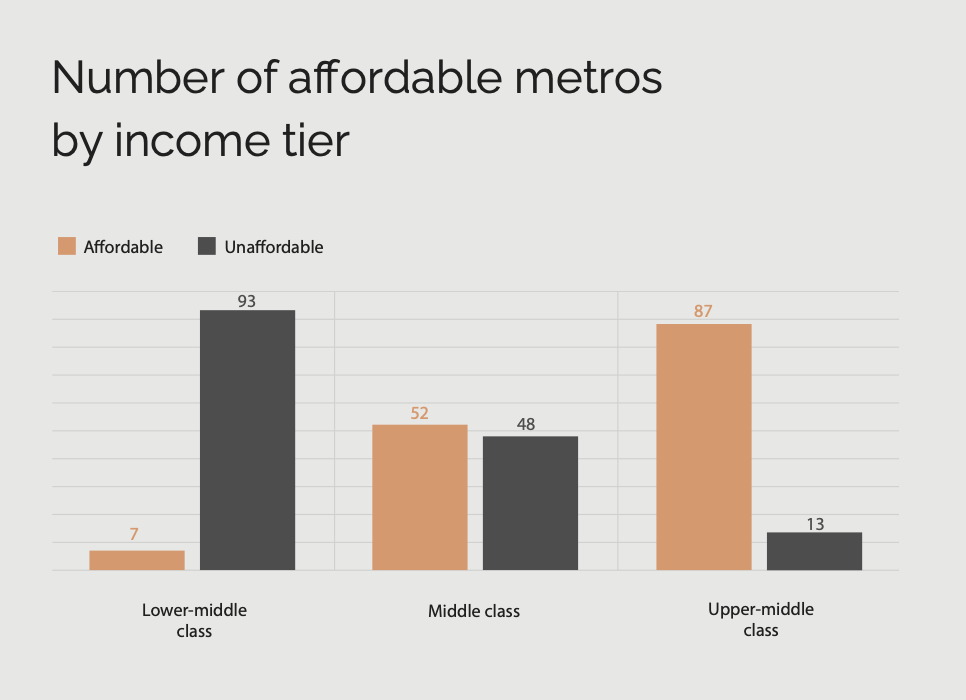

According to a new study by Creditnews Research, in 2024, middle-class households could afford to buy an average home in just 52 of the country’s 100 largest metros.

Just five years earlier, they could afford a home in 91 of the top 100 metros.

The situation is far worse for lower middle-class households, as they can only afford a home in seven of the largest 100 metros.

In total, 41 out of the 100 metros require a gross annual income of $100,000 or more to qualify for an average home. In 13 metros, an average income of more than $155,000 is needed.

In those cities, even the upper-middle class doesn’t qualify for an average home.

The study determined affordability by looking at how much income households need to earn to afford a down payment, mortgage payment, and related fees for an average home.

A home is considered affordable if monthly housing and mortgage costs don’t exceed 28% of a household’s gross income.

“There’s no two ways about it: Housing affordability has worsened significantly since Covid,” the report said. Since the pandemic, 39 of the most populous metros have fallen below the affordability threshold.

As expected, the most affordable areas for the middle class are located in the Midwest, Rust Belt, and parts of Texas, while the West Coast, Tri-State Area, and Hawaii are largely out of reach.

Affording a home is no longer a guarantee for the middle class

Being considered “middle class” doesn’t carry the same significance as it did just a few years ago.

“In the past, if you were middle class, it was almost assumed you would become a homeowner,” said Ali Wolf, chief economist of Zonda, a housing market research firm.

“Today, the aspiration is still there, but it is a lot more difficult. You have to be wealthy or lucky.”

That’s all thanks to a “perfect storm” of elevated mortgage rates, sky-high home prices, and a lack of inventory, making housing more unaffordable.

The result is that middle-income buyers, or those with an annual income of up to $75,000, could only afford about one-quarter of listings on the market last year.

According to Nadia Evangelou, the director of real estate research at the National Association of Realtors, “Middle-income buyers face the largest shortage of homes among all income groups, making it even harder for them to build wealth through homeownership.”

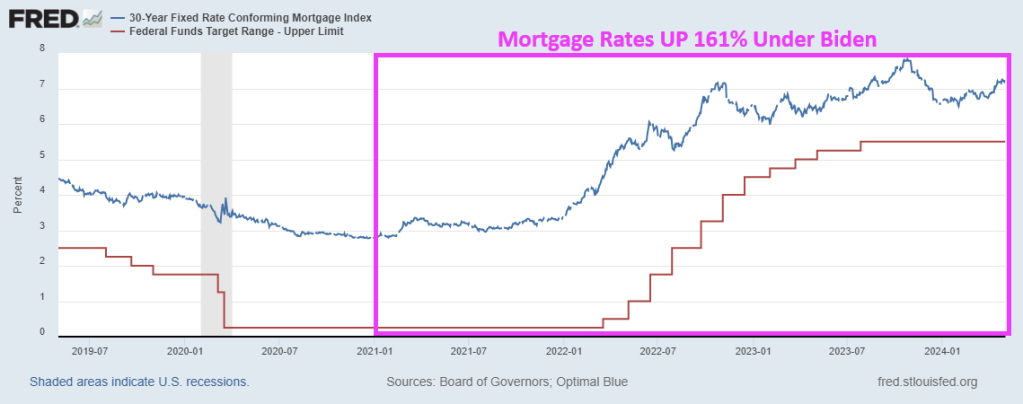

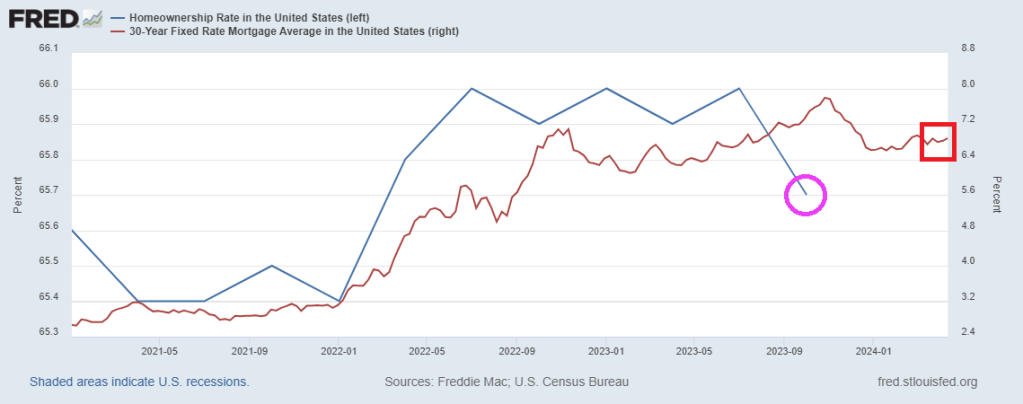

Mortgage rates (blue line) creep closer to 7%. Mortgage rates are UP 168% under Vacation Joe and home prices are up 32.5%.

After falling between November and January, mortgage rates are creeping back up.

According to Freddie Mac, 30-year fixed-rate mortgages reached 6.88% in the week of April 11 and at some point climbed well above 7%.

The reversal seems to be driven by a surprise spike in inflation, which has come out higher than expected for four consecutive months

“For homebuyers, the latest CPI report means mortgage rates will stay higher for longer because it makes the Fed unlikely to cut interest rates in the next few months,” said Chen Zaho, Redfin’s economic research lead.

“Housing costs are likely to continue going up for the near future, but persistently high mortgage rates and rising supply could cool home-price growth by the end of the year, taking some pressure off costs.”

Mortgage applications increased 3.3 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending April 12, 2024.

The Market Composite Index, a measure of mortgage loan application volume, increased 3.3 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index increased 4 percent compared with the previous week. The seasonally adjusted Purchase Index increased 5 percent from one week earlier. The unadjusted Purchase Index increased 6 percent compared with the previous week and was 10 percent lower than the same week one year ago.

The Refinance Index increased 0.5 percent from the previous week and was 11 percent higher than the same week one year ago.

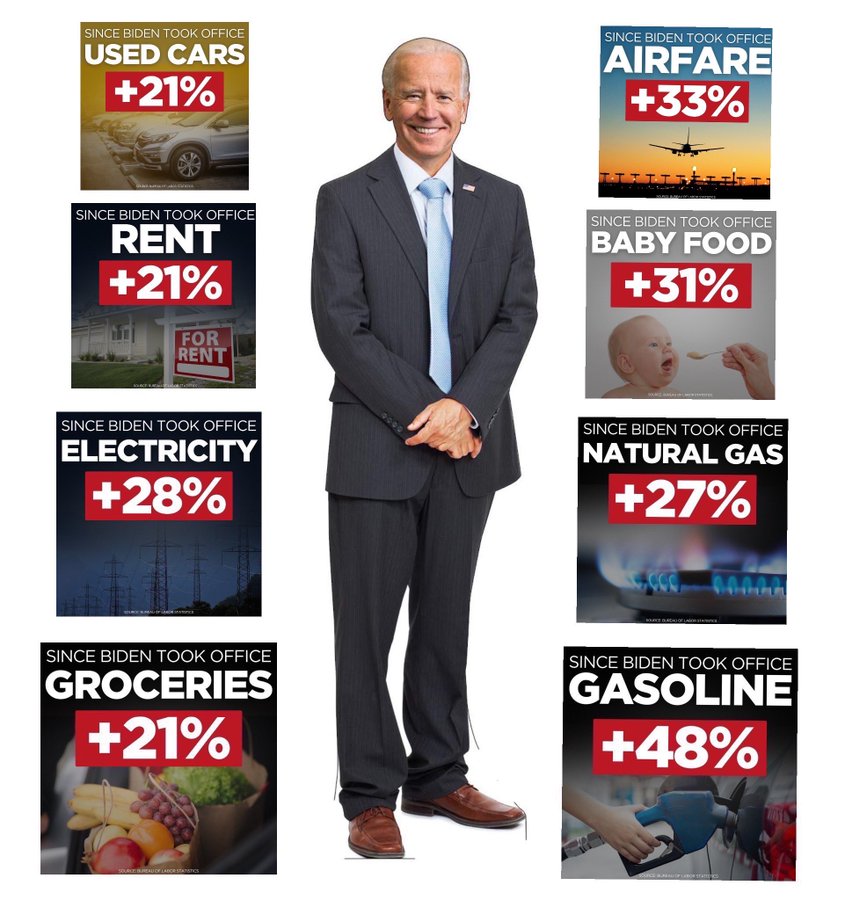

Bidenomics, a massive subsidy to the political donor class, but heartless towards the middle class.

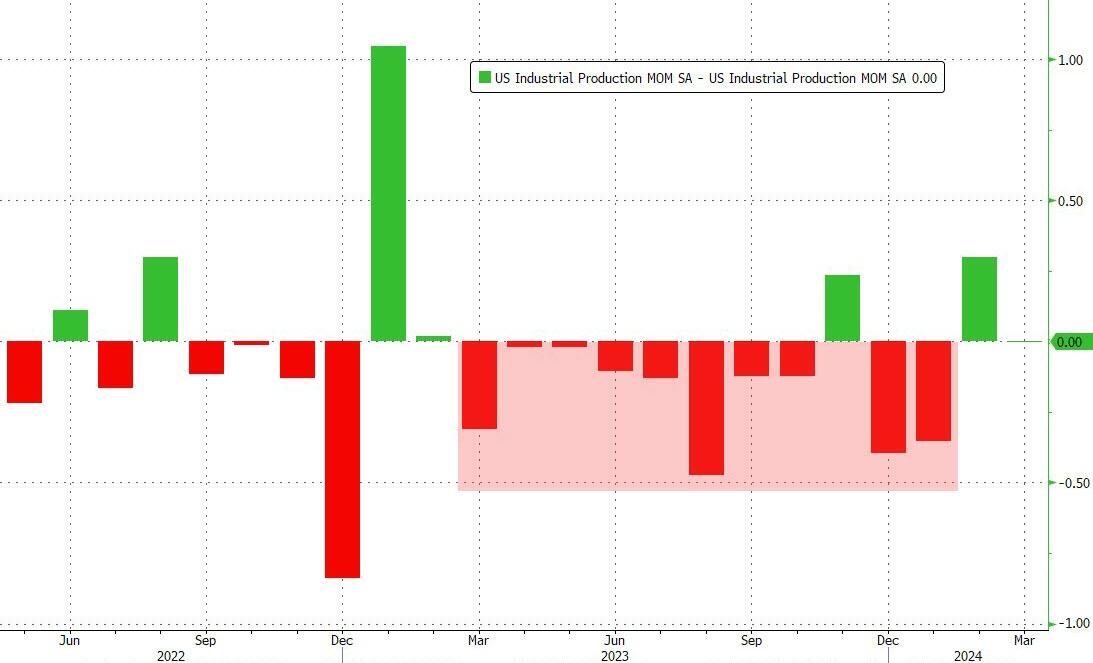

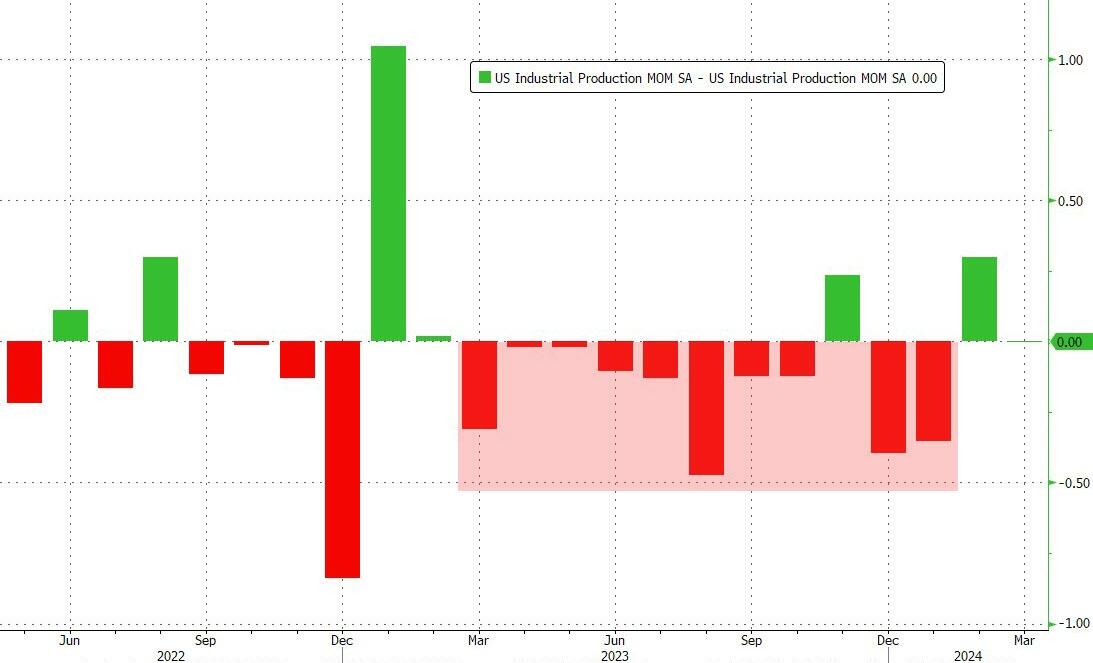

US Industrial Production rose 0.4% MoM in March – as expected – which was… wait for it… the same rise as in February after that data was revised notably higher. However, even with the revision and the subsequent rise, Industrial Production remains unchanged YoY…

Source: Bloomberg

We can’t help but see the irony that after we highlighted the serial downward revisions in data last month, that all of a sudden February’s Industrial Production data is revised drastically higher…

Source: Bloomberg

Capacity Utilization ticked modestly higher (from a downwardly revised 78.2% to 78.4% (below expectations)…

Source: Bloomberg

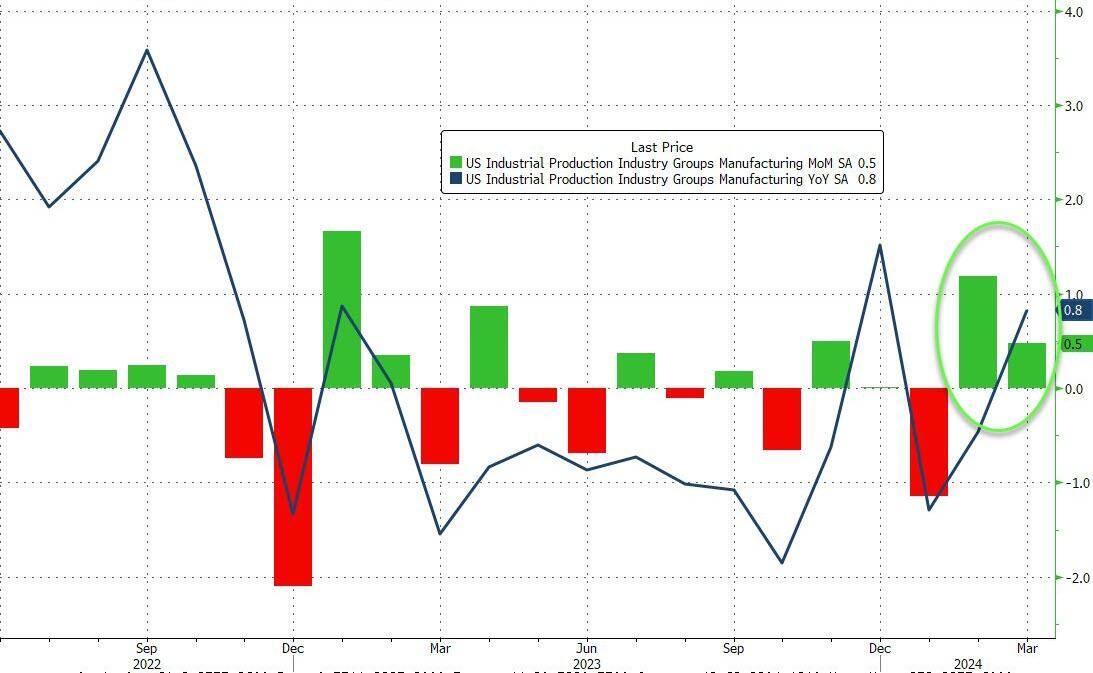

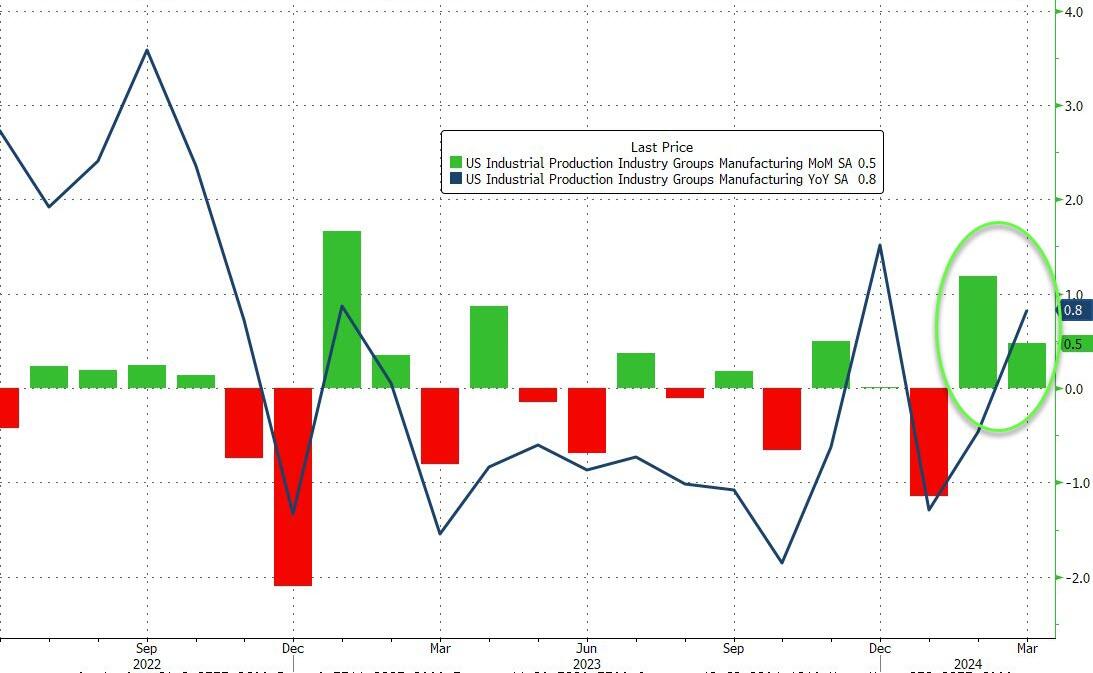

US Manufacturing also saw February’s data revised higher (from +0.8% to +1.2% MoM) and March rose 0.5% MoM (better than the 0.2% rise expected). That lifted YoY Manufacturing up by 0.8%…

Source: Bloomberg

Soft and Hard manufacturing data in agreement that things are turning up…

Nothing but blue skies here for The Fed to cut rates into… not!

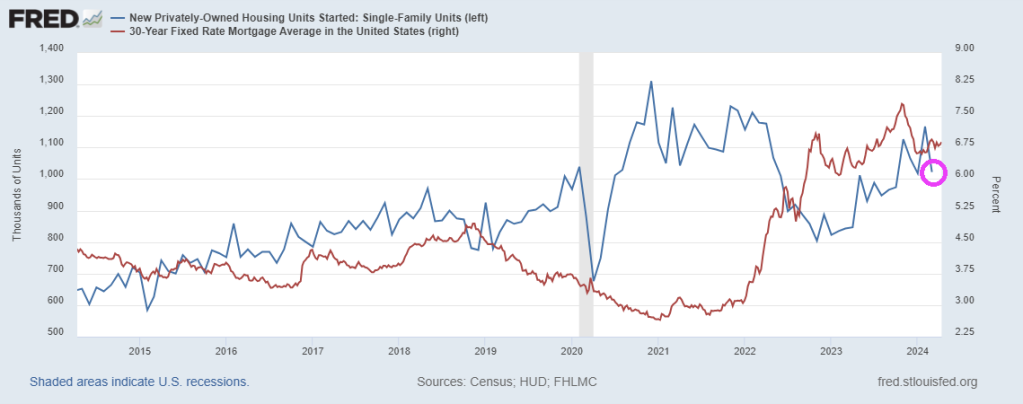

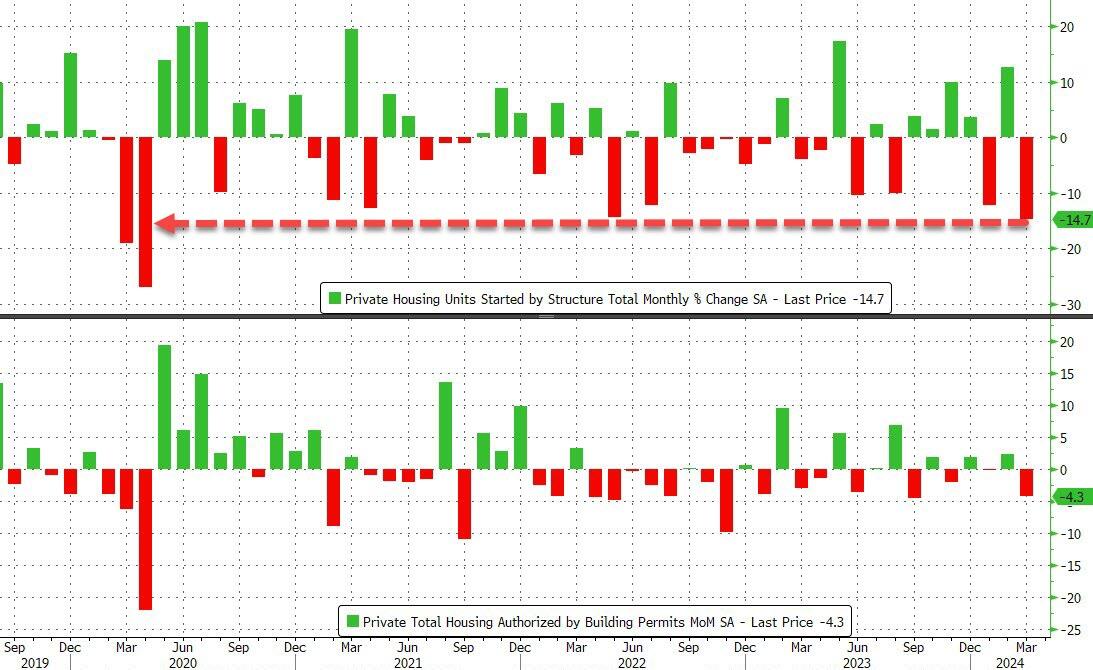

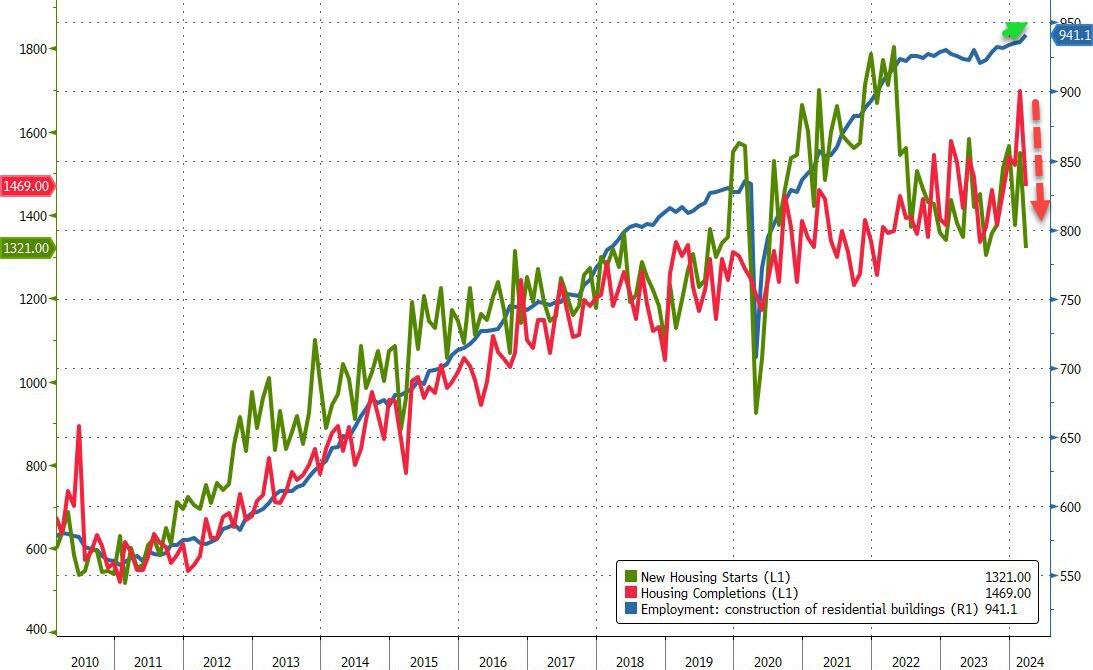

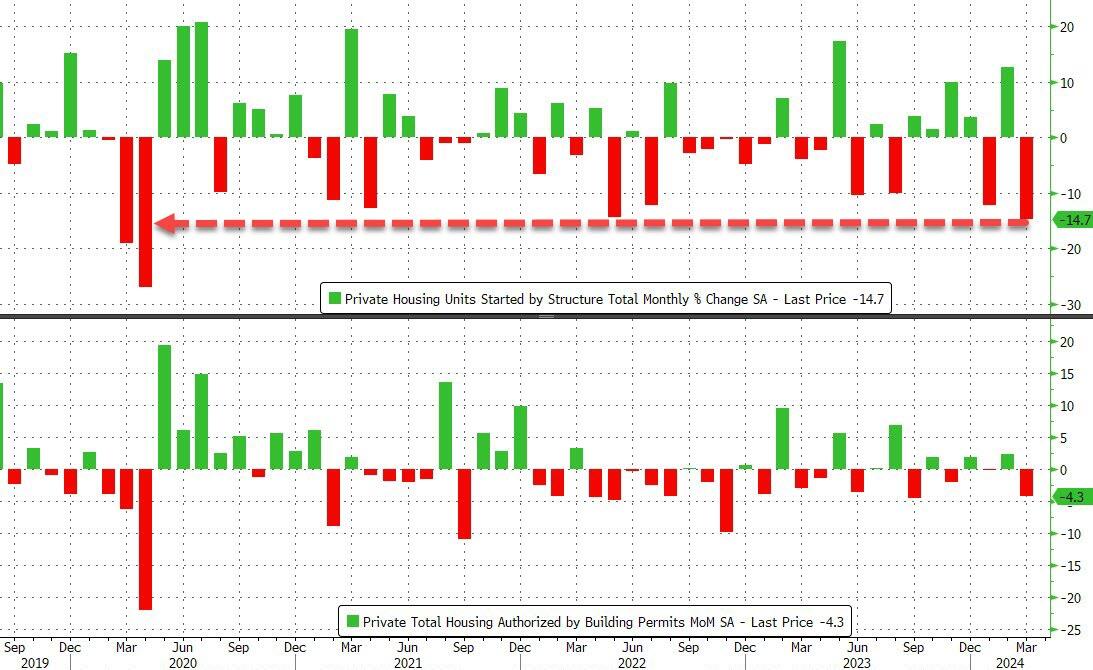

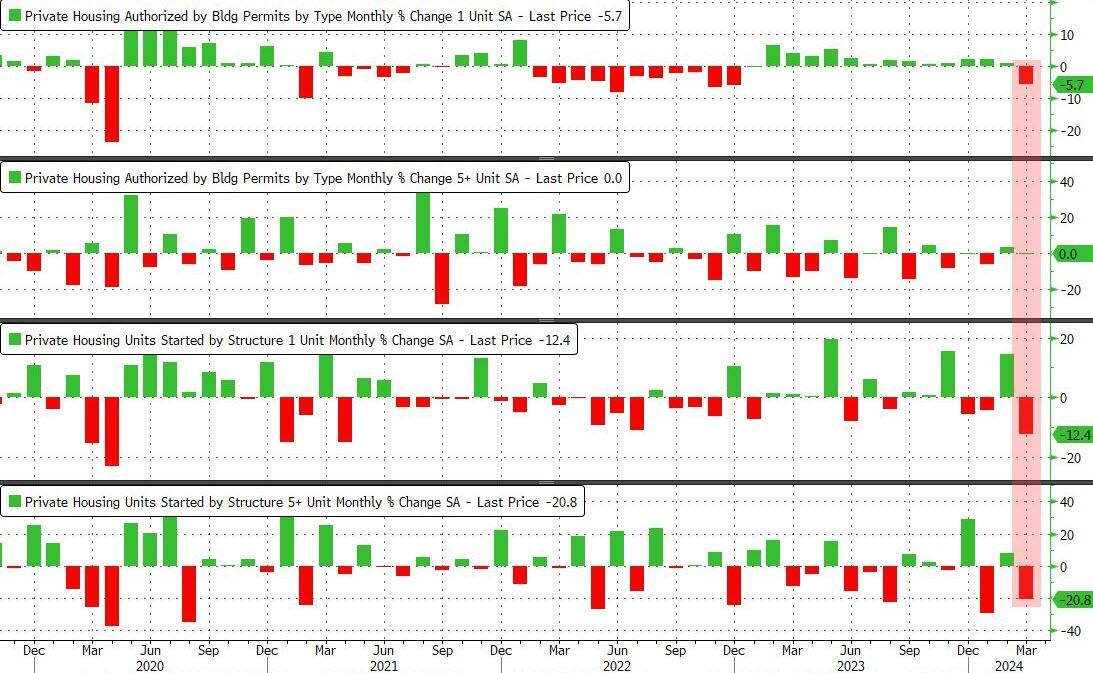

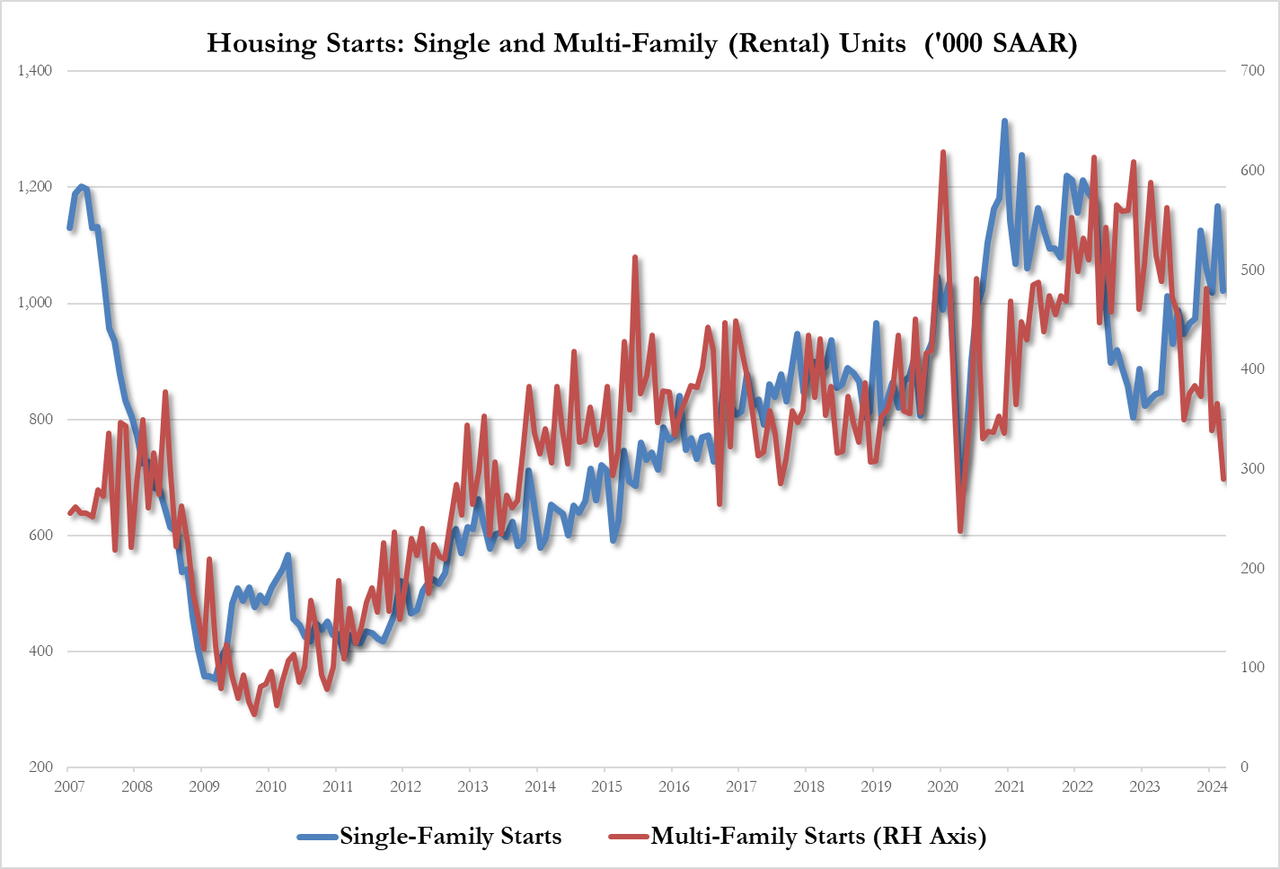

Come feel the noise! After steady growth in 1-unit housing starts under Trump, housing starts have been eratic under Biden despite the foreign invasion force of millions … of low wage workers.

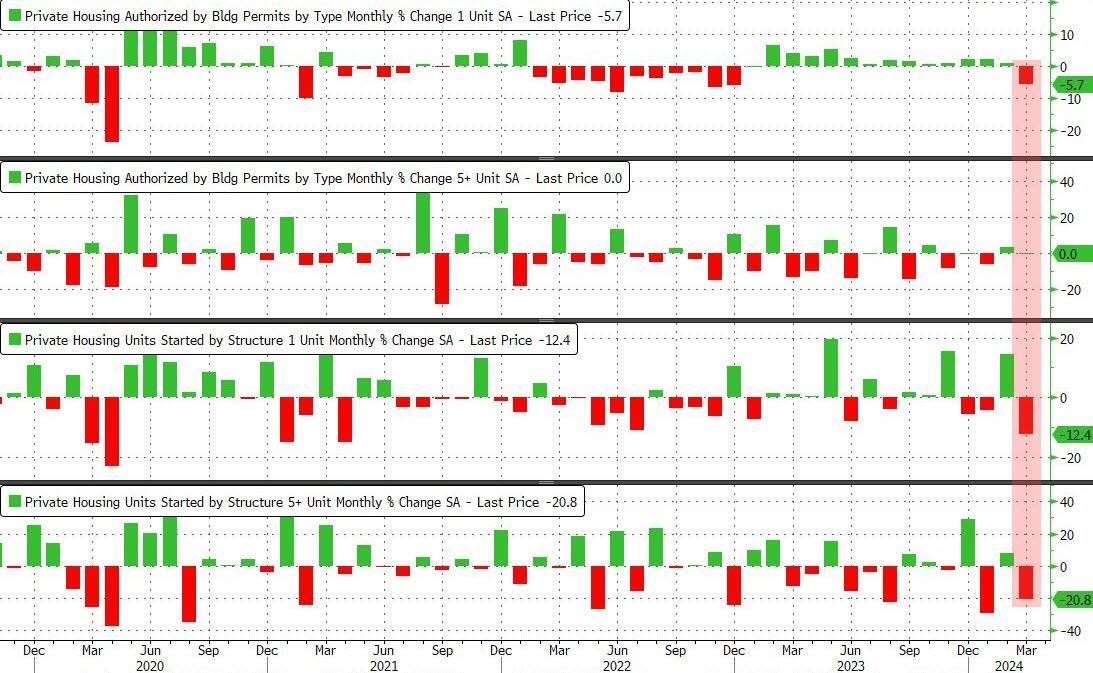

For context, this is the largest MoM drop in housing starts since the COVID lockdowns…

Source: Bloomberg

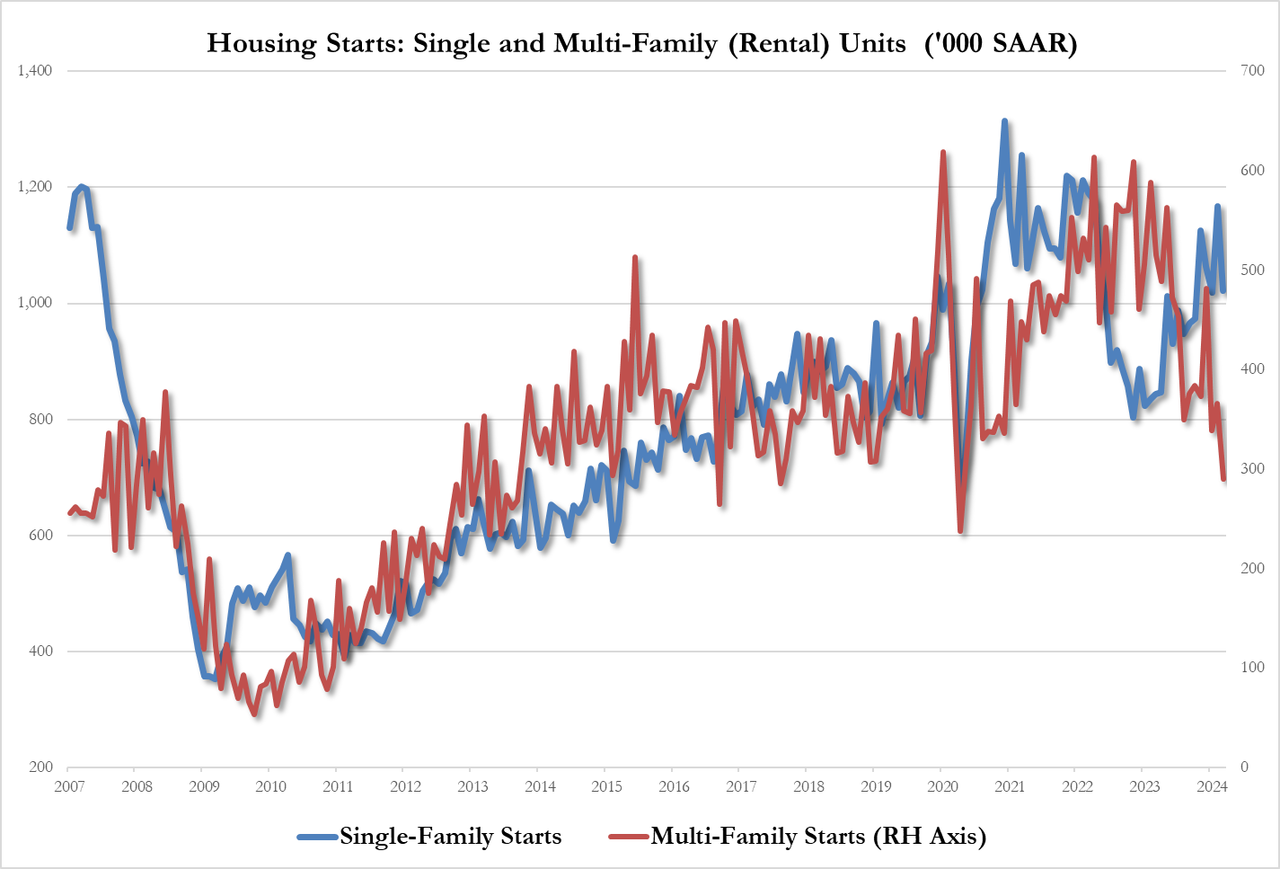

It was a bloodbath across the board with Rental Unit Starts plummeting 20.8% MoM…

Source: Bloomberg

That pushed total multi-family starts SAAR down to its lowest since COVID lockdowns…

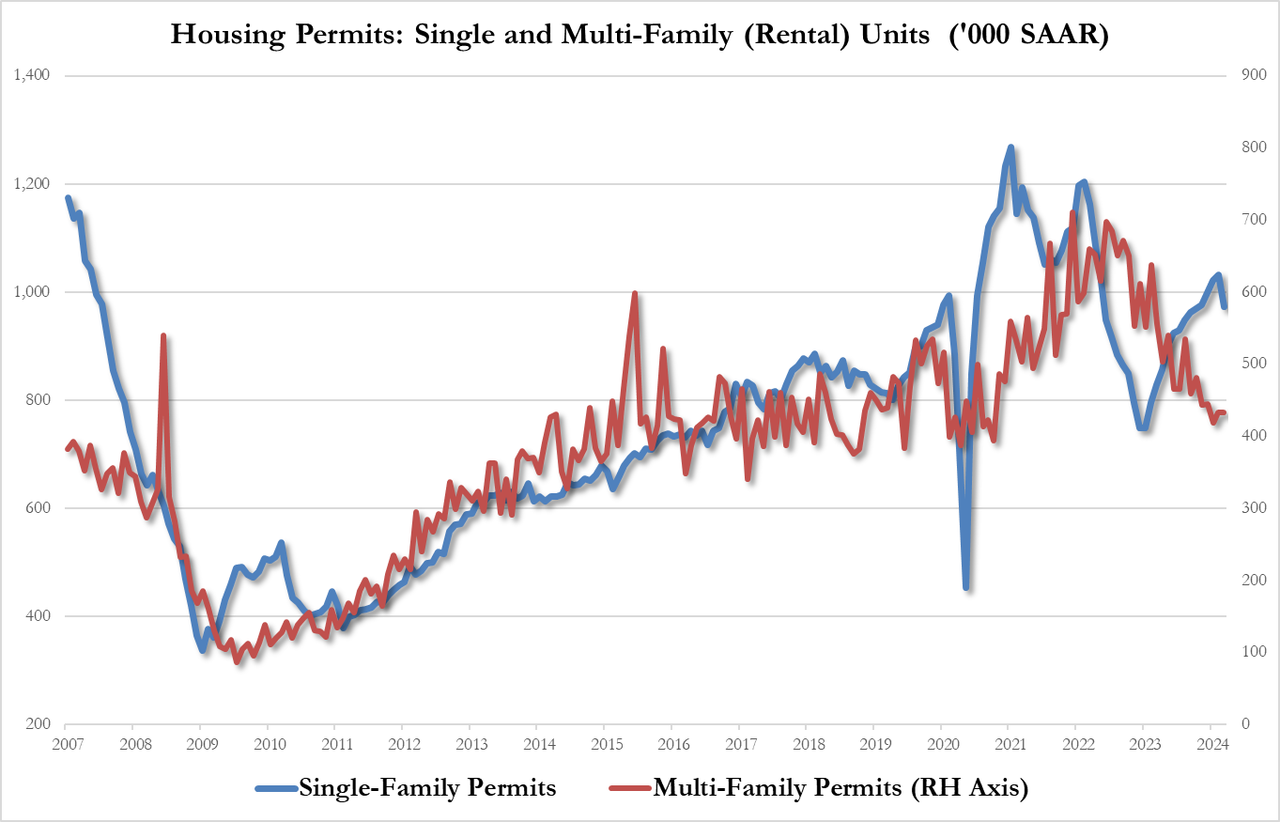

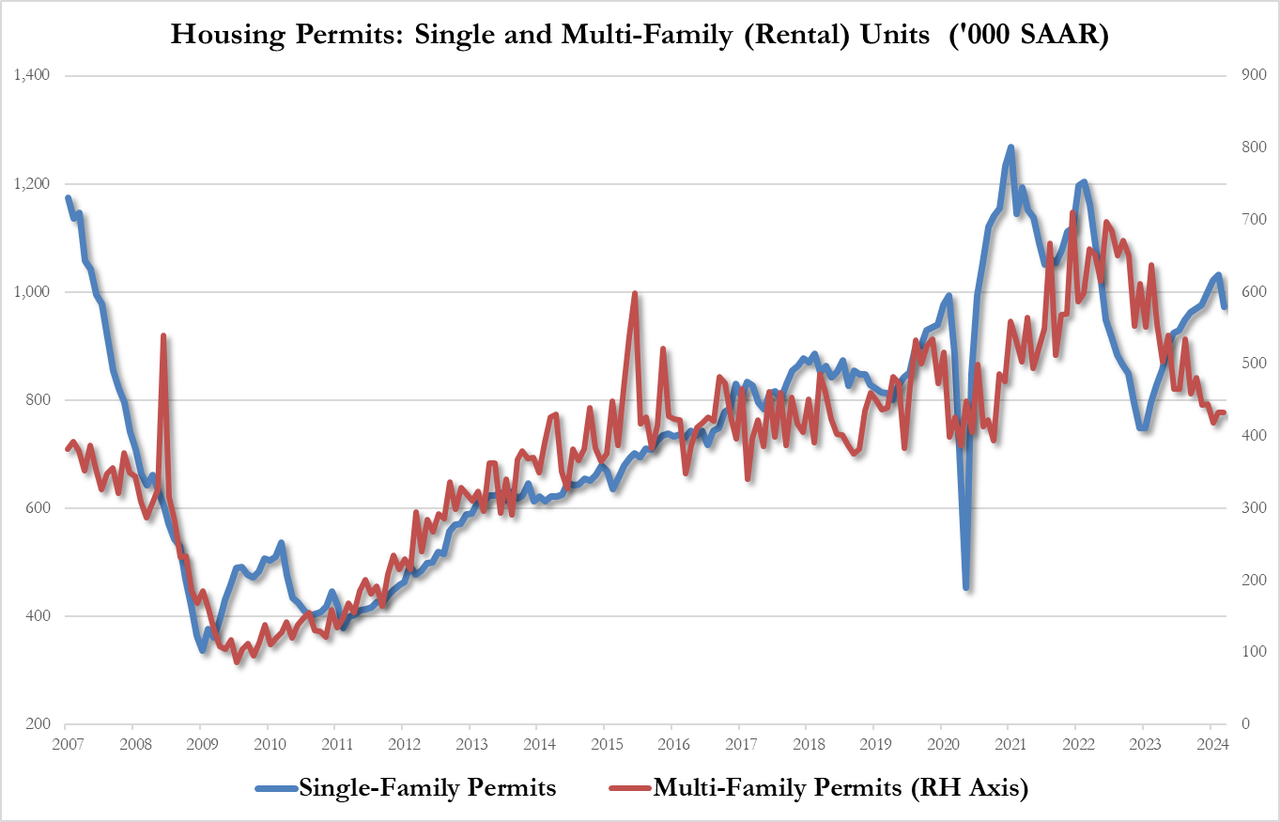

The plunge in permits was less dramatic and driven completely by single-family permits down 5.7% to 973K SAAR, from 1.032MM, this is the lowest since October. Multi-family permits flat at 433K

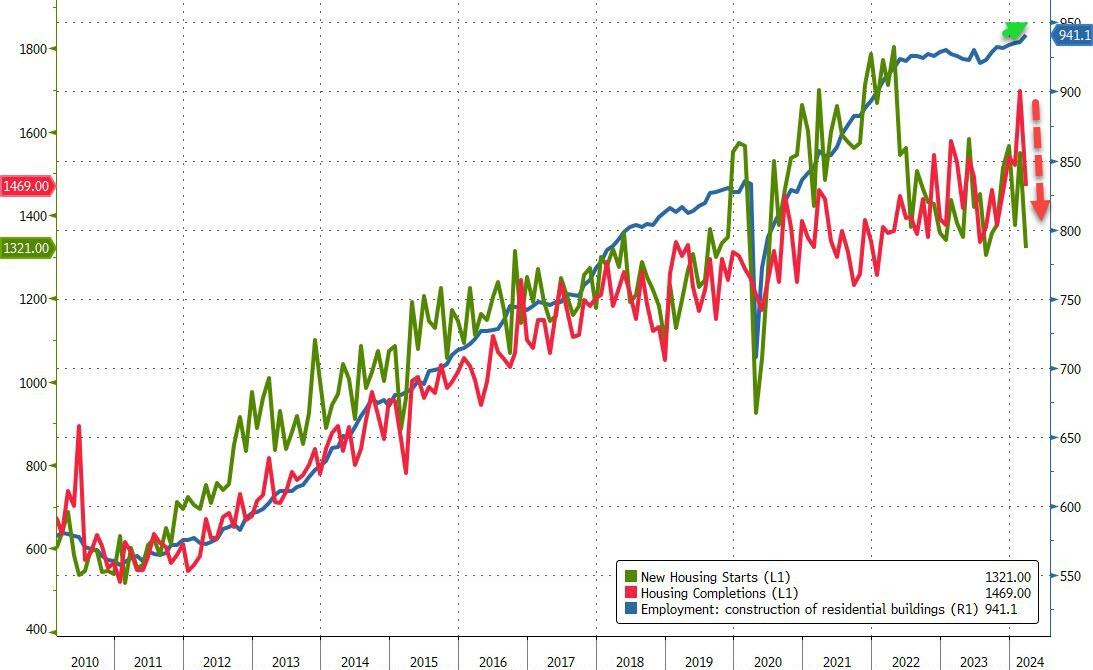

Intriguingly, while starts and completions plunged in March, the BLS believes that construction jobs surged to a new record high…

Source: Bloomberg

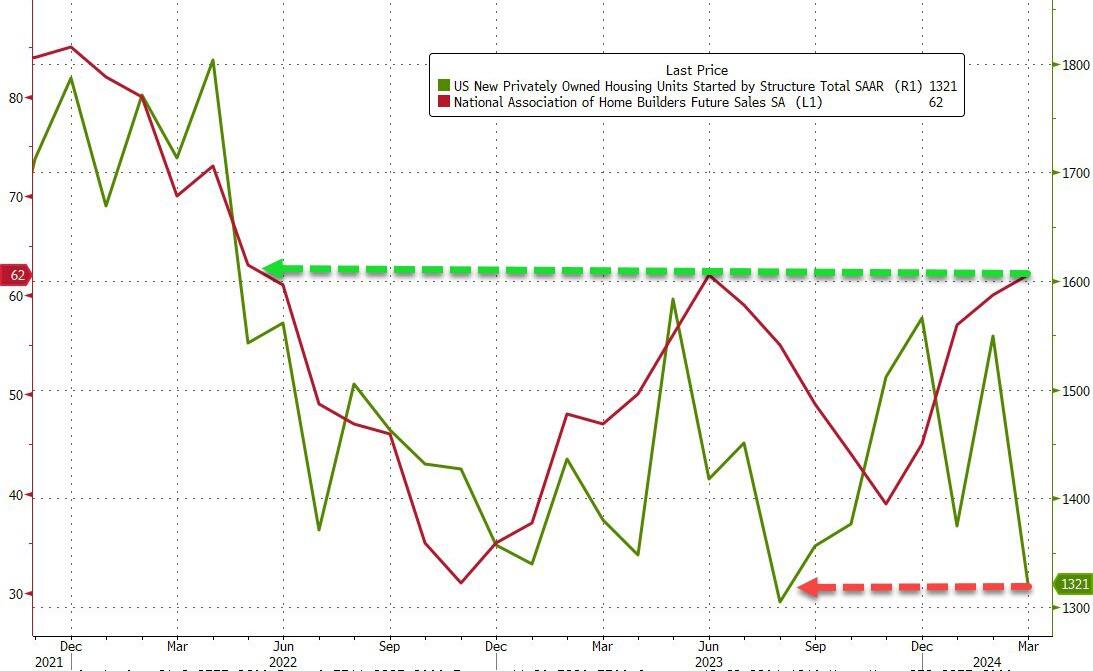

Finally, just what will homebuilders do now that expectations for 2024 rate-cuts have collapsed?

Source: Bloomberg

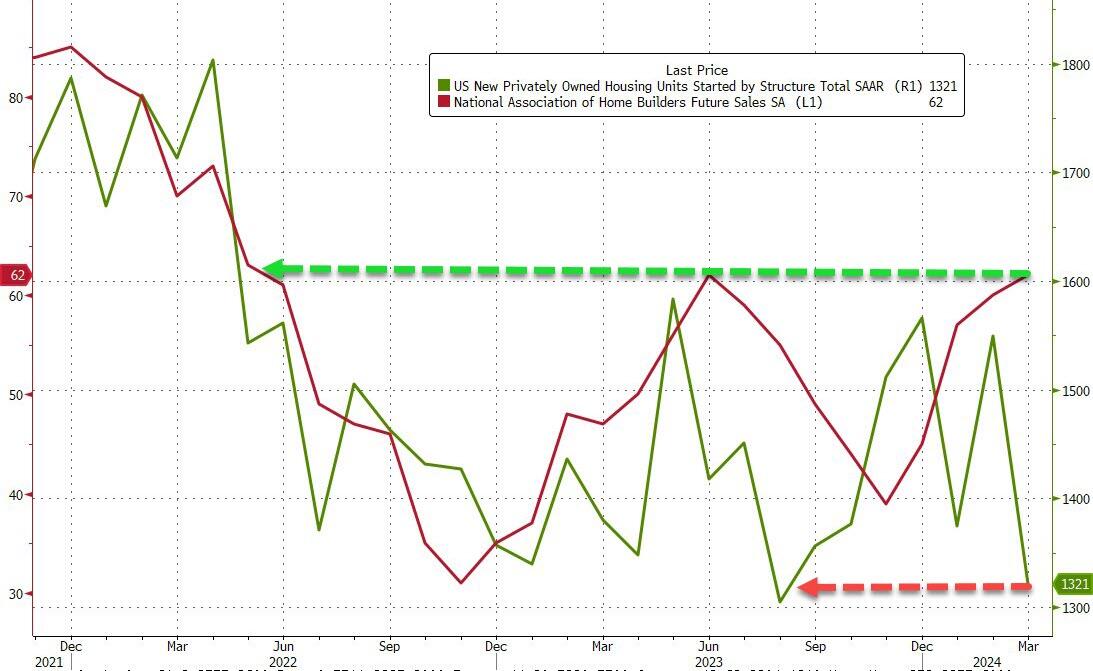

One thing is for sure – do not trust what homebuilders ‘say’ (as NAHB confidence jumped to its highest since May 2022 at the same time as housing starts crashed)…

Joe Biden likes to sell himself as “working class Joe” or “union Joe.” The truth is anything but. He is “Washington DC insider Joe” or “big corporate Joe.”

The US mortgage 30 year rate is down slightly today to 7.30%. That is a whopping 160% increase since Biden’s Presidency began.

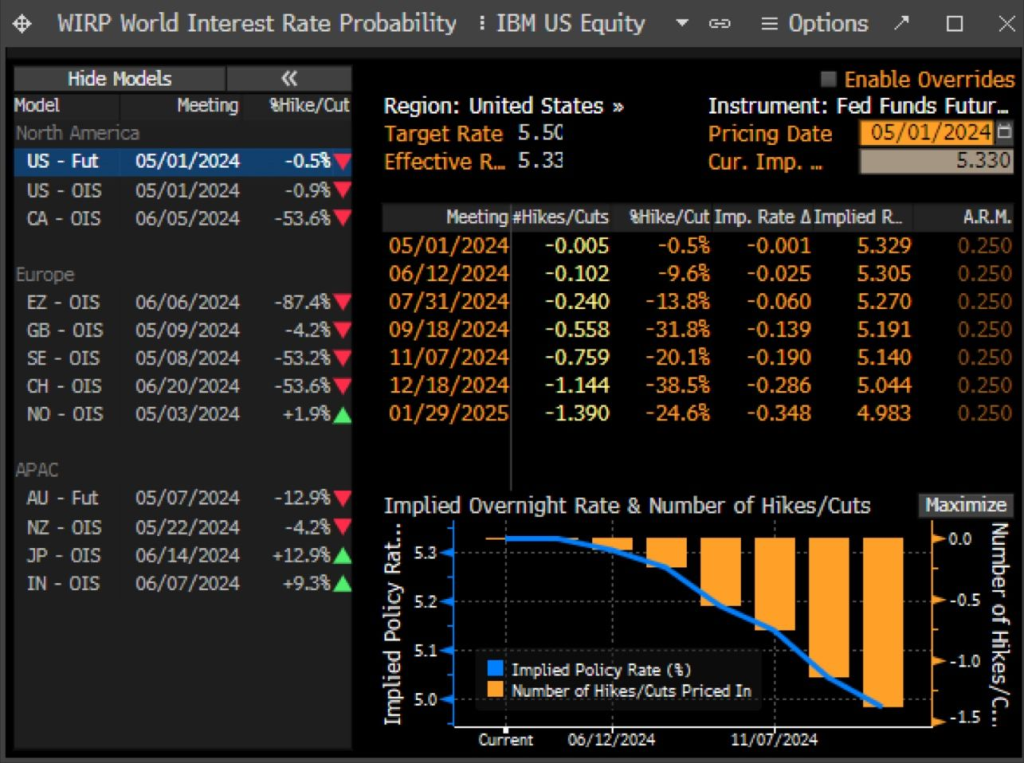

Mortgage rates will continue to climb as the US Treasury 10-year yield climbs.

The US homeownership rate is falling as mortgage rates climb.

US CPI on trend for 4-5% at US election in November.

Source: BofA

Above 5%…?

Strong CPI raises market probability of YE25 rates above 5%.

Source: Goldman

Cyclical inflation remains too elevated

“Our measure of cyclical inflation–which should capture the impact of excess demand on prices–appears to be stuck at around 5%, which is too elevated”

Source: Safra

US alone

The US is the only economy in the G10 where the latest inflation print surprised to the upside.

Source: Goldman

200% of GDP

Under current policies, government debt outstanding will grow from 100% to 200% of GDP.

Source: Apollo

Close to $9 trillion in maturities

That’s a significant amount of government debt maturing within the next year.

Source: Apollo

Every year a deficit

OMB forecasts 5% budget deficit every year for the next 10 years.

Source: Apollo

A billion per day….is long gone

US government interest payments per day have doubled from $1bn per day before the pandemic to almost $2bn per day in 2023.

Source: Apollo

Biggest Story of 2020s…Ugly End of 40-year Bond Bull

Chart shows long-term US government bond (15+ year) rolling 10-year annualized returns, %.

Source: Flow Show

Highest yields in 15 years

The intermediate part of the yield curve still offers the highest yields in over fifteen years.

Source: Piper Sandler

Finally, electricity costs keeps rising, ESPECIALLY with the misnamed Inflation Reduction Act (IRA). The real name of the IRA should have been the Large Green Donor Increase Act (LGDIA).

Joe Biden, his Administration, and The Federal Reserve are really “The Alligator People.” Despite what they tell you, they have small brains (particularly Biden) and are hyperfocused on spending.

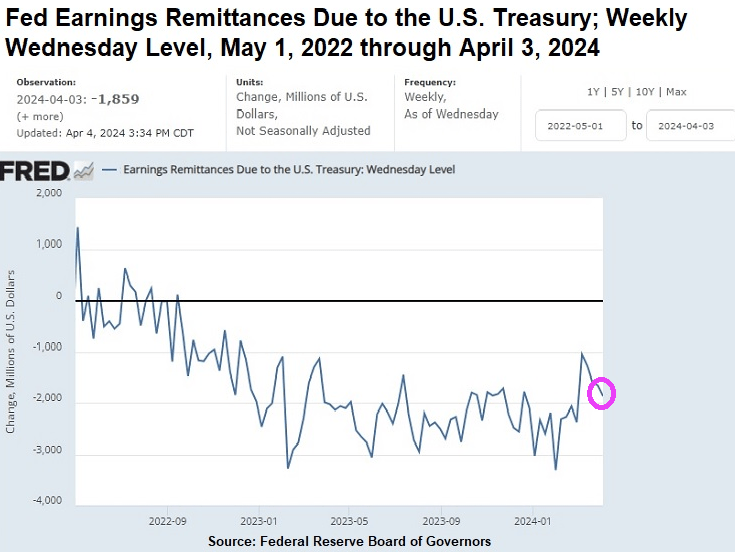

A good example comes from “Wall Street On Parade” where they show that The Federal Reserve is still paying BILLIONS to US Treasury in the form of remittances (losses). While at the same time, paying the mega banks on Wall Street high interest loans.

As of April 3 of this year, the Federal Reserve (Fed) has racked up $161 billion in accumulated losses. We’re not talking about unrealized losses on the underwater debt securities the Fed holds on its balance sheet, which it does not mark to market. We’re talking about real cash losses it is experiencing from earning approximately 2 percent interest on the $6.97 trillion of debt securities it holds on its balance sheet from its Quantitative Easing (QE) operations while it continues to pay out 5.4 percent interest to the mega banks on Wall Street (and other Fed member banks) for the reserves they hold with the Fed; 5.3 percent interest it pays on reverse repo operations with the Fed; and a whopping 6 percent dividend to member shareholder banks with assets of $10 billion or less and the lesser of 6 percent or the yield on the 10-year Treasury note at the most recent auction prior to the dividend payment to banks with assets larger than $10 billion. (This morning the 10-year Treasury is yielding 4.41 percent.)

Operating losses of this magnitude are unprecedented at the of Fed, which was created in 1913. In a press release dated March 26, the Fed stated this: “The Reserve Banks’ 2023 sum total of expenses exceeded earnings by $114.3 billion.”

As the chart above indicates, the Fed’s ongoing weekly losses have ranged from a high of $3.3 billion for the week ending Wednesday, January 31, 2024, to $1.86 billion for the most recent week ending Wednesday, April 3, 2024.

American taxpayers have good reason to sit up and pay attention to the Fed’s giant and ongoing losses. That’s because when the Fed is operating in the green, as it was on an annual basis for 106 years from 1916 through 2022, the Fed, by law, turns over excess earnings to the U.S. Treasury – thus reducing the amount the U.S. government has to borrow by issuing Treasury debt securities. According to Fed data, between 2011 and 2021, the Fed’s excess earnings paid to the U.S. Treasury totaled more than $920 billion.

WHO pays for the student loan forgiveness? It just doesn’t vanish, it is transferred to taxpayers. Alligators like Alexandria Ocasio Cortez going on talk shows to argue the benefits of being free from financial obligations that student voluntarily agreed to. Say, can AOC get my mortgage forgiven?? Just kidding. Now those same students can borrow additional money to get MBA degrees with the expectation that the student loan is “free money.”

Yes, Biden is acting recklessly (no surprise). Here is a picture of King Gator, Joe Biden.

The Biden Administration and The Federal Reserve ARE the alligator people. Except these gators are hungry for your money and votes constantly.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

You must be logged in to post a comment.