“One of the most cowardly things ordinarily people do, Is to shut their eyes to facts.” – C.S. Lewis

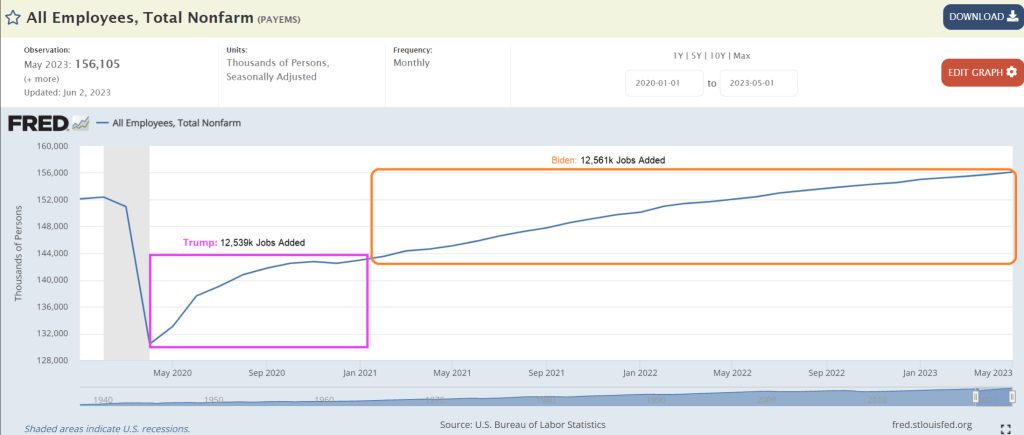

Okay, we know Biden lies constantly and misrepresents facts (hey, he is a politician like Adam Schiff (D-CA). But this graphic praising Bidenomics with Biden having created the most jobs (average per month) since Carter (notice they left out Democrat darling Jimmy Carter!!!). In this absurd graphic, Biden wins by “creating” over 400k jobs per month while Trump lost jobs per month. Riveting … except that it is completely misleading.

Actually, the US economy added 12.53 million jobs after April 2020 (Trump) while Bidenomics created took 2 1/2 years to add 12.56 million jobs. So, Biden took over twice as long to create jobs after Covid than it did under Trump. Simply opening the economy and schools produced that magical claim by Biden. And the National Teacher’s Union and Randi Weingarten worked with Fauci to orchestrate shutting down schools. Blaming Trump for local governments shutting down the economy is pure bunk.

12.53 millions jobs added / 8 months = 1.56 million jobs average per month. Biden? 12.56 million jobs added / 30 months = .43 million jobs average per month. So, Trump averaged more than 3x the job growth post-Covid than Biden.

Here is the “glories of Bidenomics” from the White House. As Biden likes to say, pure malarkey!

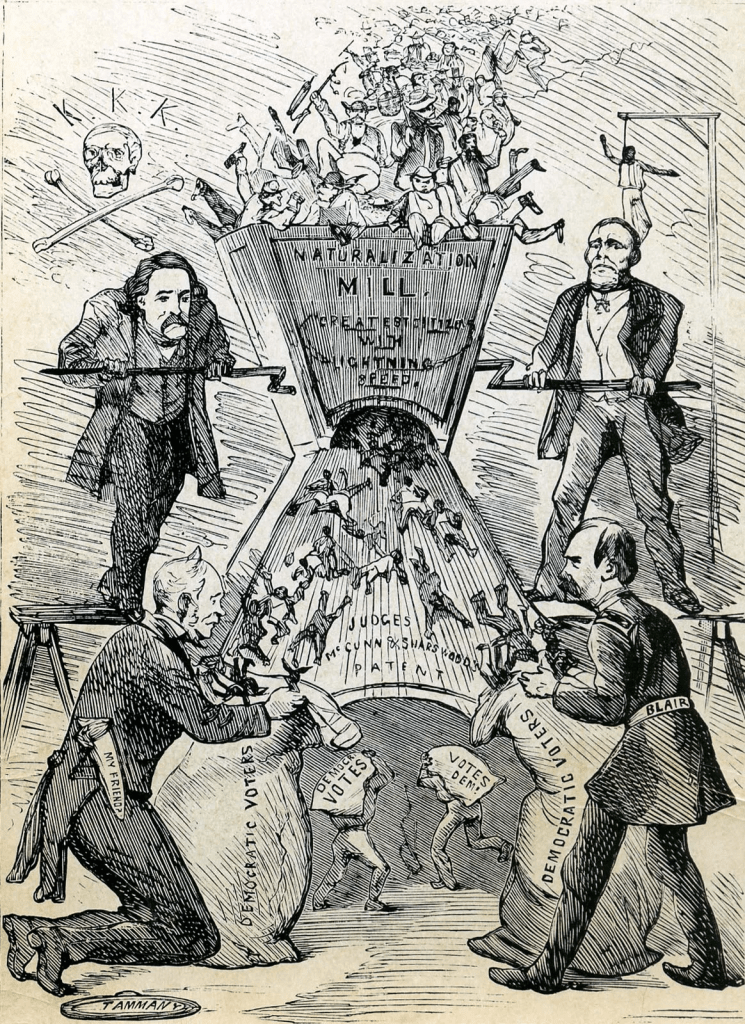

I wonder if the Democrat Party is a rebirth of New York City’s Tammany Hall corrupt political movement of the 1800s? Is Biden Boss Tweed? Or is Obama Boss Tweed with Biden as his nasty, dimwitted henchman?

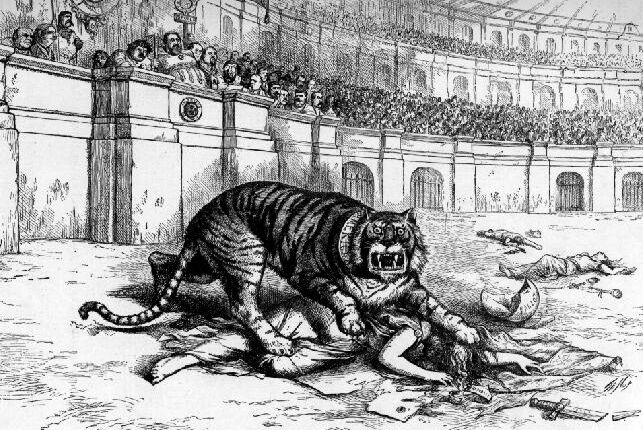

In 1871, Thomas Nast denounces Tammany as a ferocious tiger killing democracy. The image of a tiger was often used to represent the Tammany Hall political movement. Sounds an awful lot like today’s Democrat Party.

Josef Stalin of the old Soviet Union used to be called County Joe. But Biden has so many possible nicknames: Corrupt Joe, Pay-for-play Joe, Sleazy Joe, Bully Joe, etc. How about Green Joe?

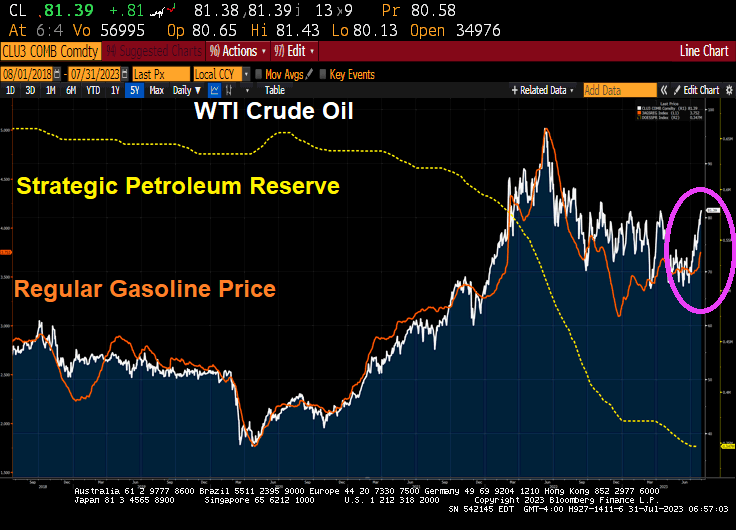

Green Joe (or the Nasty Green Giant?) along with his energy goon Jennifer Granholm, have drained the strategic petroleum reserve by 46% while gasoline prices have soared 60% under Bidenomics.

Gasoline prices have rise over 6.5% just since 7/23/2023.

Trump wants to drain the swamp, Biden/Granholm want to drain the strategic petroleum reserve so we can’t go back to fossil fuels. Biden and Granholm as Fossil Fools

Energy Secretary Jennifer “The Evil Pixie’ Granholm demostrating how she will refill the strategic petroleum reserve. Which she never will, of course.

US average hourly earnings continued at 4.4% year-over-year (YoY). However, the last core inflation reading was 4.8% YoY, so real wages continue to decline.

Rent CPI for June was 7.8% YoY.

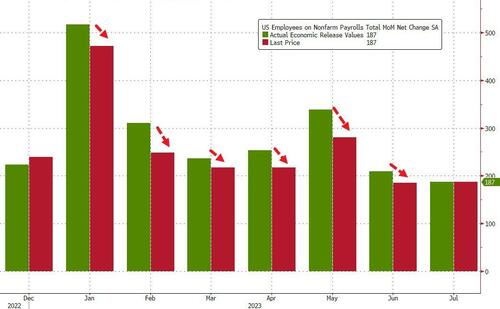

Here is the rest of the story.

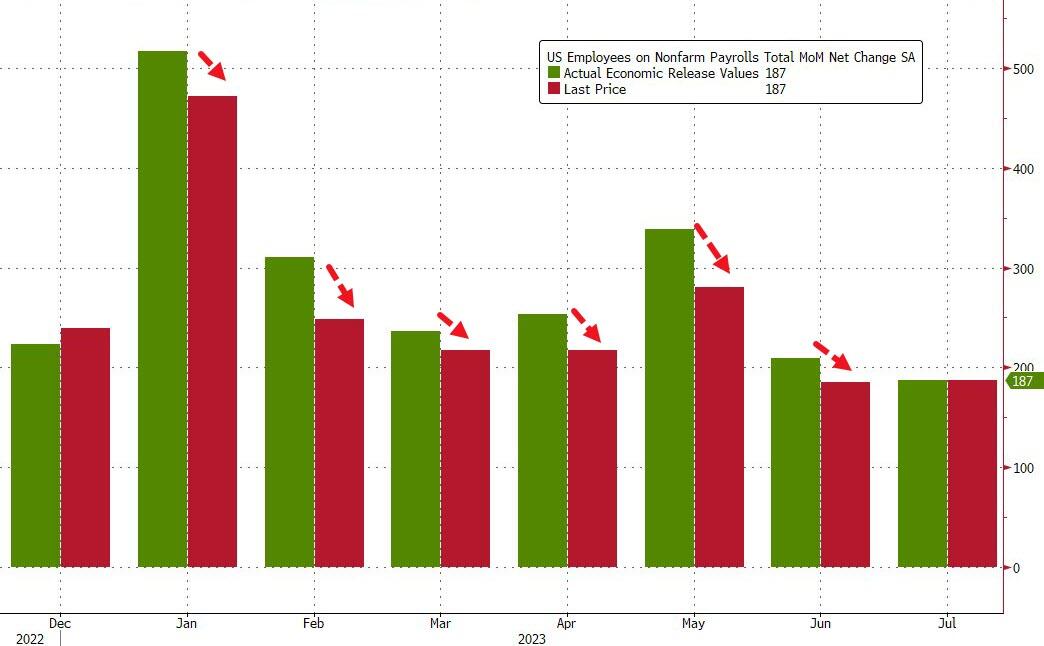

In keeping in with Biden admin’s penchant of constantly fabricating data, both May and June numbers were revised sharply lower of course:

May revised down by 25,000, from +306,000 to +281,000

June was revised down by 24,000, from +209,000 to +185,000.

To show just how ridiculous the data manipulation is, consider this chart – every monthly payrolls report in 2023 has been revised lower.

And on the disappointing jobs report and massive revisions of past data (the REAL inflation plaguing the nation is The Federal goverment lying about data), the US Treasury 2 year yield dropped like Biden on a flight of stairs.

Here are the faces of Washington DC. Lies, corruption, government for sale to highest bidder, cynacism, oppression, fear mongering, etc. This is Biden’s legacy.

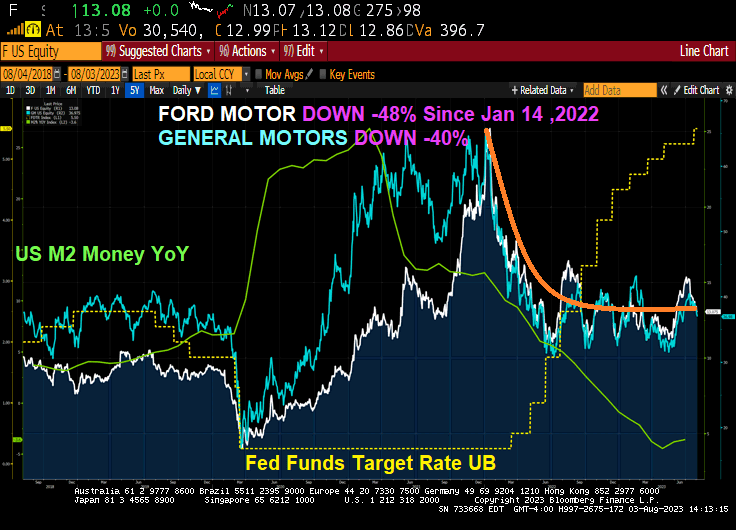

Bidenomics, the term for “Government Gone Wild! in terms of spending and EPA regulations, is a disaster for the US middle class and low wage workers. Even the 1% are now hurting if bought into Biden’s green lunacy. Ford is now down -48% since January 14, 2022 as The Fed started raising rates to fight inflation. GM is down “only” -40%.

So far this year, the division has lost $1.8 billion and this year’s $4.5 billion loss figure blows away last year’s $2.1 billion loss. Ford also announced that its electric F-150 pickup trucks will undergo a price cut, according to Fox.

Ford beat earnings on Thursday and reported adjusted EPS of $0.72, beating expectations of $0.54. It posted revenue of $45 billion and adjusted EBITDA of $3.8 billion, above estimates of $3.15 billion.

The company also raised its guidance, forecasting adjusted EBIT of $11 billion to $12 billion from $9 billion to $11 billion. The company is now guiding for free cash flow of $6.5 billion to $7 billion, from $6 billion.

But reality has sunk in about the company’s comments regarding its EV production schedule and spending plans. Price cuts in the industry, led by Elon Musk and Tesla, have thrown Ford’s production targets into a tailspin and Morgan Stanley noted on Friday morning that “major changes to the EV strategy” could be necessary, according to a wrap up by Bloomberg.

Ford now says it is “throttling back” on plans to ramp up EV production, the wrap up said. It blamed the price war for EVs as part of the cause and told shareholders it would need another year to meet its target of 600,000 EVs produced annually.

Ford CEO Jim Farley said late last week: “The shift to powerful digital experiences and breakthrough EVs is underway and going to be volatile, so being able to guide customers through and adapt to the pace of adoption are big advantages for us. Ford+ is making us more resilient, efficient and profitable, which you can see in Ford Pro’s breakout second-quarter revenue improvement (22%) and EBIT margin (15%).”

CFO John Lawler said yesterday that the company “has ample resources to simultaneously fund disciplined investment in growth and return capital to shareholders – for the latter, targeting 40% to 50% of adjusted free cash flow,” Bloomberg added. He now says Ford is “not providing a date” for producing 2 million EVs per year, which was previously the company’s target for 2026.

Is the company pulling an Intel and “kitchen sinking” its guide for the year, or has Elon Musk’s price cuts over at Tesla really put the legacy automaker on the ropes? Ford reports again on October 26, where we’ll get our next glimpse into its continuing operations this year.

Tesla is down -26% since January 14, 2022. And showing a nice turnaround!

Today, the 10-year Treasury yield is up 11 basis points.

Bidenomics is where the Attorney General Garland gives Hunter Biden blanket amnesty and arrests Biden’s Presidential opponent. Welcome to the United Venezuelan States of America!e

But while Fitch cited “the expected fiscal deterioration over the next three years, a high and growing general government debt burden, and the erosion of governance relative to ‘AA’ and ‘AAA’ rated peers” as reasons for the downgrade, the Biden administration is of course blaming Donald Trump and his supporters due to one portion of Fitch’s explanation: “a steady deterioration in standards of governance over the last 20 years,” and that “repeated debt-limit political standoffs and last-minute resolutions have eroded confidence in fiscal management.”

Then on Wednesday, Fitch’s Richard Francis told Reuters that the downgrade was ‘due to fiscal concerns and a deterioration in U.S governance as well as polarization which was reflected in part by the Jan. 6 insurrection.’

“It was something that we highlighted because it just is a reflection of the deterioration in governance, it’s one of many,” he said, adding “You have the debt ceiling, you have Jan. 6. Clearly, if you look at polarization with both parties … the Democrats have gone further left and Republicans further right, so the middle is kind of falling apart basically.”

And so of course, the Biden administration is blaming Trump.

“This Trump downgrade is a direct result of an extreme MAGA Republican agenda defined by chaos, callousness, and recklessness that Americans continue to reject,” said Biden re-election campaign spokesman Kevin Munoz. “Donald Trump oversaw the loss of millions of American jobs, and ballooned the deficit with the disastrous tax cuts for the wealthy and big corporations.”

Ah, so now it’s the Trump downgrade™

Meanwhile, White House spox Karine Jean-Pierre also blamed Trump on Tuesday, saying that the White House “strongly” disagrees with the decision, adding “it’s clear that extremism by Republican officials — from cheerleading default, to undermining governance and democracy, to seeking to extend deficit-busting tax giveaways for the wealthy and corporations — is a continued threat to our economy.”

Former Clinton Treasury Secretary Larry Summers called the decision “bizarre and inept,” while former Obama economic advisor Jason Furman called the move “completely absurd.”

On Wednesday, CNBC wheeled out Jared Bernstein, chair of Biden’s Council of Economic Advisers and former Obama official, who similarly blamed Trump.

“I think again the timing issue is is Jermaine here. The deficit went up every year under President Trump. The debt to GDP ratio rocketed under President trump. It has stabilized admittedly at a higher level under this president but we’re doing all we can to try to ameliorate those tensions,” he said.

Bernstein reflected on the “cognitive dissonance” he felt at the downgrade amid the success of ‘Bidenomics’ commenting that “creditworthiness deteriorated significantly under President Trump for good reasons… and under President Biden, it started to track back up…”

Except that’s the exact opposite of what happened. According to the 100% non-partisan “market”, the creditworthiness of US Treasury debt improved almost constantly under President Trump and worsened dramatically almost immediately upon President Biden’s inauguration:

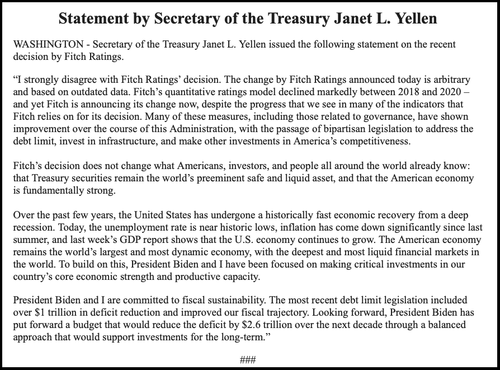

Treasury Secretary Janet Yellen said that the downgrade was “arbitrary and based on outdated data,” adding “Today, the unemployment rate is near historic lows, inflation has come down significantly since last summer, and last week’s GDP report shows that the U.S. economy continues to grow.”

CNN also blamed Trump, penning the headline: Fitch downgrades US debt on debt ceiling drama and Jan. 6 insurrection.”

The stupidity on CNN and Jared Bernstein are appalling. True, the media and Biden Administration are terrified of losing the 2024 Presidential election, but outright lies and misrepresenation are wrong no matter what.

But the claims that the US was downgraded because Trump’s economy lost miilions of jobs is ridiculous.

Actually, the US economy added 12.53 million jobs after April 2020 (Trump) while Bidenomics created took 2 1/2 years to add 12.56 million jobs. So, Biden took over twice as long to create jobs after Covid than it did under Trump. Simply opening the economy and schools produced that magical claim by Biden. And the National Teacher’s Union and Randi Weingarten worked with Fauci to orchestrate shutting down schools. Blaming Trump for local governments shutting down the economy is pure bunk.

Bidenomics and massive Federal spending is the cause for the downgrade. Not Trump.

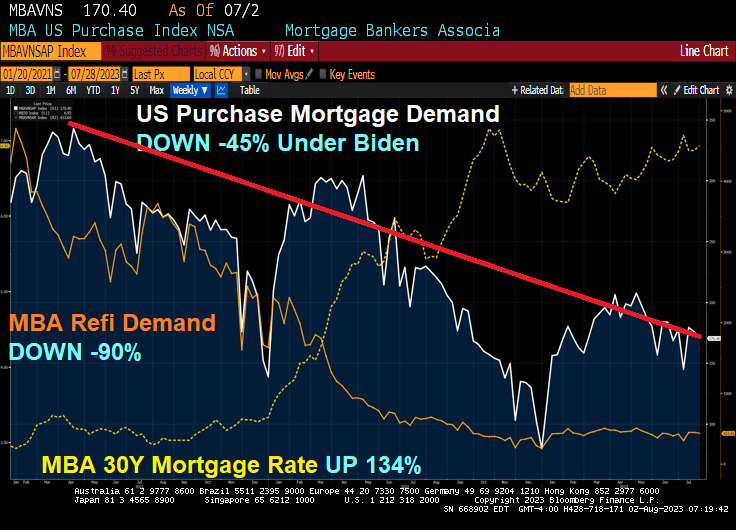

Inflation under Biden has been very painful for the US middle class and low wage workers. That inflation has resulted to surging mortgage rates thanks to The Fed’s counterattack.

The result? Mortgage rates are up 134% under Bidenomics, while mortgage purchase demand is down -45% since Biden was selected. And mortgage refinancing demand is down a staggering -90%!

Mortgage applications decreased 3.0 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending July 28, 2023.

The Market Composite Index, a measure of mortgage loan application volume, decreased 3.0 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index decreased 3 percent compared with the previous week. The Refinance Index decreased 3 percent from the previous week and was 32 percent lower than the same week one year ago. The seasonally adjusted Purchase Index decreased 3 percent from one week earlier. The unadjusted Purchase Index decreased 3 percent compared with the previous week and was 26 percent lower than the same week one year ago.

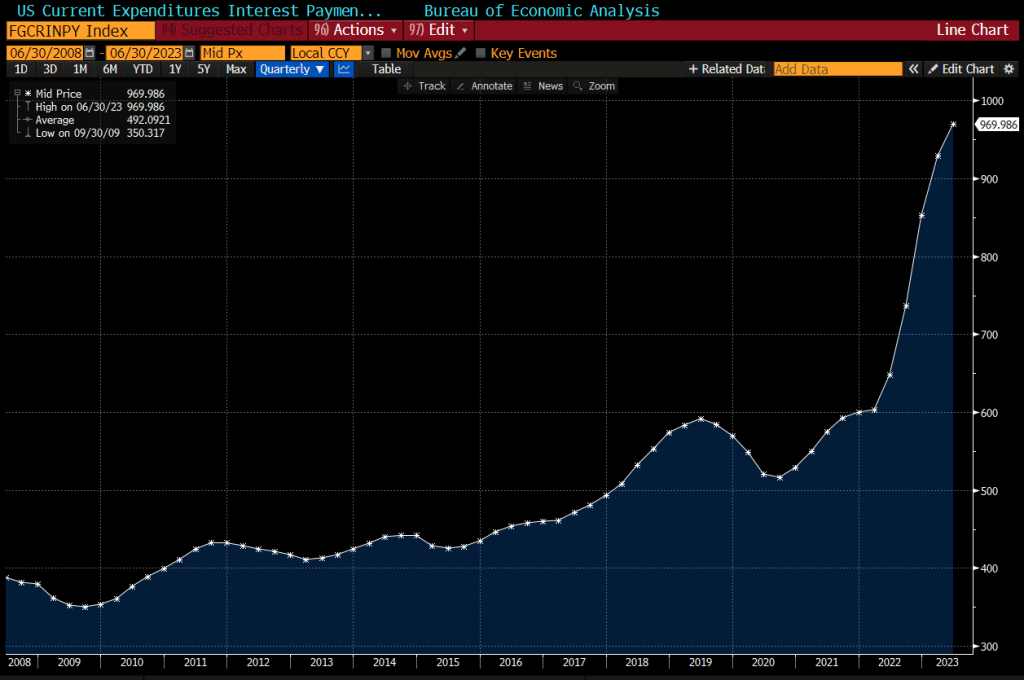

US interest expenses have surged by about 50% in the past year, to nearly $1 trillion on an annualized basis.

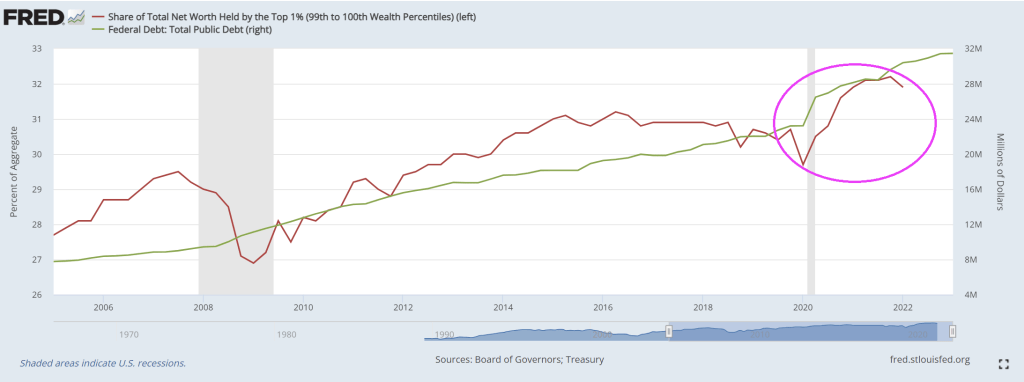

Look at the share of net worth by the top 1% as Treasury borrows more money.

Oddly, Biden is not talking about about putting US government policies up for sale to the highest bidders. But don’t worry. Biden is the King of Corruption in the District of Corruption (Washington DC).

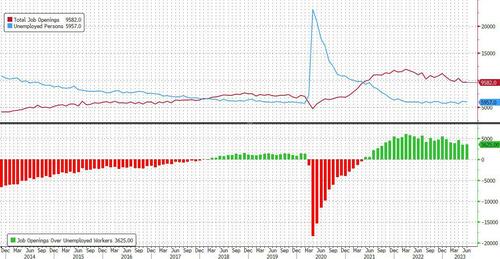

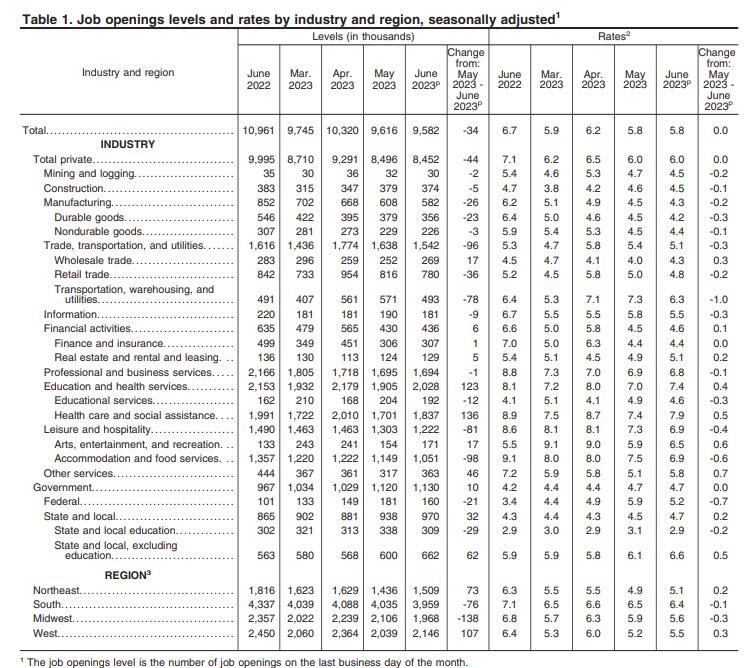

The number was about 1.4 million below the 11 million from a year ago and below the consensus estimate of 9.6 million, a rare miss in a series which has been best known for decisively beating Wall Street’s expectations.

According to the BLS, the largest increases in job openings was in health care and social assistance (+136,000) and in state and local government, excluding education (+62,000). Job openings decreased in transportation, warehousing, and utilities (-78,000), state and local government education (-29,000), and federal government (-21,000)

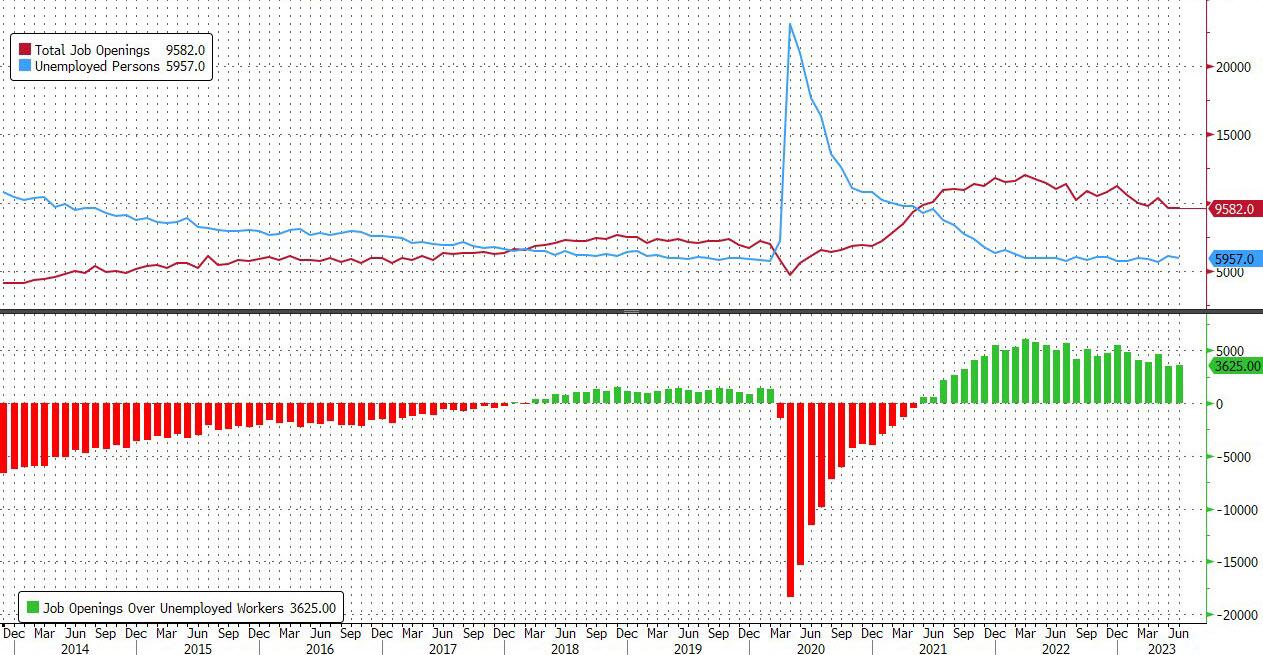

The slide in the number of job openings meant that after rising to the highest since January 2023 in April, in June the number of job openings was just 3.7625 million more than the number of unemployed workers, the lowest since Sept 2021.

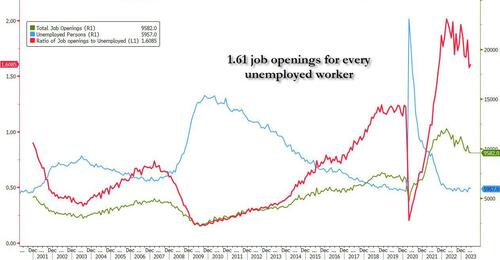

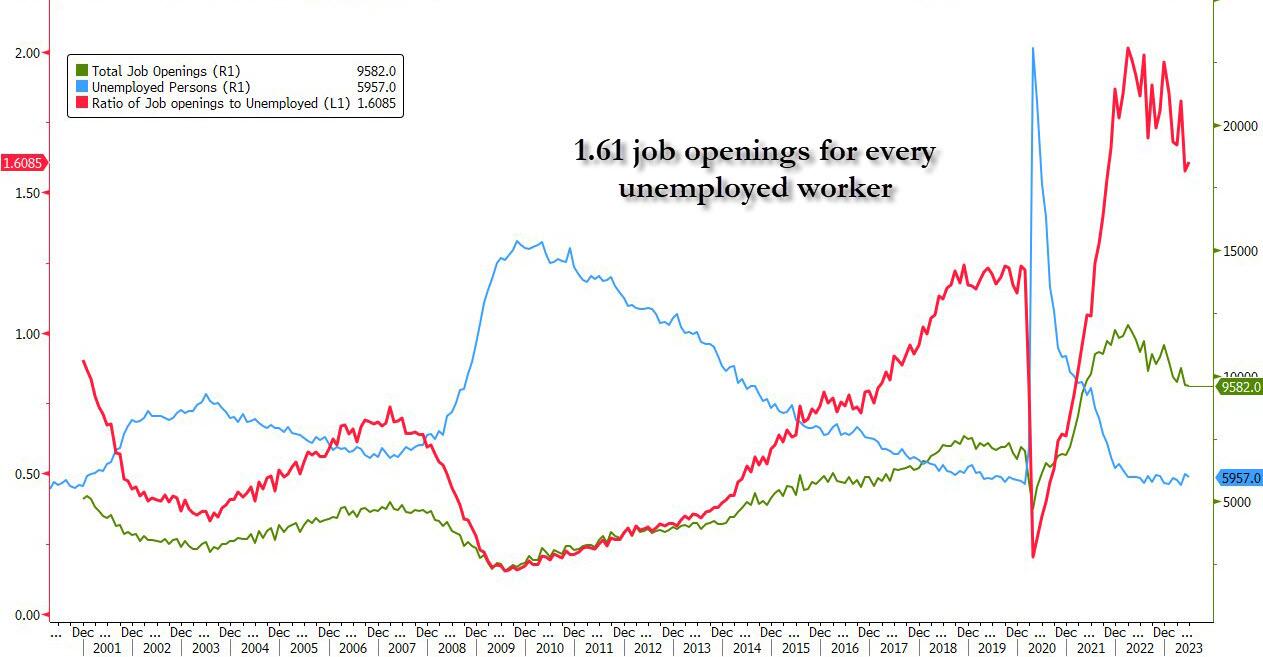

Said otherwise, after rising to 1.82 openings for every worker in April, in June the number dropped to just 1.61, which would have been the lowest level since Oct 2021 if it weren’t for last month’s sharp downward revision.

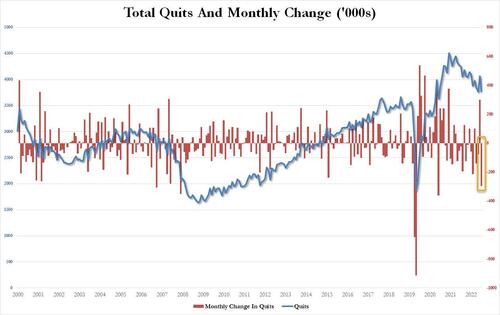

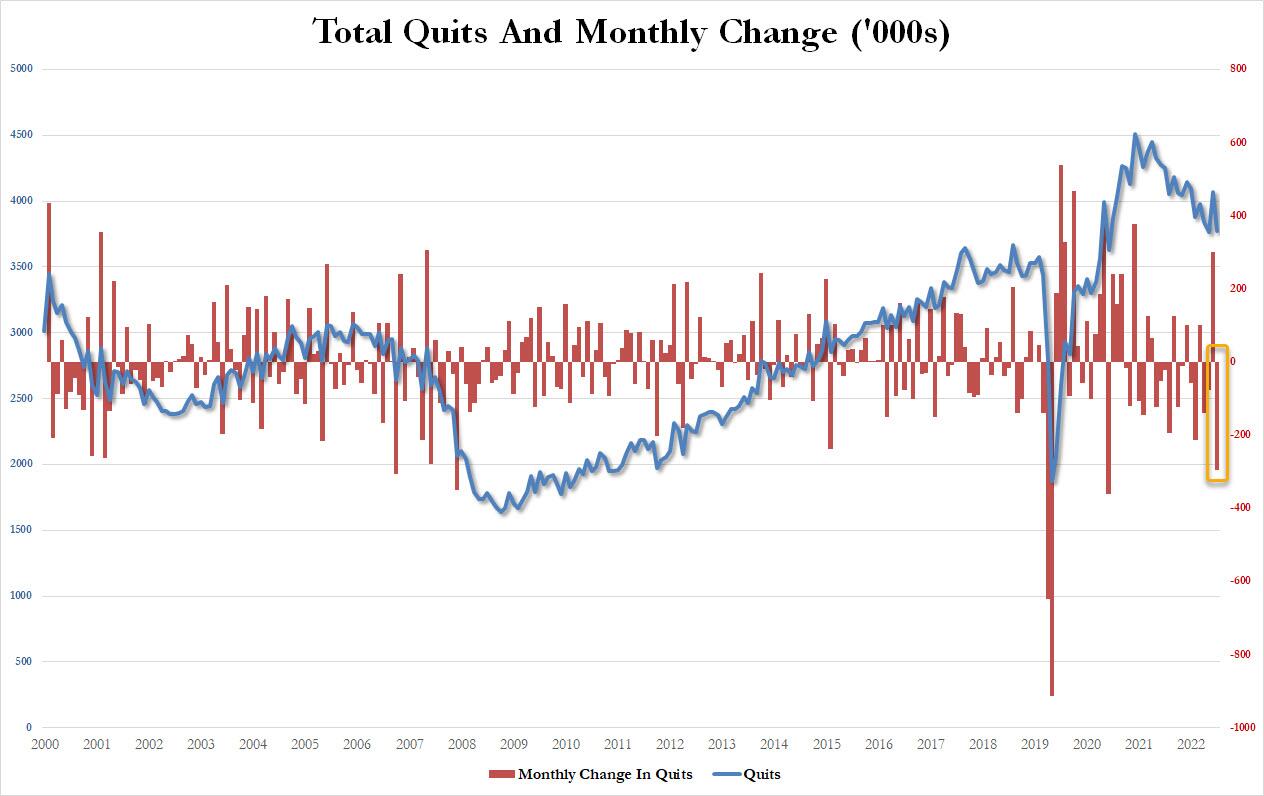

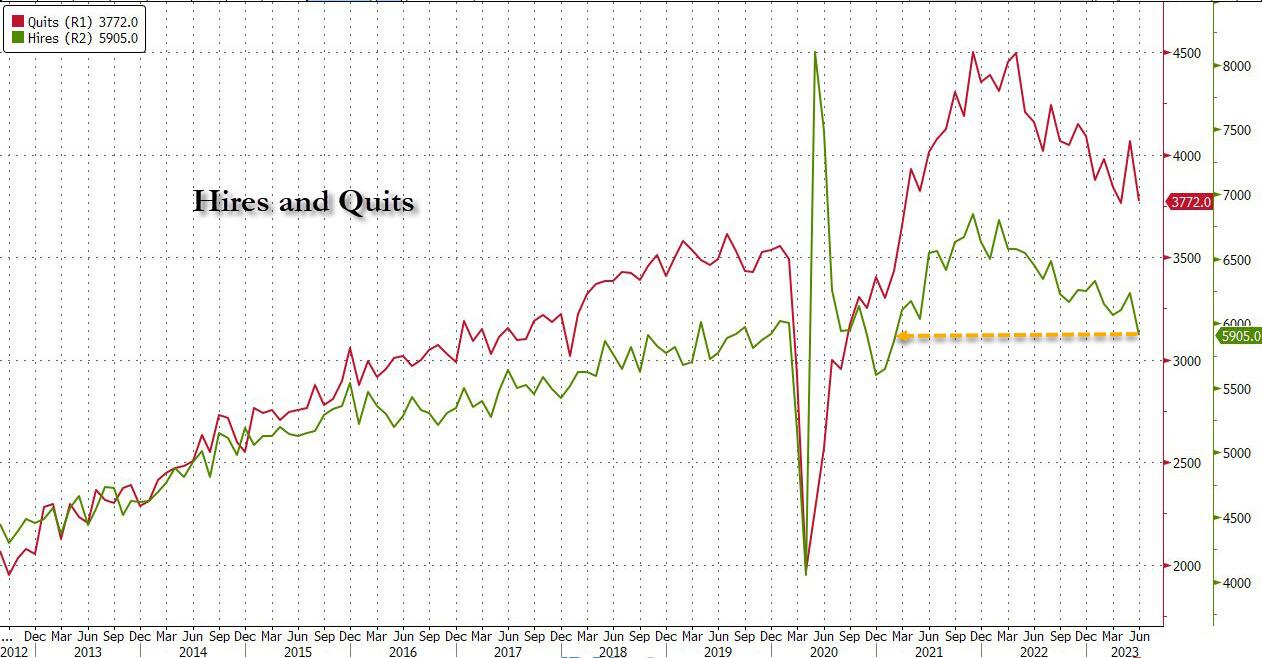

Yet even as the number of job openings dropped only modestly from the (sharply) downward revised print for May (because under Biden, no number is ever revised stronger), conflicting data remained and in June, the number of people quitting their jobs – an indicator traditionally associated with labor market strength as it shows workers are confident they can find a better wage elsewhere – unexpectedly tumbled by 295K to just 3.772MM, the biggest monthly drop since May 2021.

According to the BLS, the number of quits decreased in several industries, with the largest decreases in retail trade (-95,000), health care and social assistance (-75,000), and construction (-51,000). The number of quits increased in arts, entertainment, and recreation (+20,000).

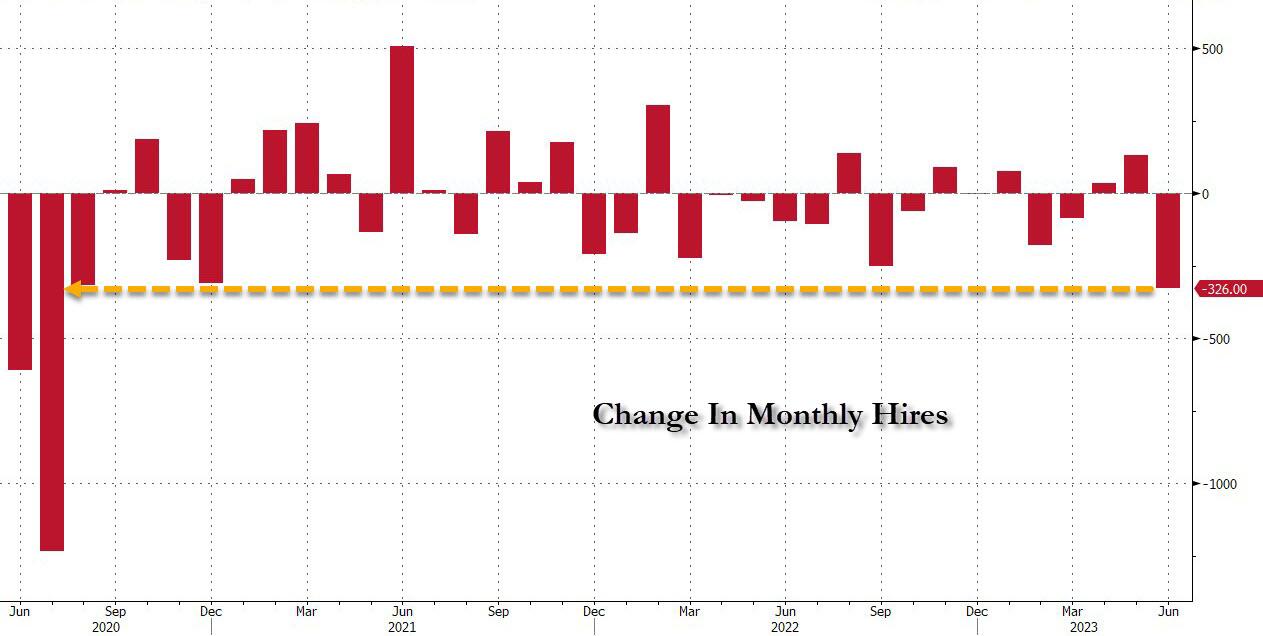

And just in case some still believe Biden’s strong jobs lie, the number of hires also tumbled in June, crashing by 326K – the biggest monthly drop since July 2020…

… to 5.905MM, the lowest since February 2021.

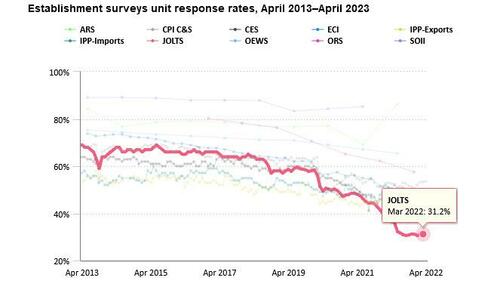

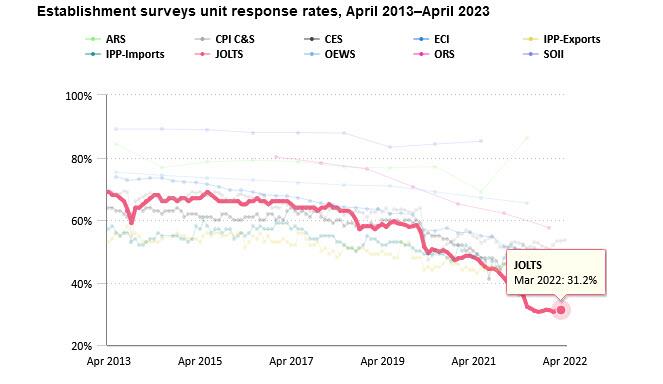

Of course, as we have explained on multiple occasions previously, none of the above data actually matters or is credible for the simple reason that the response rate of the JOLTS survey is stuck at a record low 31.2%. Which means that only those who actually have job openings to report do so, while two-thirds of employers are either non-responsive or their mail is quietly lost in the mail.

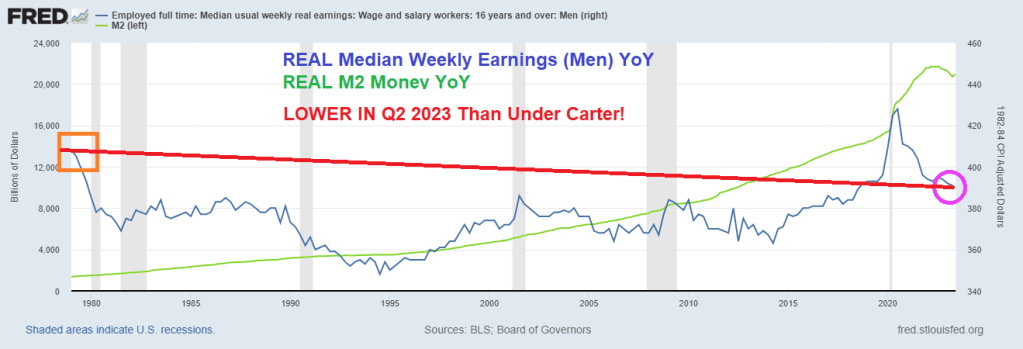

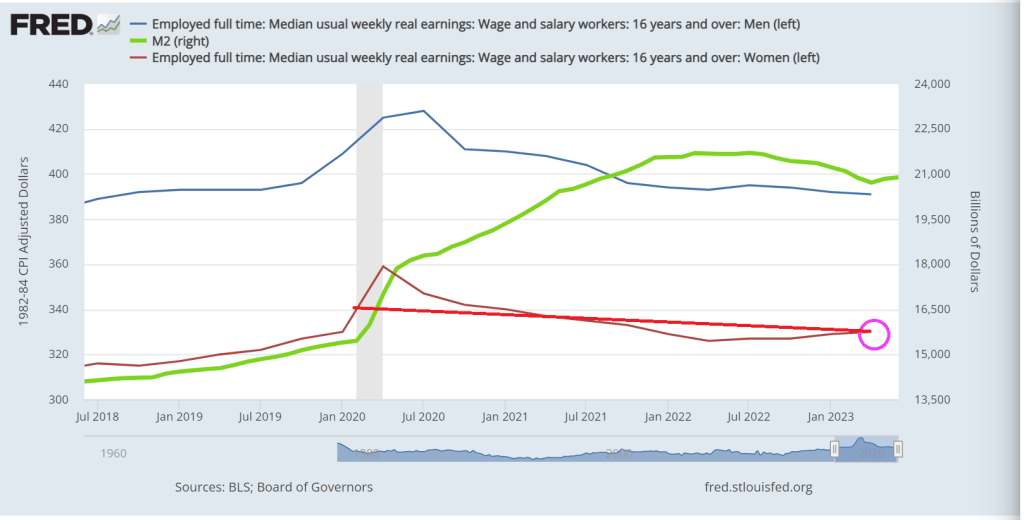

President Jimmy Carter is usually the bar for terrible Presidents. Under Carter, the US experienced economic stagnation and soaring inflation. At least it led to the election of Ronald Regan!

So, Biden’s much mentioned Bidenomics have produced REAL MEDIAN WEEKLY EARNINGS FOR MEN that is currently below 1979 levels under Jimmy Carter.

Even worse for Bidenomics, REAL MEDIAN WEEKLY EARNINGS GROWTH FOR MEN was -4.45% In April 2023, while the last reading prior to Covid under Trump was 6.674% YoY in February 2020. So, Bidenomics isn’t even back to Trump levels for men.

I like this chart which I call “Yellenomics” because it illustrates The Fed’s Folly of money printing and its impact on real earnings. After the Trump wage growth boom, real median weekly earnings for men has been steadily declining.

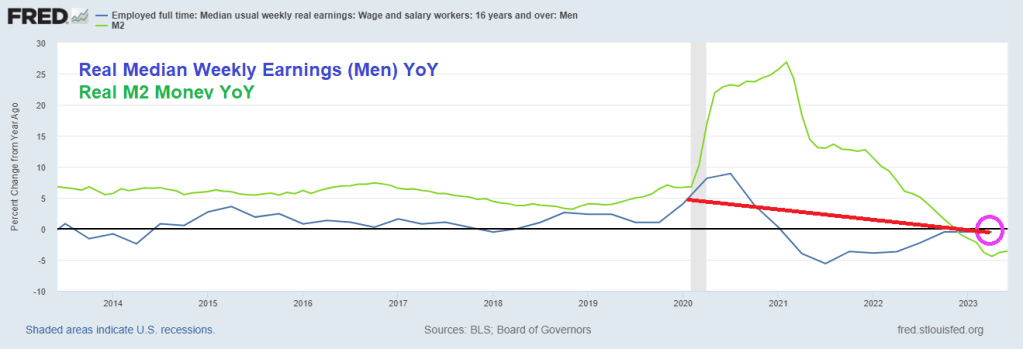

Women, on the other hand, did show a gain since Carter, but still lower than the last month before Covid struck. Women’s real median weekly earnings growth YoY since Q2 2021 are down -5%. So, Bidenomics has been less sucky for women than men.

Reminds me of The Yardbird’s classic “I’m A Man.” Worse off under Biden than under Jimmy Carter. Although The Yardbird’s “Over Under Sideways DOWN” is more emblematic of Bidenomics.

Bidenomics should be renamed Corruptionomics given Biden’s habit of selling government influence to anyone willing to waive a few million.

Bidenomics, aka the Federal government takeover of the US economy with Soviet-style economic central planning, is highly dependent on loose Federal Reserve monetary policy (Janet Yellen and Powell’s wild overreaction to the massively inappropriate Covid shutdowns),

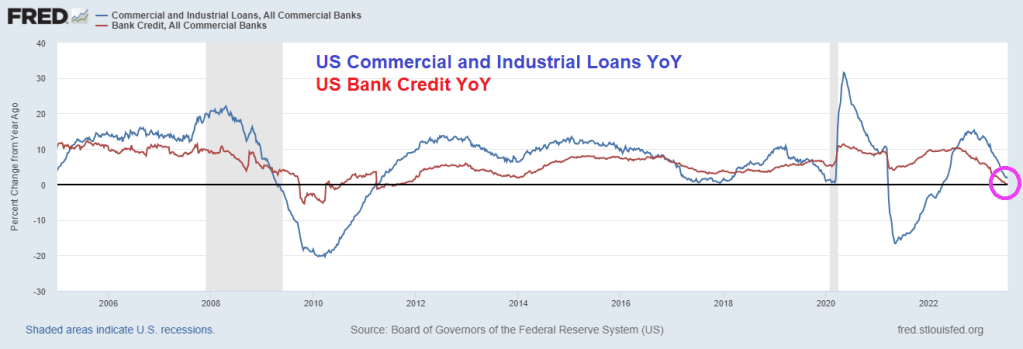

So, how is Bidenomics working out? On the bank lending front, commercial and industrial (C&I) lending growth is crashing along with bank credit growth YoY.

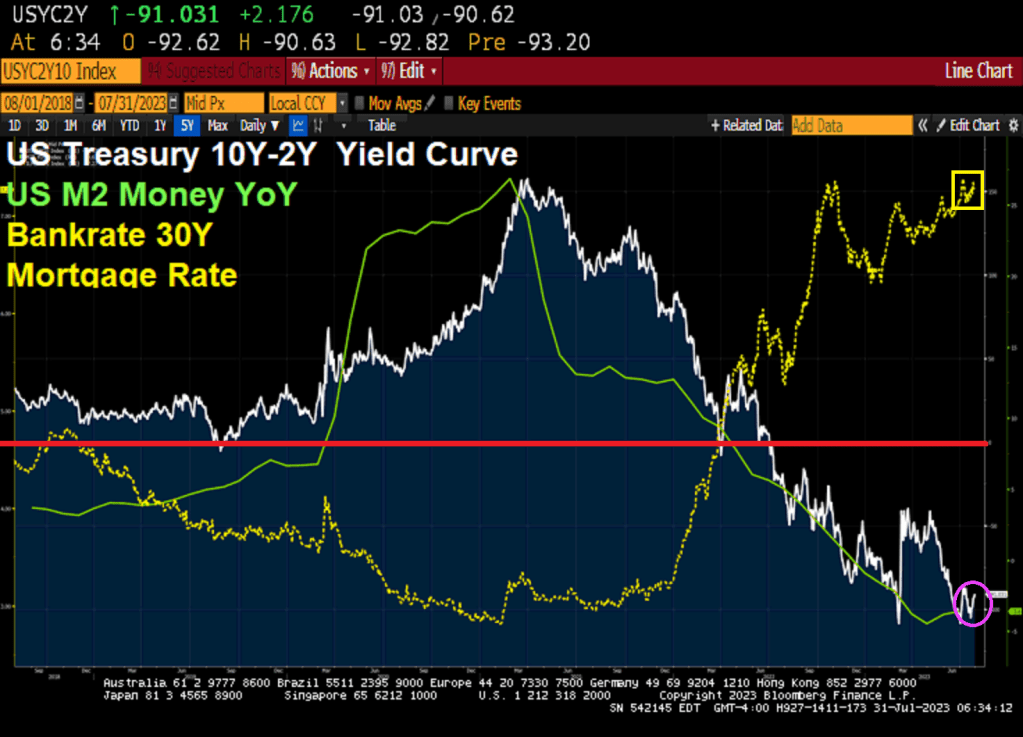

The US Treasury 10Y-2Y yield curve remains deeply inverted at -91.031 basis points and M2 Money growth has crashed. The 30 year mortgage rate is hovering around 7.27%.

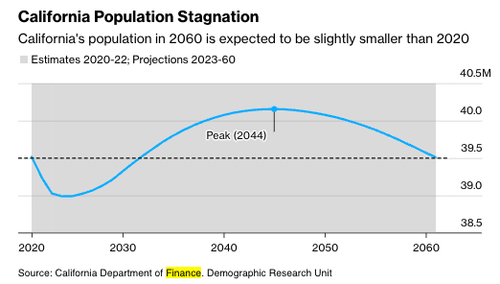

The Republicans’ little red book is showing people escaping big crime and tax states like New York and California for lower tax, lower crime states like Florida and Texas. But to Democrats who are really bad at math, 7+7 = 0?

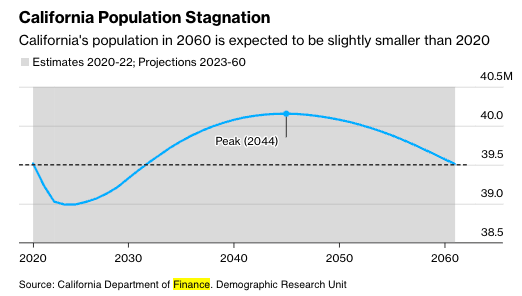

California and New York have sustained population declines during Covid and after, that have long-term implications for local economies. The exodus means workers with six-figure salaries in technology, finance, real estate, and entertainment are going elsewhere, which will reduce tax revenue for the state.

MyEListing.com, an online real estate portal, used IRS migration data to reveal California and New York lost $343 million and $299 million in 2021, respectively, due to the surge in migration outflows.

The beneficiaries of the outflow are Florida and Texas, which took in $12.4 billion and $10.7 billion, respectively.

“Despite its numerous attractions, from the booming tech industry and world-class universities to beautiful landscapes and cultural richness, California’s high personal income tax rates seem discouraging for many high-wealth individuals. This, coupled with the state’s high cost of living, will likely fuel a wealth migration out of California,” MyEListing wrote in the report.

The exodus from California is so severe that state demographers forecasted the total population will be the same today as in 2060.

If left unchecked, the largest outflows of residents from specific metro areas could experience a fiscal crisis. Such a development would be tragic for Democrat-controlled cities already plunging into crisis as progressive politicians fail to enforce law and order.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

You must be logged in to post a comment.