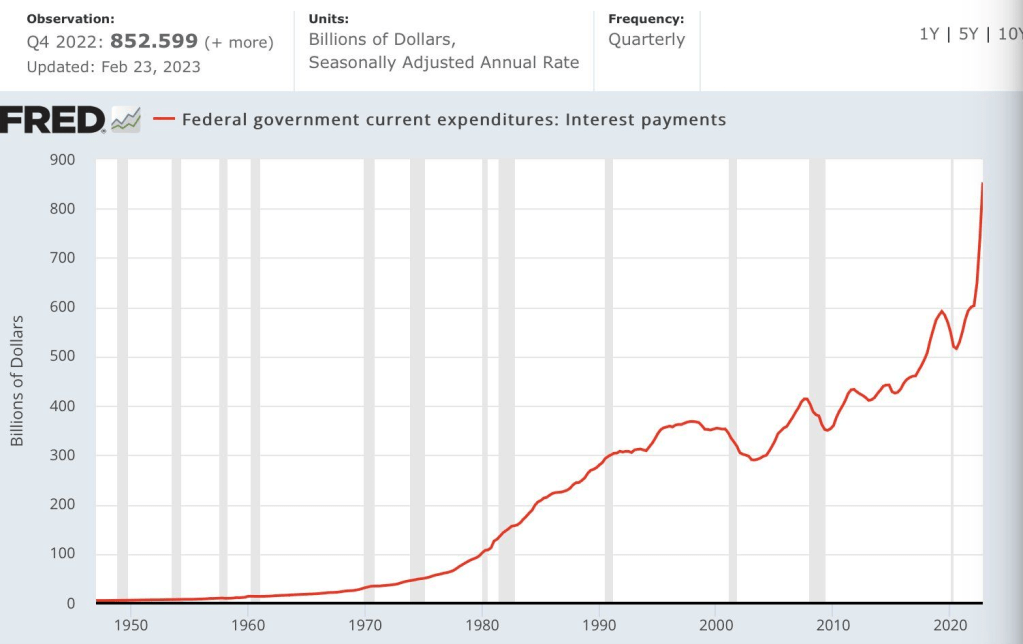

The last US debt crisis occured in 2013 when Congress finally raised the debt ceiling … and kept on borrowing and spending, But if you thought that a debt crisis would scare Congress (and the Administration) into balancing the Federal budget, you would be wrong. In fact, since the 2013 debt crisis, Federal debt is up 88% (+$14.7 TRILLION over the last 10 years).

And with the massive growth in Federal debt under Obama, Trump and Biden has resulted in an explosion in interest payments on the Federal debt.

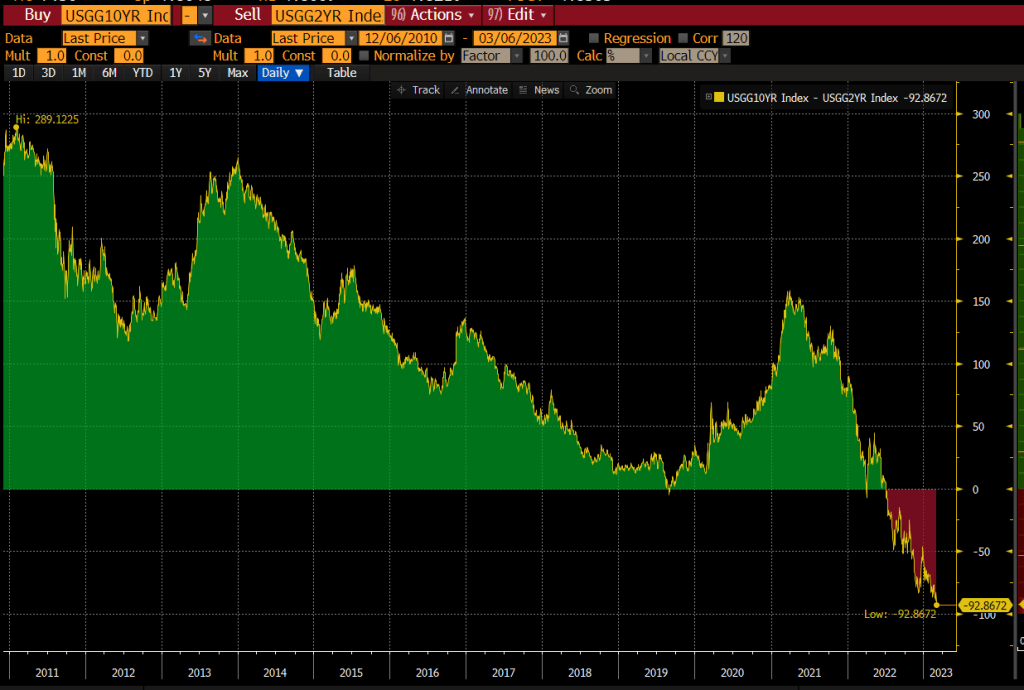

Interest rates are an important driver of the economy and financial markets. And what has happened to the S&P 500 index since The Federal Reserve started raising their target rate on May 4, 2023 to fight surging inflation?

Since that fatal day, the S&P 500 index has fallen -6% and equity REITs (commercial real estate) has fallen -16%.

What about returns on US Treasuries and Mortgage-backed Securities (MBS)? Same thing. PAIN!

Although The Fed has pledged to keep raising rates to fight inflation (and further decimate retirement accounts), investors are pointing to a peak (terminal) Fed rate of 5.44% at the September 2023 FOMC meeting. Then rate cuts following the September 2023 meeting.

Of course, much of the blame belongs to former Fed Chair Ben (QE) Bernanke and current Treasury Secretary Janet “Too Low For Too Long” Yellen who never met a Fed rate hike that she liked. But Yellen LOVES giving away US taxpayer dollars … to Ukraine.

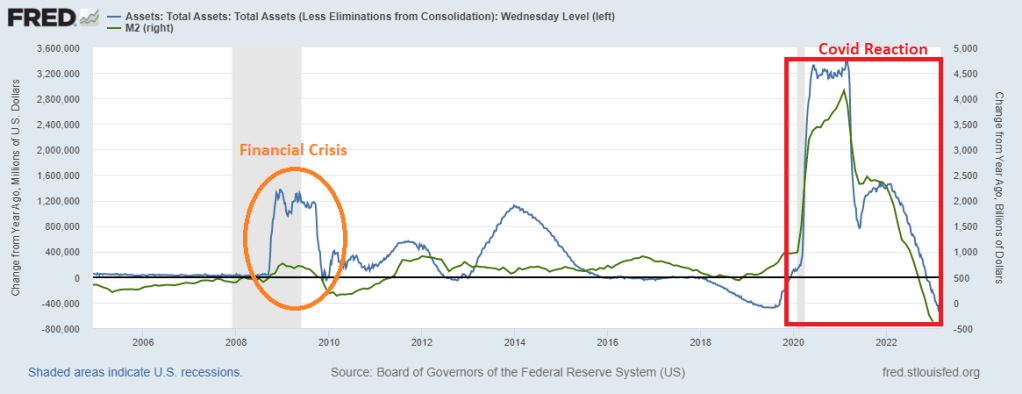

But despite how bad the financial crisis of 2008/2009 was, the growth of Fed assets on it balance sheet (orange oval) paled in comparison to The Fed’s overreaction to the Covid outbreak of 2020. And the government shutdowns and mask mandates.

The good news? The rate of growth YoY of both The Fed’s balance sheet and M2 Money is negative. But it is still startling to see the comparison of Fed reactions to crises.

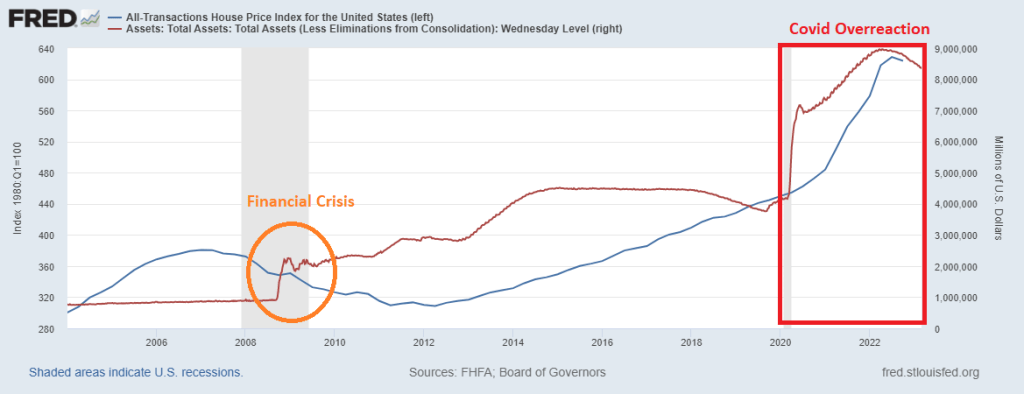

Give The Fed three steps to catch up to the mayhem they created. Particularly in inflation home prices.

Yesterday’s inflation report (in the form on skyrocketing labor costs) helped lead Bankrate’s 30-year mortgage rate to over 7% … again.

Here is yesterday’s horrible unit labor costs YoY chart showing the fastest growth in labor costs since 1982 and Fed Chair Paul Volcker. Jerome Powell, the current Fed Chair is trying to reduce the Bernanke/Yellen/Powell monetary stimulypto (with an extra dose of “sugar” from the Covid outbreak).

The good news is that the 10-year Treasury yield is down -7.3 basis points this morning.

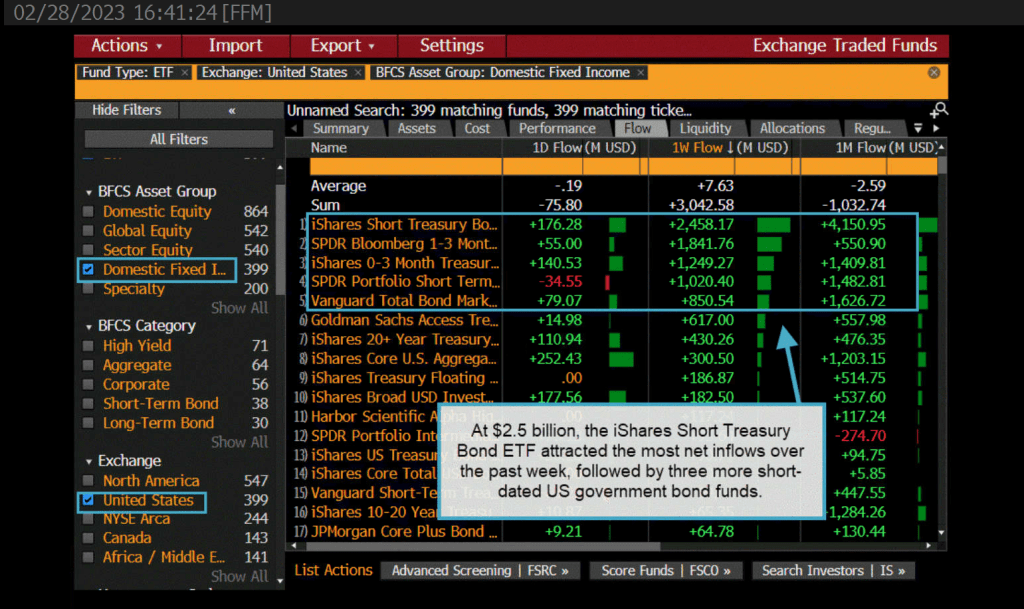

As The Federal Reserve reaffirms their draining of the monetary punch bowl, we are seeing investors flock towards the bond market. Particularly the iShares Short Treasury ETF. $2.5 BILLION to be exact.

Meanwhile, credit ETFs are hammered by record outflows of almost $12 Billion.

The reason why? Inflation remains elevated which is leading The Fed to keep their foot on the monetary brake pedal.

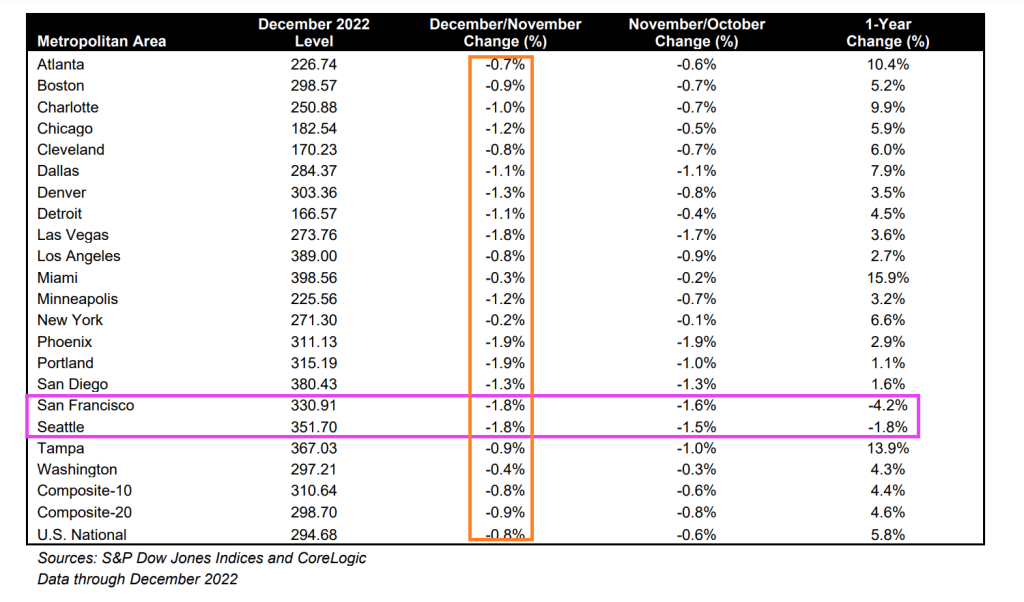

Only Seattle and San Francisco experienced negative growth in home prices on a year-over-year basis. All of the top twenty metro areas experience negative month-over-month price declines from November to December.

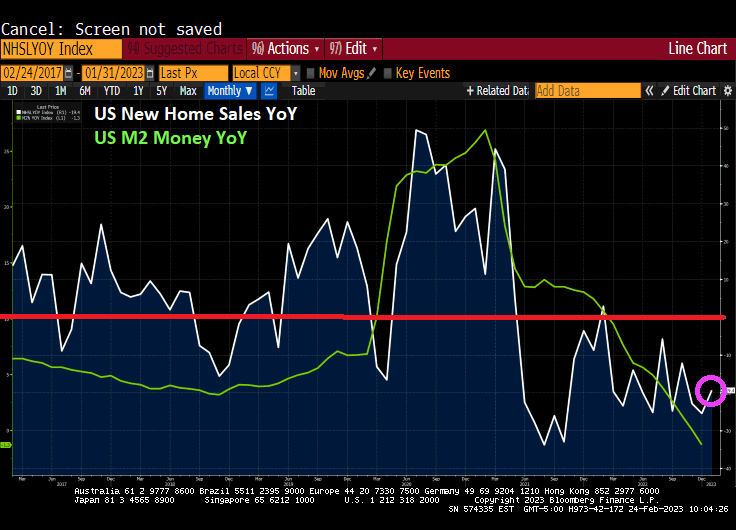

Another sign of a not healthy economy is housing. New Home Sales collapsed -19.4% from January 2022 (aka, year-over-year or YoY).

If I were Joe Biden, I would be touting the month-over-month numbers, up 7.20% from December to January. But the reality is that year-over-year new home sales are down -19.4%.

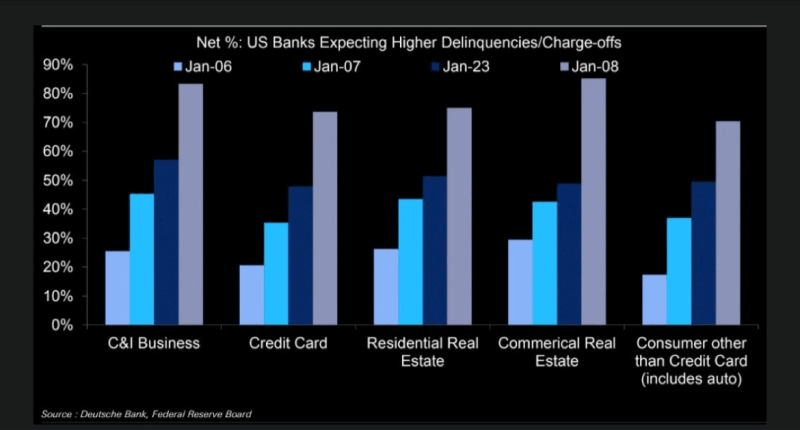

Also, on the “Alarm!” front, US banks are expecting higher delinquencies, including on residential mortgages.

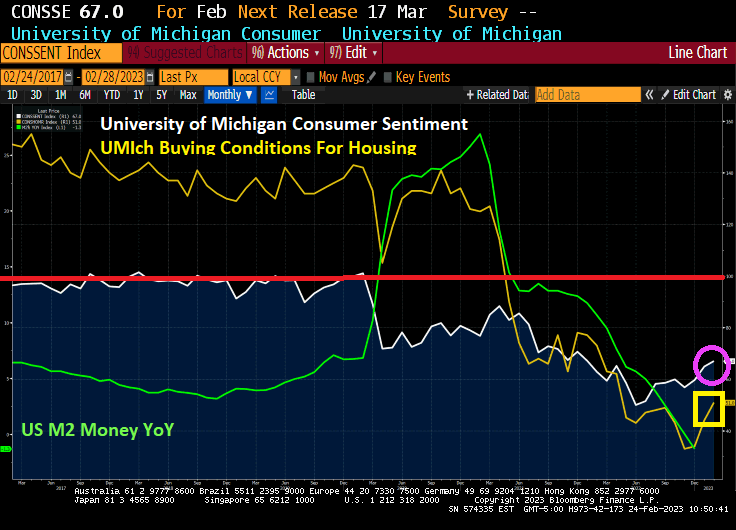

University of Michgan consumer sentiment for housing is rising, but still woefully below the 100 benchmark.

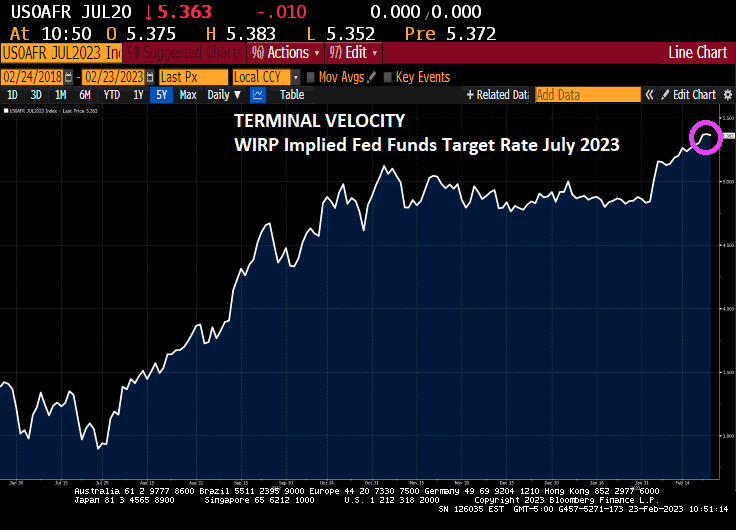

The terminal Fed Funds target rates is now 5.363% for the July FOMC (Fed Open Market Committee) meeting in 2023.

This comes as US Q4 GDP was revised lower on weaker consumer spending, revised downward to 1.4%

With the revision of Personal Consumption, real GDP was revised downward to 2.7% annualized QoQ.

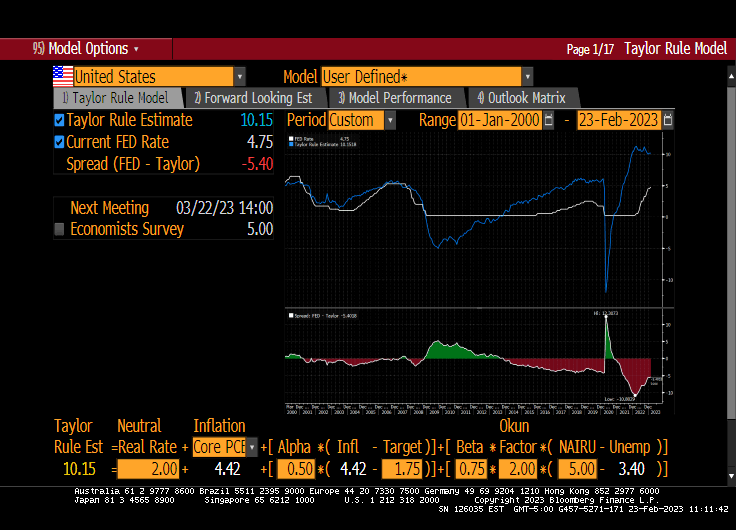

The Taylor Rule estimate for The Fed Funds Target rate is 10.15%. The Fed is only at 4.75%, so there is a long way to go! Except that The Fed doesn’t follow any useful rule like the Taylor Rule. Just the “seat of the pants” rule.

You must be logged in to post a comment.