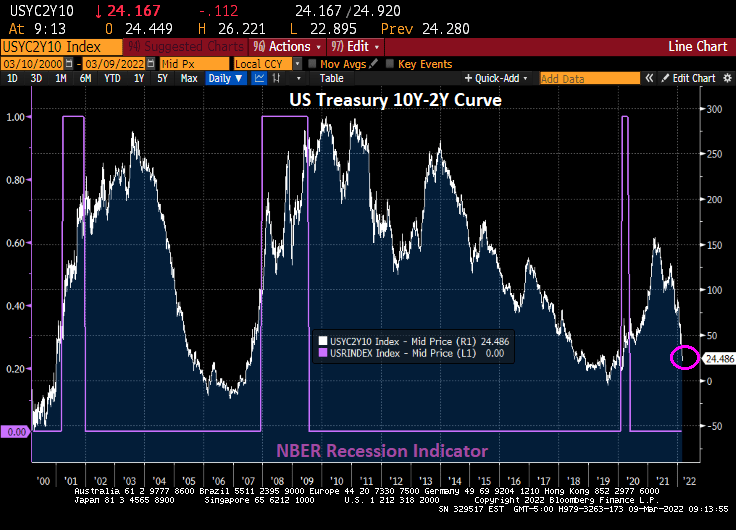

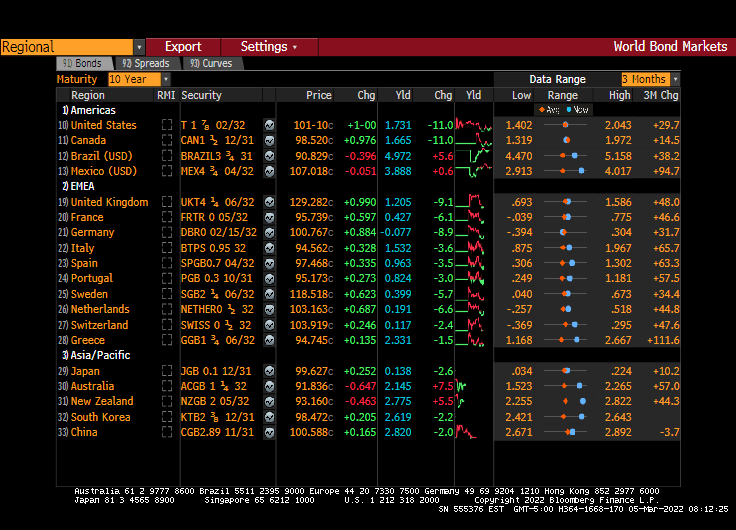

The US Treasury yield curve (10Y-2Y) is rapidly approaching inversion at 20.5 bps (where the 10-year yield is lower than the 2-year yield). But the 10Y-3M curve is generally steepening at 173.33 bps.

Of course, the driving force behind the flattening of the 10Y-2Y curve is the rapidly rising 2-year Treasury yield (orange line). The last time the 10Y-2Y curve inverted was in 2019, prior to the COVID outbreak in early 2020.

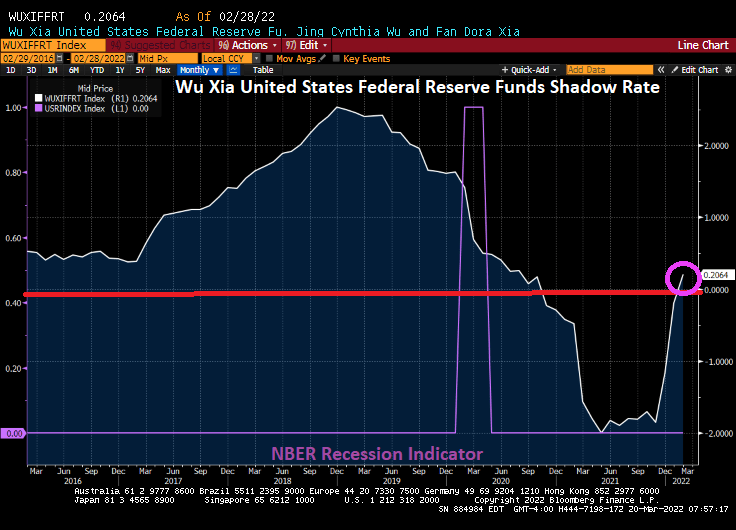

The Wu Xia United States Federal Reserve Funds Shadow Rate has finally climbed back into positive territory.

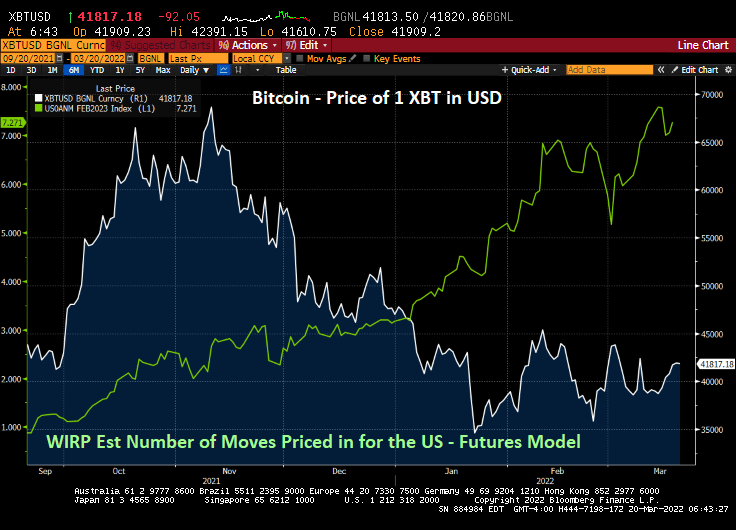

At last look, The Federal Reserve is forecast to raise their target rate 7 times over the coming year. And with the increasing forecast of rate hikes, we are seeing the cryptocurrency Bitcoin fall from near $70,000 to $41,817.

President Biden announced that he will be issuing an executive order to combat rising energy prices (the rising energy prices that he caused in the first place with … executive orders). Let’s see what happens next.

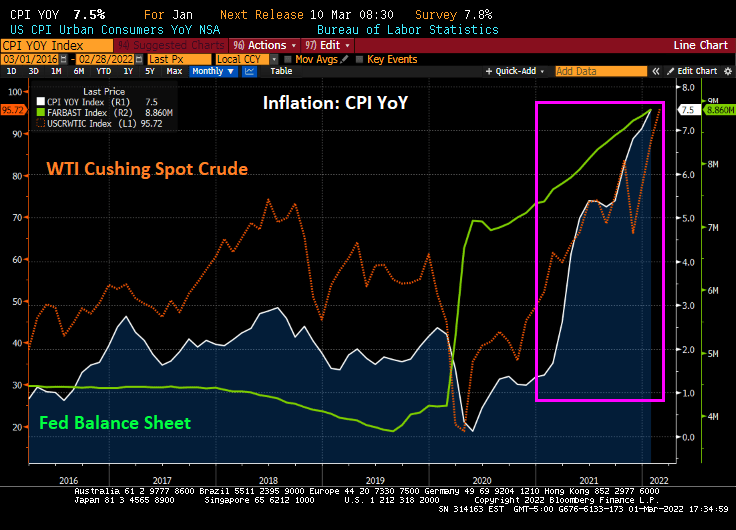

The news just keeps getting worse and worse. Russia is still assaulting Ukraine, WTI Crude prices are above $100 a barrel and climbing, the Cleveland Browns signed Deshaun Watson to replace Baker Mayfield at quarterback, etc.

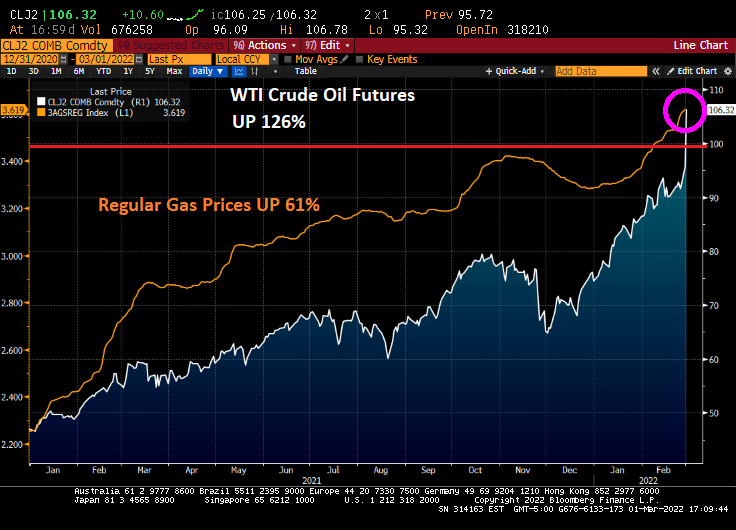

But back to energy prices. Since Biden was sworn-in as President, WTI Crude Oil futures are up 125%, regular gasoline prices are up 89%, and diesel fuel prices are up 155%. Diesel is important since America uses diesel-powered trucks to transport goods to market.

Globally? The world inflation rate has grown from 2% in January 2021 to 6.82%. Global food prices are up 24%.

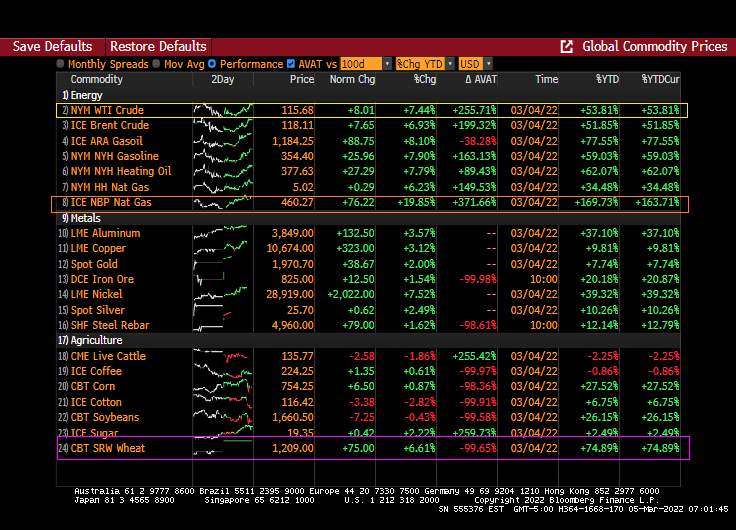

Yes, WTI Crude and Brent Crude are above $100 per barrel.

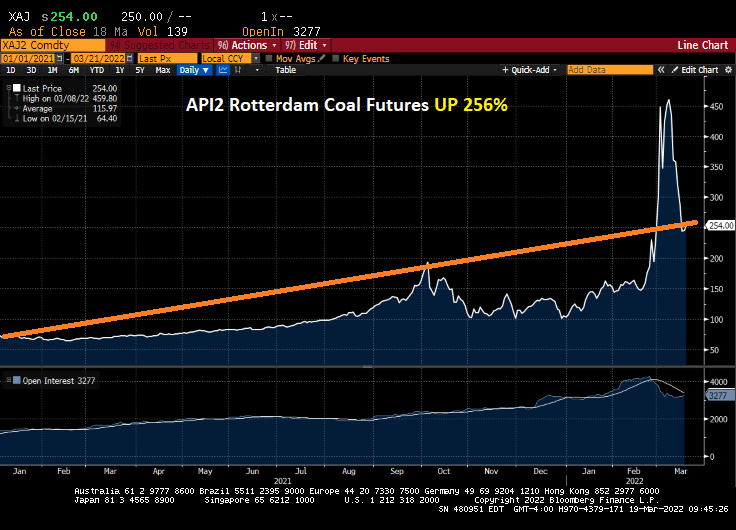

And coal prices are up 256% under Shoeless Brainless Joe.

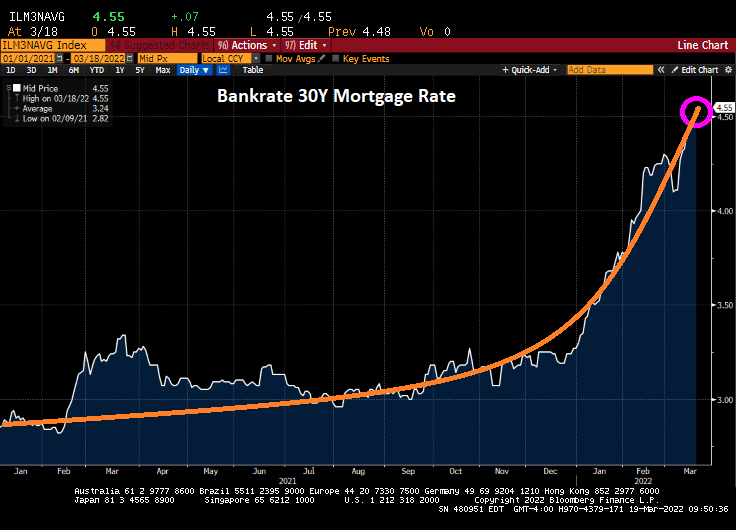

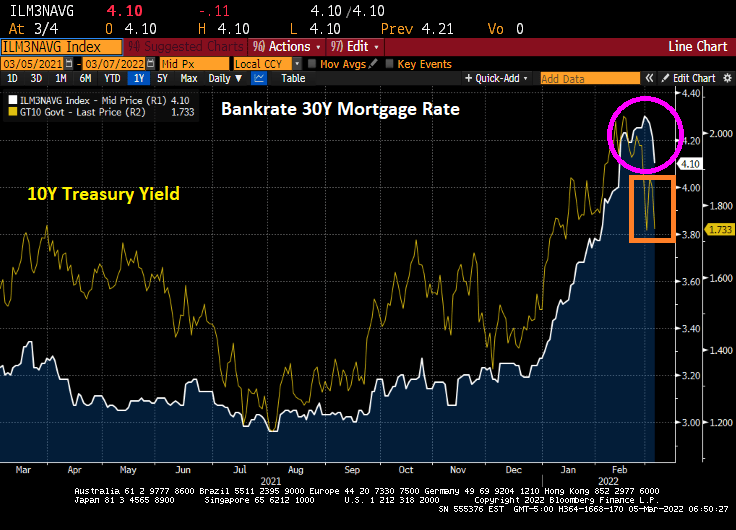

Mortgage rates? Bankrate’s 30-year mortgage rate is now above 4.50%.

Let’s see if Dr. StrangeFedpolicy raises rates as aggressively as signaled.

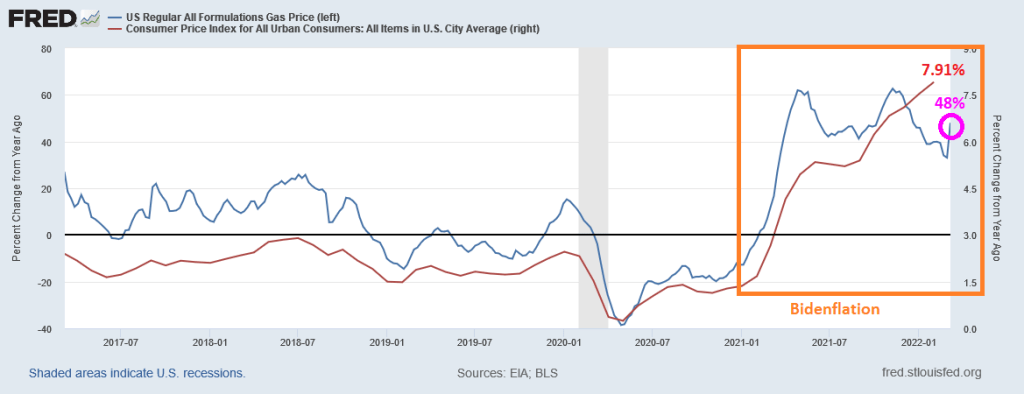

Well, so much for rising gasoline prices being the fault of Vlad “The Ukrainian Impaler” Putin and Russia invading Ukraine. In fact, gasoline prices were rising at a 62% YoY pace in April 2021, well before Russia’s invasion of Ukraine.

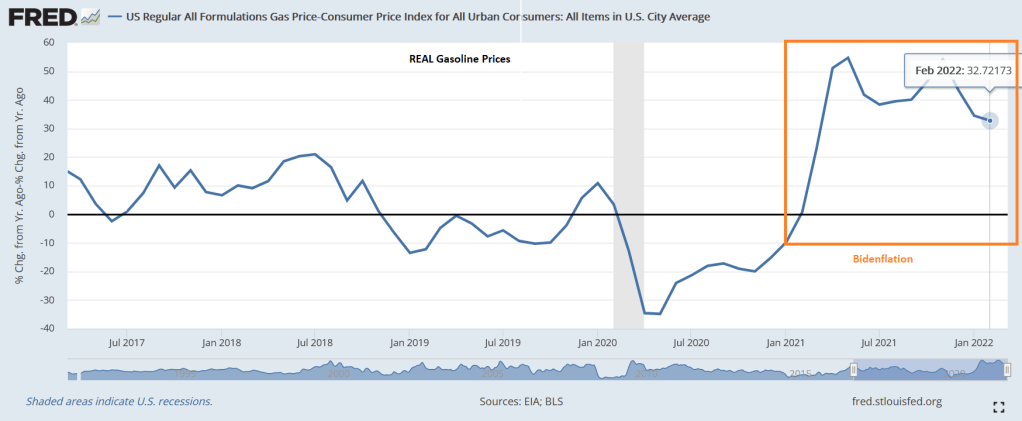

REAL gasoline prices (nominal gasoline prices less inflation) are up 32.72% YoY in February.

Press secretary Jen Psaki can take the opportunity to proclaim that REAL gasoline prices have actually declined in February.

I keep waiting for the Biden Administration and Congress to launch price controls and supply rationing rather than simply allow the Keystone Pipeline to be built and allow drilling on Federal lands.

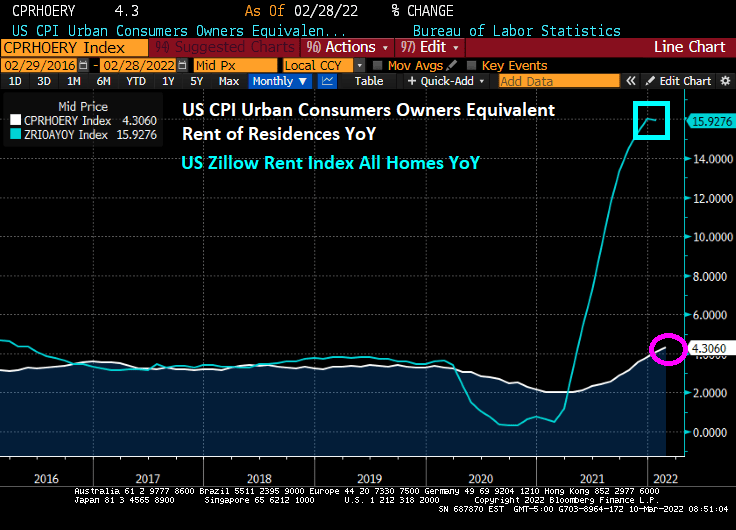

US rent inflation (owner’s equivalent rent of residence YoY) surged to 4.30%. However, Zillow’s rent index last month was 15.93% YoY.

But if we look at US Monthly Rent YoY, we see that rents are climbing at a 17.6% rate.

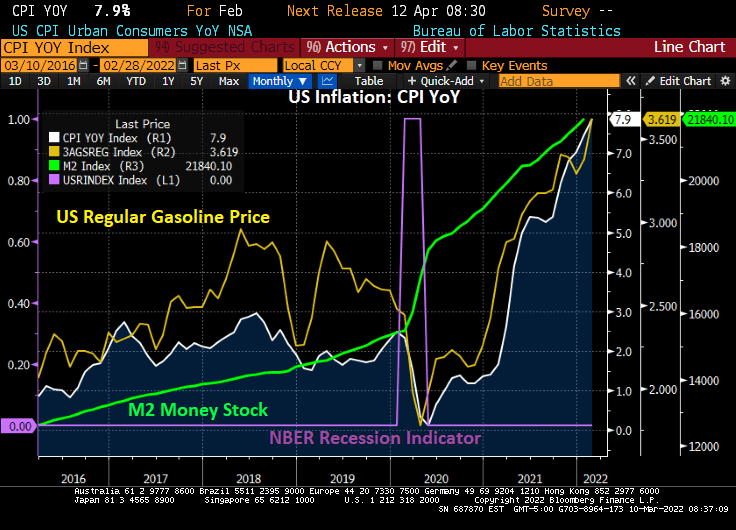

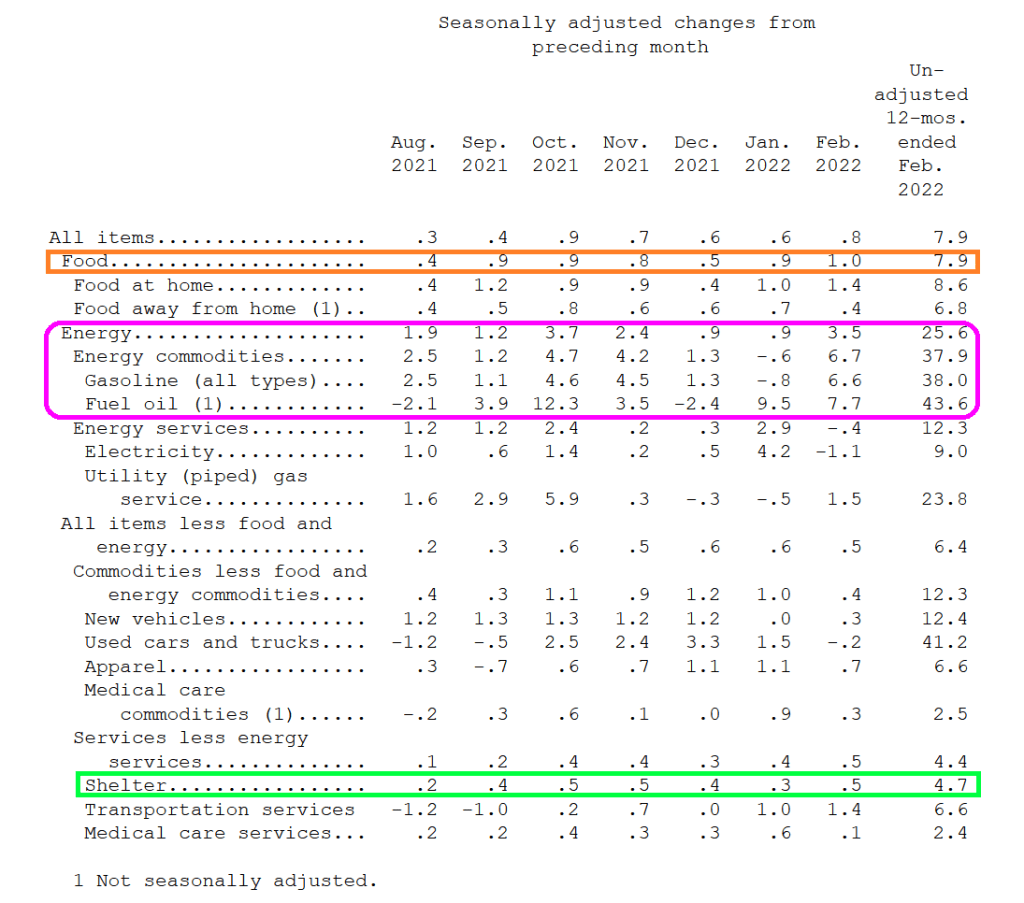

Energy costs soared in February YoY. Gasoline was up 38%. Fuel Oil was up 43.6%. Food was up 7.9%.

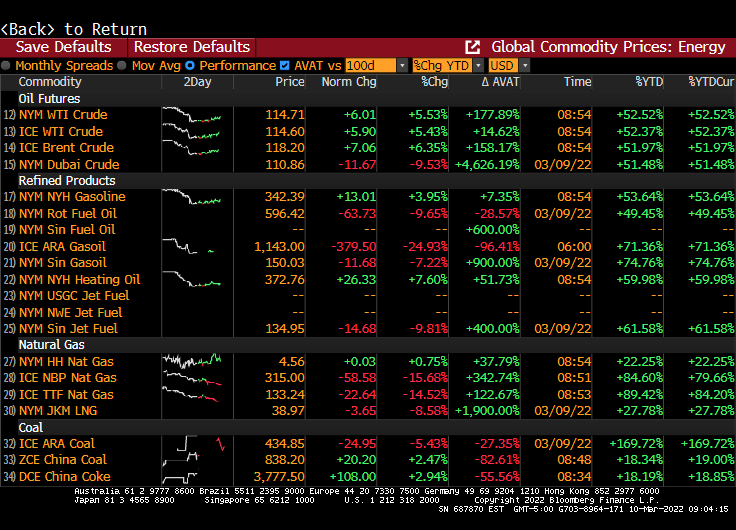

Volatility (AVAT) rages in the energy sector.

There are still 7 rate hikes in the cards from The Federal Reserve.

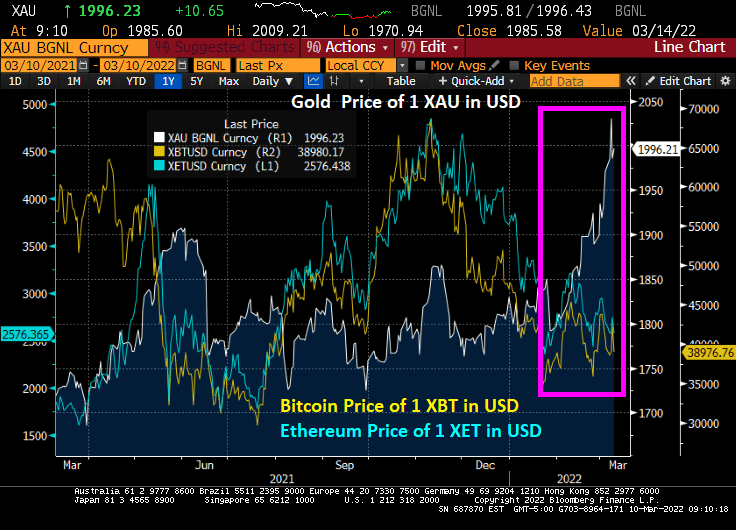

Gold has been climbing as Russia invades Ukraine. Cryptos Bitcoin and Ethereum are steady, even as the Biden Administration issues an executive order to “study” cryptocurrencies.

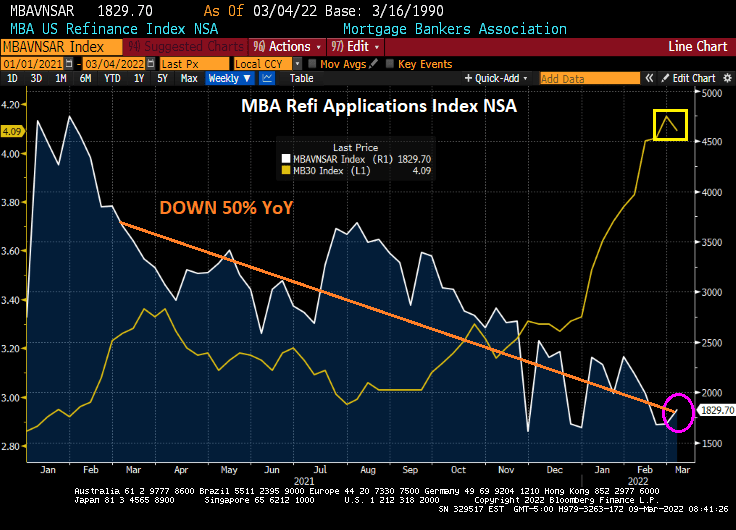

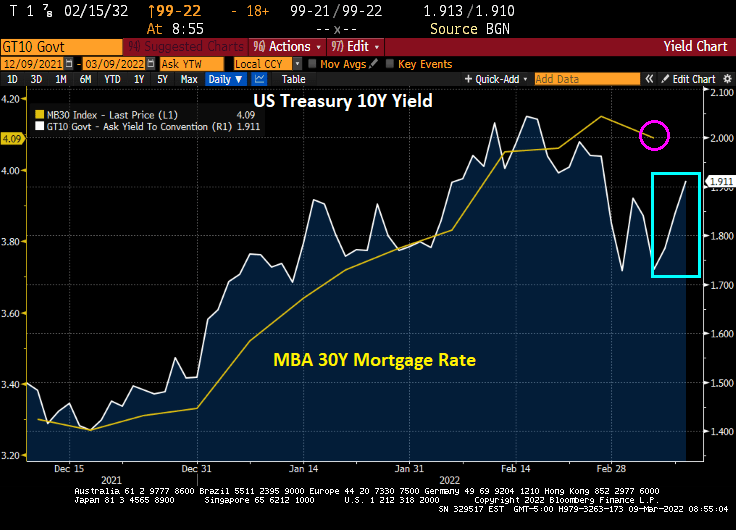

The mayhem caused by the Russian invasion of Ukraine is helping drive down interest rates … for the time being … and this is helping push down mortgage rates and increase mortgage applications.

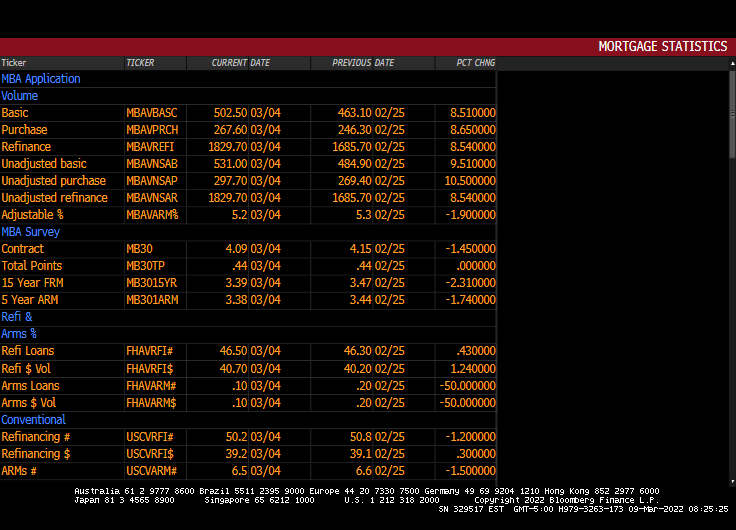

Mortgage applications increased 8.5 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending March 4, 2022.

The seasonally adjusted Purchase Index increased 9 percent from one week earlier. The unadjusted Purchase Index increased 11 percent compared with the previous week and was 7 percent lower than the same week one year ago.

The Refinance Index increased 9 percent from the previous week and was 50 percent lower than the same week one year ago. Diane Olick at CNBC has the hilarious headline “Brief drop in mortgage rates sparks mini refinance boom.” The slight rise in refi applications from the previous week is more of a firecracker going off than a boom given that refi apps are still down 50% from the same week last year.

Bear in mind that the US Treasury 10-year yield is up since the MBA’s reporting week ended on March 4, 2022. So, look for Olick’s mini-refi boom to end as quickly as it started.

Here is the rest of the MBA story.

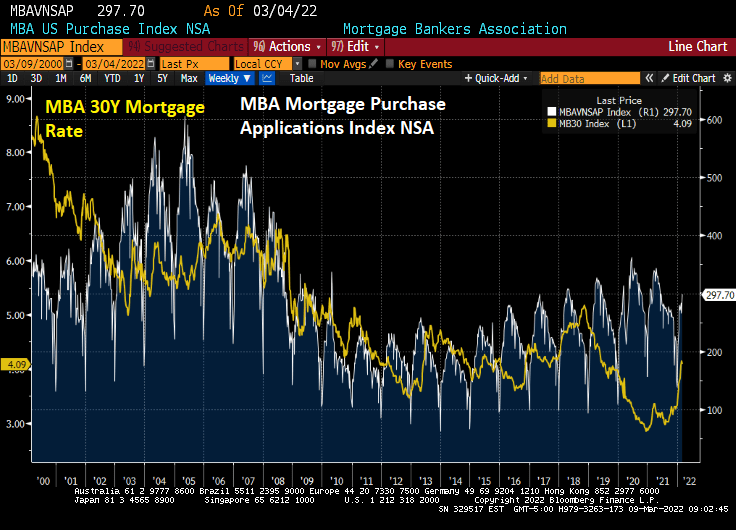

The MBA Mortgage Purchase applications index typically peaks in mid-to-late April, so we still have another month (seasonality) until purchase applications begin declining again.

The US Treasury 10Y-2Y curve continues to flatten and is the worst curve recovery in modern history.

The general rise in US mortgage rates is more closely tied to expectations of Fed rate increases than Fed Agency MBS holdings.

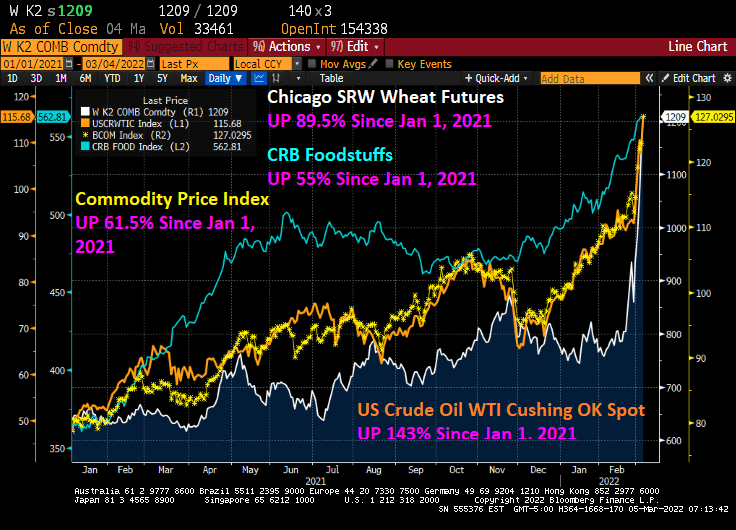

This has been a brutal week for consumers. With the Russia/Ukraine conflict raging and Congress seems determined to not allow for additional oil and gas production, and Biden’s anti-fossil fuel edicts still in place, we are seeing dramatic price increases in wheat (UP 89.5% since January 1, 2021), WTI Crude (UP 143% since January 1, 2021), and food stuffs (UP 55% since January 1, 2021).

Bankrate’s 30-year mortgage rate has actually been falling the last several days, which is good for prospective home buyers as the 10-year US Treasury Note yield has been declining.

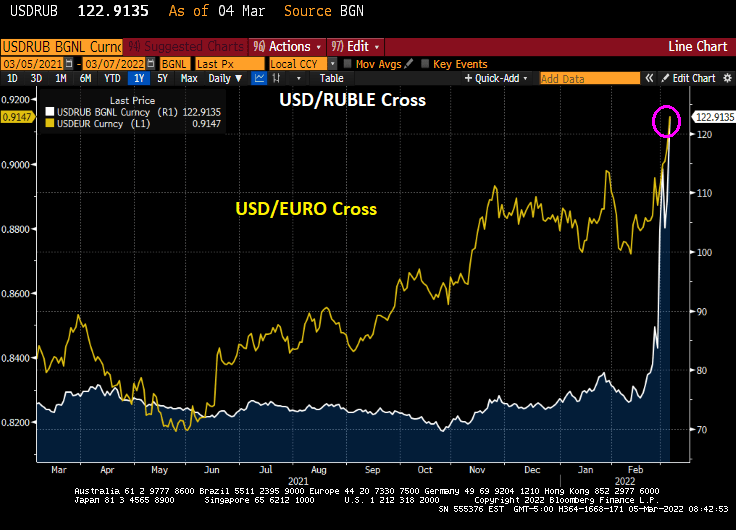

The USD/Russian Ruble cross is skyrocketing and the USD/Euro is doing likewise. Russians visiting the US will find that their trip is suddenly unaffordable (as do many American citizens will its rampant inflation). As Bruce Willis said in “Die Hard,” “Welcome to the party, pal.”

On Friday, the US Treasury 10-year yield declined 11 bps.

And energy prices continue to soar, particularly UK Natural Gas Futures that rose 19.85% overnight.

The US inflation data will be released on March 10th and the consensus is that February CPI inflation will rise to 7.9% YoY.

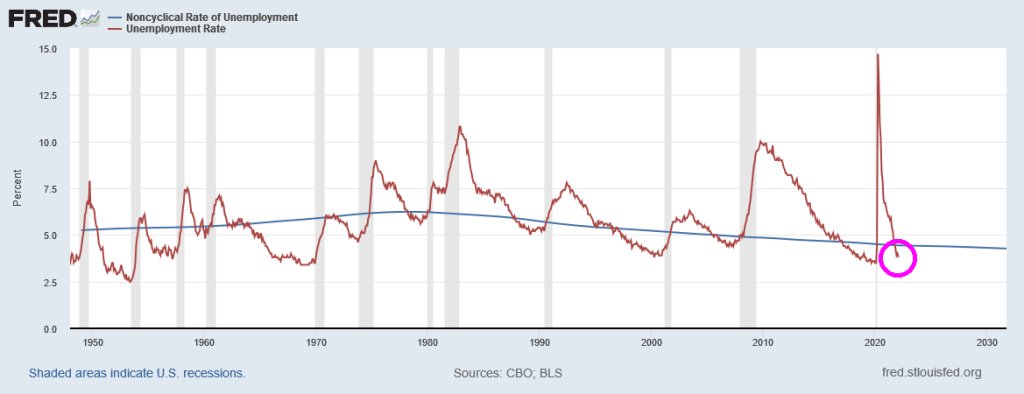

But even the latest unemployment rate report (3.8%) is signalling that The Fed should be raising interest rates since it is lower than the Natural Rate of Unemployment or NAIRU (4.44%).

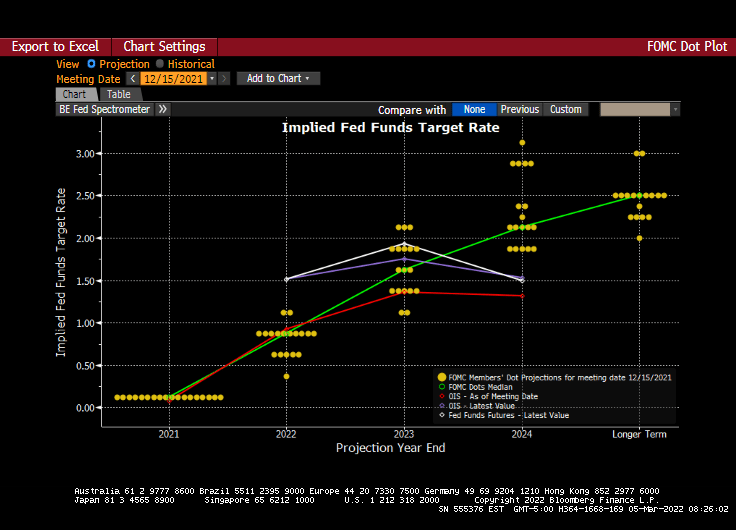

And we have the next Fed policy error on March 16th. The Fed dots plot looks like the glide slope for an aircraft, but the message is that rates will be going up at future meetings.

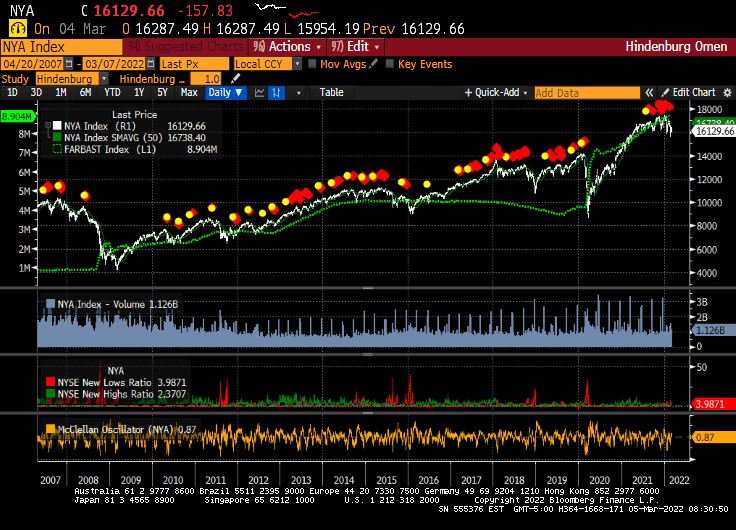

And just for amusement, I present to you the infamous Hindenburg Omen chart that forecast the 2008/2009 stock market correction. Since that correction, the Hindenburg Omen has been flashing “danger” but the only correction was the COVID-linked correction of early 2020. While the Hindenburg Omen is flashing red right now, The Federal Reserve’s balance sheet (green line) has protected against market corrections. Let’s see what happens if and when The Fed decides to remove the epic monetary stimulus.

Its anyone’s guess as to whether The Fed will actually tighten monetary policy.

President Biden is giving his first State of the Union address tonight with rebuttals from Iowa Governor Kim Reynolds and The Squad’s Rashida Talib (yes, a Republican is giving the rebuttal to Biden’s SOTU speech, and a Democrat is rebutting a Democrat President??)

Let’s look at a short list of Biden’s economic triumphs. I will ignore Biden’s catastrophic Afghanistan withdrawal and his weak response to the Russian invasion of Ukraine.

If you want higher oil and gasoline prices, Biden is a tremendous success.

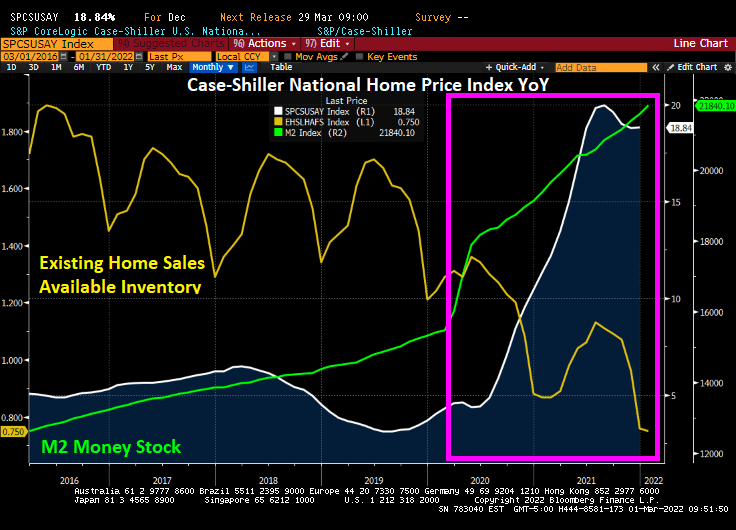

If you like rampant government spending, then Biden is your man. Home price growth is up to 18.84%, making housing unaffordable for millions of American families.

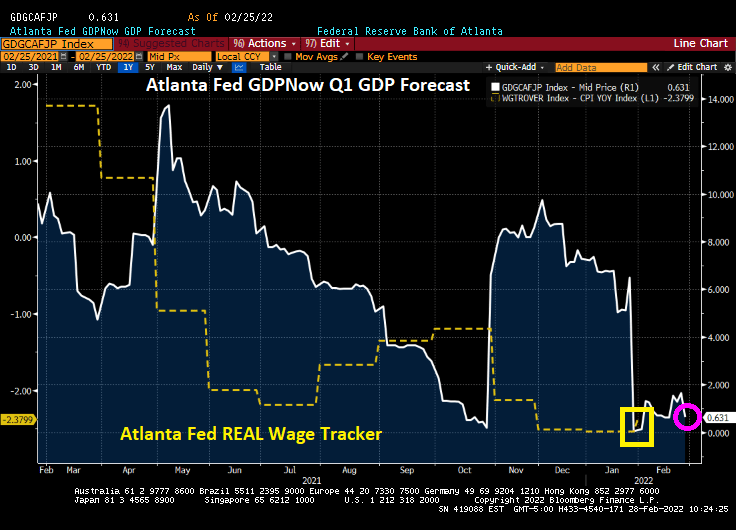

Wages? They are up, but declining after 7.5% YoY inflation. And GDP is almost zero.

Biden can only point to rising average hourly wages, but not REAL average hourly wages.

Inflation? Highest in 40 years, due to excessive Federal spending, The Fed’s crazy printing and Biden’s energy mandates.

I am scratching my head to think of accomplishments for Biden to mention in the SOTU. But I am sure that he will say something positive. Otherwise, Biden’s SOTU speech should be the Billy Preston song “Nothing from Nothing.“

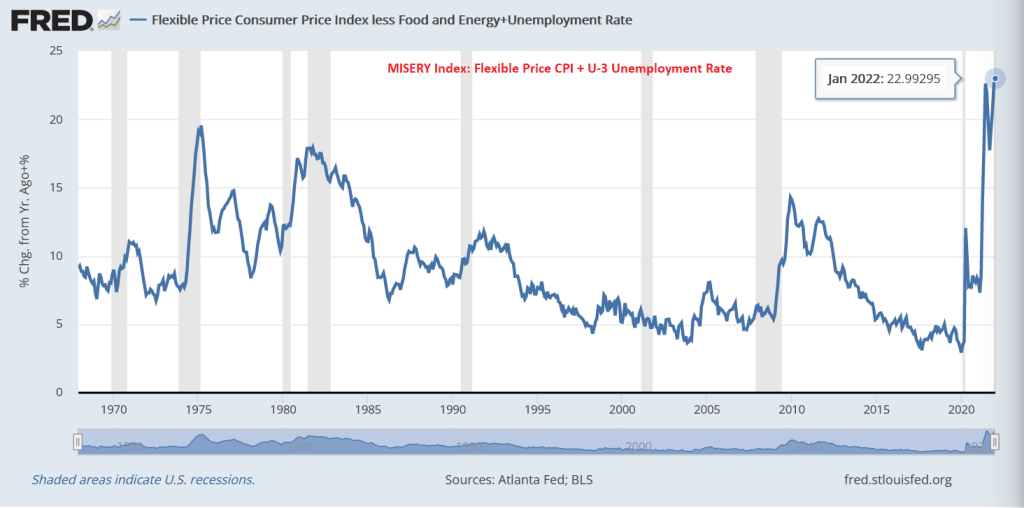

It is truly a miserable time for many Americans as demonstrated by the Misery Index (inflation rate + unemployment rate). But rather than using the CPI YoY measure at 7.5%, I am using the FLEXIBLE CPI YoY to compute the misery index. And is it ever miserable!

In January, the CORE flexible CPI YoY + U-3 unemployment rate hit a modern high at 22.99%. Or at least since 1967.

Like the movie “50 Shades of Gray,” we have 50 shades of inflation. Examples?

How about hardwood? Producer Price Index for hardwood is up 30.8% YoY.

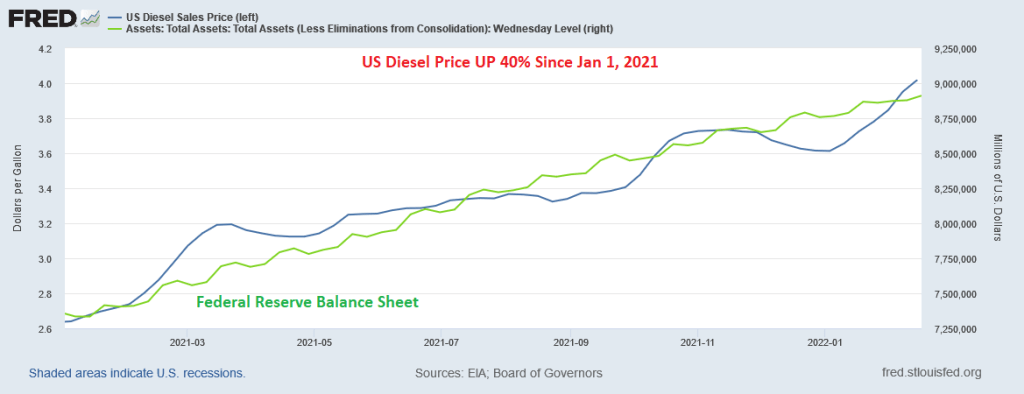

How about diesel fuel prices? They are UP 40% since January 1, 2021.

How about housing? UP 20% YoY according to Zillow’s home value index.

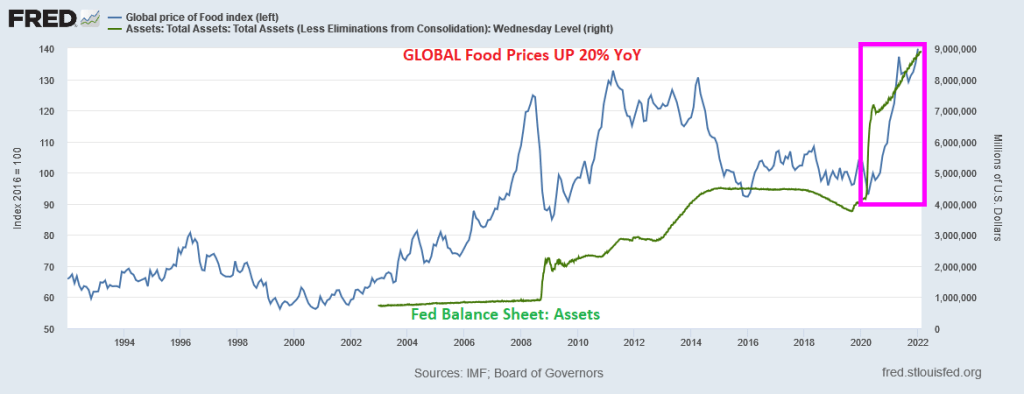

Global food prices? UP 20% YoY.

I could go on and on, but you get the picture. Rising energy, food and construction materials are soaring making many Americans miserable.

But Powell and The Fed have promised to whip inflation. Whip it good … with interest rate increases.

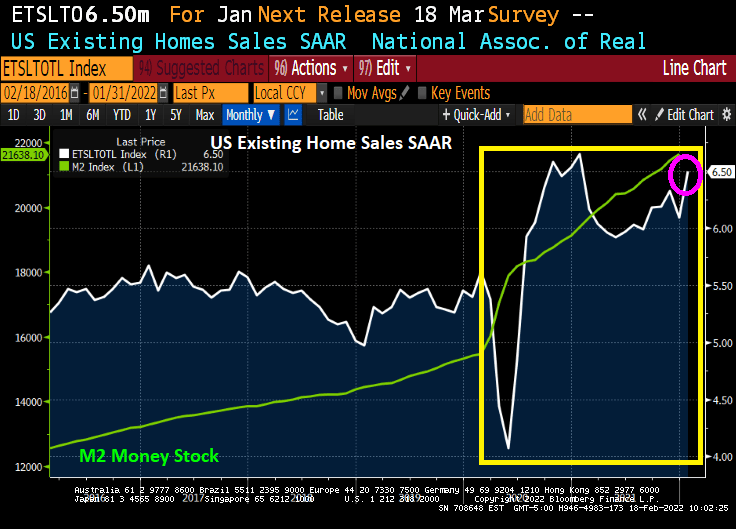

Surprise! US existing home sales in January rose to 6.50 million units SAAR versus the expected 6.10 million units. That is a 6.7% increase over December.

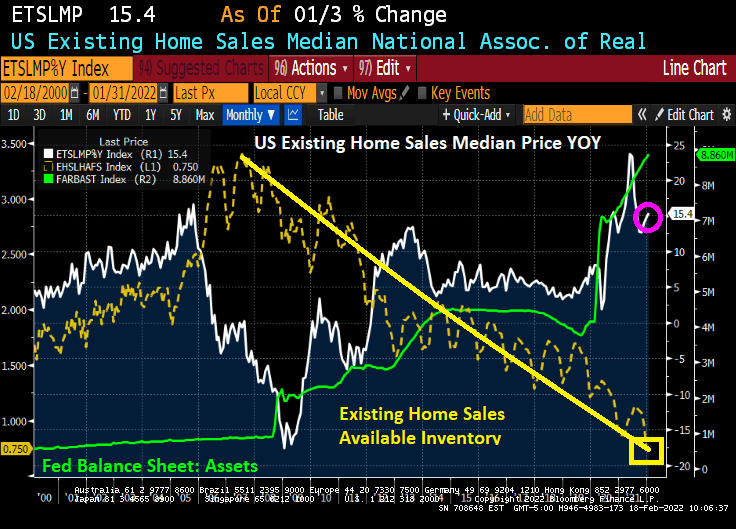

The disturbing news is the continued lack of available inventory that peaked in Q4 2007 and has continued its decline to today … the lowest level of available inventory since 1981. Despite the Fed’s massive stimulus that they allegedly will take away. Median price of existing home sales rose to 15.4% YoY. Making homes affordable should NOT be a slogan for The Federal Reserve, the Biden Administration or Congress.

The massive Federal stimulypto (fiscal and monetary) has helped push existing home sales to 6.50 million units SAAR in January. What will happen after The Fed withdraws it stimulus??

What is surprising is that with declining REAL wage growth, we saw a surge in home buying in January.

Call this a double whammy! Red-hot rents combined with a slowing economy.

According to CoreLogic, single-family annual rent growth finished 2021 at a new record: 11.7% YoY for high tier rental properties and 10.4% YoY for low tier rental properties.

Of course, southern and southwest rental properties are seeing the fastest rent growth. Particularly Miami at 36% YoY. Phoenix is no slouch at 19% growth in rents.

You must be logged in to post a comment.