We are truly living in Strange Days under Joe Biden. And with Elon Musk’s release of Twitter’s suppression of the Hunter Biden laptop scandal, they call Joe Biden the Sleaze.

As The Federal Reserve tries to crush Bidenflation, we are seeing Fed Remittances to the US Treasury soaring (white line). At the same time, we see the Biden Administration draining the Strategic Petroleum Reserve (orange dashed line). And as The Fed tightens, M2 Money growth crashes (green line).

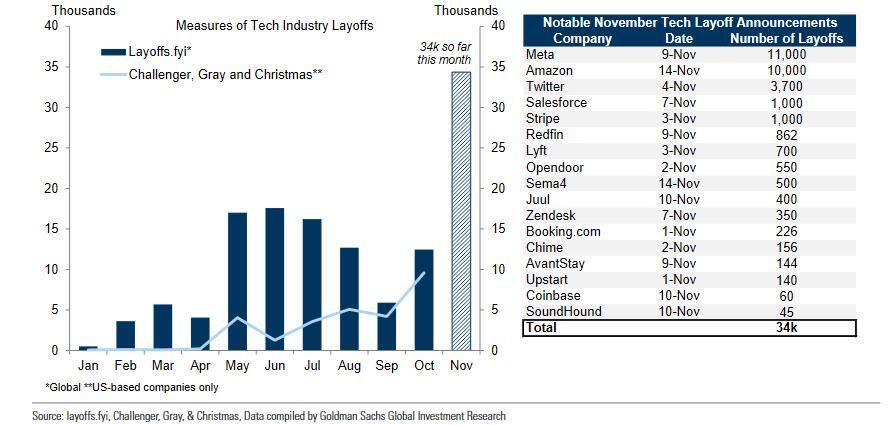

And with tech layoffs, I predict that 2023 job growth will be pretty bad.

As I have discussed before, I am a fan of ADP’s job reports and not a fan of the BLS NFP reports. As M2 Money growth slows, we can see declining ADP jobs added (yellow line), but BLS’s NFP report shows huge spikes.

Lastly, we have Sam Bankman-Fried and FTX. SBF should be in custody for being involved in one of the biggest fraud cases in history, but like Hunter Biden, is roaming free and trying to raise MORE funds. Why are these lapses in justice occuring with “10% for The Big Guy” Biden?

Corruption in Washington DC?

You must be logged in to post a comment.