US pending home sales rose 8.1% in January. At the same time, pending home sales declined -22.4% on a year-over-year (YoY) basis.

So, YoY pending home sales growth has been negative for 19 of the last 20 months.

Confounded Interest – Anthony B. Sanders

Financial Markets And Real Estate

US pending home sales rose 8.1% in January. At the same time, pending home sales declined -22.4% on a year-over-year (YoY) basis.

So, YoY pending home sales growth has been negative for 19 of the last 20 months.

The gap between the VIX Put-call volume and CBOE Put-call ratio is the widest since 2006, the precursor of a major volatility spike.

Meanwhile, for those of you interest in railroad regulatory issues, as a general matter, regulations are rarely ever “reversed,:” but rather modified or replaced with changes. No administration would be able to outright “repeal” a major safety regulation because it almost certainly be immediately enjoined by a court and found to be counter to Congressional delegation.

I assume most of the attention will be on this final rule (https://www.federalregister.gov/documents/2020/10/07/2020-18339/rail-integrity-and-track-safety-standards) published and effective on Oct 7, 2020. It is considered”deregulatory” in the sense that it results in an economic or compliance cost savings, mostly owing to a change in the permissible type of track integrity monitoring, and decrease in the resulting number of “slow orders.”

Unlike Pete Buttigieg who apparently did not read the regulations when he blamed Trump, read the actual published “deregulation.” A faulty railcar axel which was the cause of the East Palestine Ohio trail derailment was NOT impacted by the “deregulation.” Instead of Mayor Pete, he should be called “Cheap Shot Pete.”

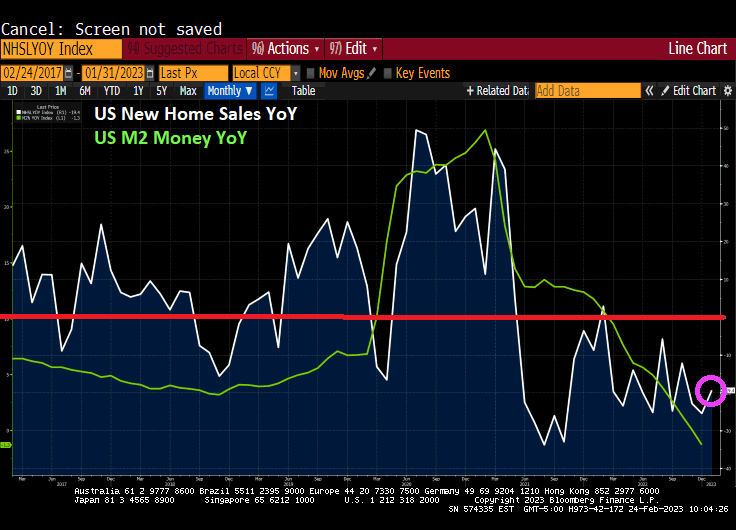

Another sign of a not healthy economy is housing. New Home Sales collapsed -19.4% from January 2022 (aka, year-over-year or YoY).

If I were Joe Biden, I would be touting the month-over-month numbers, up 7.20% from December to January. But the reality is that year-over-year new home sales are down -19.4%.

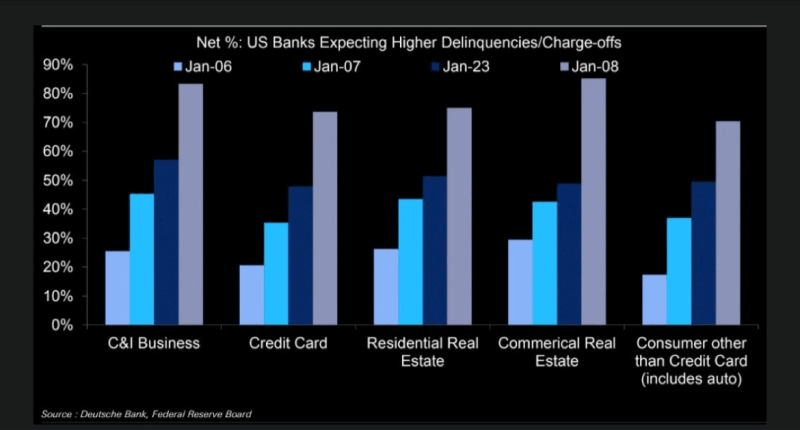

Also, on the “Alarm!” front, US banks are expecting higher delinquencies, including on residential mortgages.

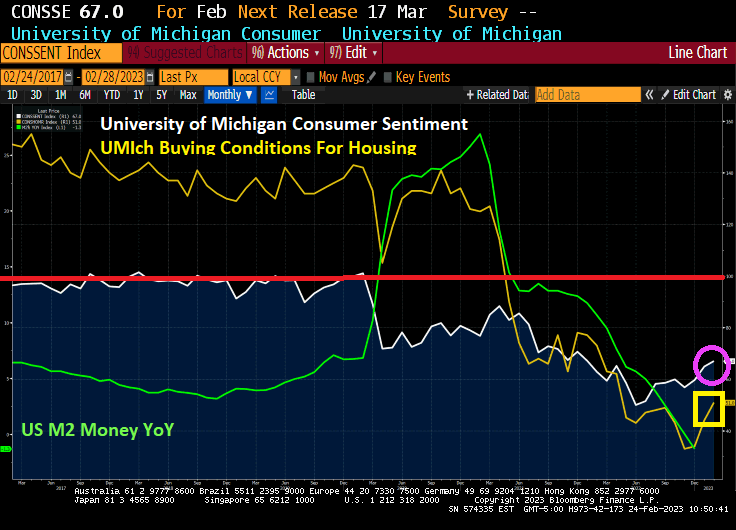

University of Michgan consumer sentiment for housing is rising, but still woefully below the 100 benchmark.

Not really a surprise, but January’s personal spending numbers came in hot at 1.8% MoM. Also, Personal Consumption Expenditures PRICE index (aka, inflation) rose to 5.4% YoY.

Here comes The Fed! The 2-year Treasury yield rose 10 basis points this morning.

Pelsoi and Schumer (with McConnell) got the gold mine and American consumers got the shaft.

The US economy has a case of the summertime blues.

Bull steepenings in the yield curve are generally seen as a precursor to a recession, but they are often preceded by bear steepenings. The 3m30y curve is currently bear steepening, indicating a recession could begin as early as the summer. In fact, the 3m30y curve is now inverted at -94.628 basis points pointing to a recession in summer 2023.

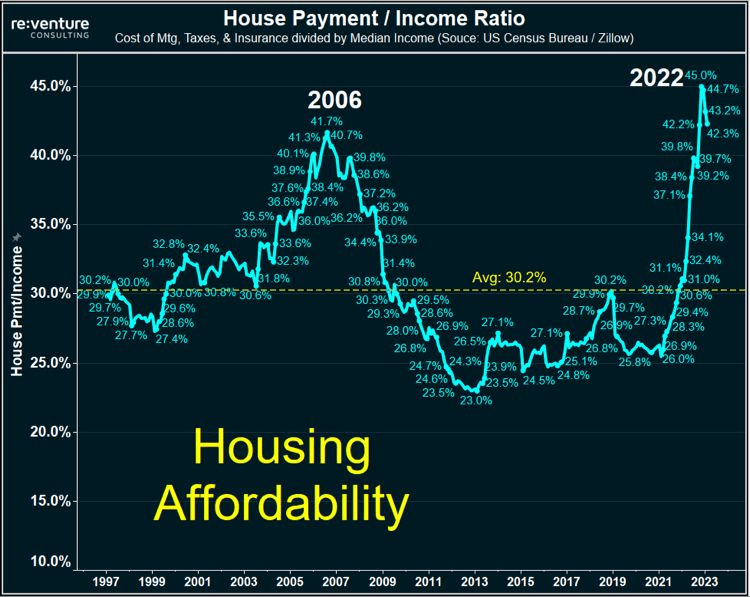

This is happening as the US house payment to income ratio near all-time highs.

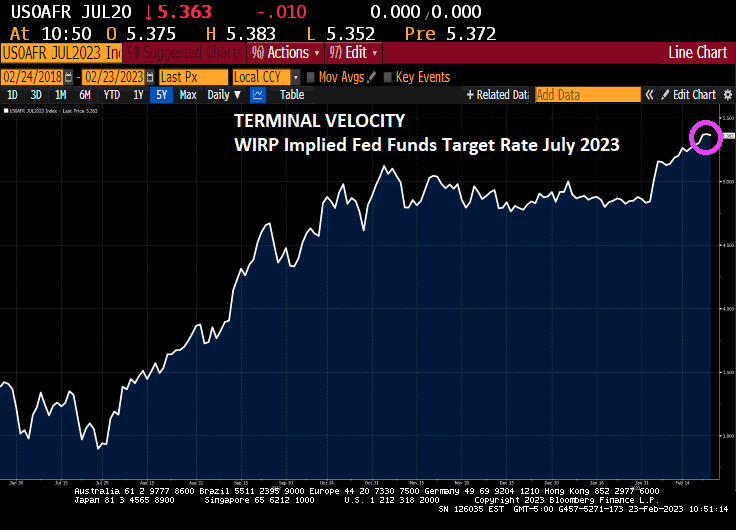

Yesterday, we saw The Federal Reserve release the minutes of the last meeting. In a nutshell, The Fed is going to keep raising rates.

The terminal Fed Funds target rates is now 5.363% for the July FOMC (Fed Open Market Committee) meeting in 2023.

This comes as US Q4 GDP was revised lower on weaker consumer spending, revised downward to 1.4%

With the revision of Personal Consumption, real GDP was revised downward to 2.7% annualized QoQ.

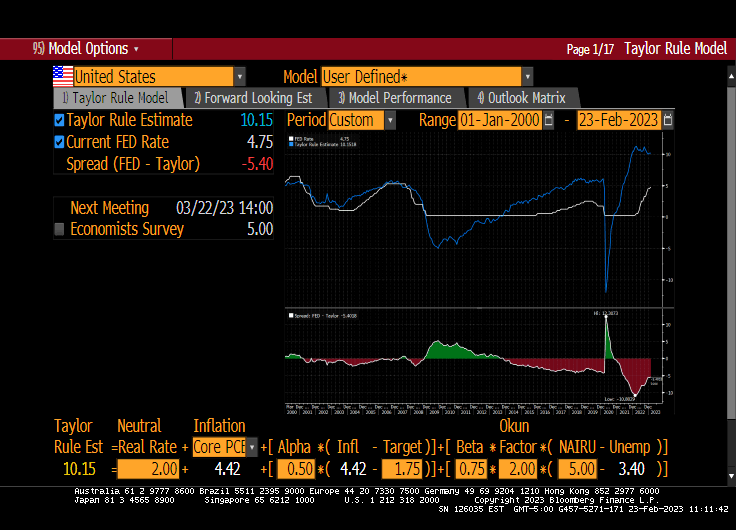

The Taylor Rule estimate for The Fed Funds Target rate is 10.15%. The Fed is only at 4.75%, so there is a long way to go! Except that The Fed doesn’t follow any useful rule like the Taylor Rule. Just the “seat of the pants” rule.

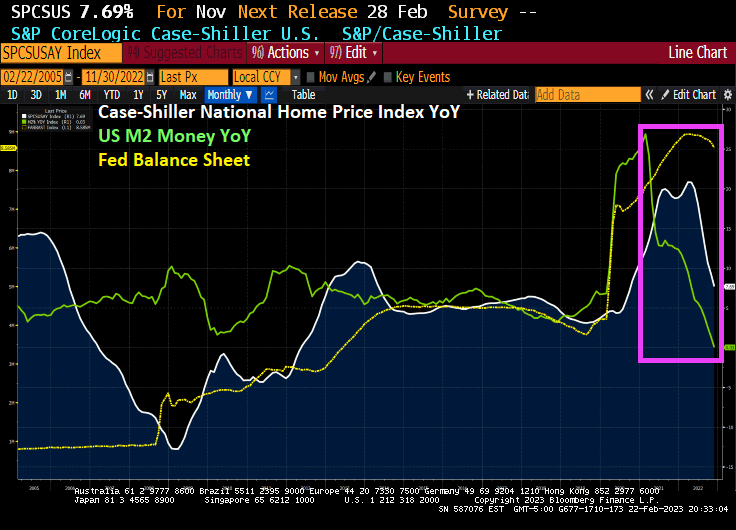

The value of the US housing market shrunk by the most since the 2008 as the pandemic boom (and M2 Money growth) fizzled out.

After peaking at $47.7 trillion in June, the total value of US homes declined by $2.3 trillion, or 4.9%, in the second half of 2022, according to real estate brokerage Redfin. That’s the largest drop in percentage terms since the 2008 housing crisis, when home values slumped by 5.8% from June to December.

Homebuyers, already facing record-high prices, took an additional hit from mortgage rates that more than doubled last year. With less competition in the market, the median US home sale price was $383,249 last month, down from a peak of $433,133 in May.

To be sure, home prices are not collapsing. In December, the total value of US houses was still 6.5% higher than it was a year earlier.

How much homeowners lost depends on where they bought. The biggest declines were in pricey cities like San Francisco and New York, while buyers who moved to pandemic boomtowns are still seeing the returns on their investment, particularly in Florida.

That was especially true in Miami, where the total value of homes ballooned 20% year-over-year to $468.5 billion in December, the largest annual percentage increase among the top metro areas. While the overall US housing market is down, Miami’s market has about the same value as when it peaked at $472 billion in July. Meanwhile, homeowners in North Port-Sarasota, Florida, Knoxville, Tennessee, and Charleston, South Carolina, all saw annual gains above 17% in 2022.

The thrill is gone from housing as The Fed tightens away.

Well, January’s existing home sales numbers were horrific. Down -37% year-over-year (YoY) and down -0.7% MoM.

The median price of existing home sales fell to 0.67% YoY.

I am now posting my Podcasts on Spotify.

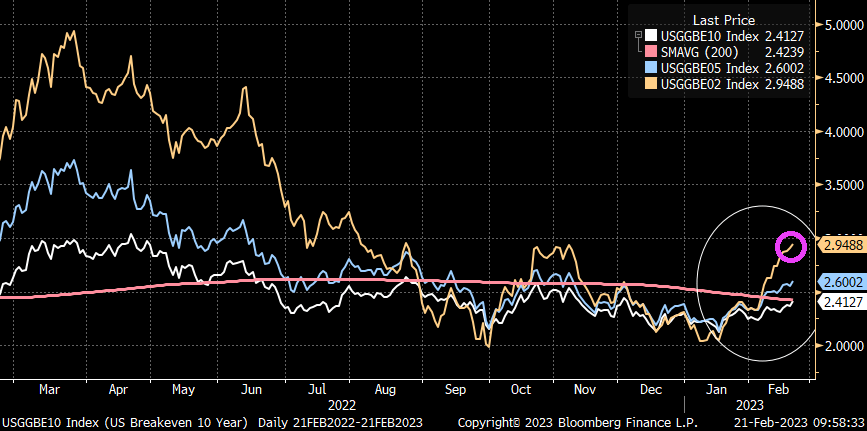

But before I go for experimental therapy for my brain tumor, I will leave you with this diddy. Inflation expectations are on the rise, not falling like Biden and Yellen keep screaming.

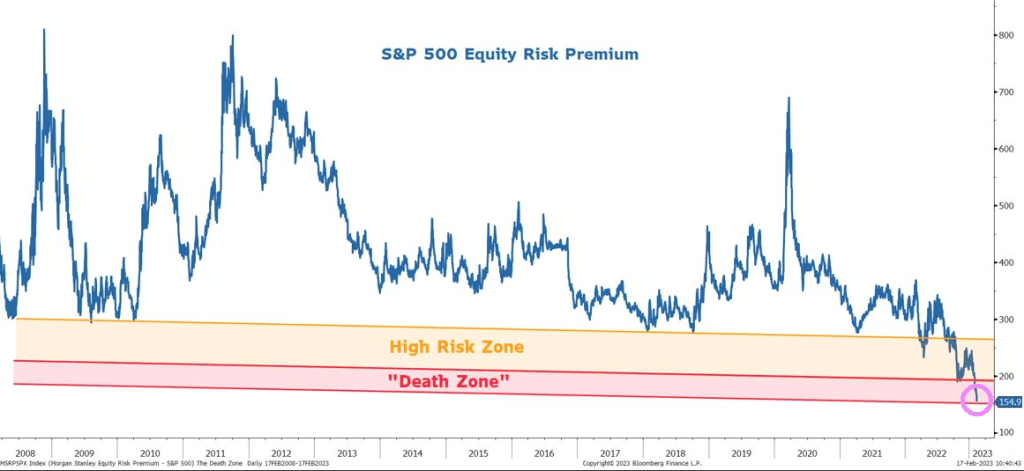

As the economy weakens and The Federal Reserve tightens (to fight inflation), we are seeing the lowest level of S&P 500 equity risk premiums since before the financial crisis.

Way to go, Mayor Pete amd Dementia Joe!

The US economy, despite the tight labor market, has been shot through the heart by Biden’s economic policies. The Biden Administration (aka, Obama’s third term as President) is giving government a bad name.

On the corporate side, US bankruptcies in 2023 had the worst start to a year since 2010 and the financial crisis.

On the personal finance side of the ledger, the delinqueny rate on credit cards is growing at the faster rate since 2010.

Throw in 22 straight months of negative REAL wage growth, and have a scary situation facing middle America.

And the shate of outstanding subprime auto debt (30 days or more delinquent) is up to the highest rate since … well, you know when. The financial crisis of 2009-2010.

The US middle class is living on a prayer, because Washington DC doesn’t care.

But don’t worry. Mayor Pete, the EPA and Ohio governor Mike DeWine claim the air is good to breath and the water safe to drink in East Palestine Ohio.

Why isn’t Greta Thunberg racing to Ohio to protest the dumping of toxic chemicals?

You must be logged in to post a comment.