Why is this terrifying? Blockchain technology is a fantastic innovation for processing payments given its ledger capabiliities. But that means that The Federal Reserve might be able to look at your complete history of expenditures. Or worse, perhaps even shut down your ability to make payments, This may lead to a China-style “social credit score” where the Fed and the Federal government punish people for driving “too much” increasing your carbon footprint or eating non-Federal government approved foods and lowering your social credit score.

Will there be safeguards? Allegedly, but remember the FBI hid Hunter Biden’s laptop prior to the Presidential election of late 2020. And HOW did our nation’s regulators completely drop the ball on Sam Bankman-Fried (or Spam Bankfraud)?

With an impending railroad strike that can torpedo the US economy (but if that is possible, why is the Biden Clan vacationing in Nantucket for Thanksgiving weekend when Joe should be talking with railroads and the unions to not let this happen?), let’s see what interest rates are telling us.

First, the US Treasury 10Y-2Y yield curve continues to descrend into the abyss (now at -80 basis points).

Second, the latest Fed Dot Plot (from September, new one will be issued during December) show that The Fed thinks that their target rate, while rising in 2023, will likely start falling again in 2024.

Third, since it is Thanksgiving Day, US bond markets are closed. But in Europe, the 10-year sovereign yields are falling, a sign that the ECB is reversing course by increasing monetary stimulus and/or a European are slow down.

Fourth, US mortgage rates have cooled since peaking (locally) at 7.35% on November 3, 2022 and now sit at 6.81%, a decline of 54 basis points. A clear sign of cooling.

Fifth, how about Fed Funds Futures data? It is pointing to a peak Fed Funds Target rate of 4.593% at the June FOMC meeting. Then a decline in rates to 2.301% by January 2024.

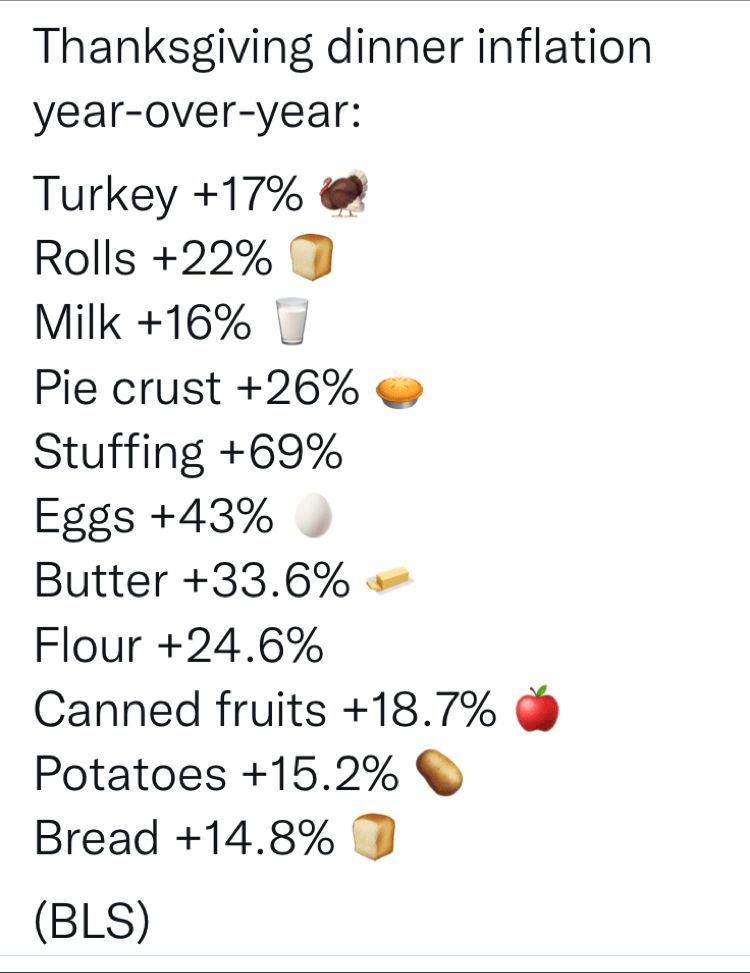

Now, go and enjoy your Thanksgiving dinner with friends and family (up 20% since last year), courtesy of Jerome Powell, Joe Biden, Nancy Pelosi and Chuck Schumer.

Not surprisingly, the median price of new home sales are up 8.2% MoM (since September).

The Fed’s minutes for their last FOMC meeting will be out at 2pm EST. Let’s see if they discuss WHY they haven’t reduced their balance sheet by much which is contributing to asset bubbles.

Here is The Fed’s Dots plot from the September meeting. I get the impression that The Fed thinks that their target rate will be coming down in 2024 and after.

The global economic slowdown has one nice unintended consequence: as the 10-year Treasury yield softens, mortgage rates decline.

US mortgage rates retreated sharply for a second week, hitting a two-month low and providing a bit of traction for the beleaguered housing market.

The contract rate on a 30-year fixed mortgage decreased 23 basis points to 6.67% in the week ended Nov. 18, according to Mortgage Bankers Association data released Wednesday.

Rates have plunged nearly a half percentage point in the past two weeks, the most since 2008, as recession concerns mount, inflation shows signs of cooling and a number of Federal Reserve officials say it may soon be appropriate to slow the pace of monetary tightening.

The slide in borrowing costs helped stir demand as the group’s index of applications to buy a home climbed 2.8%. That marked the third-straight increase since the gauge stumbled to the weakest level since 2015.

The pickup in demand allowed the overall measure of mortgage applications, which includes refinancing, to rise for a second week, but it still remains depressed. The index of refinancing activity edged up from a 22-year low.

The Refinance Index increased 2 percent from the previous week and was 86 percent lower than the same week one year ago.The unadjusted Purchase Index increased 9 percent compared with the previous week and was 41 percent lower than the same week one year ago.

But you need an electron microscope to see the increase in both purchase and refi apps.

One indicator of a slowing global economy is the decline of FANG (Facebook, Amazon, Netflix, Google) with declining liquidity.

The US economy is in “The Deep.” Deep into yield curve inversion, that is.

The US Treasury 10Y-2Y yield curve swam deeper into inversion at -75 basis points. The deepest inversion since just before The Great Recession and housing market crash.

The Biden Administration is setting all sorts of records. One is the worst inflation rate in 40 years. Another is highest gasoline prices in history (until the latest global slowdown). The list goes on, but here is another one: the US Treasury 10Y-2Y yield curve is now at -72.5 basis points, the more inverted curve since 1981.

This is the US Treasury version of 50 Shades Of Grey.

As Americans prepare to hit the road for Thanksgiving, average gas prices will be at their highest seasonal level ever, according to GasBuddy.

GasBuddy says the national average is projected to stand at $3.68 on Thanksgiving Day. This is nearly 30¢ higher than last year, and over 20¢ higher than the previous record of $3.44 set in 2012.

And diesel prices, the life blood of the shipping industry, relative to gasoline prices, are soaring. Highest since 2004.

As we approach Thanksgiving Day, it is important to be thankful … that things aren’t even worse under Billions Biden. US CRB foodstuffs are up 49% under Biden while diesel fuel is up 102%.

Now, gasoline prices fell recently as WTI crude prices slipped on slowing demand. And as stimulus wears out.

And its now only food.

Have a holly jolly Thanksgiving!!

My Thanksgiving dinner, because of the cost, will be a Jersey Mike’s turkey and provolone sub (mini). Or this canned dinner.

The chaos created by Sam Bankman-Fried (FTX Crypto Exchange) and Alameda Research (SBF’s hedge fund) will go down in history as one of the biggest scams. And should earn a top spot on Phil Hall’s 100 Years Of Wall Street Crooks.

Sam Bankman-Fried’s bankrupt crypto empire owes its 50 biggest unsecured creditors a total of $3.1 billion, new court papers show, with a pair of customers owed more than $200 million each.

FTX-linked entities owe their single biggest unsecured creditor more than $226 million, according to a redacted list of top 50 creditors filed late Saturday. All of them were listed as customers and ten have claims of more than $100 million each, the filings show.

The creditors, whose names and locations weren’t disclosed, are among the vast array of people and institutions caught up in FTX’s insolvency. The 50 largest claims are all from customers owed $21 million or more.

In the US, bankrupt companies are required to disclose information about their debts as part of insolvency proceedings. Creditors will get to weigh in on the best way for FTX to repay its debts as the bankruptcy unfolds.

FTX said it has assets and liabilities of at least $10 billion each in preliminary court papers. The case may involve more than one million creditors, according to lawyers for FTX.

The case is FTX Trading Ltd., 22-11068, U.S. Bankruptcy Court for the District of Delaware.

On top of that, SBF is attempting to raise MORE money. The question is … who would be dumb enough to listen to SBF?

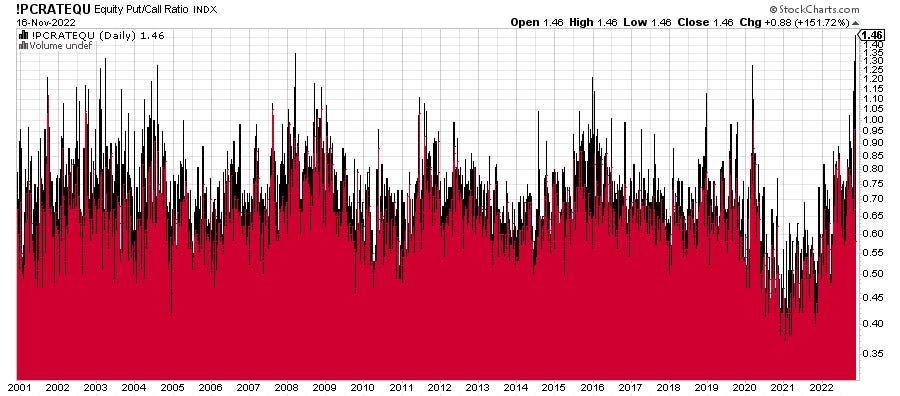

Crytpo continue to fall as investor confidence in crytpo has waned since SBF’s fraud was exposed. (In SBF’s defense, I am sure that current House Financial Services committee Chair Maxine Waters will declare he is a victim of changing market conditions, not historically massive fraud and political influence pedaling).

Didn’t SBF or his Alameda Research girlfriend Caroline Ellison look at Bitcoin as inflation roared under Biden and Fed started to remove its epic monetary stimulus? Or did any of the investors or their representatives bother to look at the books of FTX or Alameda Research??

I have the sneaking suspicion that Caroline Ellison or some other little fish will take the fall for SBF’s fraud. SBF has bought-off too many politicians.

The US housing market is slowing, to be sure. Yesterday’s existing home sales (EHS) report revealed that US EHS were down -28.43% YoY and the median price of EHS slowed to 6.6% YoY.

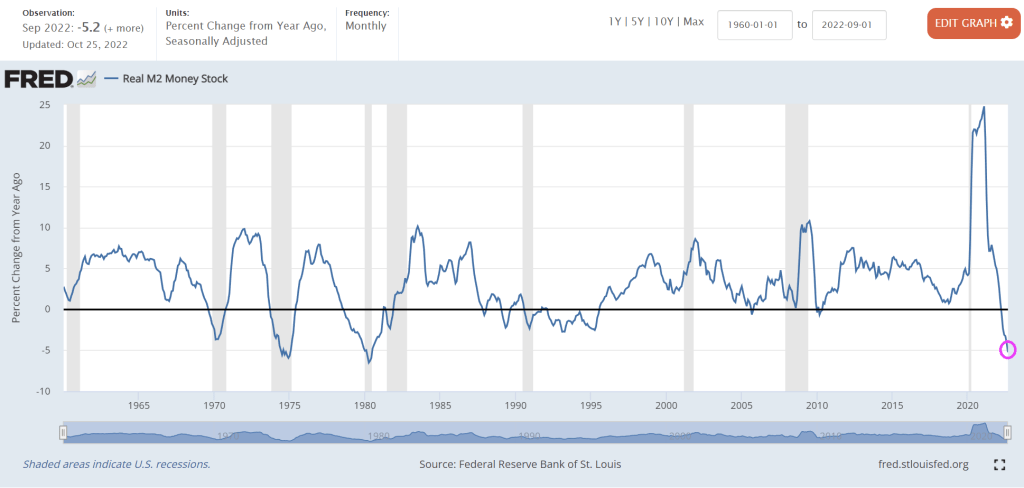

But that is just the surface of the EHS report for October. Once I removed inflation (CPI YoY) from the numbers, we are left with REAL median price of EHS growth of -1.17% and REAL average hourly earnings YoY of -3.0% YoY. The REAL 30-year mortgage rate is -5.25%. That reveals how horrible inflation is in the US.

It is important to note that EHS numbers are lower in October than they were before Covid stimulypto (my name for the massive spending spree by Congress and massive injection of monetary stimulus by The Fed. Even the REAL 30-year mortgage rate is negative at -0.5254%.

You must be logged in to post a comment.