There was a hilarious film with Hillary Swank and Aaron Ekhart called “The Core” where earth’s core stops spinning and the earth gets cooked by the Sun’s rediation. Now we learn that the Earth’s inne core has actually stop spinning. This time, however, all that has happened is that Joe Biden is President which is almost as bad,

But also related to “The Core” is that the important Personal Consumption Expenditures (PCE) are out for December along with PCE price deflator numbers. In short, personal income was up 0.2% month-over-month (MoM) in December while personal spending was down -0.2%. REAL personal spending was down -0.3% MoM.

But the all important PCE deflators numbers were down all well. The REAL PCE price index (or deflator) was down to 5.0% YoY in Decmember while REAL CORE price index was down to 4.40%. All this is happening as M2 Money growth has stop spinning (down to -1.3% YoY in December).

Based on a CORE PCE YoY of 4.40%, the Taylor Rules suggest that The Fed Fund Target rate should be … 10%. However, the current Fed Funds Target rate is only 4.50%, so The Fed is not even half way there.

Fed Funds Futures are pointing to a peak rate of 4.90% by the June ’23 FOMC meeting, then a pivot (despite denials from Fed talking heads).

Of course, The Fed doesn’t follow the Taylor Rule or any other transparent rule for rate management. Rather, Fed Chair Powell like former Chair (and current Treasury Secretary Janet Yellen) follow a more seat-of-the-pants approach.

Today’s GDP report from the BEA reminds me of the Peggy Lee song “Is That All There Is?” Between the massive Fed monetary stimulus since late 2008 (and particularly since Covid in 2020) and all the Federal spending (Covid relief, Inflation reduction, Omnipork spending bill, etc.), US real GDP rose by only 2.9% in Q4 from Q3.

But signs of slowing underlying demand mounted as the steepest interest-rate hikes in decades threaten growth this year.

Gross domestic product increased at a 2.9% annualized rate in final three months of 2022 after a 3.2% gain in the third quarter, the Commerce Department’s initial estimate showed Thursday.

Personal consumption, the biggest part of the economy, climbed at a below-forecast 2.1% pace (forecast was for 2.9%). Again,

The report also showed some signs of stress for American consumers whose wages have failed to keep up with inflation and continued to encourage them to draw down savings accumulated from government pandemic-relief programs. The burden of elevated prices and higher borrowing costs is mounting, pointing to a tenuous outlook for the economy.

A key gauge of underlying demand that strips out the trade and inventories components — inflation-adjusted final sales to domestic purchasers — rose an annualized 0.8% in the fourth quarter after a 1.5% gain.

Core PCE growth grew at 3.9%, but is slowing already as M2 Money growth dies.

Stock-index futures and Treasury yields remained higher and the dollar was little changed after the GDP report and better-than-expected weekly jobless claims. Applications for unemployment insurance dropped to 186,000 last week, the lowest since April.

Recent data show cracks are developing more broadly. Retail and motor vehicle sales data showed households are starting to retrench, the housing market continues to weaken and some businesses are reconsidering capital spending plans.

As the Federal Reserve continues to hike interest rates to ensure inflation is extinguished, housing and manufacturing have deteriorated quickly while industries including banking and technology are carrying out mass layoffs.

The GDP report showed the personal consumption expenditures price index, a key inflation metric for the Fed, rose at an annualized 3.2% rate in the fourth quarter, down from a 4.3% pace in the prior three months. The core index that excludes food and energy climbed at a 3.9% rate compared with 4.7% paces in the prior two quarters. Monthly data for December will be released Friday.

The moderation in price pressures is consistent with forecasts that the Fed will further scale back its tightening campaign next week, when it’s expected to raise rates by 25 basis points. Policymakers boosted the benchmark rate by 50 points in December after 75 basis-point hikes at their previous four meetings.

The world’s largest economy expanded 2.1% last year. In 2021, when demand snapped back from pandemic-related shutdowns, the economy grew 5.9% — the best performance since 1984.

The GDP data showed services spending increased at 2.6% annualized rate in the October-December period, the slowest since last year’s first quarter. Outlays on goods rose at a 1.1% pace, the first advance since 2021.

Business investment slowed sharply after a third-quarter surge. Spending on equipment declined an annualized 3.7%, the most since the second quarter of 2020. Outlays for structures rose at a 0.4% pace.

Let’s hope the BEA isn’t padding the numbers like the BLS was caught doing in the first half of 2022.

Lastly, US Real GDP growth YoY FELL to only 0.95925% as M2 Money growth disappears.

While the children in Congress and the Administration argue about cutting the Fedcral budget (as if there isn’t trillions of dollars of wasteful spending in the budget), we saw an even dumber suggestion from Pramila Jayapal (WA-D), Adam (Shifty) Schiff (CA-D) and Sheila Jackson Lee (TX-D): a bill to eliminate the debt ceiling altogether to allow unlimited Federal spending. That reminds me of the Tom Arnold/Julie Ford film “The Stupids.” Yet these clowns keep getting re-elected.

In any case, The Federal Reserve’s quantitative-tightening program risks being propelled toward an early end as US politicians bicker in Washington over raising the national debt limit, according to some economists and bond-market participants. As of this morning, the US credit default swap (1-year CDS) remains elevated signaling a positive probability of a US debt default. (CDS represents the price of insuring against a default).

But notice that The Fed still has $8.5 TRILLION in assets (largely Treasuries and Agency MBS) on their balance sheet. But The Fed’s plans to continue shrinking their balance sheet will be put on hold (and if fact will be reversed) if Democrats and President (10% for the big guy) Biden don’t budget on cutting some of the enormous fat from the Federal budget.

The Conference Board’s Leading Indicator should be called The Bleeding Indicator given that the leading index has declined to 10 straight months. This is happening as The Fed tightens monetary policy to combat inflation.

Leading indicators include economic variables that tend to move before changes in the overall economy. These indicators give a sense of the future state of an economy.

The first headline I saw when I turned on Bloomberg.com was “DOJ Officials Find More Classified Documents at President Biden’s Home.” This is an improvement! So far, the task has been handled by Biden’s private attorneys who don’t have proper security clearance; at least the Justice Department is finally getting involved!

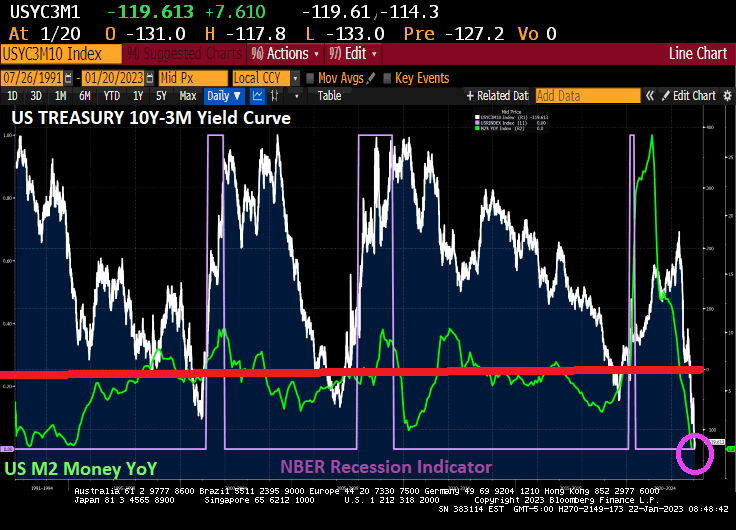

But back to the US yield curve. It is now the most inverted in 30+ years as M2 Money growth stalls. Inverted yield curves have preceded recessions in the past.

But as China reopens and Europe is experiencing a warmer winter than expected (meaning that Europe has sufficient natural gas reserves) and US inflation cooling,

we are seeing market-implied odds of a recession falling in January.

I am still betting on a recession in the second half of 2023.

First, US default risk as measured by credit default swaps remains elevated (primarily because Biden and Democrats refused to cut wasteful spending or reign in non-retirees on Social Security). And NY Fed’s Reverse Repos remain elevated.

And then we have Citi’s economic surprise index for the US at -17 as The Fed slows money growth to 0%.

I wish I knew a place where inflation and insane Federal government spending and policies doesn’t exist.

The Thrill Is Gone from the US housing market as M2 Money growth fells to 0%.

US Existing Home Sales fell -1.5% from November to December (MoM) to 4.02 SAAR units sold. That translates to a depressing -34% decline since December 2021 (YoY).

On the positive side, these numbers are better than expected (-3.4% MoM expected). Still, these numbers are pretty dismal.

Existing home sales MEDIAN PRICE fell to $366.9k as M2 Money growth vanishes. And inventory of existing homes for sale remains lower than pre-Covid levels.

Let’s see what Powell and the Gang (aka, The Federal Reserve Board of Governors) does with interest rates going forward.

Today, the 10-year Treasury yield is up 7.1 basis points, but the real action is in Europe where sovereign yields are up 11.5 bps in France, 9.8 bps in Germany and 18.6 bps in Italy.

Notice that the debt ceiling keeps on climbing once the Kabuki Theater of Democrats and Republicans is over.

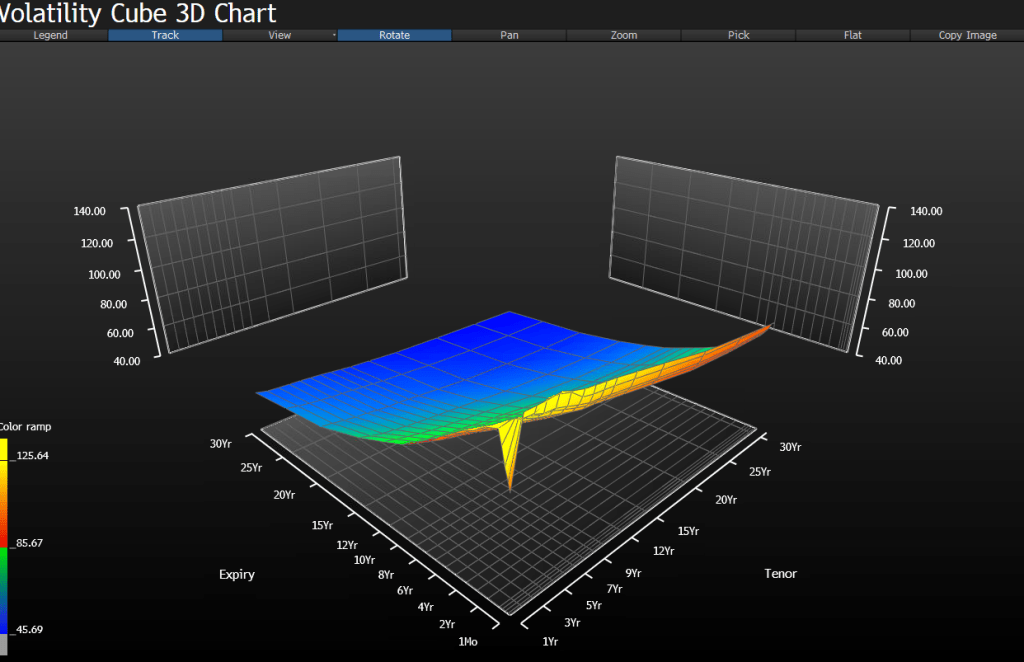

The Volatility Cube for the US CDS 1 year signals that it will all be over soon.

So, Yellen and Treasury are threatening us with taking away Social Security and Medicare if we don’t agree with their lavish Pelosi-like spending sprees and debt.

And why exactly is Janet Yellen flying to China? I admit Washington DC has lousy Chinese food, but at least I hope Yellen takes Hunter Biden with her to negotiate the impending US default and debt workout.

I watched Biden’s Press Secretary Karine Jean Pierre giving Biden credit for the lowest unemployment rate in US history thanks to his economic policies. And Biden mentioned that he inherited a terrible economy from Trump.

Hmmm.

Let’s let the data talk.

Covid was horrific (I almost died from it), but it was the government response to Covid there was disastorous. Government shutdowns (and the masking of the populace) killed off numerous small businesses and sent jobless claims soaring in 2020 (white line) and U-3 unemployment rate rose to the highest level since The Great Depression.

The response from The Federal Reserve was a massive printing of money (green line). And after governments stopped their economic shutdowns (coupled with massive money printing), we saw jobless claims and unemployment shrink rapidly BEFORE Biden took office as President.

The 1981 recession begat an epic borrowing of money by The Federal government (under House Speaker Tio O’Neill D-MA) and we saw another explosion in Federal debt under House Speaker Nancy Pelosi D-CA TWICE, once in 2009 following the financial meltdown and again in 2020 following the Covid economic lockdowns.

So does Trump get any thanks for the rapidly improving labor market before his ouster by Biden? Of course not. But who gets the blame for the staggering growth in Federal debt? House Speaker Nancy Pelosi.

The US did get positive wage growth under Biden, but due to inflation, American workers have experienced 21 straight months of NEGATIVE wage growth.

While Trump tried deregulation to free-up the US economy, Biden has consistently used regulation as a weapon of obidience. His slavish obidience to activist groups on the environment, which is a shame since temperatures have actually been coming down since 2016.

When you look at the data, Trump actually set in motion the jobs recovery, not Biden. Other than helping to create inflation, I can’t think of one positive thing Biden has done for the economy.

On an unrelated note, why is US FBI Director Chris Wray at the World Economic Forum in Davos Switzerland when there is a top secret document fiasco going on in DC and Delaware?

You must be logged in to post a comment.