Yes, The US Treasury 10Y-2Y yield curve remains inverted, for the 104th straight day. And Bankrate’s 30-year mortgage rate has dropped -57 basis points since November 3, 2022.

This comes after a gruesome Pending Home Sales and mortgage applications reports today.

Not surprisingly, the median price of new home sales are up 8.2% MoM (since September).

The Fed’s minutes for their last FOMC meeting will be out at 2pm EST. Let’s see if they discuss WHY they haven’t reduced their balance sheet by much which is contributing to asset bubbles.

Here is The Fed’s Dots plot from the September meeting. I get the impression that The Fed thinks that their target rate will be coming down in 2024 and after.

The global economic slowdown has one nice unintended consequence: as the 10-year Treasury yield softens, mortgage rates decline.

US mortgage rates retreated sharply for a second week, hitting a two-month low and providing a bit of traction for the beleaguered housing market.

The contract rate on a 30-year fixed mortgage decreased 23 basis points to 6.67% in the week ended Nov. 18, according to Mortgage Bankers Association data released Wednesday.

Rates have plunged nearly a half percentage point in the past two weeks, the most since 2008, as recession concerns mount, inflation shows signs of cooling and a number of Federal Reserve officials say it may soon be appropriate to slow the pace of monetary tightening.

The slide in borrowing costs helped stir demand as the group’s index of applications to buy a home climbed 2.8%. That marked the third-straight increase since the gauge stumbled to the weakest level since 2015.

The pickup in demand allowed the overall measure of mortgage applications, which includes refinancing, to rise for a second week, but it still remains depressed. The index of refinancing activity edged up from a 22-year low.

The Refinance Index increased 2 percent from the previous week and was 86 percent lower than the same week one year ago.The unadjusted Purchase Index increased 9 percent compared with the previous week and was 41 percent lower than the same week one year ago.

But you need an electron microscope to see the increase in both purchase and refi apps.

One indicator of a slowing global economy is the decline of FANG (Facebook, Amazon, Netflix, Google) with declining liquidity.

The US economy is in “The Deep.” Deep into yield curve inversion, that is.

The US Treasury 10Y-2Y yield curve swam deeper into inversion at -75 basis points. The deepest inversion since just before The Great Recession and housing market crash.

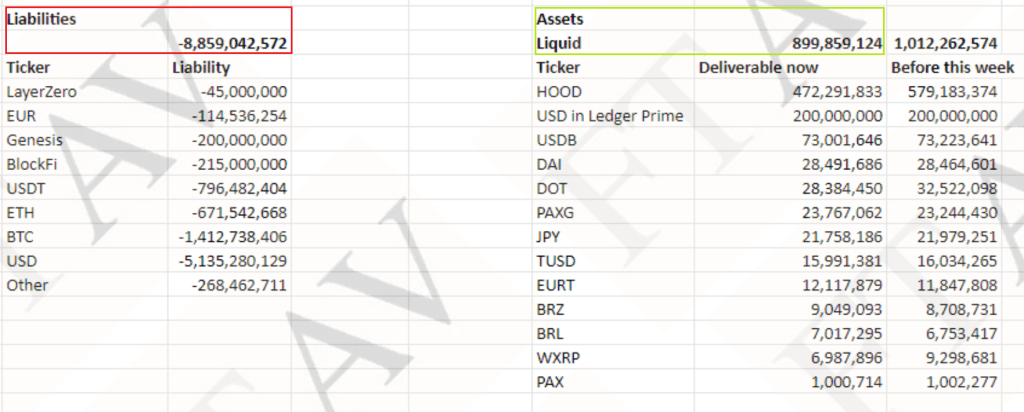

What do Bernie Madoff and Sam Bankman-Fried have in common? Greedy investors who apparently didn’t bother to monitor what was going on.

Yes, had they monitored FTX, Bankman-Fried’s company, they would have noticed that FTX held less than $1bn in liquid assets against $9bn in liabilities.

Generally, with buyer beware, the onus falls on investors to monitor what is going on. But The Fed’s completely dropped the ball on Bernie Madoff where investors didn’t seem at all curious about earning supercharged returns. The same is the case for FTX.

FTX had partnered with Ukraine to process donations to their war efforts within days of Joe Biden pledging billions of American taxpayer dollars to the country. Ukraine invested into FTX as the Biden administration funneled funds to the invaded nation, and FTX then made massive donations to Democrats in the US.

The SEC’s Gary Gensler blew it again. After his agency failed to warn investors about Terra and Celsius—whose collapses this spring sparked a trillion-dollar investor wipeout—the Securities and Exchange Commission chair allowed an even bigger debacle to unfold right under his nose. I’m talking, of course, about the revelation this week that the $30 billion FTX empire was a house of cards and that its golden boy founder, Sam Bankman-Fried, is the crypto equivalent of Theranos’s Elizabeth Holmes (Stanford University is where Holmes was an MBA student and Stanford Law School is where both SBF’s parents are professor).

To be fair, Gensler was not the only one suckered by SBF. Nearly everyone else fell for the narrative that SBF, with his cute afro and aw-shucks demeanor, was exactly the savior crypto needed to shake off its dodgy reputation and emerge as part of the mainstream financial system. The problem is that cop-on-the-beat Gensler not only failed to spot the crime—he appeared set to go along with a legislative strategy that would have given SBF a regulatory moat and made him king of the U.S. crypto market.

While it is easy to blame Gensler, the onus still falls on investors (and their managers) to MONITOR. Buyer beware.

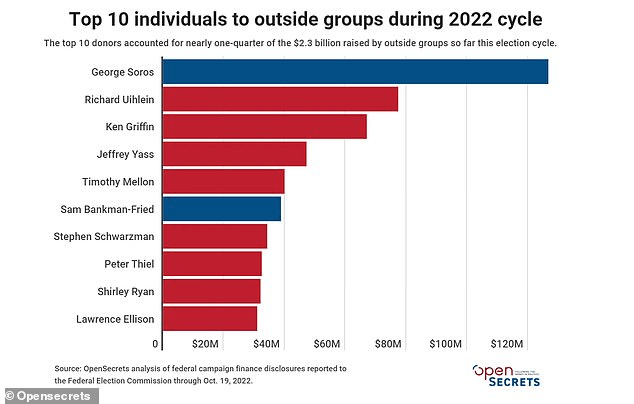

What will happen to Sam? Likely nothing. He is a golden child of Democrats and was the second biggest donor to Biden and the Democrats after America-hating George Soros. Just like Biden’s son Hunter will never pay for his many inappropriate antics, I doubt that Merrick “Double Standard” Garland will do much to Sam.

Steph Curry, Shaq and Tom Brady should fire their investment advisors and possibly sue then for failure to monitor. No one noticed $1bn in assets against $9bn in liabilities??

Sam Bankman-Fried’s bankrupt digital-asset exchange FTX was hit by a mysterious outflow of about $662 million in tokens in the past 24 hours, the latest twist in one of the darkest periods for the crypto industry.

Customers still coming to terms with the platform’s Friday plunge into Chapter 11 proceedings were subsequently confronted with what the general counsel of its US arm, Ryne Miller, described as “abnormalities with wallet movements.”

Miller said on Twitter that FTX had begun moving digital assets into cold storage — wallets that are unconnected to the internet — following its bankruptcy filing on Friday. The process was later expedited “to mitigate damage upon observing unauthorized transactions.”

Blockchain analytics firm Nansen, which gave the overall estimate of $662 million in withdrawals, said the coins flowed out of both FTX’s international and US exchanges. A separate analysis by Elliptic stated that initial indications showed almost $475 million had been stolen from the exchange in illicit transactions, with the stablecoins and other tokens that were taken being rapidly converted to Ether on decentralized exchanges — “a common technique used by hackers in order to prevent their haul being seized.”

And like that, O’Biden’s Treasury secretary Janet Yellen FTX Debacle said that it shows need for crypto regulation. Or Yellen could suggest a “buyer beware” tactic, but she is part of the most aggressively regulatory administration in history, MORE regulation is needed! /sarc

At least Yellen is noticing Bankman-Fried (a new twist on Kentucky-Fried) and FTX since she is seemingly oblivious to the harm being done by The Federal Reserve and The Federal government with regards to inflation and debt growth. She is a Bird of War.

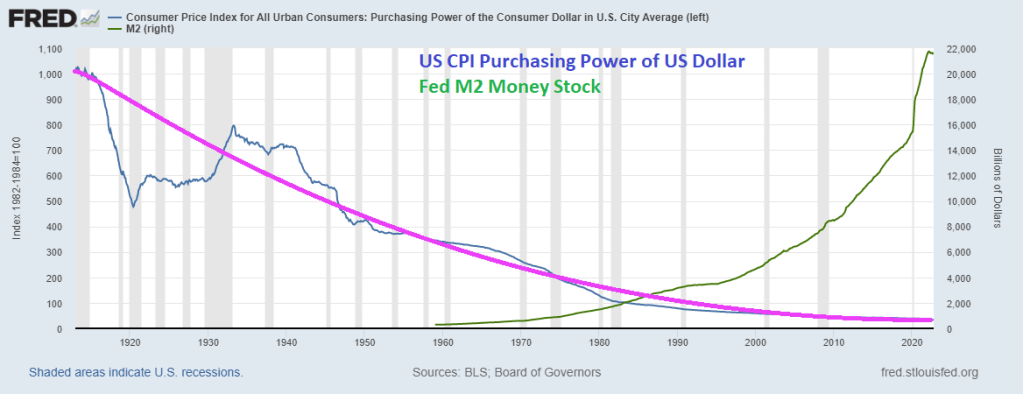

Like this chart of the Purchasing Power of the US Dollar CPI. Janet?

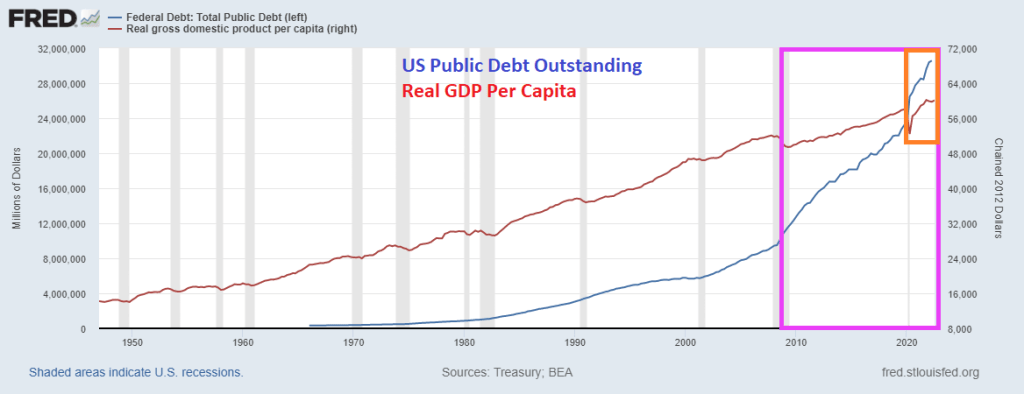

Or how about this chart of US Public Debt Outstanding and Real GDP growth per capita? The Fed and Federal government broke the bank, so to speak, by bailing out the banks in the financial crisis (pink box) and then again for the Covid crisis (orange box). Janet?

Damn it, Janet. Why don’t you discuss the Medicare and Social Security crisis (remember Joe Biden said Republicans may try to fix it which Biden turned into a nasty attack claiming that Republicans were going to take away your Social Security).

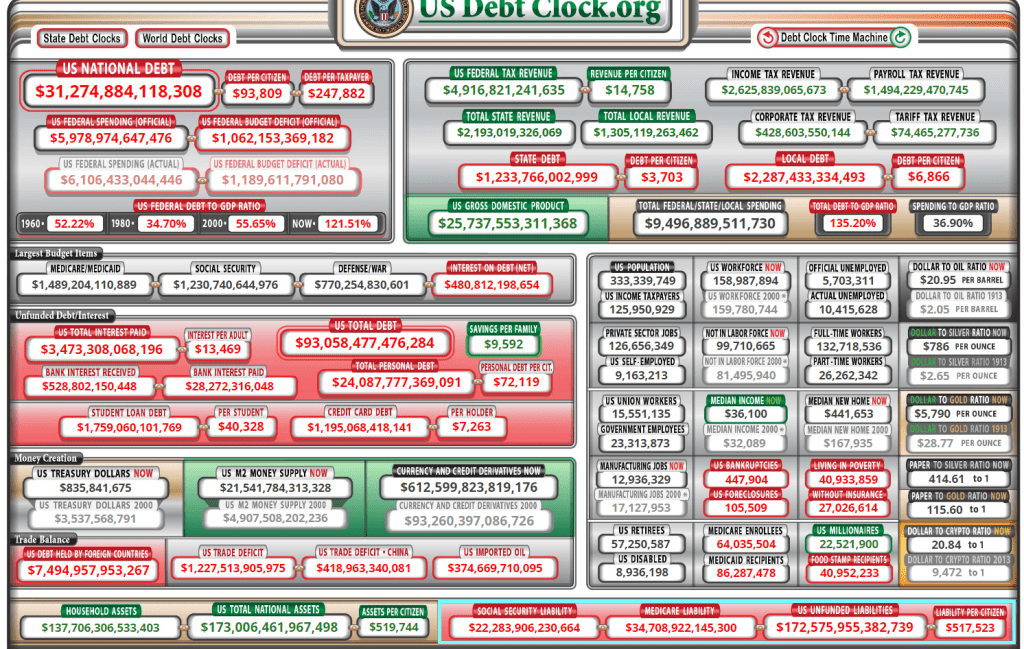

Lastly, the US has $172.6 TRILLION in unfunded Federal promises. Janet? A least FLA Senator Rick Scott tried to address the problems with Social Security, but Nasty Joe Biden “yelled Republicans are going to take away your Social Security!” I argue that O’Biden, Yellen and Democrats are going to let SS blow-up rather than take on politically challenging issues. Social Security liability is $22.23 trillion yet O’Biden just promised $500 billion per year to third-world countries and keeps sending billions to Ukraine. Janet?

On the crypto side (that Yellin’ Yellen wants to regulate), at least Dogecoin is up 10.37%.

The Bank of England followed the Fed’s 75 basis-point increase with an equivalent hike on Thursday, but strongly pushed back against market expectations for the scale of future increases, warning that following that path would induce a two-year recession. The pound fell 1.8% to $1.1183.

Stocks and bonds fell as Jerome Powell’s warning that the Federal Reserve would raise interest rates more than previously anticipated sapped risk appetite. The dollar gained.

Futures on the S&P 500 fell 1% in the wake of Wednesday’s 2.5% drop. The selloff spread to Europe and Asia, where China’s affirmation of its Covid-Zero stance dashed hopes of a reopening. Lumen Technologies Inc., Peloton Interactive Inc., Moderna Inc. and Qualcomm Inc. tumbled in premarket trading, while Etsy Inc. and EBay Inc. rose.

So, the BofE, Fed and ECB are back to 2008/2009 era central bank rates.

But the US Fed is slow to shrink its enormous balance sheet.

US mortgage applications declined for the sixth consecutive week despite a slight drop in rates.

Mortgage applications decreased 0.5 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending October 28, 2022. This week’s results include revised data to reflect an update to last week’s survey results.

The Refinance Index increased 0.2 percent from the previous week and was 85 percent lower than the same week one year ago. The seasonally adjusted Purchase Index decreased 1 percent from one week earlier. The unadjusted Purchase Index decreased 2 percent compared with the previous week and was 41 percent lower than the same week one year ago.

This morning’s WIRP (Fed Funds Futures data) is pointing to a 75 basis point increase from The FED FOMC (open market committee) at 2pm EST, rising to over 5% by the May 2023 meeting before declining again.

You must be logged in to post a comment.