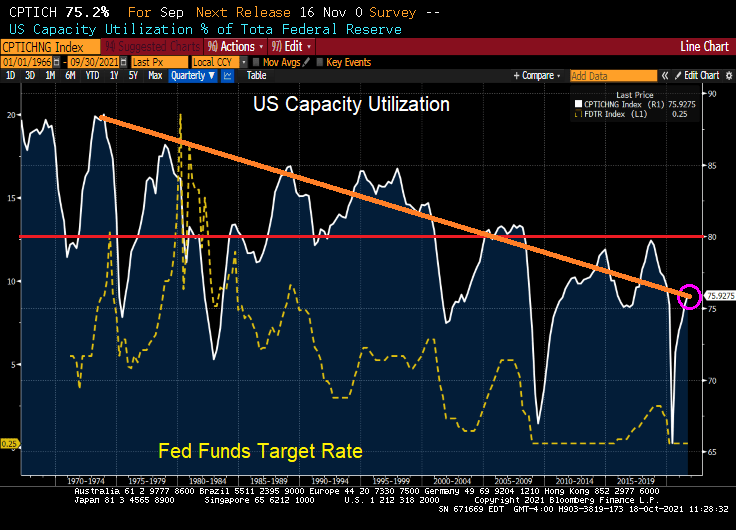

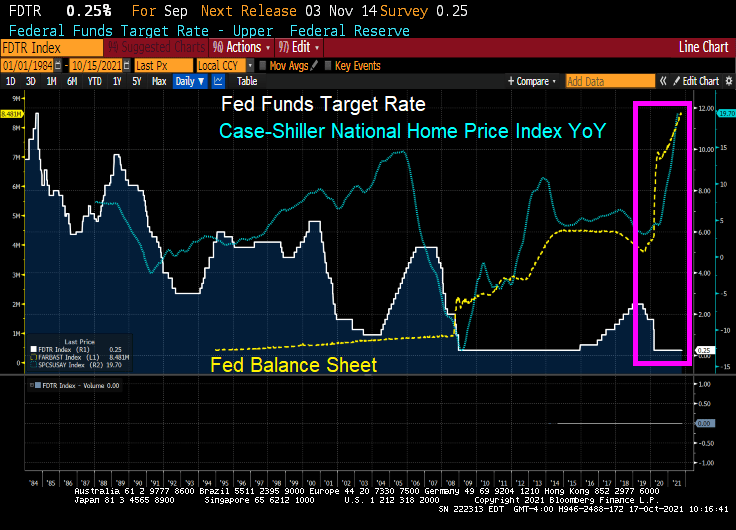

It used to be that capacity utilization was a signal for The Federal Reserve to raise or lower their key target rate. When capacity utilization rose above 80%, the economy was deemed to getting “hot” and The Fed would raise rates. And vice-versa.

But then mass outsourcing occurred, primarily to China and southeast Asia. Since the 1970s, the general trend in US capacity utilization has been downward. But the last time the US saw capacity utilization of above 80% in Q4 2007. Capacity utilization almost hit 80% in August 2018

Oddly, The Fed started raising their target rate in 2015 under Fed Chair Janet Yellen AS CAPACITY UTILIZATION WAS FALLING. Capacity utilization hit almost 80% as The Fed put the brakes on rate hikes before Covid struck.

So, capacity utilization was obviously not on the mind of Yellen and the FOMC. Call it the new abnormal.

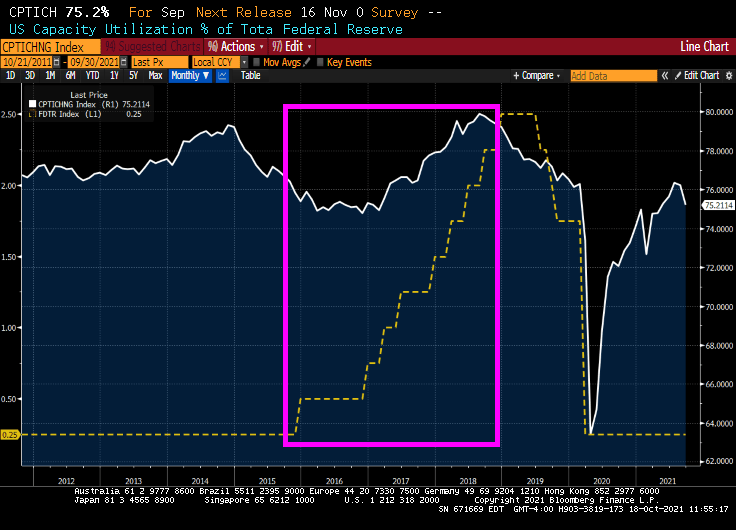

With capacity utilization falling, the path of Fed policy rate has shifted sharply over the past couple of weeks, to currently pricing first hike into the September 2022 FOMC meeting and second hike by February 2023 — there are now 100bp of rate hikes priced by the end of 2023, in line with the Fed’s dot-plot forecast.

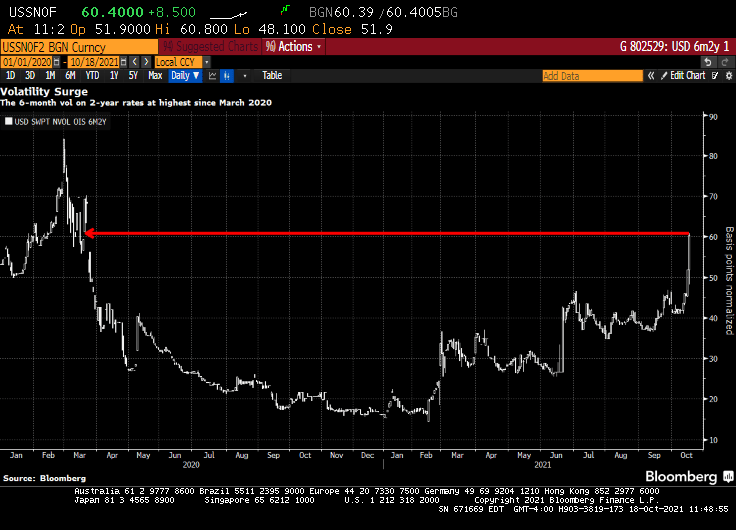

Short-dated volatility on front-end U.S. rates — known as the upper left corner of the volatility surface — continues to catch a bid over the U.S. morning session, spurred by a sharp hawkish re-pricing of the Fed’s policy stance.

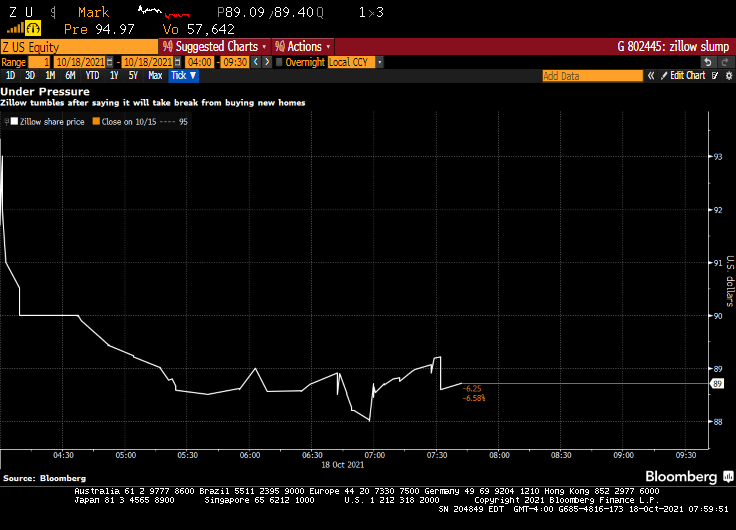

Zillow Group Inc. shares fell as much as 6.8% in premarket trading Monday after the online real estate firm said it would stop buying new homes and work to clear a backlog of properties it already has.

The Seattle-based company, which acquired more than 3,800 homes during the second quarter, has seen its stock price tumble about 27% this year after it nearly tripled in 2020 amid the pandemic-fueled housing market boom.

The shares have come under additional pressure in recent weeks after a viral TikTok video from a real estate agent in Las Vegas said an unnamed company was pulling off a convoluted scheme to manipulate housing prices in his home market. Zillow is also facing increased competition from firms like Opendoor Technologies Inc., which announced in August that it bought about 8,500 homes during the second quarter.

Zillow, which acquired more than 3,800 homes in the second quarter, will stop pursuing new home purchases as it works through a backlog of properties already in its pipeline.

“We are beyond operational capacity in our Zillow Offers business and are not taking on additional contracts to purchase homes at this time,” a spokesperson for Zillow said in an email. “We continue to process the purchase of homes from sellers who are already under contract, as quickly as possible.”

Zillow is best known for publishing real estate listings online and calculating estimated home values – called Zestimates – that let users keep track of how much their home is worth. The popularity of the company’s apps and websites fuels profits in Zillow’s online marketing business.

Of course, The Fed dumping in trillions into a bottlenecked housing market is helping to fuel the flipper fire.

Is this a secret warning about a possible slowdown in the housing market?

Has The Federal Reserve lost control of the economy? And inflation? The answer is likely yes. Why?

The Covid crisis has been played by the Federal government as an excuse for insane levels for spending coupled with massive monetary stimulus from The Federal Reserve.

As an example of The Fed losing control is US savings. The Fed’s model is to drive savers into consumption, therefore raising production and increasing GDP growth. But alas, The Fed can’t overcome the fear faced by consumers with Covid, Covid shutdowns, and rapidly rising prices.

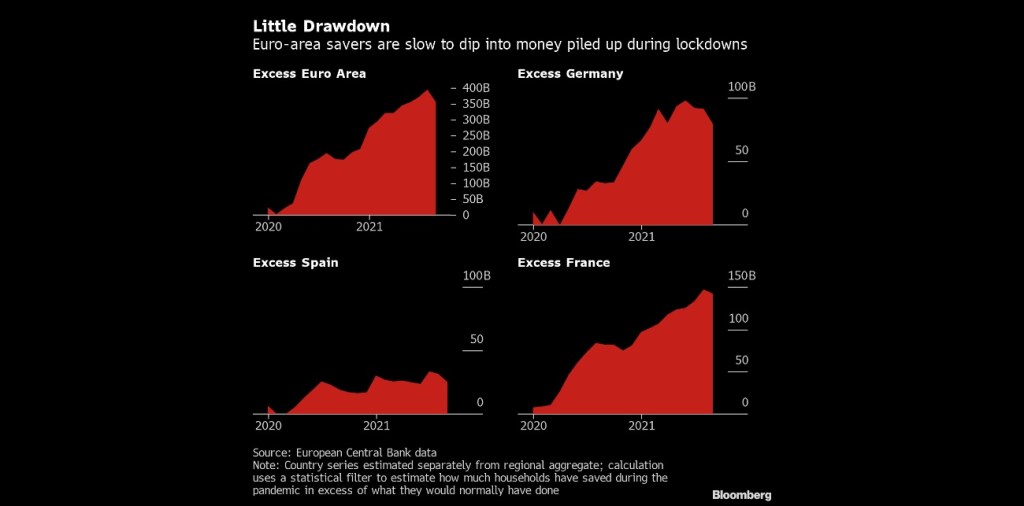

(Bloomberg) — Consumers in Europe and the U.S. aren’t rushing to spend more than $2.7 trillion in savings socked away during the pandemic, dashing hopes for a consumption-fueled boost to economic growth on both sides of the Atlantic.

In the wake of lockdown easing during the northern hemisphere’s summer holiday season, excess savings in euro-area bank balances declined only marginally in August, and Italy still recorded an increase, according to calculations by Bloomberg Economics. In the U.S. there has also been no drawdown, the figures show.

The absence of a consumption surge that had been anticipated by some economists may speak against the prospect of a lasting inflation shock feared by central banks. While higher balances could help households cope with skyrocketing heating bills, tepid demand might temper businesses’ ability to push through permanent price increases.

In the USA, we see accumulated savings despite near-zero deposit rates at banks.

To be sure, The Fed reacted (or overreacted) to the Covid outbreak by increasing the money supply and their purchase of Treasuries and Agency MBS as the Federal government went on a wild spending spree.

But with trillions in Stimulypto Federal spending and Fed money printing, the bottlenecks in the economy (which apparently weren’t known before … ) have contributed to massive price increases that aren’t going away any time soon.

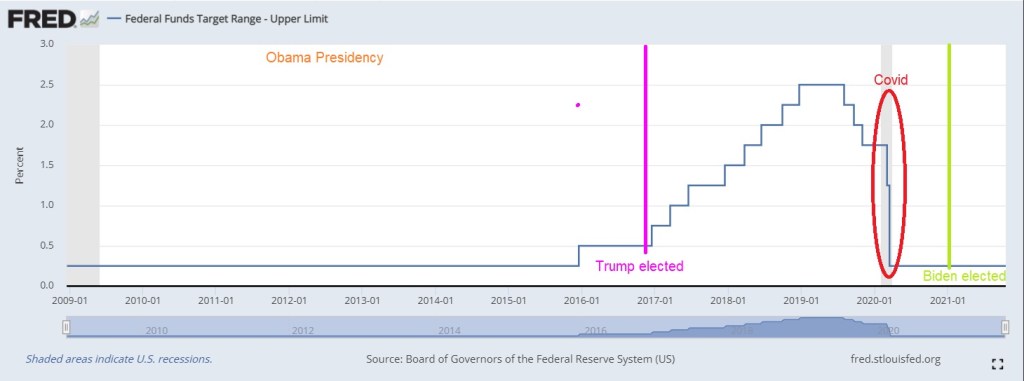

Notice how Fed monetary policies changed after the housing bubble burst and ensuring financial crisis/Great Recession. Before 2008, The Fed periodically whipsawed their Fed Funds target rate. But since late 2008, we have seen hardly any move from The Fed (except for 2017-2020 while Trump was President). For Obama,

Here is a look at The Fed’s record under Obama, Trump and Biden. The Fed raised their target rate only once under Obama until Trump was elected. Then The Fed raised rates 8 times. Then began lowering them again (5 times) leading to a big drop when Covid stuck. So for Trump, The Fed changed their target rate 13 times compared to 1 rate change under Obama and none under Biden.

And the above chart is only The Fed’s target rate. My point is that Yellen failing to raise rates under Obama has resulted in this over DC-Stimulypto we are seeing today.

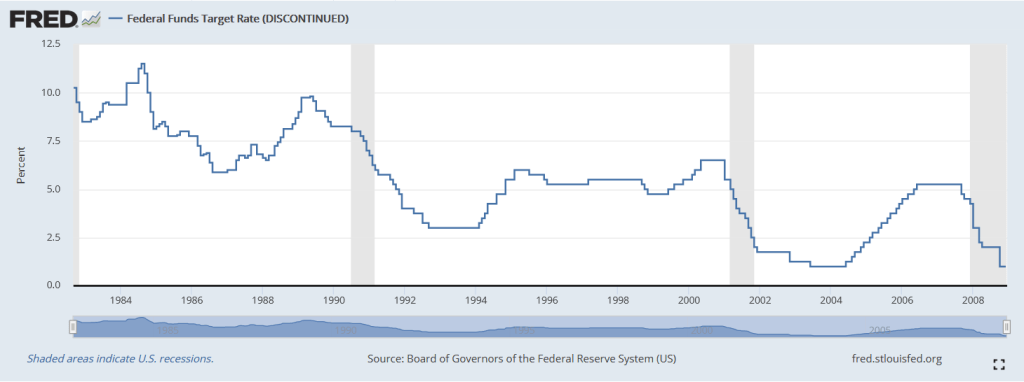

Note the difference in Fed policies BEFORE the financial crisis. We need to return to a normal Fed policy rather than the hyper-inflationary zero-rate, QE policies since 2008.

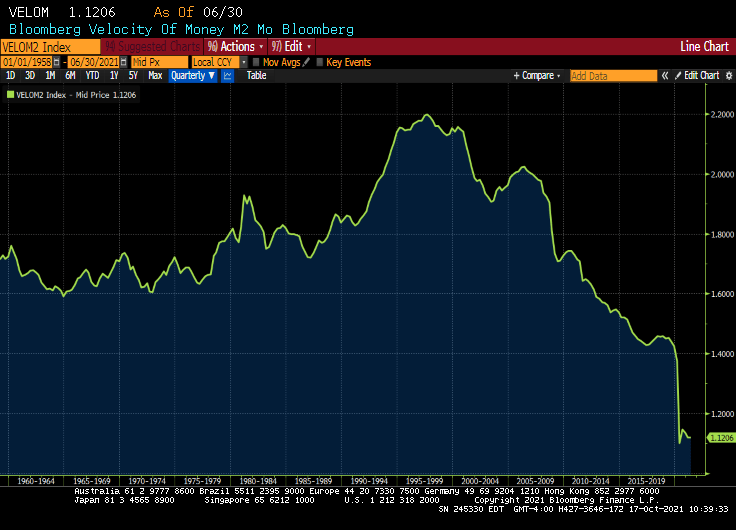

M2 Money velocity (GDP/M2 Money) remains near an all-time low.

But given DC’s spending spree and all-time lows for M2 Money Velocity, The Fed is going to need to keep purchasing trillions in debt at low interest rates. The abnormal Obama years (Bernanke/Yellen) are the NEW abnormal. Or should I say abby normal policies?

Dr. Frederick FrankensteinAre you saying that I put an abnormal brain into a seven and a half foot long, fifty-four inch wide GORILLA?

So, yes, Bernanke and Yellen put into place abnormal policies that Powell is following into the world’s largest economy (or gorilla).

Only Igor and The Federal Reserve would pick such abnormal policies that ultimately lead to massive misallocations and inflation.

On a side note, do Biden and Transportation Secretary Pete Buttigieg really believe that they can fix the backed-up ports that are flooded with cargo thanks to Stimulypto? By Christmas??

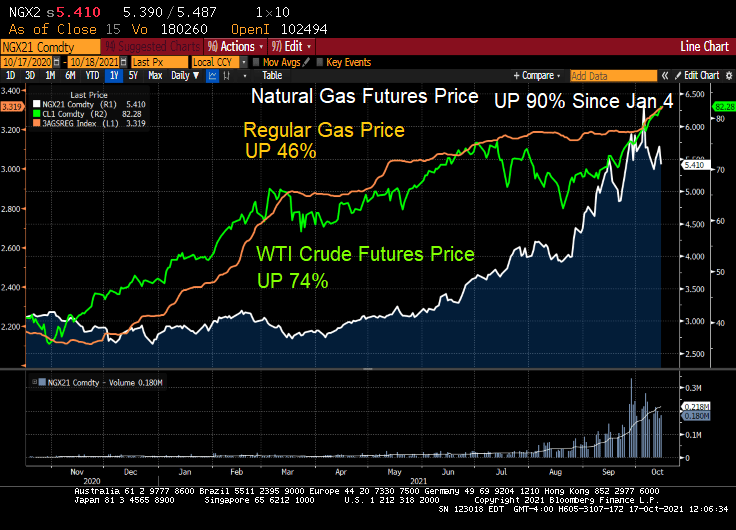

Not with natural gas prices up 90% since January 4th!

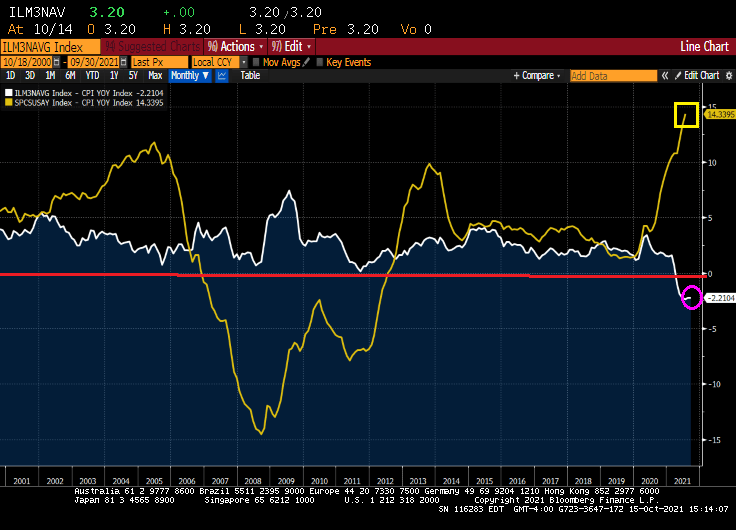

This is a time even unlike the disastrous housing bubble of the 2000s that led to the financial crisis and Great Recession. Even during the housing bubble years, we still had positive REAL mortgage rates: Bankrate 30Y Fixed rate – CPI YoY. But today we have even FASTER REAL home price growth and NEGATIVE mortgage rates!

And yes, REAL home price growth is 14.34% YoY while REAL hourly earnings growth is -0.79%.

The University of Michigan consumer survey came out today and buying conditions for housing improved to 75. Which means that more people were negative than positive due to skyrocketing home prices.

With negative 30Y mortgage rates and rising apartment rents, is it time to buy? Just remember what happened to Leon in Blade Runner.

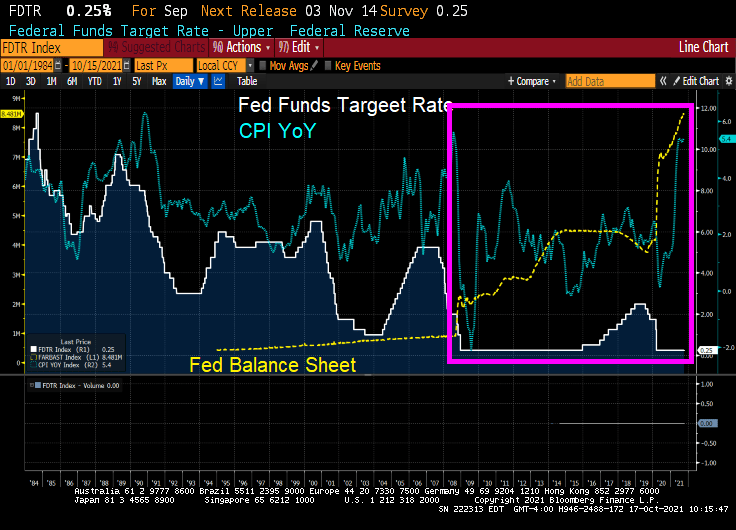

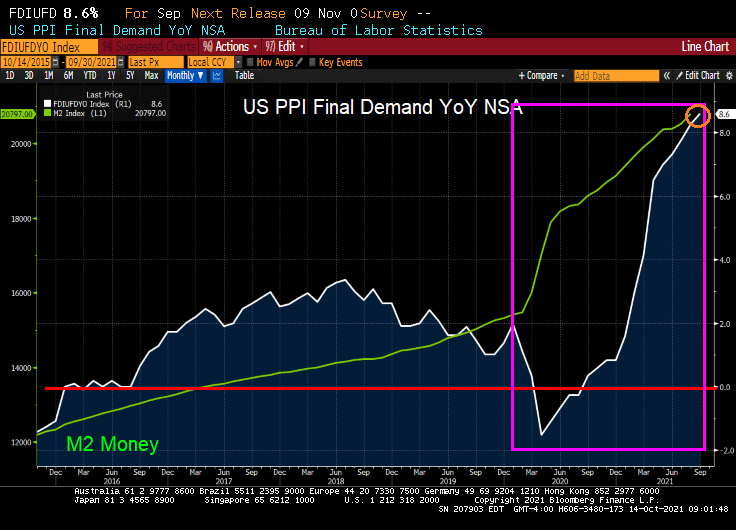

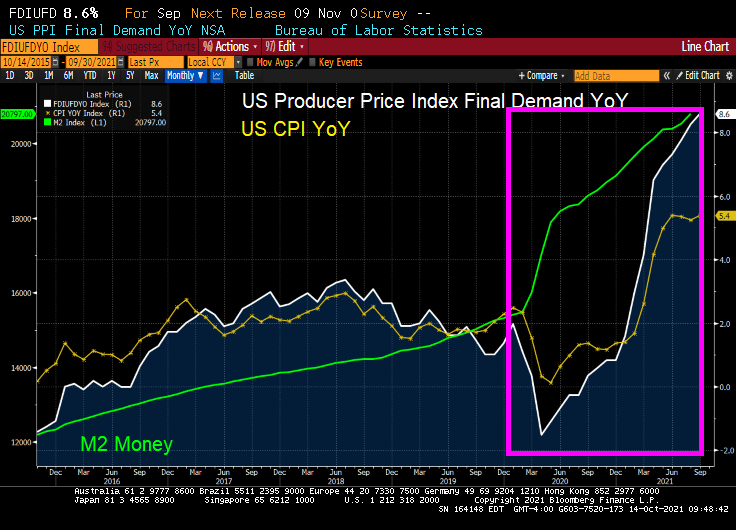

The US Producer Price index (Final Demand) rose to a blistering rate of 8.6% YoY.

Will this translate to higher consumer prices? Of course it will.

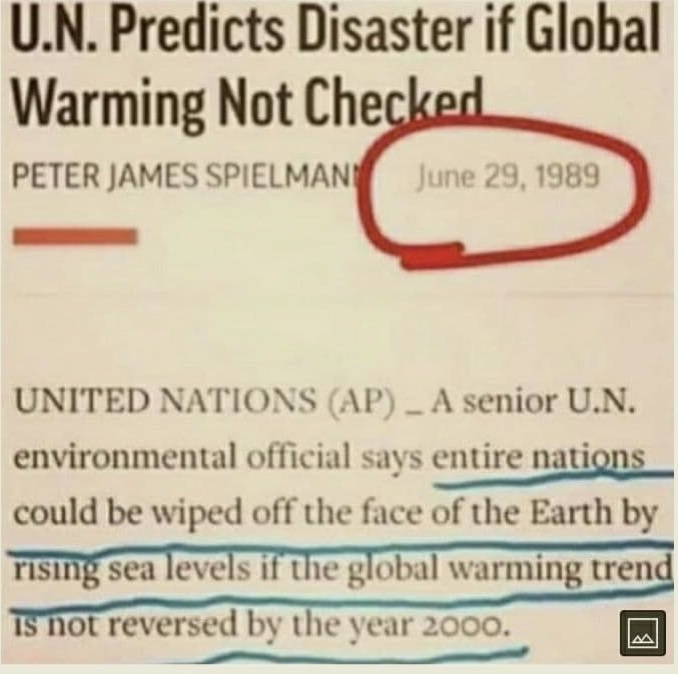

When The Fed or the Biden Administration says that inflation is transitory and will be fixed once we unclog the shipping pipes, remember this warning from the UN that global warming will wipe out entire nations if not reversed by 2000. So, it is too late! I am buying a gas-guzzling Cadillac Escalade with a monster V-8 engine!! (Not really, I am more of a Ford kind of person).

Everyone seems worried about it. Bridgewater Associates co-Chief Investment Officer Greg Jensen says spiraling prices that choke off growth are a “real risk” that many portfolios are massively overexposed to. A “fairly strong consensus” of market professionals believe that some kind of stagflation is more likely than not, according to a Deutsche Bank AG survey. And while Goldman Sachs Group Inc. urged investors to buy the dip, strategists said “stagflation” was the most common topic in client conversations.

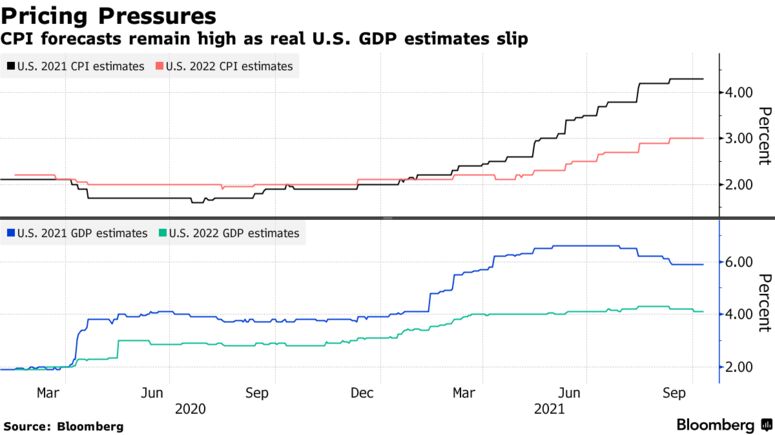

Wherever you fall on the debate, alarm bells are ringing as energy prices head toward multiyear highs and persistent shortages crimp supply chains worldwide. That’s fueling price pressures and pushing up bond yields just as economic growth is cooling and central banks such as the Federal Reserve weigh scaling down pandemic-era stimulus. And after a second straight month of disappointing U.S. jobs gains, the stakes are rising heading into this week’s inflation report.

“The reality that inflation is more persistent and sustainable than the ‘transitory’ camp thought, and that inflation and its causes are in turn slowing economy growth,” said Peter Boockvar, chief investment officer for Bleakley Advisory Group.

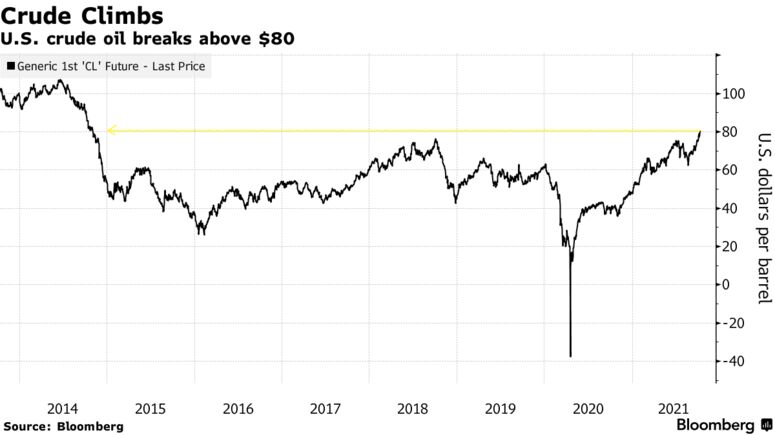

Energy Epicenter

Much of the stress is emanating from the energy market, where West Texas Intermediate crude oil broke above $82 per barrel for the first time since 2014 on Monday amid a power crisis from Europe to Asia. Prices of coal and natural gas have also jumped, with demand ahead of winter whittling worldwide stockpiles.

The commodity surge has thrust stagflation fears front-and-center in markets, given that higher energy prices have the potential to pinch consumers, according to Principal Global Investors. Gains in consumer spending are already expected to slow, leading Goldman economists to slash U.S. growth estimates over the weekend.

“The idea was already starting to take shape. The increase in commodity prices has just formalized those fears,” said Seema Shah, Principal’s chief global strategist. “While there have been complaints around higher food prices, higher lumber prices, higher clothes prices, it’s the increase in household bills that has really put fear into peoples’ minds, because it is so visible and rising gas prices are difficult to substitute away from for an average household.”

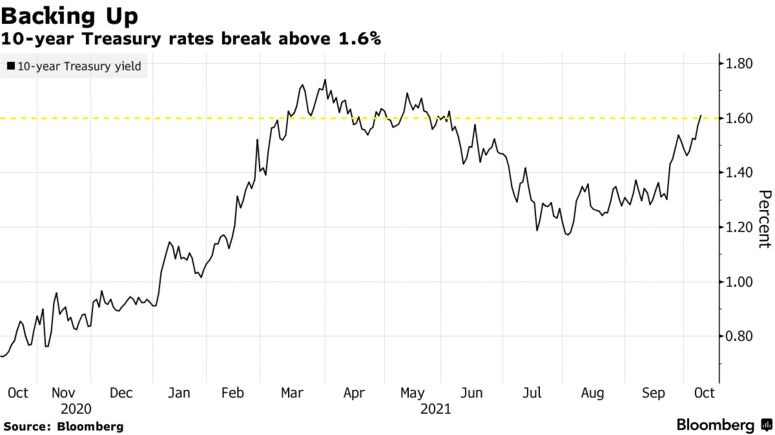

Murky Bond Picture

Sky-high commodity prices have filtered through to the Treasury market, where yields on benchmark 10-year notes broke above 1.6% for the first time since June last week. Driving the gain is an increase in breakeven inflation rates, while so-called real yields — often viewed as a proxy of growth expectations — have retreated so far this month.

“If we look at the composition within the TIPs market, we see an increase in breakevens to the detriment of real yields,” BMO strategist Ian Lyngen said on the firm’s “Macro Horizons” podcast. “We read this as the market’s focus on longer-term inflation has taken some of the optimism out of the growth profile going forward.”

Morgan Stanley strategist Andrew Sheets disagrees. Breakeven rates are still below their May peaks, while the cross-asset landscape is distinct from the stagflationary setup of the 1970s, he argued. Data compiled by Bloomberg shows gross domestic product is forecast by economists to rise 5.9% this year, 4.1% next year and 2.4% in 2023.

“Asset pricing also couldn’t be more different. Over the last century, the 1970s represented an all-time high for nominal interest rates and an all-time low for equity valuations,” Sheets wrote in a note Sunday. “Today we’re near a low in yields and a high in those valuations.”

Stocks Still Serene

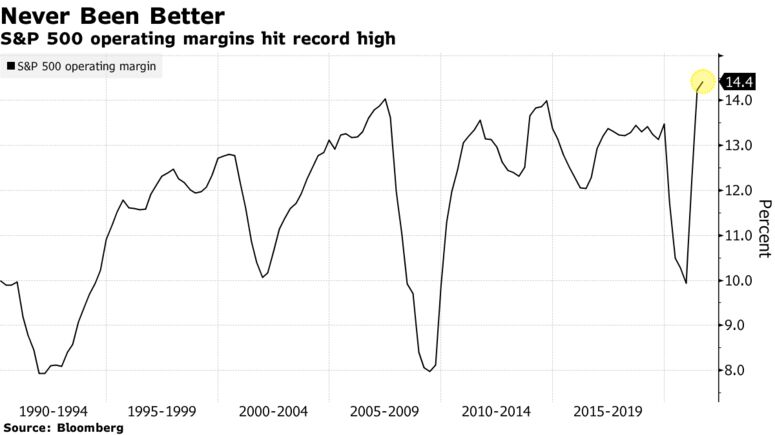

Equity investors so far seem unperturbed. That’s the view of Matt Maley, chief market strategist for Miller Tabak + Co., given that the S&P 500 is just 3.9% lower from its all-time high. However, the mood music could change as the third-quarter reporting season kicks off and corporate executives sound off on supply chain issues and rising input costs, he said.

“The key should be this earnings season,” Maley said. “If a lot of companies start talking about margin pressures, the stock market will start pricing in stagflation rather quickly.”

So far, balance sheets have been resilient. Operating margins for the S&P 500 clocked in at 14.4% last quarter, a record high, with companies in many cases actually benefiting from the inflation uptick.

But should stagflation fears start to meaningfully rattle equity markets, shares of companies with higher pricing power — the ability to pass on costs — should profit, according to Goldman, after several weeks of underperformance.

“Stocks with strong pricing power have recently lagged but appear attractive if stagflationary concerns continue to build,” strategists led by David J. Kostin wrote. “If inflation remains high alongside a weakening economic growth outlook, firms with strong pricing power should be best positioned to maintain profit margins despite slowing revenue growth and rising input costs.”

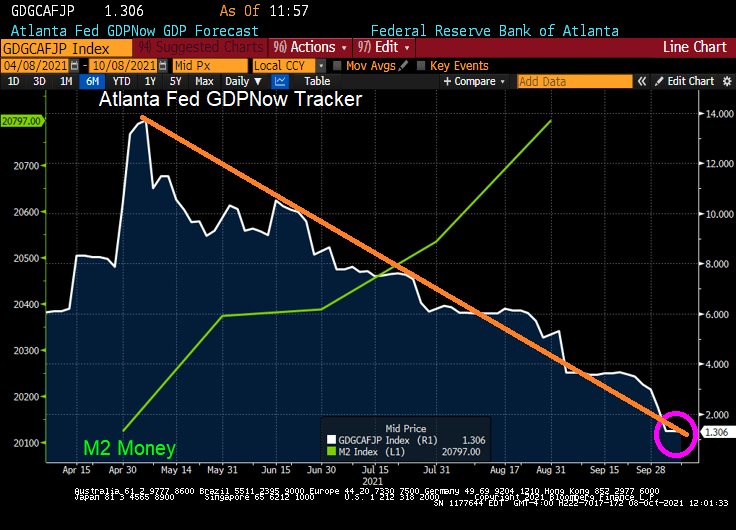

Not to mention real-time GDP of 1.3%. And falling!

Of course, there will be cries in Washington DC to spend trillions … and trillions … and trillions.

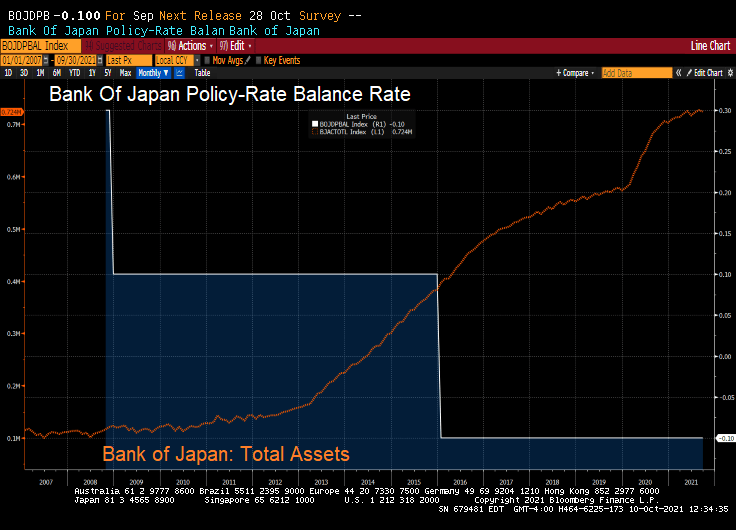

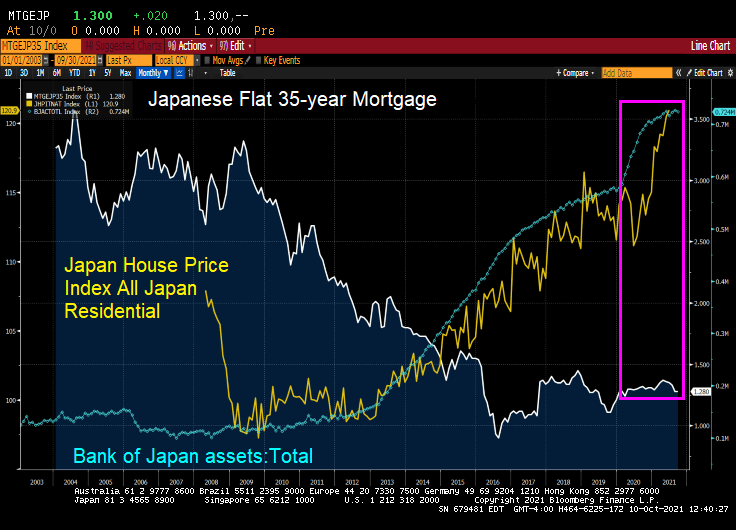

What’s left of it is that the BoJ (and Bank of Japan Governor Haruhiko Kuroda) now holds about half of the huge pile of the central government’s debt. With their target rate at -0.10% and a gargantuan balance sheet, what could go wrong?

But BOJ’s QE has ended. The BoJ’s overall assets stopped growing, and its holdings of government bonds have started to decline.

As of the BoJ’s balance sheet dated September 30, released on Thursday, total assets declined to a still monstrous ¥724 trillion ($6.4 trillion), below where it had been in May 2021.

But look at Japanese home prices with the growth of the BOJ’s balance sheet and general decline in mortgage rates. Like the USA, there was a balance sheet spike associated with Covid and a resulting spike in home prices.

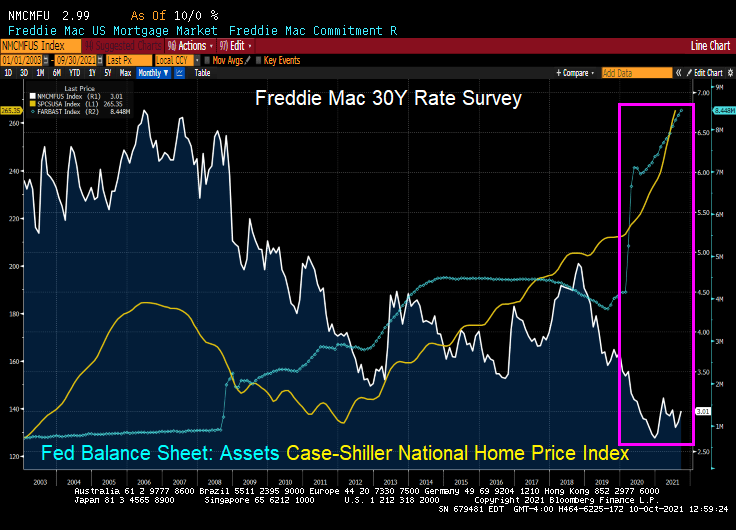

The USA? We also saw a surge in home prices following The Fed’s monetary “stimulypto.”

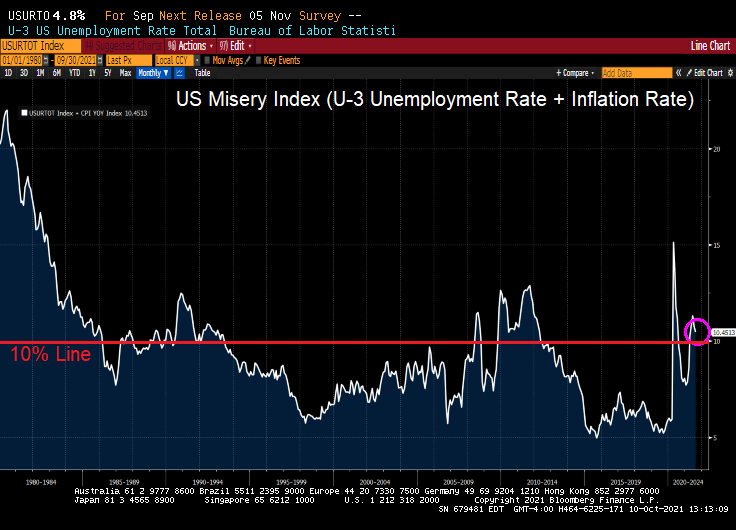

Bear in my that the US Misery Index is above 10% (U-3 unemployment + inflation).

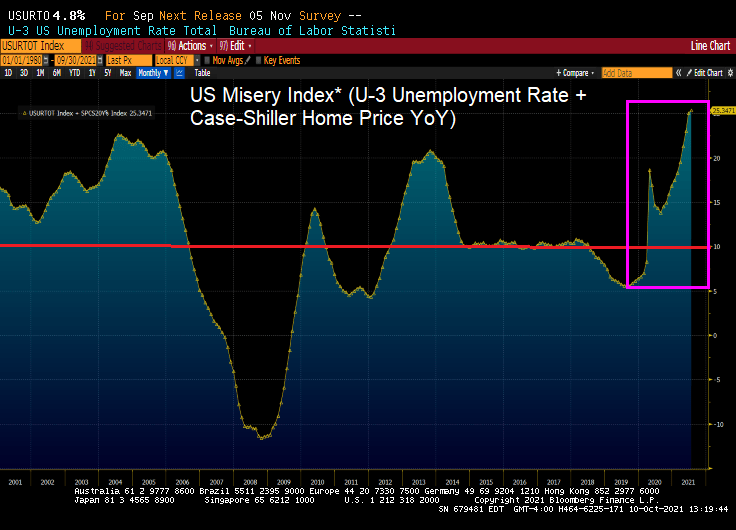

And if I define the US Misery Index as U-3 unemployment + home price growth, we can see we are at record misery rates. Miserable for households that don’t own a home or are trying to move to a higher housing price area).

Like the poem, Casey At The Bat, the US economy struck out with a shockingly bad jobs report for September.

Oh, somewhere in this favored land the sun is shining bright; The band is playing somewhere, and somewhere hearts are light, And somewhere men are laughing, and somewhere children shout; But there is no joy in Mudville USA—mighty Casey Biden has struck out.

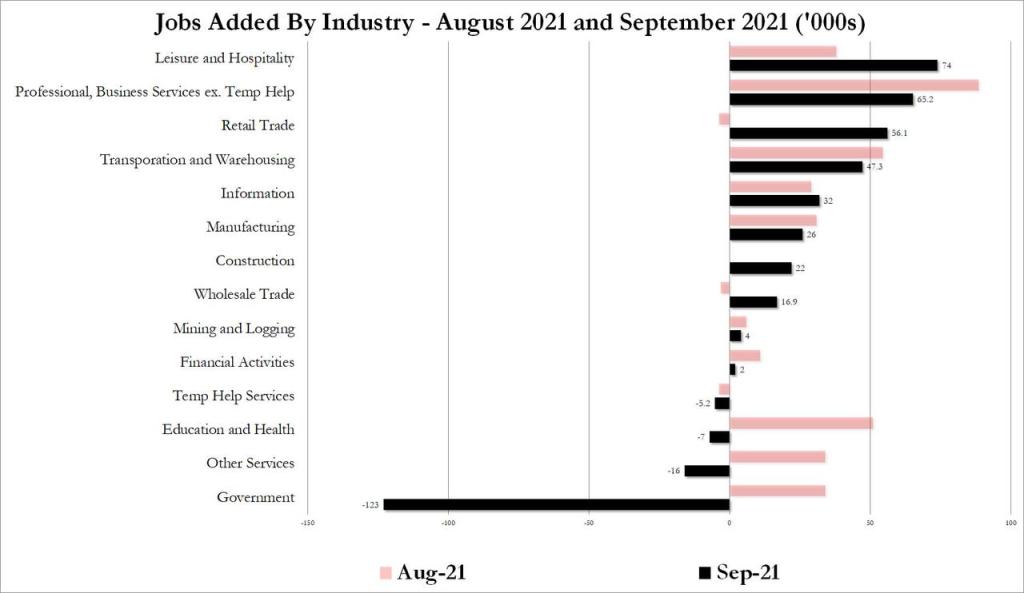

The U.S. economy added fewer jobs than forecast for a second straight month in September. Nonfarm payrolls increased by just 194,000 last month after an upwardly revised 366,000 gain in August, Labor Department figures showed Friday. 500K was expected.

The U-3 unemployment rate declined to 4.8% (meaning that the labor force shrank due to people dropping out of the labor force). In fact, 338,000 people dropped out of the labor force.

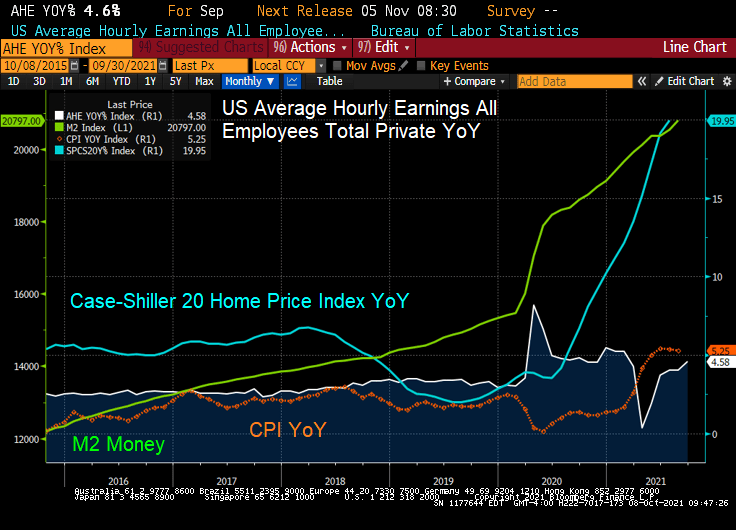

Average hourly earnings YoY rose to 4.6%. While that is an improvement, but it is lower than the inflation rate of 5.25% YoY and house price inflation of 20% YoY.

This miserable jobs report is a victory for Fed doves that don’t want to raise rates or slow down the balance sheet growth.

Where were the jobs created? Leisure and hospitality, as usual, leads in job gains.

It was great to be a “Master of the Universe” (Treasury and MBS trader) since October 1981 when the US 10Y Treasury yield peaked at 15.84% and mortgage rates peaked at 18.63%. Treasury and mortgage rates have generally fallen ever since. But what happens if Treasury and mortgage rates rise?

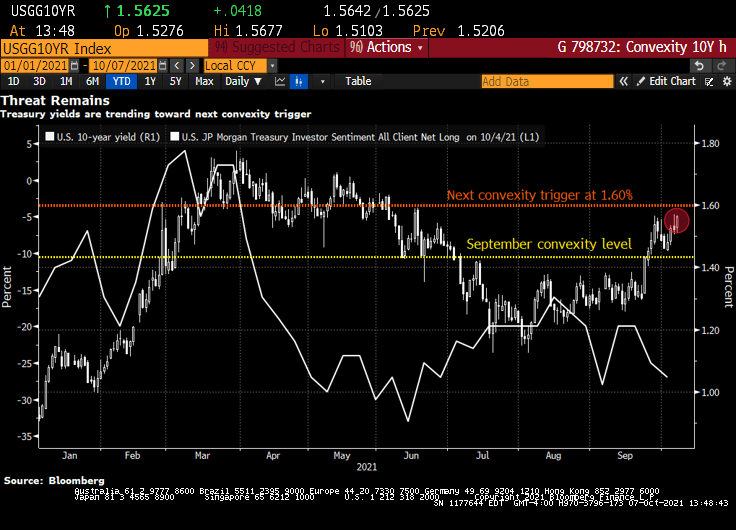

Bond investors are piling back into short positions, motivated not only by the specter of inflation but also by the risk that yields are approaching levels that will unleash a wave of new selling by convexity hedgers.

That level is around 1.60% in the U.S. 10-year Treasury yield, less than 10 basis points from its current mark, according to Brean Capital’s head of fixed income strategy, Scott Buchta. It’s the mid-point of “a key threshold” between 1.40% to 1.80%, an area “most critical from a convexity hedging point of view.”

Convexity hedging involves shedding U.S. interest-rate risk to protect the value of mortgage-backed securities as yields rise, slowing expected prepayment rates.

It’s already begun to pick up as yields stretched past the 1.40% level. Another wave is expected at around 1.6% — a point of “maximum negative convexity” in agency MBS, “where 25bp rallies and sell-offs should have an equal effect on convexity-related buying and selling,” Buchta says.

Signs that short positions are accumulating include Societe Generale’s “Trend Indicator.” Among its 10 newest trades are short positions in Japanese 10-year debt, German 5-year debt futures, U.K. 10-year gilts, U.K. short sterling and U.S. 2- and 5-year notes. Meanwhile, CFTC positioning data for U.S. Treasury futures show asset managers flipped to net short in 10-year note contracts in the process of dumping the equivalent of $23 million per basis point of cash Treasuries over the past week. Hedge-fund shorts also remain elevated in the long-end of the curve, as measured by net positions in Bond and Ultra Bond futures.

“Bond-bearish impulses remain in place,” says Citigroup Inc. strategist Bill O’Donnell in a note, citing tactical and medium-term set-ups. Traders should be aware of short-covering rallies in the meantime, however, he says.

“Potentially extreme short-term positioning and sentiment set-ups could easily allow for a counter-trend correction under the right conditions,” he said.

U.S. 10-year yields topped at 1.57% this week, the cheapest level since June, spurring the breakeven inflation rate for 10-year TIPS to 2.51%, the highest since May. Friday’s September jobs report could add fuel to this inflationary fire, rewarding bond shorts.

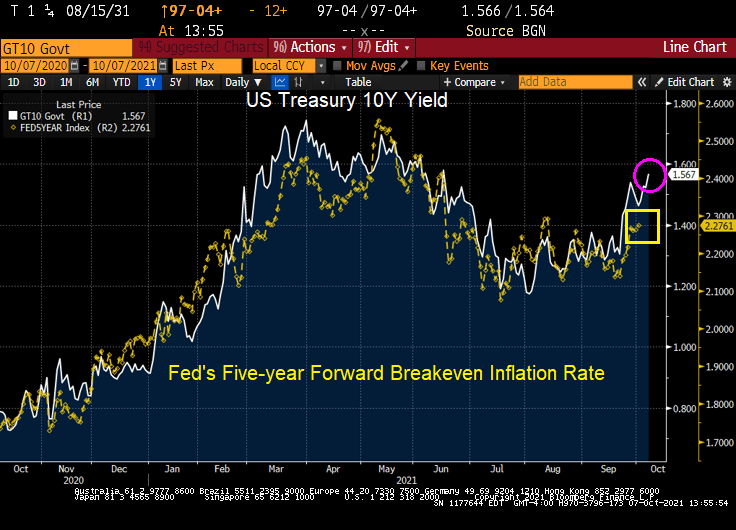

Here is a chart of the rising 10Y Treasury yield against The Fed’s 5Y forward breakeven rate.

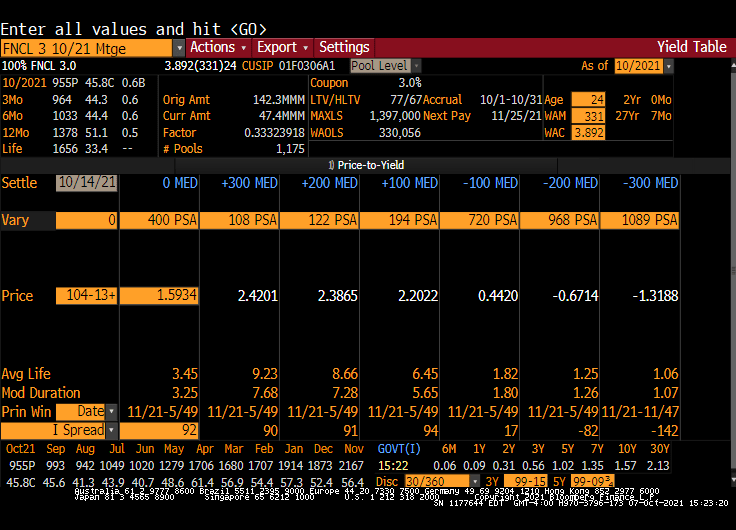

Here is a Fannie Mae 3% coupon MBS. Note the rise in Modified Duration with an increase in interest rates.

You must be logged in to post a comment.