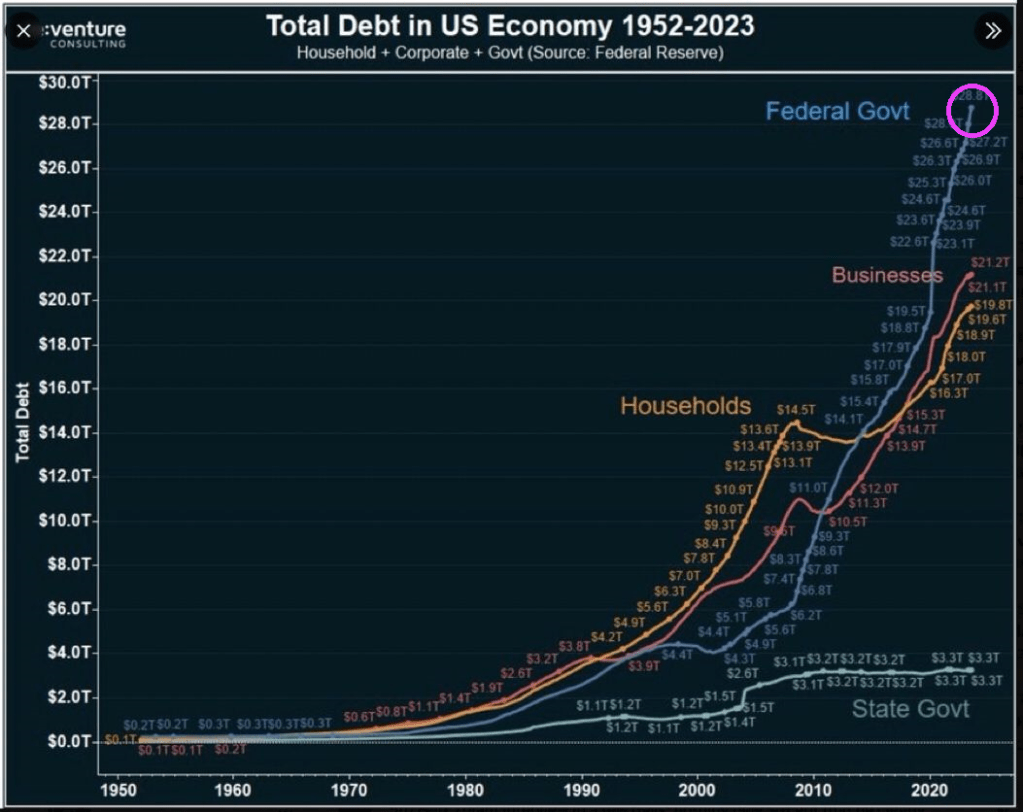

Both the US Federal government and California’s government are facing a fiscal inferno. Thanks to a softening economy and inane fiscal policies.

At the macro level, we see that The Federal government has gone wild spending money and borrowing it. Much more than businesses and households. Biden’s wild spending reduces the degrees of freedom that Treasury has if the US slips into another recession or depression.

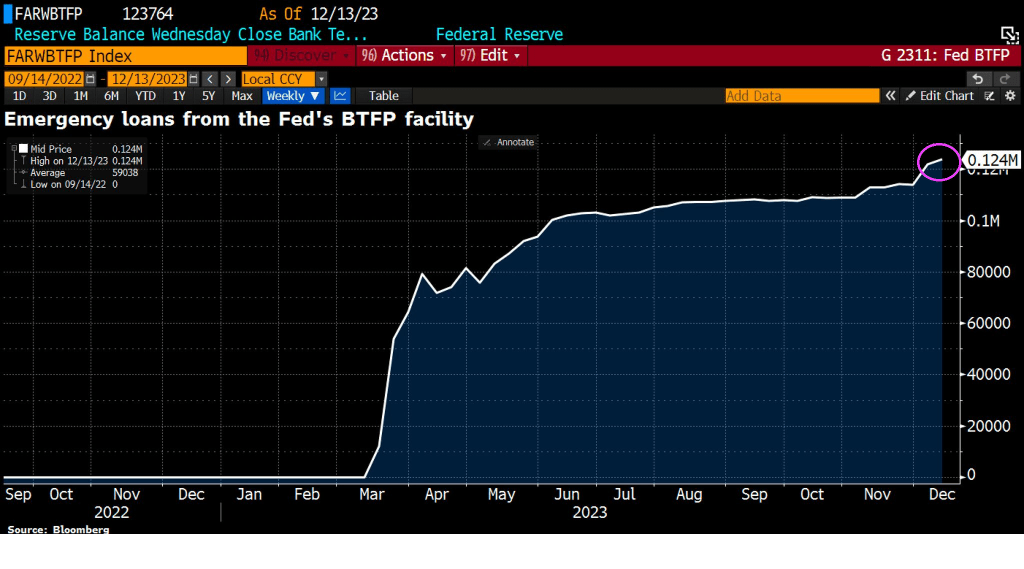

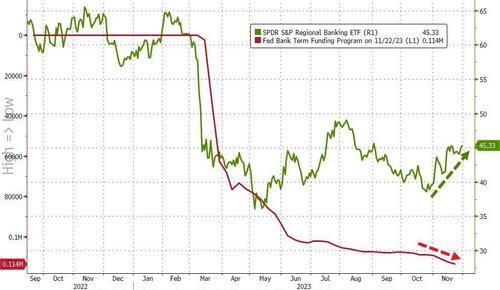

First, let’s begin with banks to illustrate the worsening condition of the economy. Emergency loans from The Fed’s Bank Term Funding Program (BTFP) is on the rise, signaling perceived trouble in the economy.

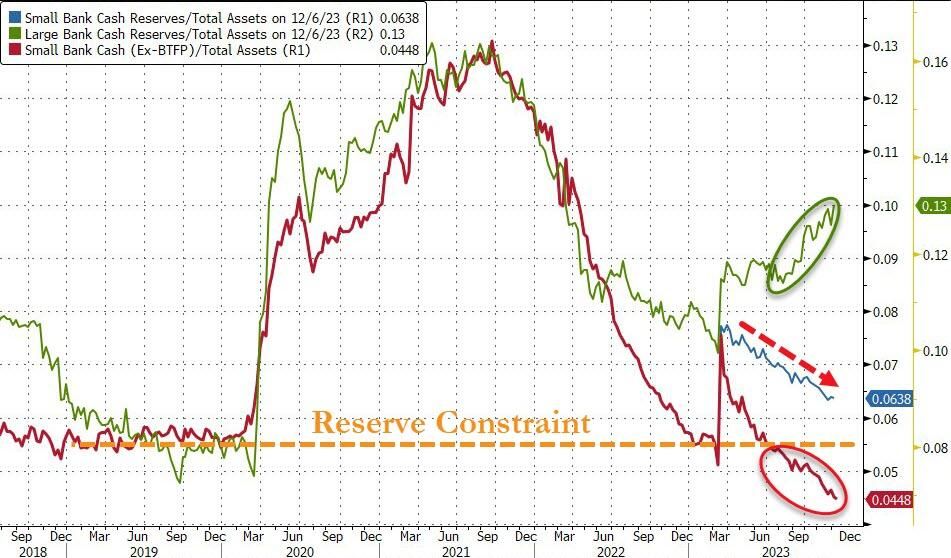

Small banks are suffering more than big banks.

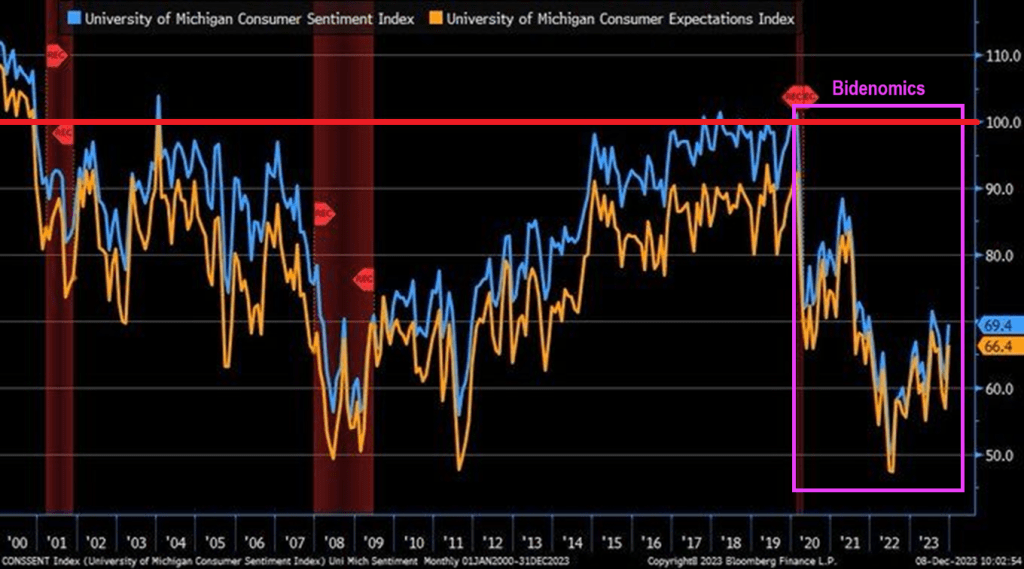

Consumer sentiment is below 70 (100 baseline) under Biden and Bidenomics.

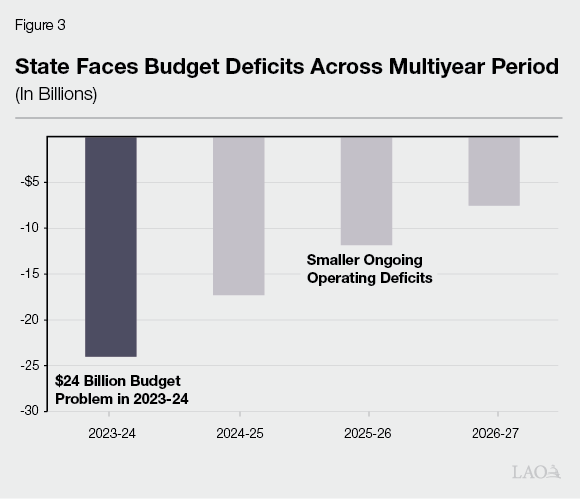

And then we have Gavin “Gruesome” Newsom and California. California is now facing a $68 billion deficit. It has also defaulted on a $20 billion loan from the federal government. The situation is so dire the state is telling agencies not to replace broken printers or re-stock office supplies. Workers are being stripped of benefits and could face furloughs. This is all happening as the state has spent billions funding High-Speed Rail and expanding Medi-Cal to all undocumented immigrants, while losing billions in tax revenue from people leaving the state.

$68 billion is over twice this forecast deficit of $24 billion.

But never fear. “Billions Biden” will make sure California is okay, ar least until the 2024 Presidential election.

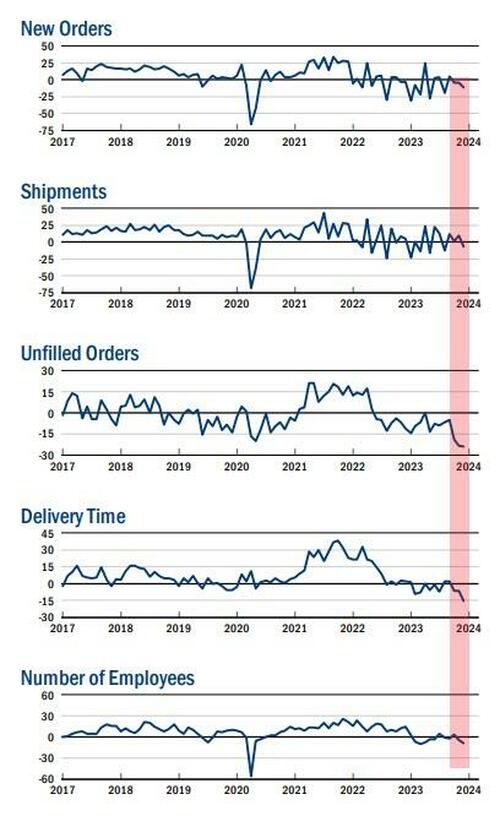

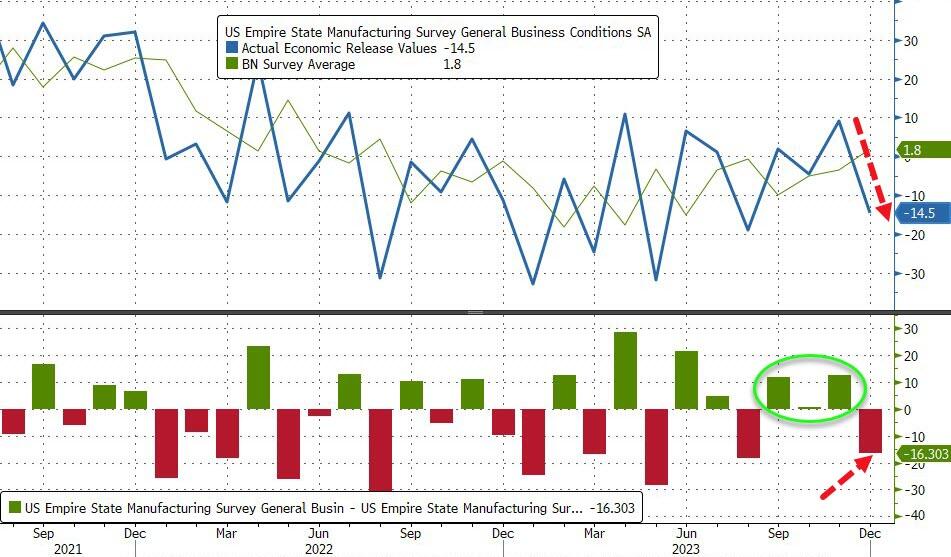

The drop takes the measure from ‘expansion’ at 7-month-highs to ‘contraction’ at 4-month-lows…

Source: Bloomberg

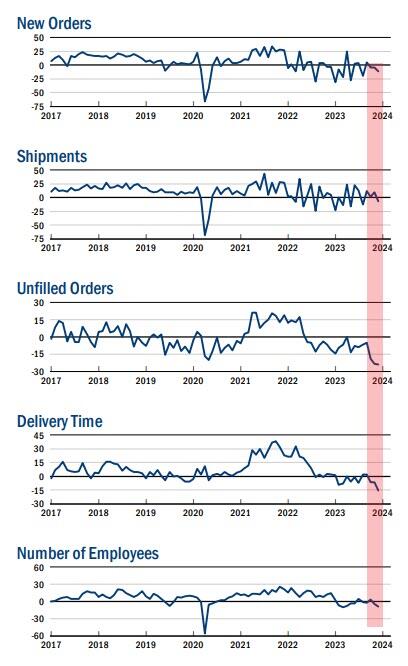

The new orders fell six points to -11.3, pointing to a decline in orders for a third consecutive month, and the shipments index fell sixteen points to -6.4, indicating that shipments fell.

The unfilled orders index held steady at -24.0, a sign that unfilled orders continued to fall significantly.

After rising into positive territory last month, the inventories index retreated fourteen points to -5.2, suggesting that inventories moved lower.

The delivery times index dropped ten points to -15.6, its lowest reading in several years, a sign that delivery times shortened.

The index for number of employees fell four points to -8.4, its lowest level in several months, pointing to a modest decline in employment levels.

On the bright side, the prices paid index moved down six points to 16.7, suggesting an ongoing moderation in input price increases, while the prices received index held steady at 11.5, a sign that selling price increases remained modest.

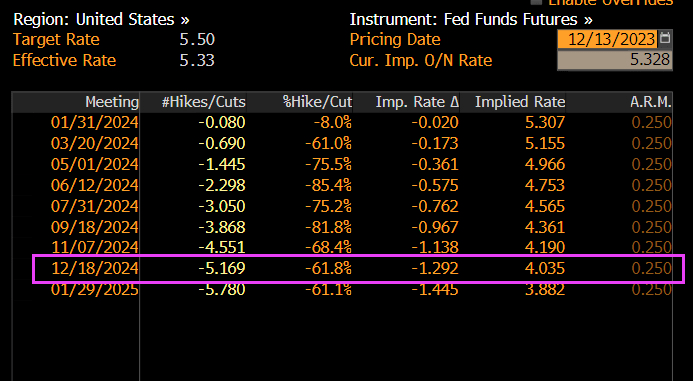

Is this the start of ‘soft’ data’s reversion to ‘hard’ reality?

The Fed – with its six rate-cuts – better hope so.

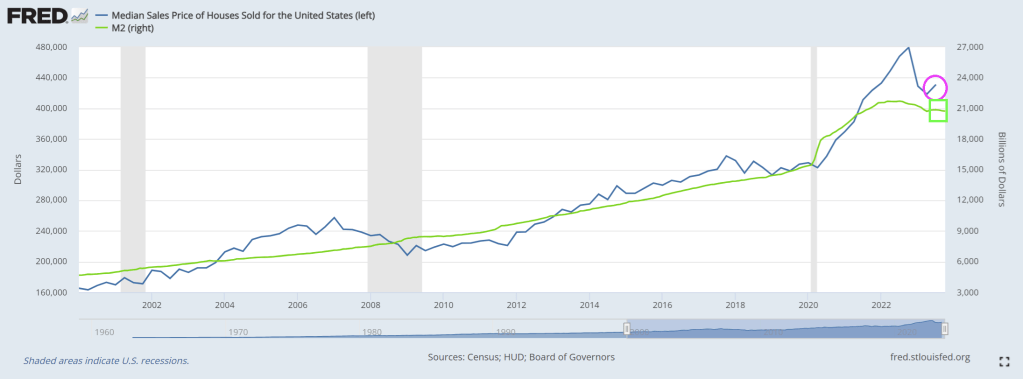

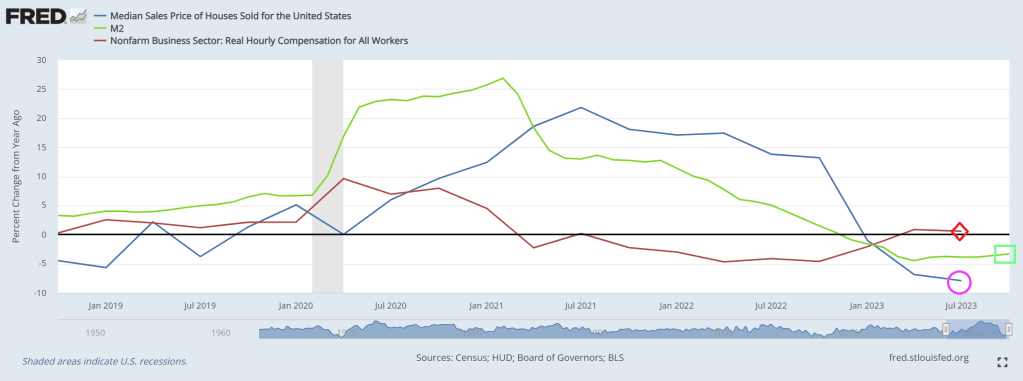

Median home prices are up a whopping 20% under Biden and his signature Bidenomics, growing the economy from the inside-out (?) instead of top-down. Excuse me Joe, Bidenomics is pure top-down Soviet-style economic planning. Markets be damned! The end result? Housing is far more expensive under Biden as are down payments.

If we look at year-over-year (YoY), we can see the burst of Covid-related spending and M2 Money growth (green line) that surged in 2020/2021. And rising home prices followed shortly thereafter. But as M2 Money growth slows, median home price growth declined into negative growth. The only factor that is positive is real hourly compensation (red line). But that is barely above 0%.

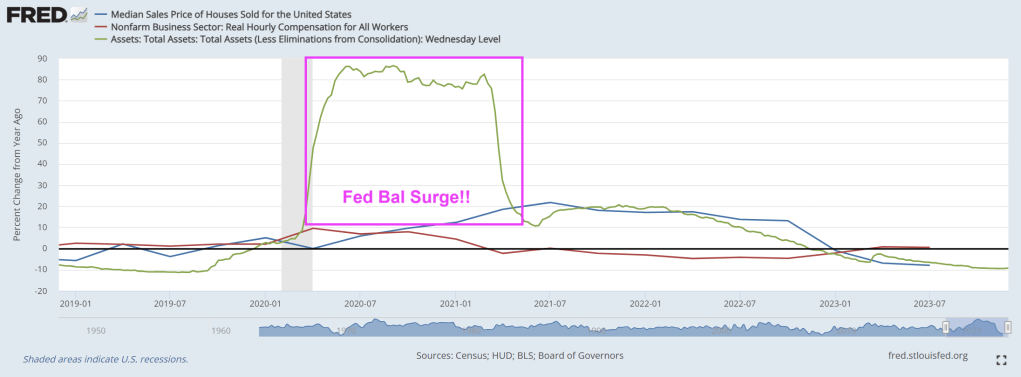

If we look at The Fed’s balance sheet surge (much like a storm surge), you can see the 2020/2021 overreaction to Covid and the various government shutdowns (along with school shutdowns).

The problem is that The Fed is shrinking their balance sheet like Biden shuffles. Maybe The Fed is following Biden’s lead: slow walking, incoherent messaging. And with the Fed storm surge of 2020/2021, Case-Shiller national home price index is up 33.2% under Bidenomics. Good luck with that down payment if you are renting and want to become a homeowner.

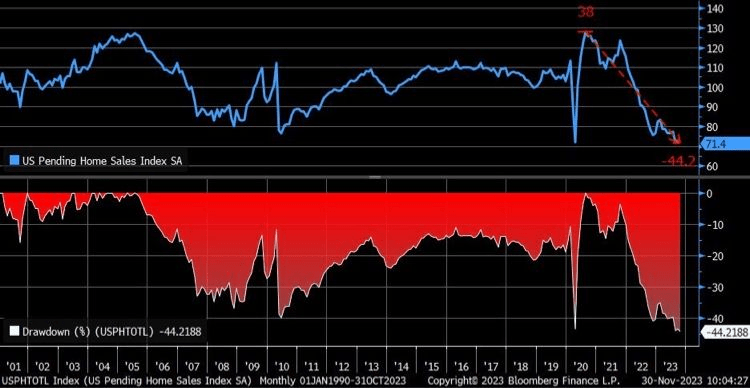

Pending home sales crash is showing why government usually fails to deliver sensible outcomes.

After all, Biden (and his overlord Obama) are truly addicted to gov solutions. Which means they are doomed to fail, as most government policies do.

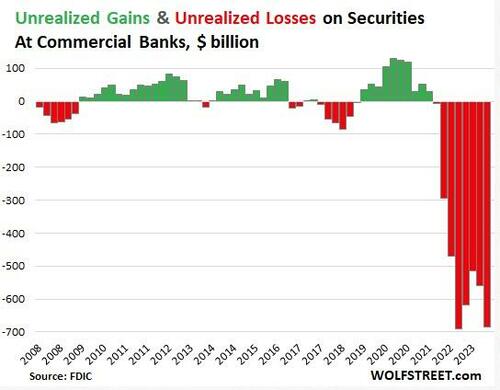

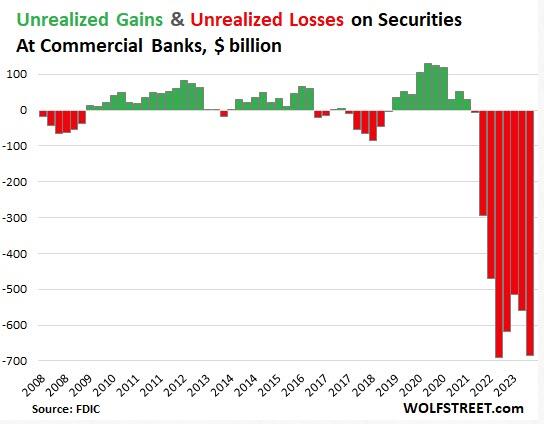

Unrealized losses on securities held by US banks exploded by 22% in the third quarter.

Of course, unrealized losses don’t really matter — until they do.

This is yet more evidence that the financial crisis that kicked off last March continues to bubble under the surface.

Unrealized losses, primarily on US Treasuries and mortgage-backed securities rose by $126 billion in Q3 and now total $684 billion, according to the FDIC’s quarterly bank data release.

Current unrealized losses are only slightly below the record set in the third quarter of 2022. This reflects the fact that the FDIC took over three failed banks earlier his year and ate their unrealized losses when it sold the banks’ assets, thus wiping them from the books.

Unrealized looses on securities are divided between two accounting methods.

Unrealized losses on held-to-maturity (HTM) securities jumped by $81 billion to $391 billion.

Unrealized losses on available-for-sale (AFS) securities jumped by $45 billion to $293 billion.

It’s important to understand these are only paper losses. Ostensibly, the banks will hold these bonds until maturity and then will be paid their face value. If it plays out this way, there won’t be any real losses.

The problem is that these unrealized losses drastically decrease a bank’s liquidity. If it has to sell bonds in order to raise capital, the bank will experience significant losses. This is exactly what took down Silicon Valley Bank last March.

Here’s what happened.

SVB sold a large portion of its bond portfolio at a $1.8 billion loss. At the time, SVB CEO Greg Becke said the bank made the sale “because we expect continued higher interest rates, pressured public and private markets, and elevated cash burn levels from our clients.”

The bank bought the bonds when interest rates were low. As a result, the $21 billion available for sale (AVS) bond portfolio was not yielding above cash burn. Meanwhile, rising interest rates caused the value of the portfolio to fall significantly. The plan was to sell the longer-term, lower-interest-rate bonds and reinvest the money into shorter-duration bonds with a higher yield. Instead, the sale dented the bank’s balance sheet and caused worried depositors to pull funds out of the bank.

WolfStreet explained more generally how these “irrelevant” unrealized losses can suddenly become relevant.

Banks, via a quirk in bank regulations, don’t have to mark these securities to market value, but can carry them at purchase price. The difference between market value and purchase price is the ‘unrealized gain or loss’ that the bank must disclose in its quarterly financial filings, so that we the depositors can see them and get spooked by them and yank our money out, us billionaires and centimillionaires first, on the two fundamental principles of investing: 1, he who panics first, panics best; and 2, after us the deluge.”

The Federal Reserve set up a bailout program to allow banks to deal with this problem. Instead of selling bonds at a loss, cash-strapped banks can go to the Fed’s Bank Term Funding Program (BTFP) and borrow against them “at par” (face value). This allows banks to use these undervalued assets to raise cash (at least temporarily) without realizing big losses on their balance sheets.

As unrealized losses rise, banks continue to tap into this bailout program more than nine months after the crisis kicked off.

In effect, the Fed managed to paper over the financial crisis with this bailout program.

It basically slapped a bandaid on it. But it has not addressed the underlying issue – the impact of rising interest rates on an economy and financial system addicted to easy money.

Remember, the US is on the cusp of a REAL recession, thank to Bidenomics.

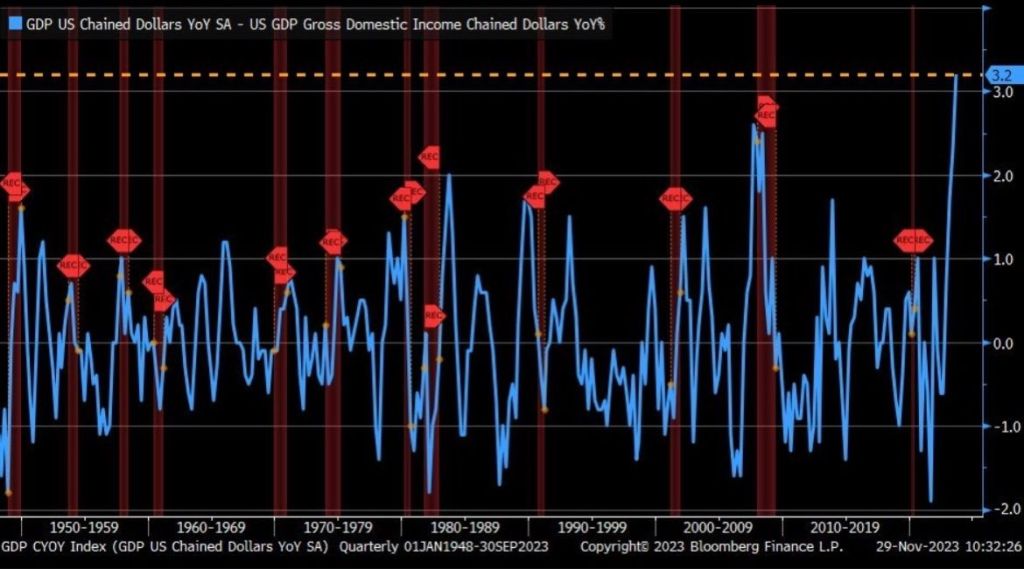

The spread between real GDP and real Gross Domestic Income (GDI) just hit an all-time high. Even higher than The Great Recession of 2009.

Might as well have AC/DC’s Angus Young as US Treasury Secretary instead of tone-deaf Janet Yellen.

The benchmark small cap index, the Russell 2000, has hit the lowest levels since November 2020, when the world was still without a vaccine and shut down from Covid. And before Biden’s/Congress wild spending spree and debt volume explosion creating massive inflation causing The Fed to hike rates.

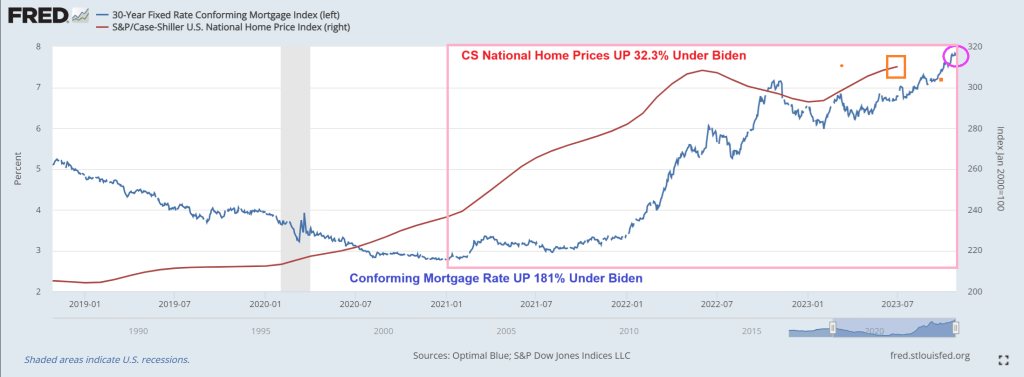

Speaking of over, under, sideways, down under Bidenomics, mortgage rates are up 181% and home prices are up 32.3% under Biden.

Bidenomics is a windfall for the donor class (high rate of return on campaign contributions) while the middle class gets beaten to a pulp. Waiting for Biden to lean over and creepily whisper “It’s working!” Even though it is clearly not working, at least for the middle class.

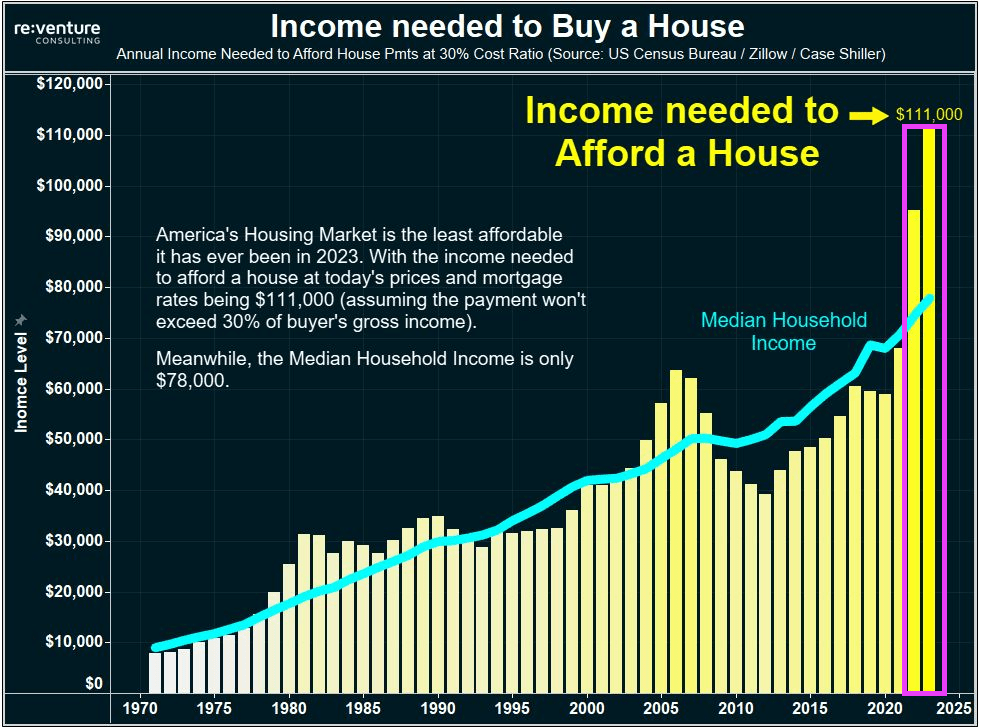

Evidence that Bidenomics is not working and destructive? Try the surging income needed to buy a house under Biden. Home prices are rising faster than median household income. As in $111,000 income needed to buy a house, while median household income is only $78,000. So, housing is simply unaffordable under Bidenomics. The Biden era is outlined in pink.

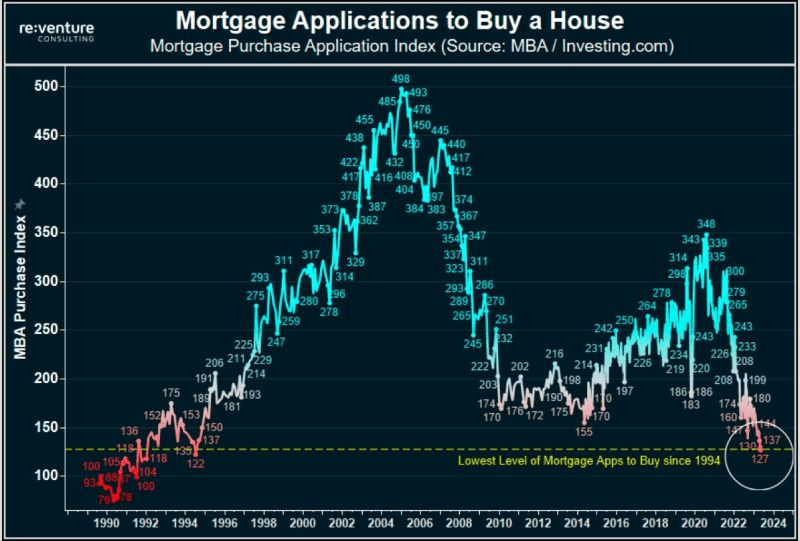

Mortgage purchase applications have collapsed to 1994 levels.

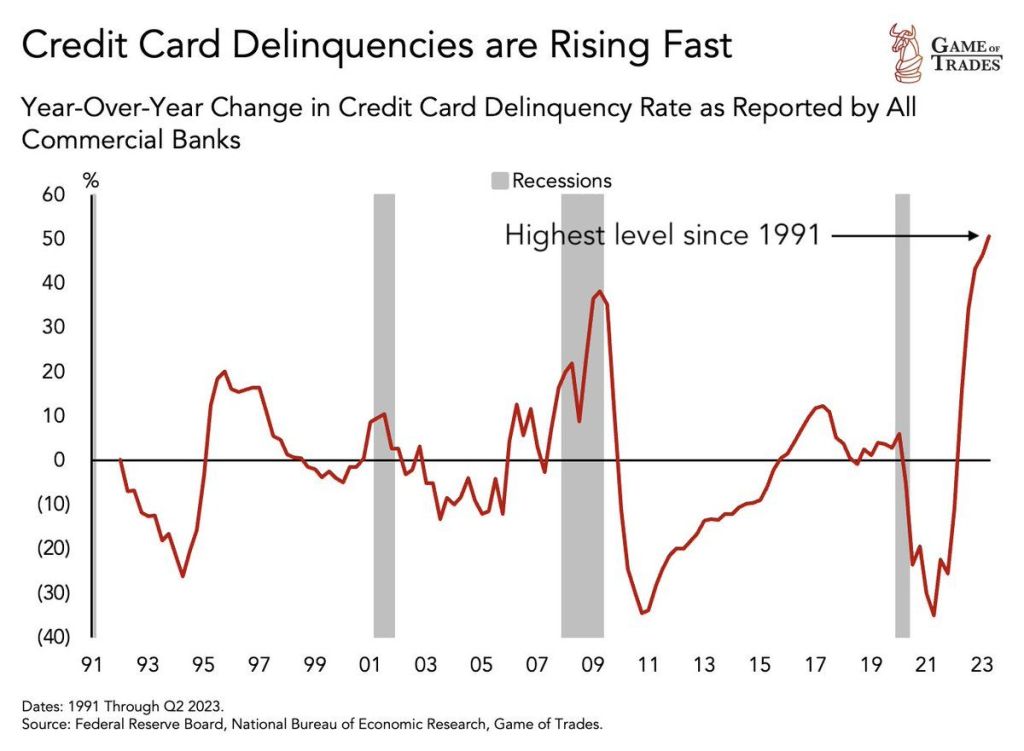

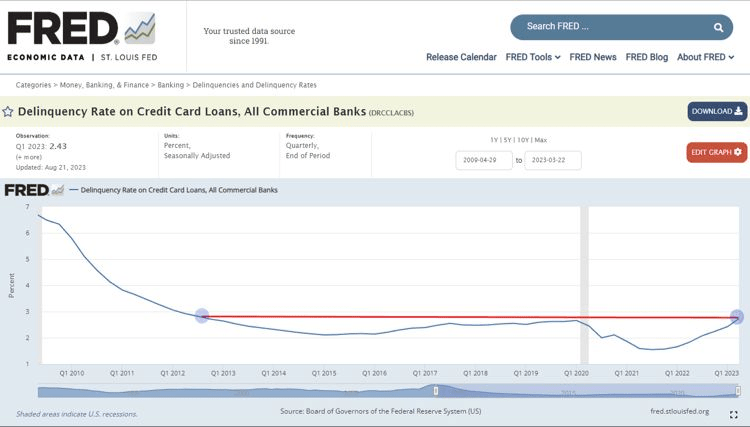

Meanwhile, stressed households are seeing credit card delinquencies at the highest level since 1991.

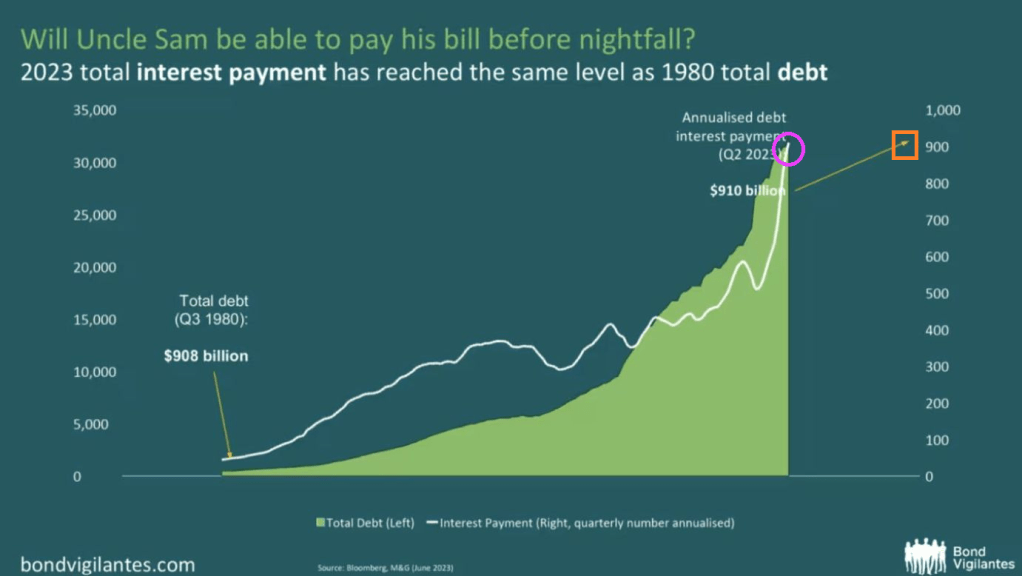

And thanks to Uncle Spam (given how Uncle Sam is destroying the middle class it is now Uncle Spam), 2023 interest payments are the same as the total debt from 1980! Spam, which the Federal government has devolved into, is very high in fat, calories and sodium and low in important nutrients, such as protein, vitamins and minerals.

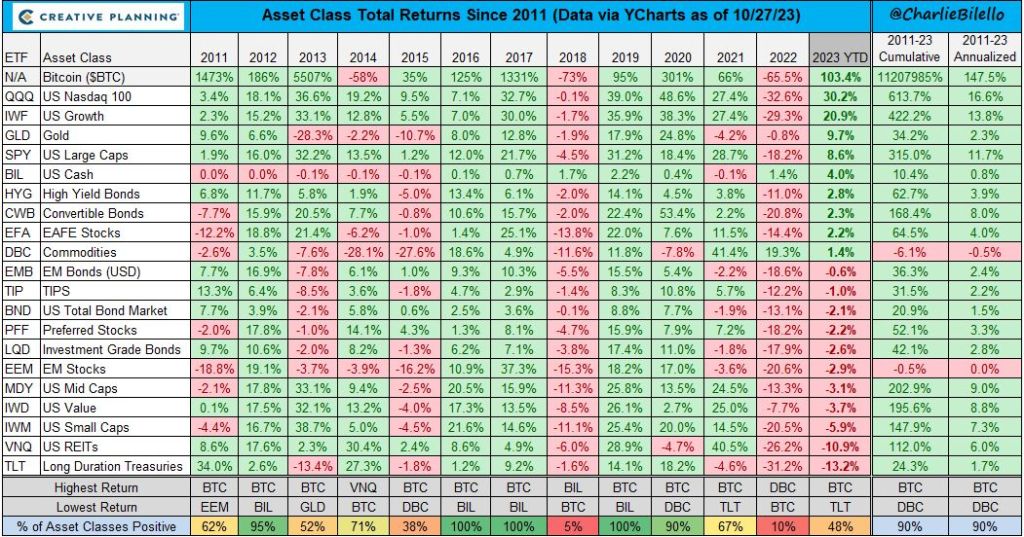

2022 was a bad year for investments under Bidenomics. 2023 year to date is showing huge gains for Bitcoin, the NASDAQ and gold. Bringing up the rear are long duration Treasuries and REITs (real estate investment trusts), both earning negative returns thus far of less than -10%.

As Bidenomics fails to do anything other than make big donors wealthier (green energy companies, big tech and union bosses, etc), we are seeing the impacts of Fed monetary tightening to combat inflation caused by Biden/Pelosi/Schumer’s spending spree.

First, the 10-year REAL Treasury yield is close to breaching 2%.

Second, 30-year mortgage rates are now 7.62%, up over 150% under Bidenomics.

Third, mortgage purchase applications crashed to the lowest level since 1995.

Fourth, the 2-year Treasury yield just breached 5%.

Fifth, the 10Y-2Y yield curve remains deeply inverted.

Speaking of Bidenomics, US mortgage purchase demand just declined to the lowest level in 28 years.

Mortgage applications decreased 2.9 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending September 1, 2023.

The Market Composite Index, a measure of mortgage loan application volume, decreased 2.9 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index decreased 5 percent compared with the previous week. The Refinance Index decreased 5 percent from the previous week and was 30 percent lower than the same week one year ago. The seasonally adjusted Purchase Index decreased 2 percent from one week earlier. The unadjusted Purchase Index decreased 5 percent compared with the previous week and was 28 percent lower than the same week one year ago.

This is not good.

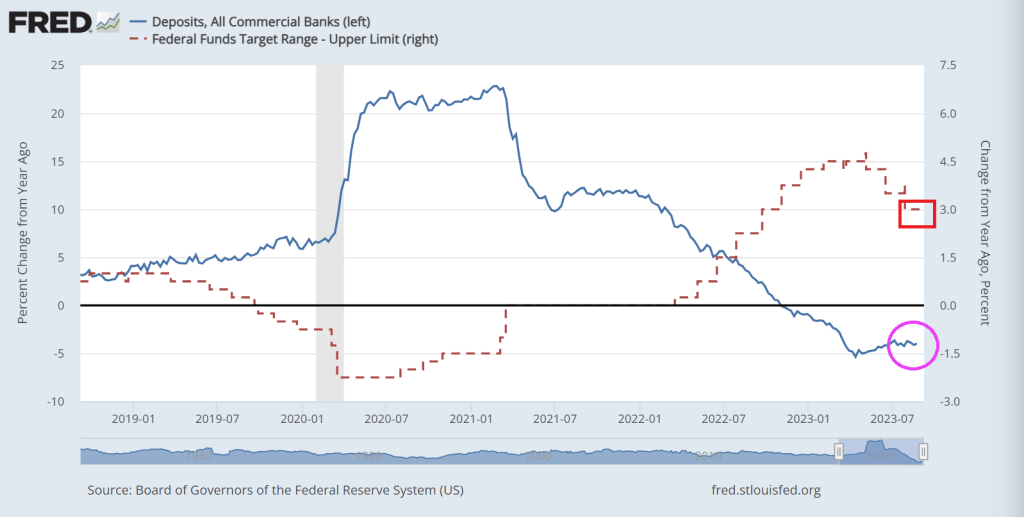

Bank deposits, a source of bank lending, are down -4% YoY as The Fed tightens rates.

Here is Lefty Frizzell’s original version of the Bidenomic’s themesong “If you’ve got the money, honey,I’ve got the time.” Like big donors receiving green energy subsidies. But not middle class mortgage borrowers.

Thanks to Bidenomics, code for massive Federal spending on green energy initiatives and payoffs fo large donors, we have agonizing inflation and consumers are borrowing more and more to cope with inflation. And with the increased use of debt comes …. drumroll … delinquenices!

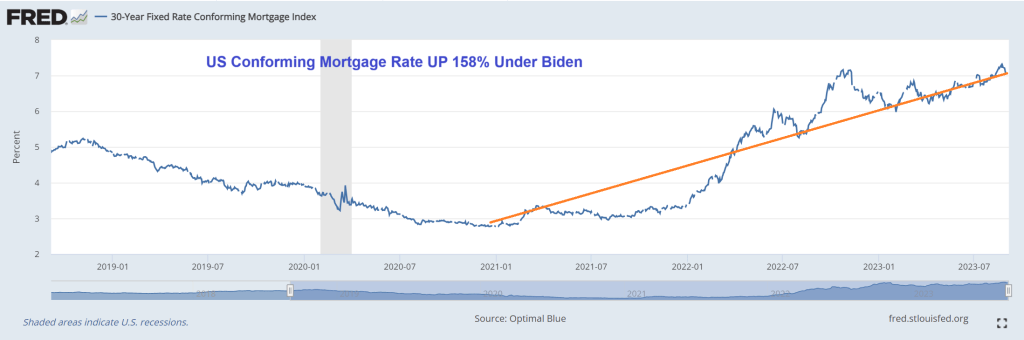

The US conforming mortgage rate is UP 158% under Bidenomics.

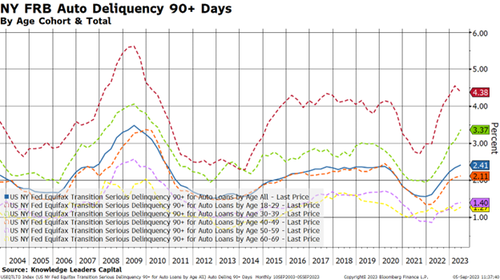

Let’s move on to some forms of consumer loans, where the story is a little more daunting.

Auto loans are definitely the epicenter of the credit cycle. While the overall average is a still somewhat tame 2.41%, younger borrowers are not keeping up. Younger borrowers have delinquency rates that are 1-2% higher than the average while the inverse is true for older borrowers. Eighteen-to-thirty-nine year-old borrowers have the highest delinquency rate in 13 years.

Somehow, I sense that used car lots are going to start filling up again as these vehicles get repossessed. This should put downward pressure on used car prices, bringing that element of inflation down. This is one of the channels through which monetary policy works.

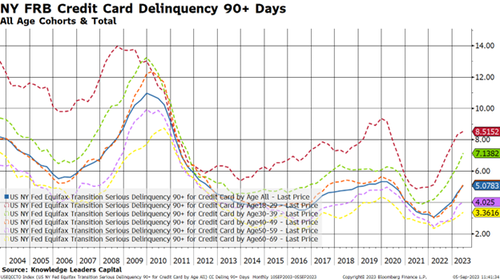

Lastly, I’ll take a look at credit card delinquencies.

Here is where we can really see the stresses building.

First, the overall delinquency rate has about doubled from 2.5% to 5% over the last couple years.

Second, older borrowers have seen a tick up in delinquency rates, a feature we don’t really see in other credit products.

Third, one in 12 younger 18-29 year-old borrowers are 90+ days late making their credit card payments.

Credit Card Delinquency Rate across all commercial banks hit 2.77% in the 2nd quarter, the highest level in more than a decade.

In conclusion, we are in the early days of a consumer credit cycle. Younger borrowers are the weakest link in this analysis, and this makes me wonder where rates go when student debt payments turn back on at the end of the month.

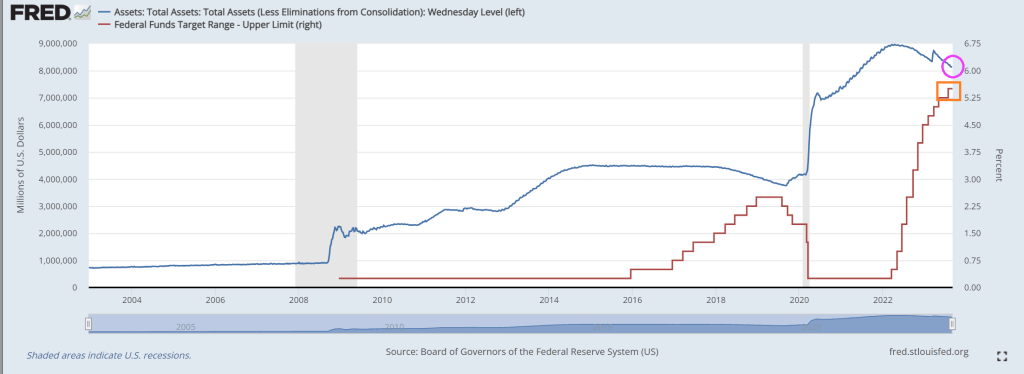

Soviet Joe Biden, who is a believer in Soviet-style command economies where rather than rely on free market capitalism, we now have CC (Crony Communism) running the US economy. Into the ground. But in the tradition of bad Federal policiies, Soviet Joe and Energy Secretary Granholm (with help from Congress) mandate green energy transition at all costs, watch the auto industry suffer, then bail them out. Sounds a lot of like the banking crisis of 2008 where The Federal government pushed homeownership until it helped almost collapse the banking sector, then the Federal government bailed out the banks. Rinse, repeat, bailout. And the bailout of banks in going! (Notice that The Fed has barely shrunk its $8+ trillion balance sheet!).

Automakers are looking to finish the week with strength after it was announced on Thursday that the Biden administration would be making “up to $12 billion” available to retrofit facilities to make both EVs and hybrids.

The money will include $10 billion from a US Energy Department loan program for clean vehicles and an additional $3.5 billion in financing to expand domestic battery manufacturing, according to Bloomberg.

The United Auto Workers, currently in negotiations with Detroit, has argued that a shift to EVs will cost the industry union jobs. US Energy Secretary Jennifer Granholm said on Thursday that the funding would help Detroit retain workers.

However, we’ve seen this “bailout” business model to save jobs before – at banks and during Covid, to name two examples – and it always winds up turning into a company cash grab before ultimately firing workers regardless. The UAW will try to prevent such a situation from taking place as it negotiates.

UAW President Shawn Fain “cautiously” welcomed the news after warning earlier this month that the White House should not push an EV agenda if it means the loss of jobs in Detroit.

Almost like the government should stay out of the auto industry as a whole, right? But that would make too much sense.

“The EV transition must be a just transition that ensures auto workers have a place in the new economy,” Fain said this week. Meanwhile, the Alliance for Automotive Innovation, a Washington lobby group that represents most Detroit automakers, said this week the funding “will further advance the domestic automotive supply chain and globally competitive battery manufacturing platform that automakers have already made sizable investments.”

Instead, Bloomberg calls the move the Biden administration “doubling down on efforts to support carmakers’ transition to EVs”. In a statement this week, President Biden said: “This funding will help existing workers keep their jobs and have the first shot to fill new good jobs as the car industry transforms for future generations.”

The Biden administration continues to aim for half of all vehicles on the road being EVs by 2030.

Oh and now that UAW Boss seeks 46% raise and 32-hour work week. Reminds me of Federal student loans where students run up massive amounts of debt to major in useless degrees like political “science” and gender/race studies, yet universities hire more admininstrators.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

You must be logged in to post a comment.