Get ready! The mad dash for metals is here!

- Copper set to be most valuable opportunity in race to net zero

- Electric vehicles and wind turbines are main demand drivers

Everything is a race when it comes to the energy transition. A race against time to reach net-zero emissions by the 2050 crunch point; a race to build enough wind turbines and replace gas-guzzling cars with electric vehicles; a race between superpowers to shore up domestic supply chains and capture the economic benefits of decarbonization.

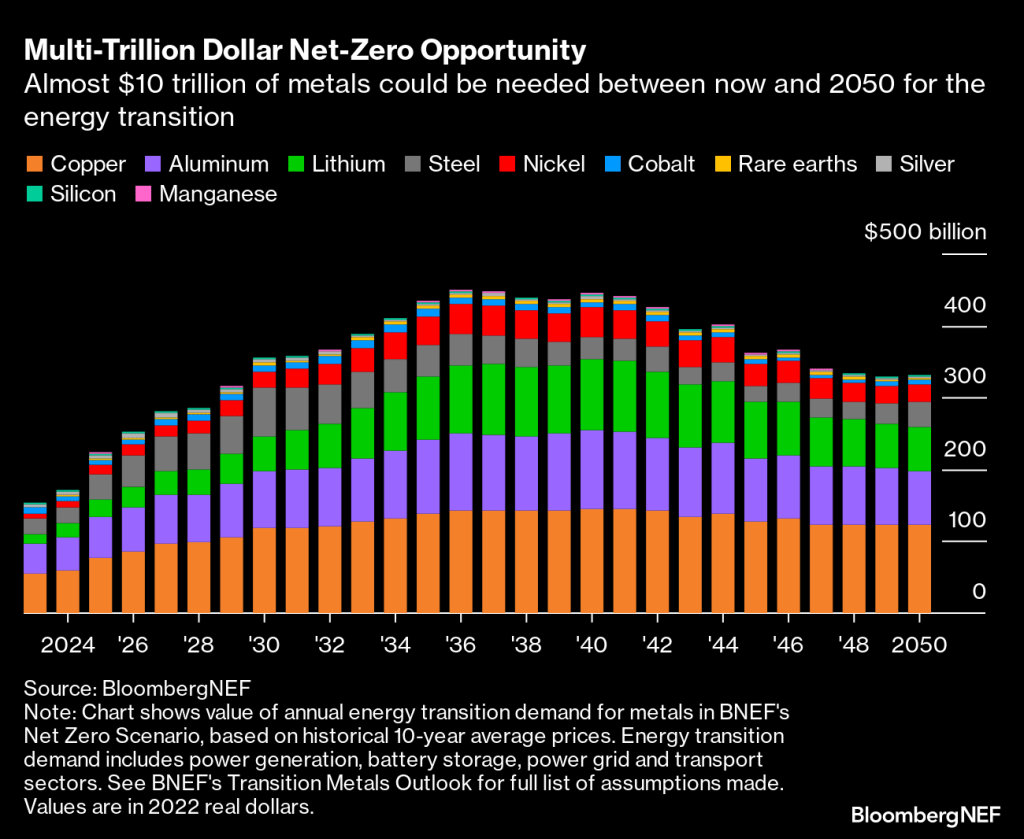

There’s one common thread that runs through them all: the need for metals. A greener future is impossible without copper to expand the world’s electricity grids, lithium for batteries and aluminum for solar panel frames.

Companies are now hunting for more direct access to these essential raw materials as they recognize metals will form the backbone of the energy transition. General Motors Co., for example, announced at the end of last month that it will invest $650 million in Lithium Americas Corp. and help develop the Thacker Pass mine in Nevada. The automaker is also reportedly competing to buy a stake in the base metals unit of mining giant Vale SA, according to Bloomberg News.

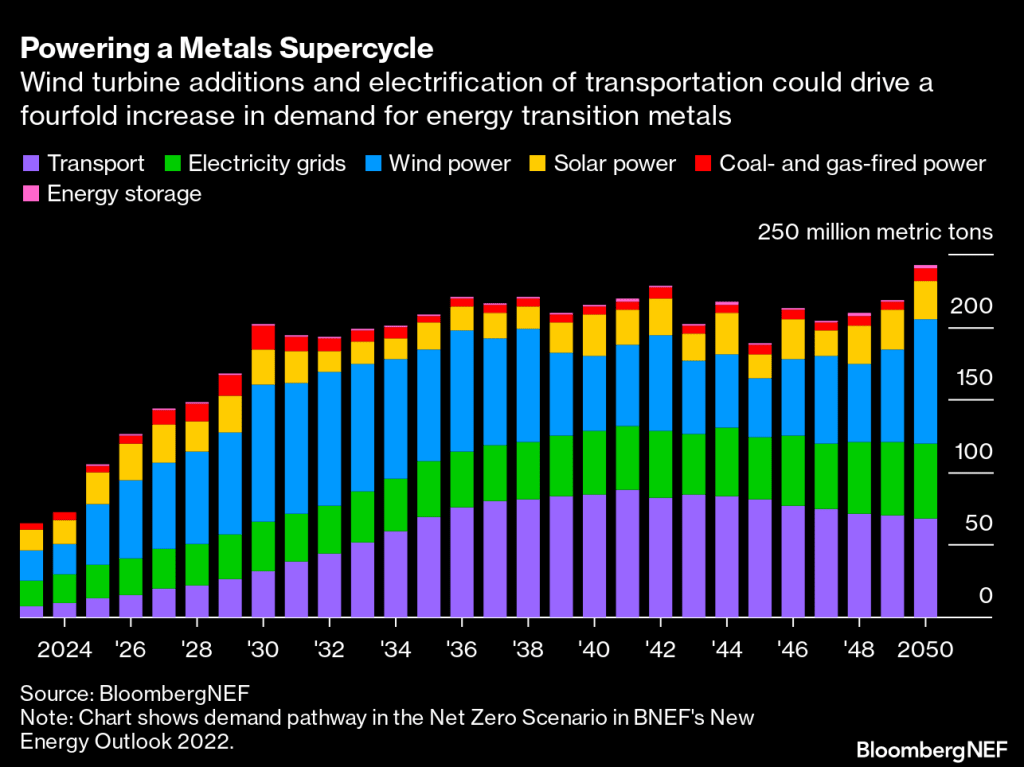

What exactly is driving this hunger for metals? Achieving a net-zero world will entail electrifying as much as possible. BNEF estimates the size of the global power grid will have to almost double to 152 million kilometers by 2050, requiring masses of steel, copper and aluminum. This means the expansion of grids will use the most copper out of all energy transition applications, coming in at 427 million tons between now and mid-century.

Clean electrons will need to flow through those grids, enabled by the scale-up of wind and solar power. Wind turbines are projected to consume the most metals overall by 2050 if the world gets on track for net-zero emissions. Today, steel accounts for nearly 90% of the materials used by weight in offshore wind and about 25% in onshore wind, although as turbines get bigger, they will use less steel on a per-megawatt basis. Consumption of rare earth metals such as neodymium will become more intense, however, as permanent magnet generators become more common in turbines.

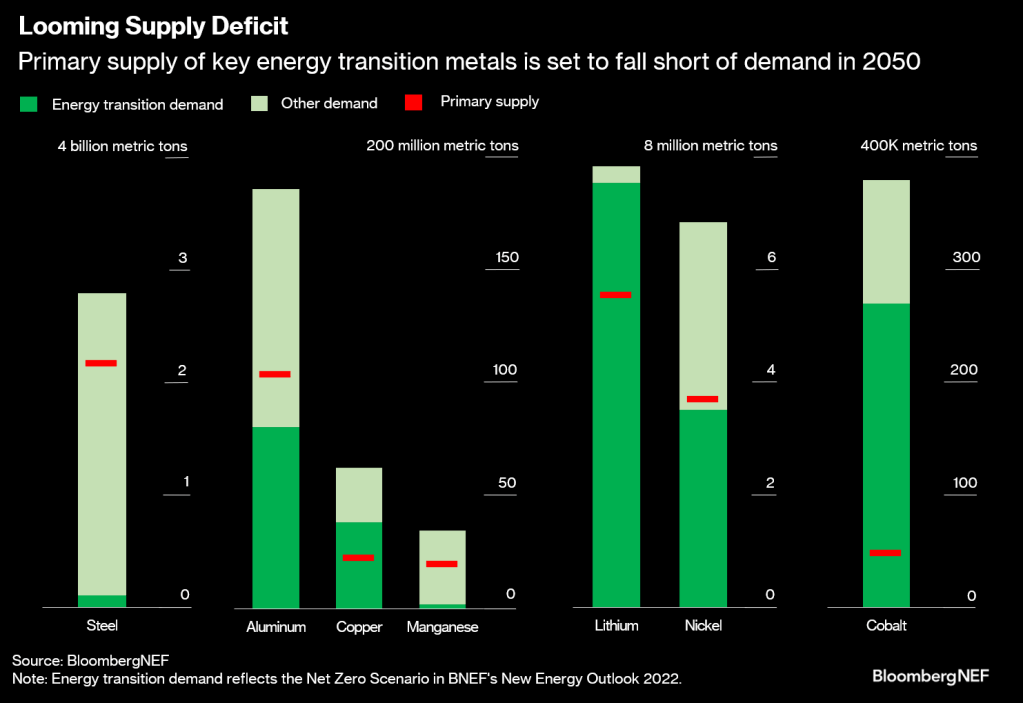

Rising demand for energy transition metals is essentially a given at this point. The real question is whether there will be enough supply. As things currently stand, lots of these metals, including copper and cobalt, are at risk of a shortfall in the coming decades unless current reserves can be supplemented with new geological discoveries and projects, and recycling of old material is stepped up.

Many countries have known resources of metals – in other words, natural occurrences of minerals in high concentrations and sufficient quantities. But not all of these resources have been turned into reserves that can be profitably mined yet. This requires time and investment to go through the exploration, discovery and feasibility stages, and these processes could be thwarted by policy.

Here are metals today.

So, people get ready! Whether you agree with green energy policies or not, it is where markets are headed. Personally, I am sticking to my gasoline guzzling cars until I am ordered not to drive them. Stated differently, if Joe Biden can drive a gas guzzling V-8 in a Chevy Corvette, why can’t I?

At least I didn’t leave classified documents in my garage.

You must be logged in to post a comment.