金融政策に限界があるとは考えておりません

(I do not believe that there is a limit to the effect of monetary policy.)

Haruhiko Kuroda, Bank of Japan, 13 April 2016

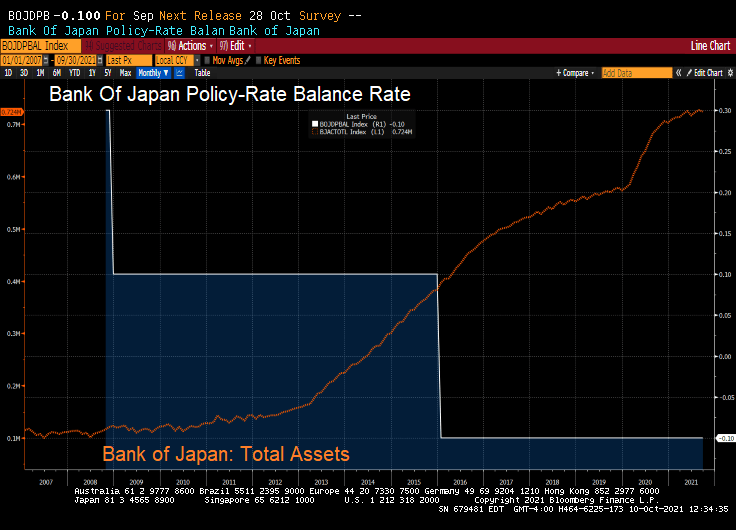

The Bank of Japan is one of the top three Quantitative Easing (QE) Monsters in terms of the absolute amount of assets it purchased. The Fed and the ECB round out the trio. The BoJ started QE over 20 years ago, and went hog wild under Abenomics, which became the economic religion of Japan in 2013. But the era of Prime Minister Shinzo Abe ended in September 2020, and Abenomics is now finished.

What’s left of it is that the BoJ (and Bank of Japan Governor Haruhiko Kuroda) now holds about half of the huge pile of the central government’s debt. With their target rate at -0.10% and a gargantuan balance sheet, what could go wrong?

But BOJ’s QE has ended. The BoJ’s overall assets stopped growing, and its holdings of government bonds have started to decline.

As of the BoJ’s balance sheet dated September 30, released on Thursday, total assets declined to a still monstrous ¥724 trillion ($6.4 trillion), below where it had been in May 2021.

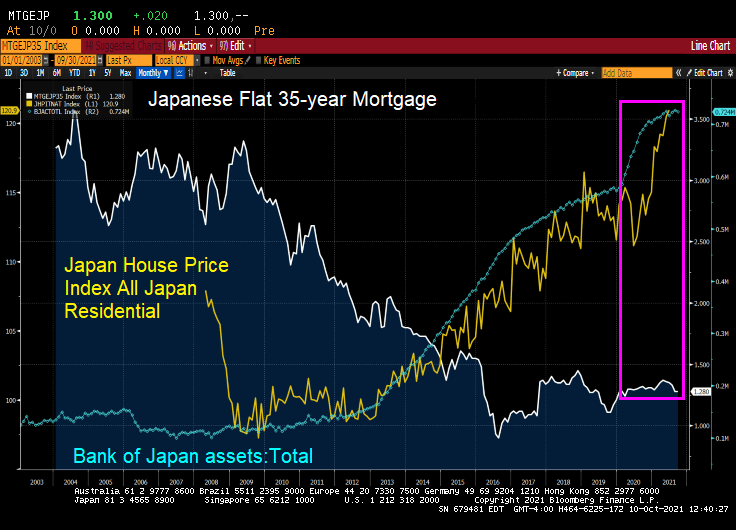

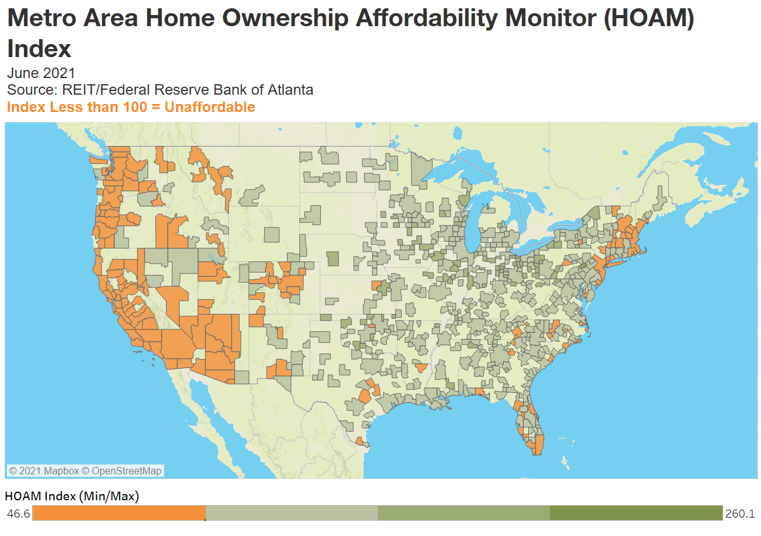

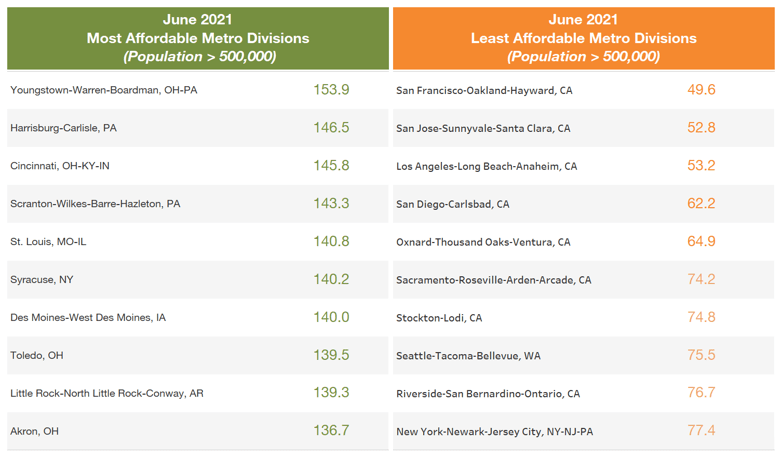

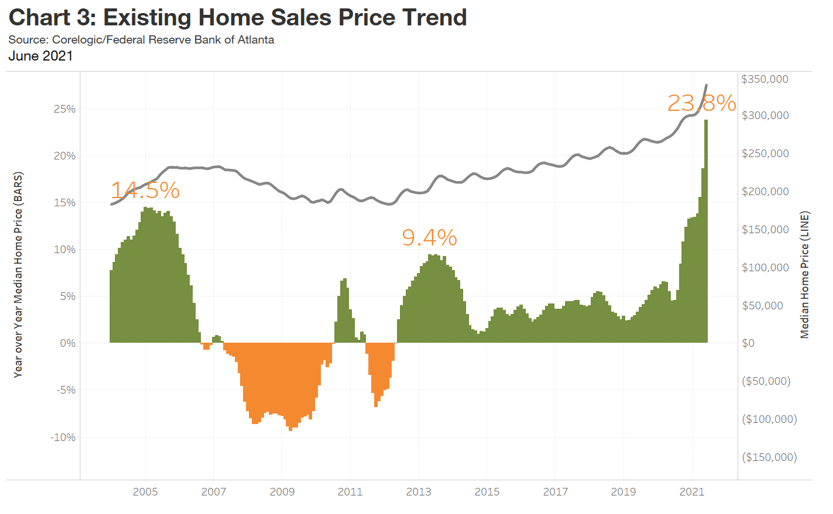

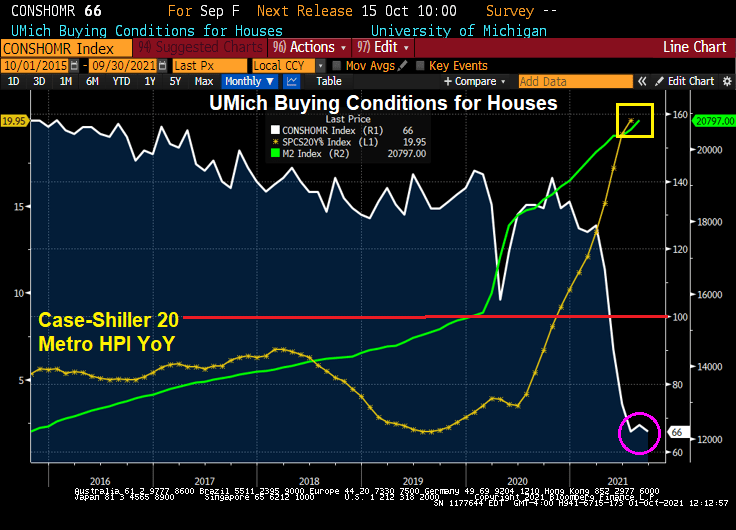

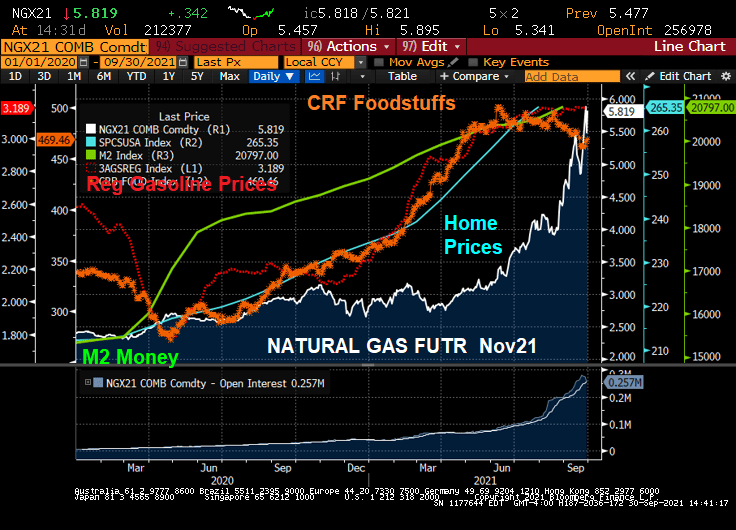

But look at Japanese home prices with the growth of the BOJ’s balance sheet and general decline in mortgage rates. Like the USA, there was a balance sheet spike associated with Covid and a resulting spike in home prices.

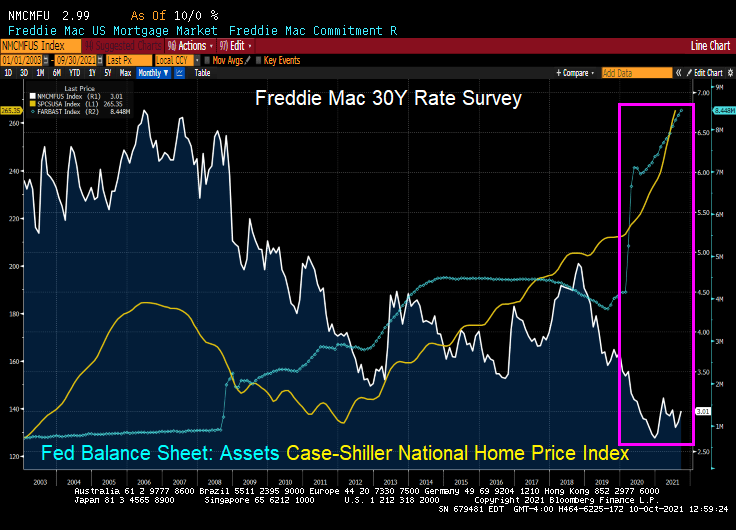

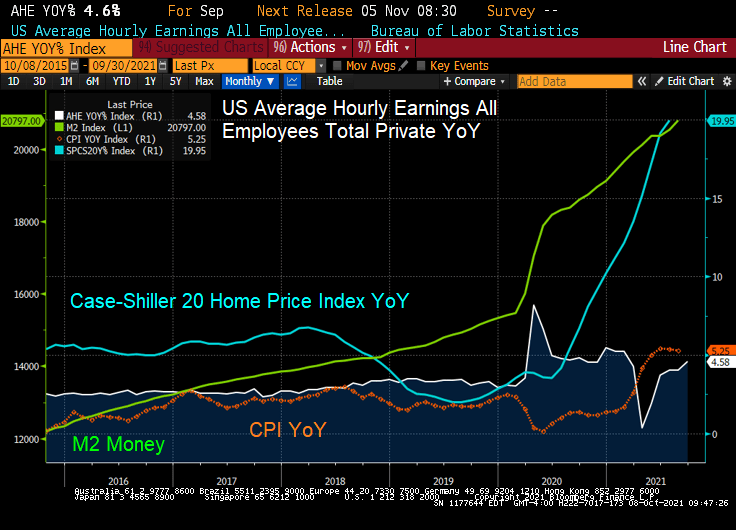

The USA? We also saw a surge in home prices following The Fed’s monetary “stimulypto.”

But will The Fed follow BOJ’s lead and stop asset purchases? Not yet, anyway. It seems that The Fed can’t turn market forces loose and let interest rates rise.

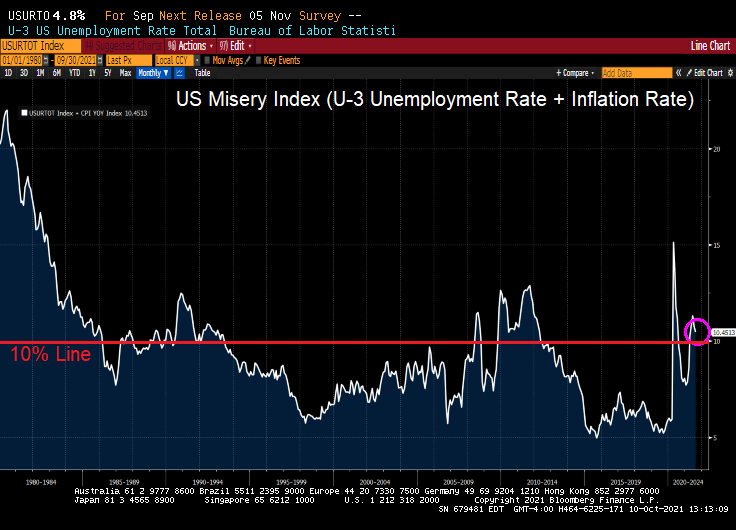

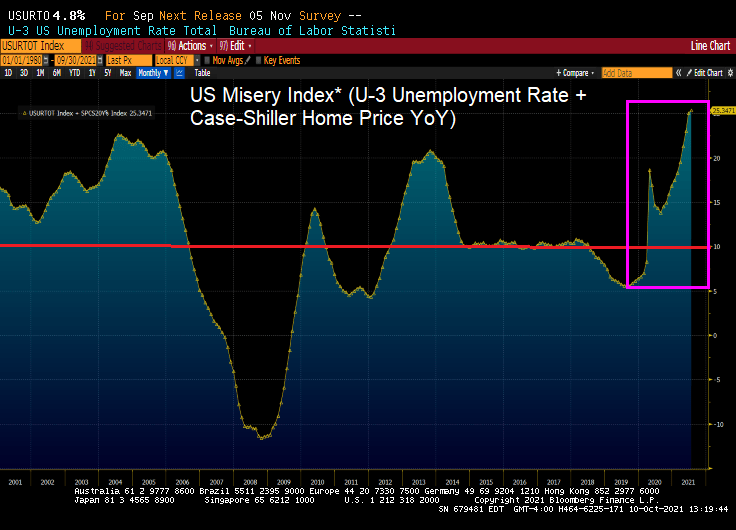

Bear in my that the US Misery Index is above 10% (U-3 unemployment + inflation).

And if I define the US Misery Index as U-3 unemployment + home price growth, we can see we are at record misery rates. Miserable for households that don’t own a home or are trying to move to a higher housing price area).

What I like about The Fed’s monetary policies?? Nada.

You must be logged in to post a comment.